Envirotech Vehicles appoints Jason Maddox to board of directors

Introduction & Market Context

Delek US Energy Inc (NYSE:DK) presented its second quarter 2025 earnings on August 6, highlighting significant improvements in operational performance despite reporting continued net losses. The company’s stock has shown resilience, trading at $21.07 as of August 5, 2025, well above its 52-week low of $11.03 but still below its high of $27.07.

The refiner has made substantial progress in its Efficiency and Optimization Plan (EOP), which appears to be driving improved results compared to the first quarter’s disappointing performance when the company reported a net loss of $173 million or -$2.78 per share.

Quarterly Performance Highlights

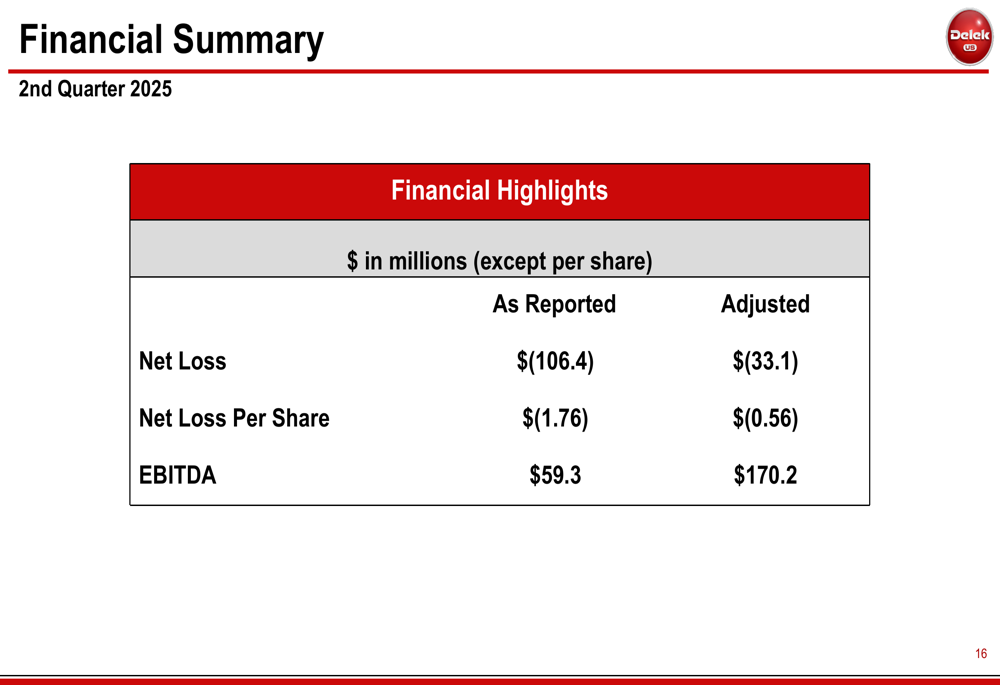

Delek reported a net loss of $106.4 million ($1.76 per share) for Q2 2025, with adjusted net loss of $33.1 million ($0.56 per share). Despite these losses, the company’s Adjusted EBITDA showed remarkable improvement, reaching $170.2 million compared to $107.5 million in Q2 2024 and just $26.5 million in Q1 2025.

As shown in the following financial summary from the presentation:

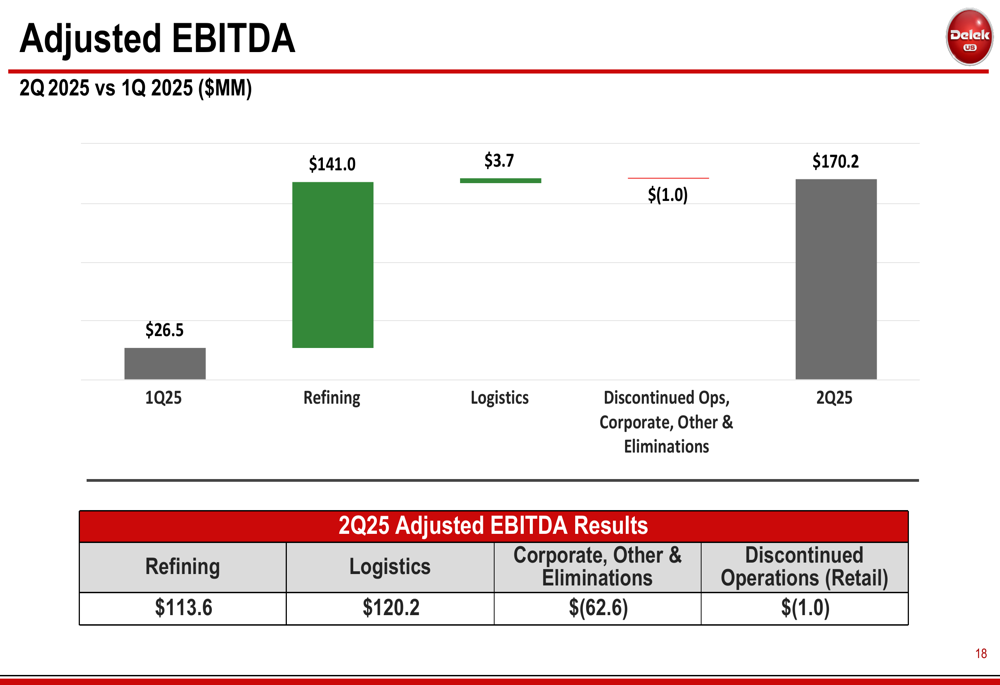

The refining segment led this improvement with a $71.5 million increase in EBITDA year-over-year, while the logistics segment contributed an additional $19.6 million. Total (EPA:TTEF) refining throughput remained stable at 316.3 thousand barrels per day (MBPD), marginally higher than the 316.0 MBPD in the same quarter last year.

The quarterly EBITDA improvement is clearly illustrated in this comparison between Q1 and Q2 2025:

Efficiency and Optimization Plan Progress

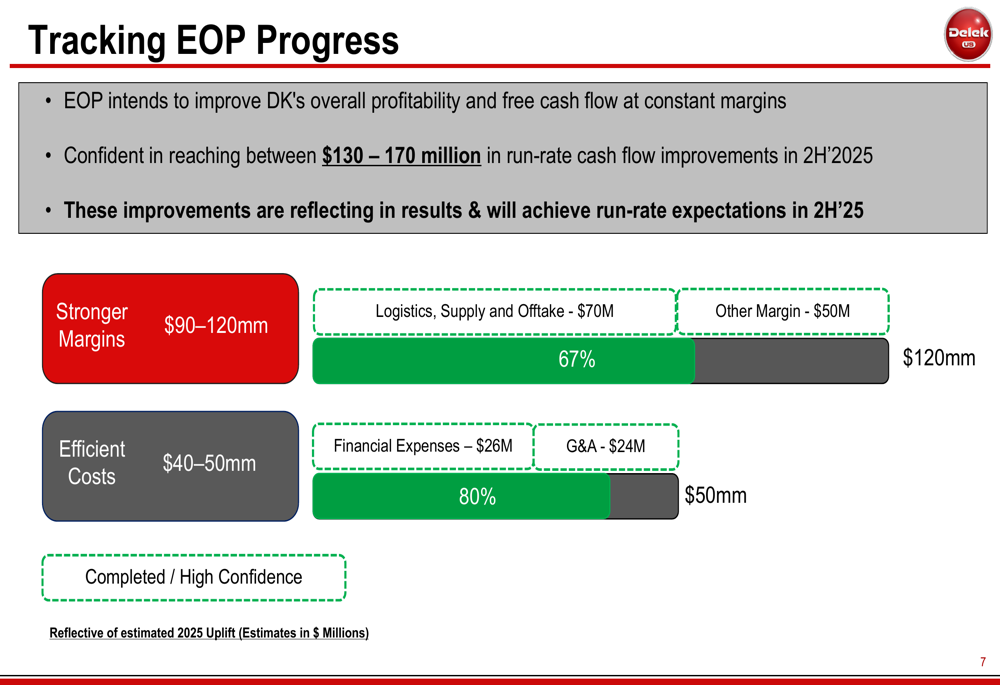

A central theme of Delek’s presentation was the progress of its Efficiency and Optimization Plan (EOP), which has now achieved a run-rate of $120 million in cash flow improvements during Q2 2025. Based on this success, management has raised the EOP target to $130-170 million in cash flow improvements.

The company provided a detailed breakdown of how these improvements are being achieved:

Approximately $30 million of cash improvements from the EOP flowed through to the P&L in Q2 2025. The plan focuses on two main areas: stronger margins ($90-120 million) and efficient costs ($40-50 million). The margin improvements come primarily from logistics, supply and offtake ($70 million) and other margin enhancements ($50 million), while cost efficiencies are derived from financial expenses ($26 million) and G&A reductions ($24 million).

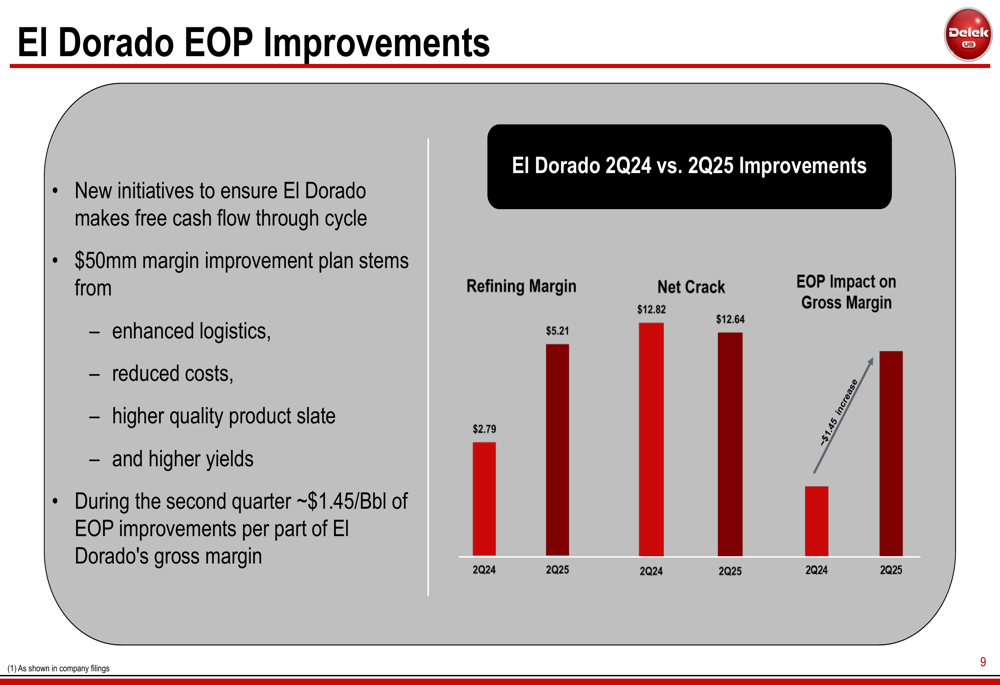

The El Dorado refinery has been a particular focus of the EOP efforts, with margin improvements helping to boost its performance:

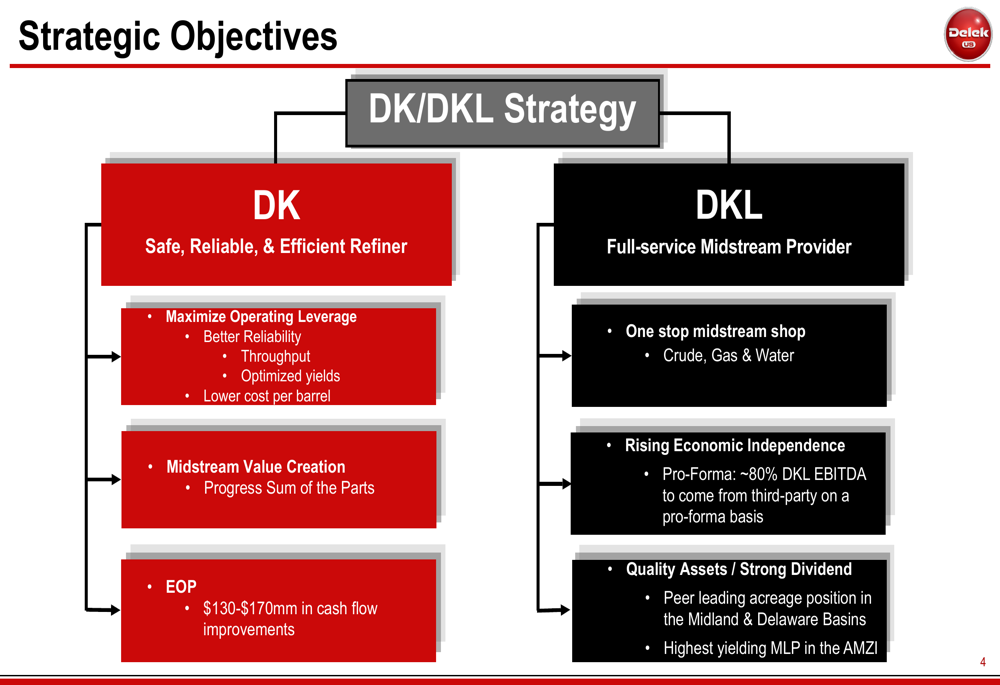

Midstream Strategy and Value Creation

Delek continues to emphasize its midstream strategy through Delek Logistics Partners (NYSE:DKL), which reported another record quarter and is on track to deliver 2025 EBITDA guidance of $480-520 million. The company proudly noted that DKL has achieved 50 consecutive quarters of distribution growth.

The strategic alignment between Delek US Energy and Delek Logistics is outlined in this flowchart:

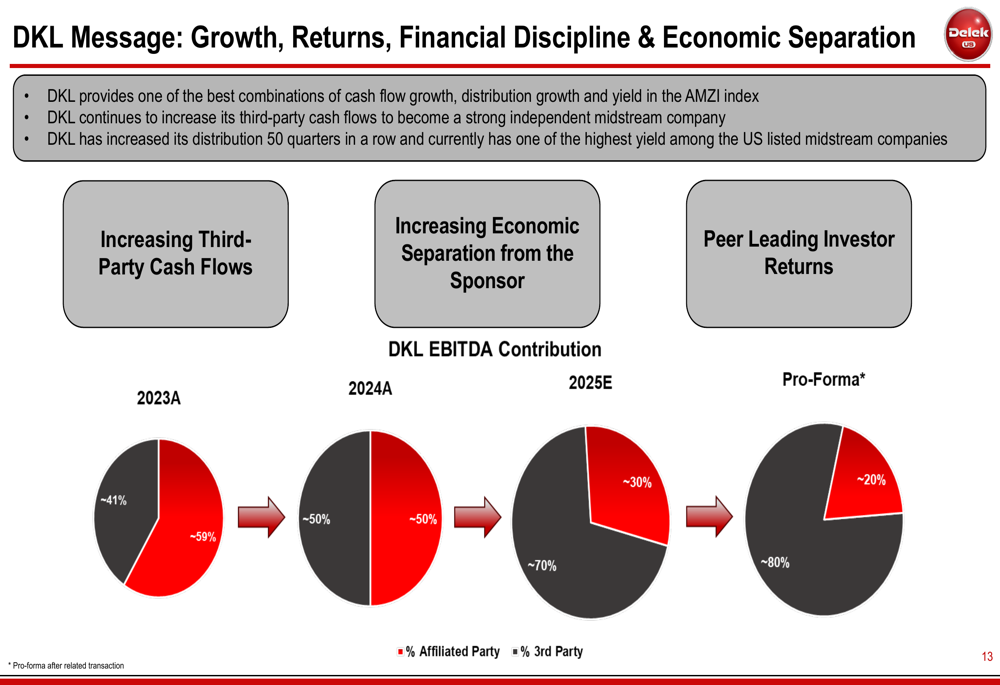

A key component of Delek’s strategy is increasing the economic separation between DK and DKL while realizing the full value of rising third-party DKL EBITDA. The company is pursuing several approaches to midstream value creation, including strategic combinations, DKL unit buybacks from DK, bolt-on acquisitions, and potential asset sales to capitalize on premium M&A multiples.

The progress in midstream value creation is illustrated in this chart showing the increasing contribution from third-party cash flows:

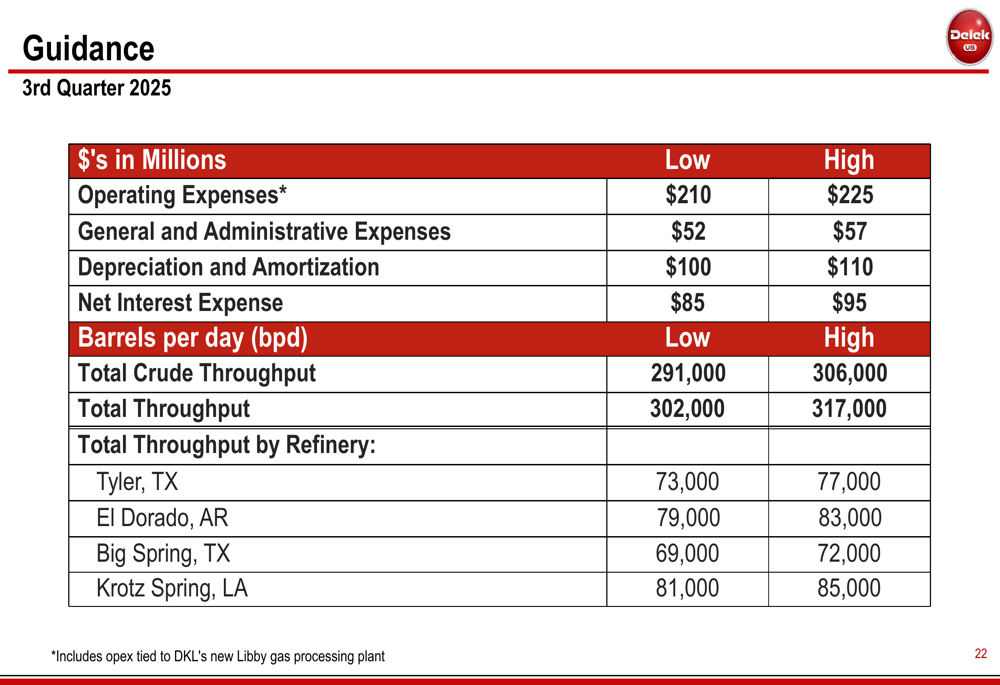

Forward-Looking Guidance

Looking ahead to Q3 2025, Delek provided guidance for key operational metrics. The company expects total crude throughput between 280-290 MBPD, with operating expenses ranging from $190-200 million and G&A expenses between $65-70 million.

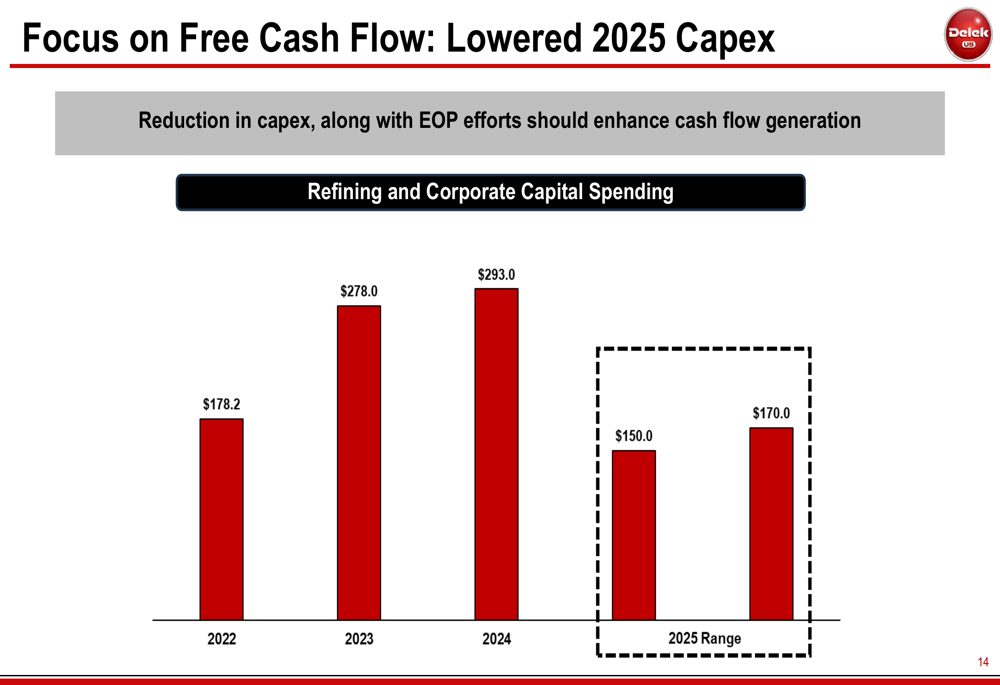

In a significant move to enhance free cash flow, Delek has lowered its 2025 capital expenditure forecast to $150-170 million, a substantial reduction from $293 million in 2024. This reduction, combined with EOP efforts, is expected to strengthen cash flow generation.

The company ended Q2 with a cash balance of $615.5 million, slightly down from $623.8 million at the end of Q1 2025. Management emphasized that the focus on free cash flow generation remains a top priority as they continue to implement their optimization initiatives.

While Delek continues to face challenges in achieving consistent profitability, the significant improvement in EBITDA and the progress of its efficiency initiatives suggest the company is moving in a positive direction. Investors will be watching closely to see if these operational improvements can translate into sustainable profitability in coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.