NVIDIA launches Jetson Thor robotics computers for physical AI systems

Introduction & Market Context

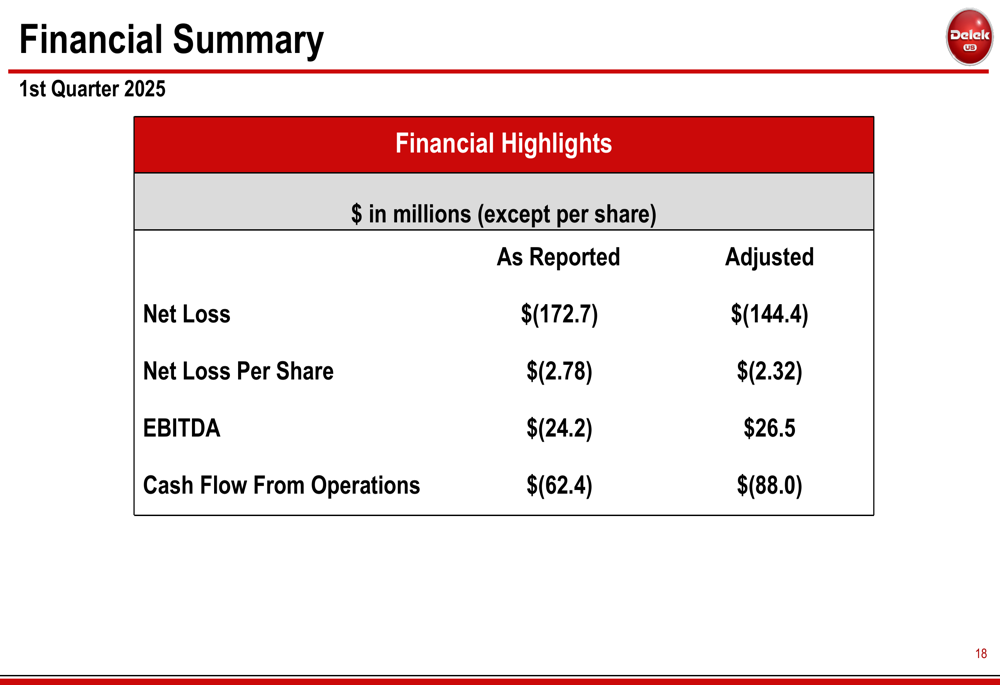

Delek US Energy Inc (NYSE:DK) released its first quarter 2025 earnings presentation on May 7, revealing continued financial challenges despite ongoing strategic initiatives. The company reported a net loss of $172.7 million, or $2.78 per share, as refining margins remained under pressure. Despite these disappointing results, Delek’s stock has shown resilience, trading at $14.06 in premarket activity, up 0.21% following the earnings release.

The quarter’s performance reflects a challenging operating environment for refiners, with Delek’s results continuing a trend of losses after reporting a $414 million net loss in Q4 2024. However, the company emphasized progress on its Enterprise Optimization Plan (EOP) and midstream value creation efforts as key pillars for future improvement.

Quarterly Performance Highlights

Delek’s Q1 2025 financial results showed significant weakness, with an adjusted net loss of $144.4 million, or $2.32 per share, compared to a loss of $26.2 million, or $0.41 per share, in the same period last year. Adjusted EBITDA fell dramatically to $26.5 million from $158.7 million in Q1 2024.

The following chart summarizes the company’s key financial metrics for the quarter:

The refining segment was particularly weak, generating negative EBITDA of $27.4 million, while the logistics segment through Delek Logistics Partners (NYSE:DKL) continued to perform well with EBITDA of $116.5 million. Total (EPA:TTEF) refining throughput for the quarter was 289.2 thousand barrels per day (MBPD), slightly down from 296.7 MBPD in Q1 2024.

Strategic Initiatives

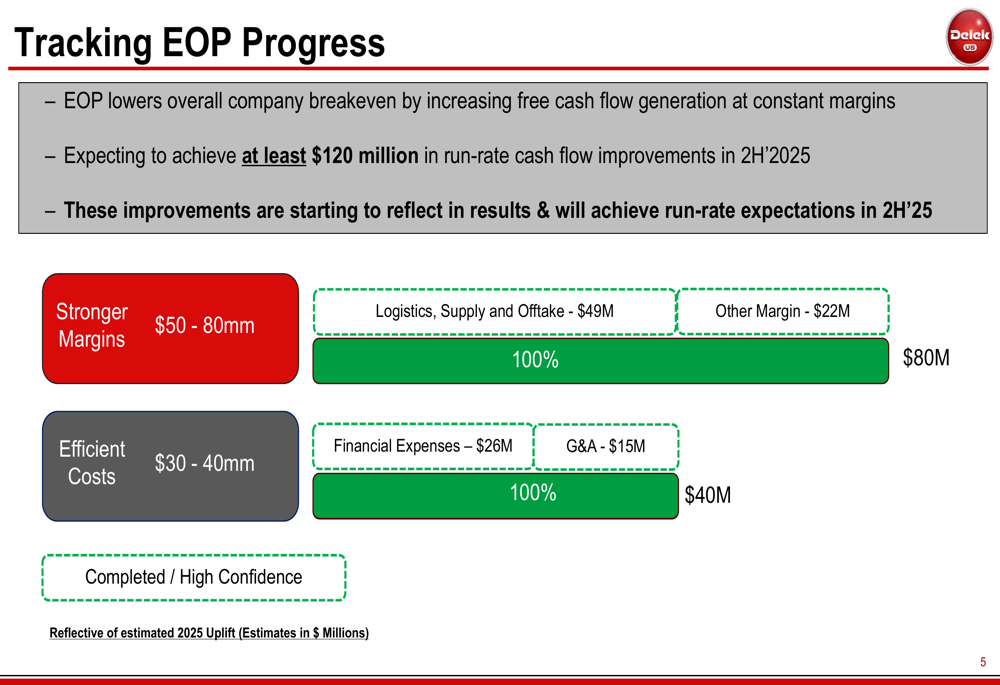

Delek continues to emphasize its Enterprise Optimization Plan, which aims to deliver at least $120 million in cash flow improvements by the second half of 2025. The company reported significant progress on this initiative, with completed or high-confidence projects across both margin improvement and cost efficiency categories.

As shown in the following chart detailing the EOP progress, Delek has identified specific initiatives to improve margins by $50-80 million and reduce costs by $30-40 million:

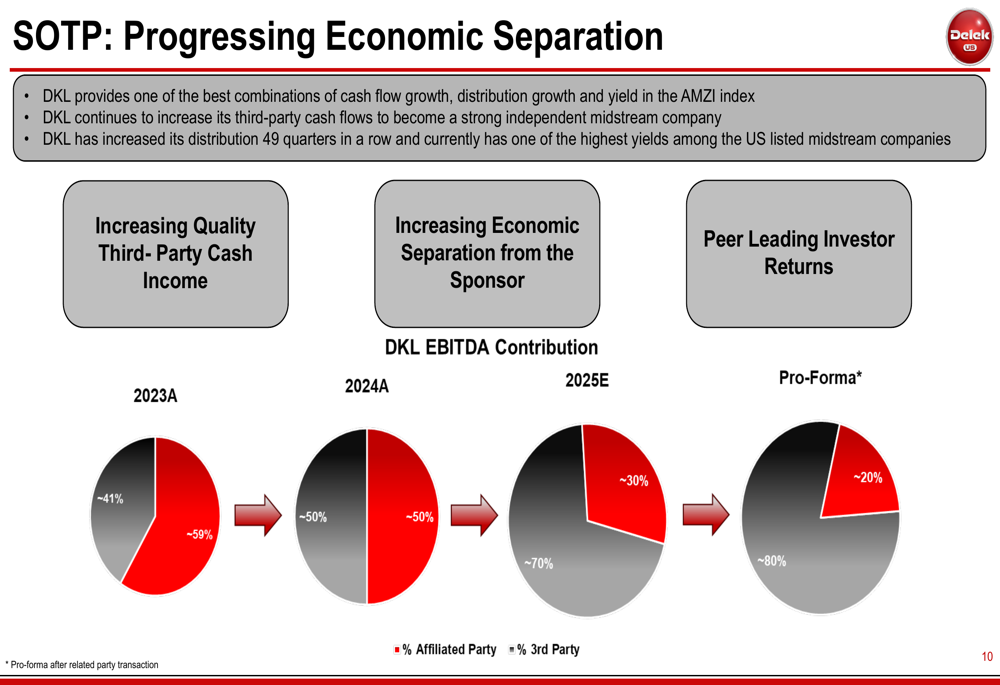

A key component of Delek’s strategy involves separating its midstream business from its refining operations to unlock value. The company has made progress on this front, with new intercompany transactions increasing DKL’s third-party contribution to approximately 80% on a pro-forma basis.

The following chart illustrates the progression of this economic separation:

Detailed Financial Analysis

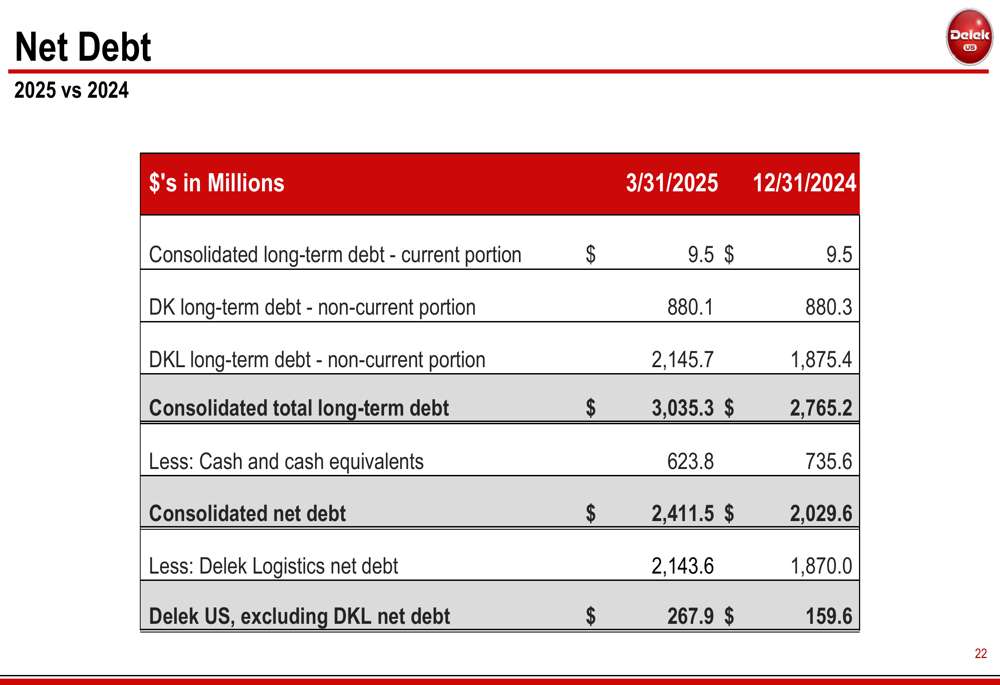

Delek’s consolidated net debt increased to $2.41 billion as of March 31, 2025, up from $2.03 billion at the end of 2024. However, when excluding Delek Logistics’ debt, Delek US’s standalone net debt was $267.9 million, up from $159.6 million at year-end 2024.

The detailed breakdown of the company’s debt position is shown below:

The company has made significant progress in reducing general and administrative expenses, which fell to $51 million in Q1 2025 from $101 million in Q4 2022, representing a substantial cost-cutting achievement amid inflationary pressures.

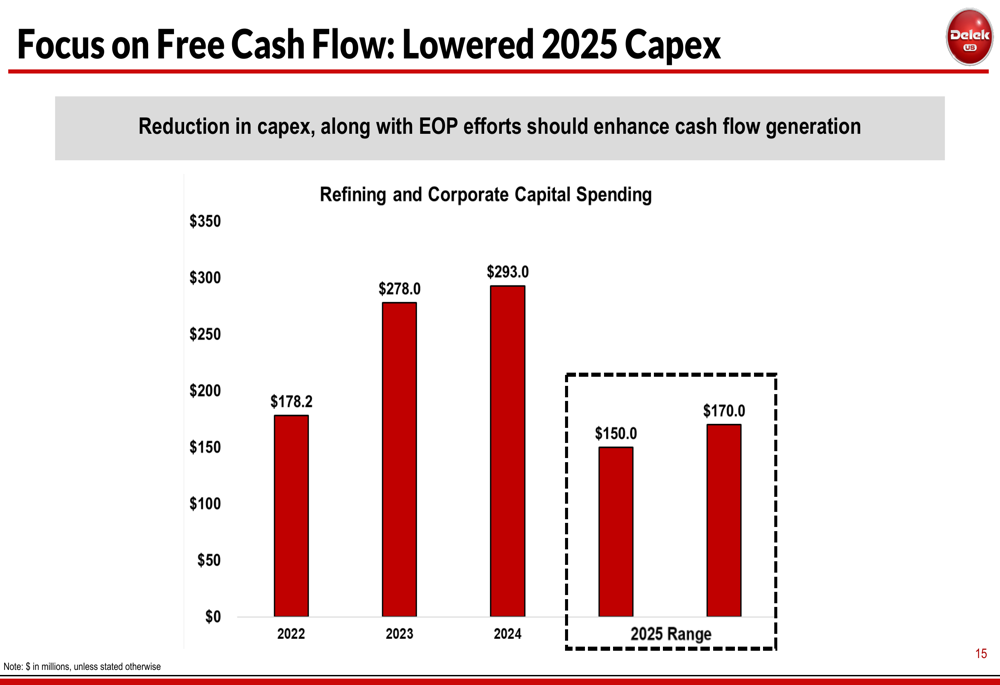

Delek has also reduced its capital expenditure forecast for 2025 to $150-170 million, down significantly from $293 million in 2024, as part of its focus on free cash flow generation:

Segment Performance

The stark contrast between Delek’s refining and logistics segments continued in Q1 2025. While the refining segment struggled with negative EBITDA of $27.4 million, Delek Logistics Partners delivered strong results with EBITDA of $116.5 million.

The logistics business announced its 49th consecutive quarterly distribution increase and reiterated its 2025 Adjusted EBITDA guidance of $480-520 million. The segment successfully closed the acquisition of Gravity Water Midstream and is commissioning the Libby 2 gas plant.

Delek’s refining operations completed planned maintenance at the Tyler and Big Spring refineries during the quarter, positioning these facilities for the summer driving season. However, production margins varied significantly across refineries, with Tyler achieving $7.82 per barrel while El Dorado lagged at $3.83 per barrel.

Forward-Looking Statements

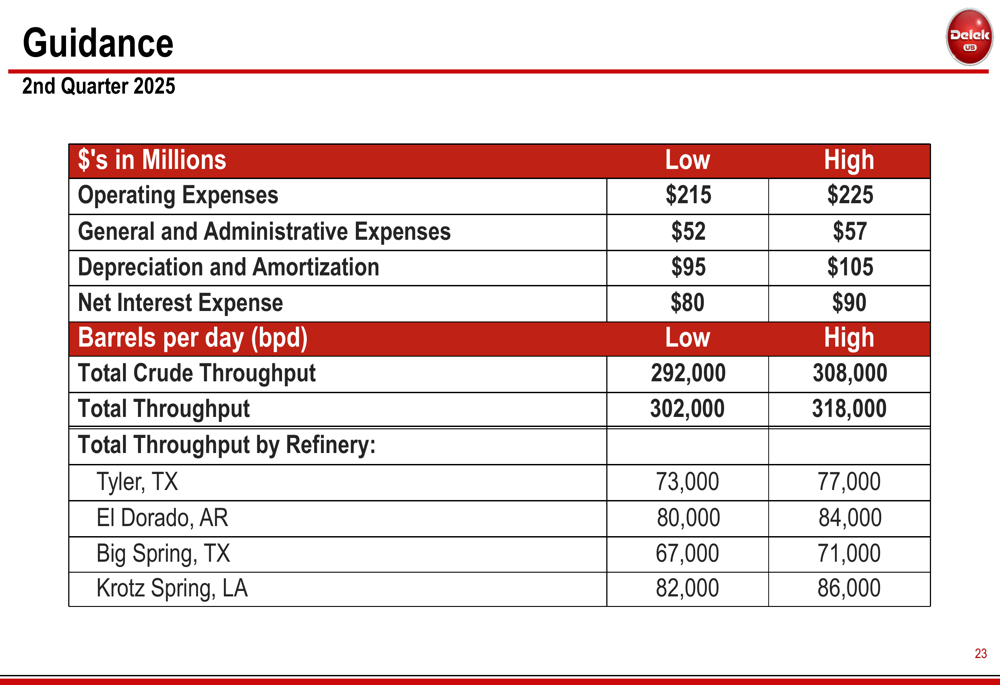

Looking ahead, Delek provided guidance for the second quarter of 2025, projecting total crude throughput of 292,000 to 308,000 barrels per day and operating expenses between $215 million and $225 million:

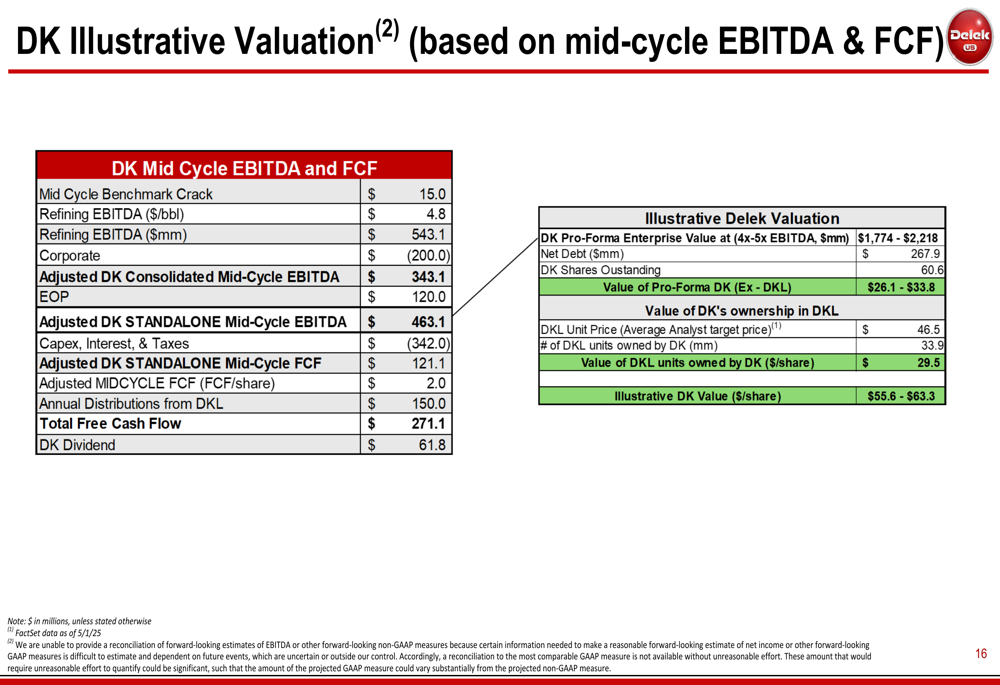

The company continues to emphasize its illustrative valuation model, suggesting significant upside potential if it can successfully execute its strategic initiatives. Delek estimates its standalone mid-cycle free cash flow at approximately $121.1 million, with additional annual distributions from DKL of $150 million.

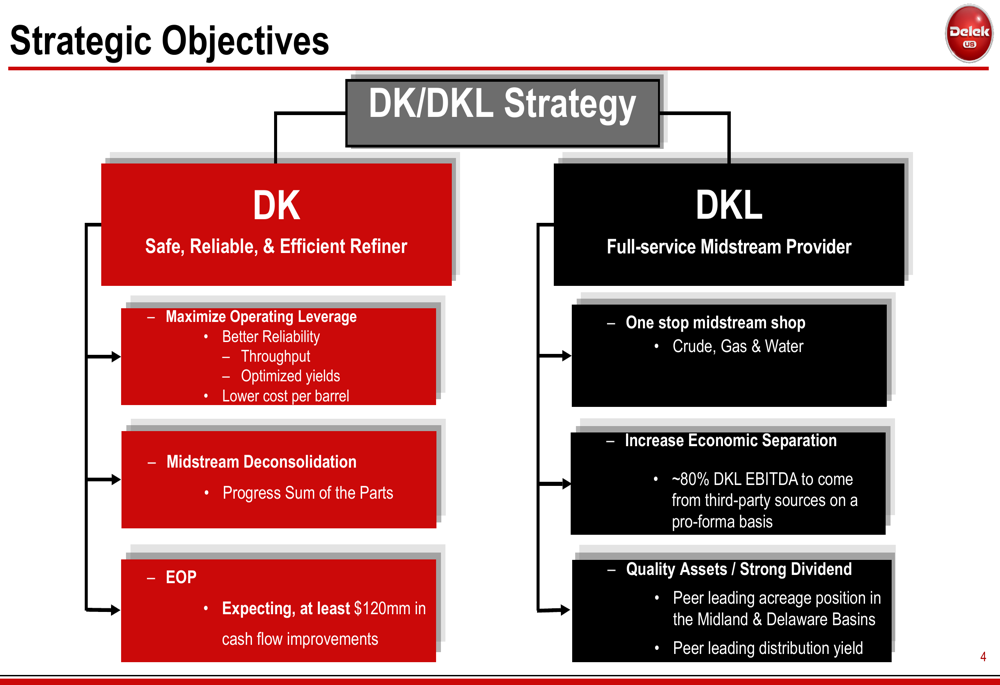

Delek’s management remains focused on the four strategic objectives outlined for both DK and DKL entities:

Conclusion

Delek US faces continued challenges in its core refining business, as evidenced by the significant losses in Q1 2025. However, the company’s strategic initiatives, particularly the Enterprise Optimization Plan and efforts to unlock midstream value, provide potential pathways to improvement.

The stark performance contrast between the struggling refining segment and the thriving logistics business underscores the rationale behind Delek’s Sum of the Parts strategy. If successful, this approach could create significant shareholder value by highlighting the worth of Delek Logistics while improving the operational efficiency of the refining business.

Investors will be watching closely to see if Delek can deliver on its promised $120 million in cash flow improvements in the second half of 2025, which would represent a significant turnaround from current performance levels. With the stock trading near $14, well below the company’s illustrative valuation range of $55.6-$63.3 per share, the market appears skeptical about Delek’s ability to achieve these ambitious targets in the near term.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.