U.S. stocks lower as investors rotate out of tech ahead of Jackson Hole

Introduction & Market Context

De’Longhi SpA (BIT:DLG) presented its Q1 2025 financial results on May 13, showing continued momentum with double-digit revenue growth and improved profitability. The Italian home appliance manufacturer saw its shares rise 6.99% to €30.92 following the announcement, reflecting positive investor sentiment toward the company’s performance and outlook.

The results demonstrate De’Longhi’s successful execution of its growth strategy, particularly in expanding its professional coffee machine business while maintaining strength in its core household appliance segments. This follows the company’s solid performance in 2024, when it achieved 14% annual revenue growth.

Quarterly Performance Highlights

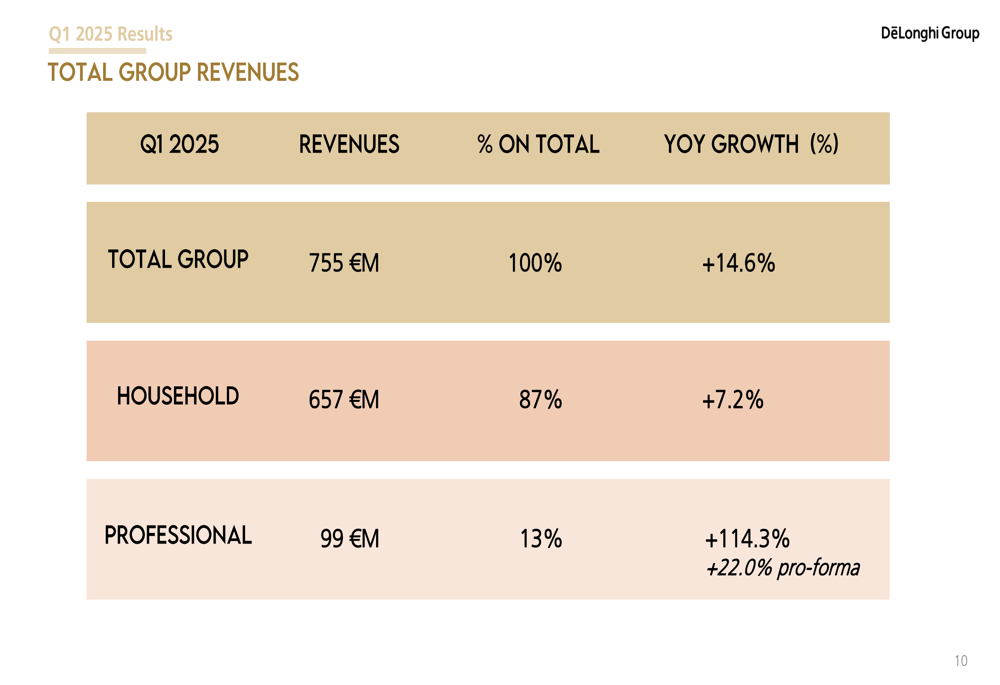

De’Longhi reported total group revenue of €755.2 million for Q1 2025, representing a 14.6% increase compared to the same period last year. This growth was driven by strong performance across both its household and professional divisions.

As shown in the following revenue breakdown:

The household division, which accounts for 87% of total revenue, grew by 7.2% year-over-year to €657 million. Meanwhile, the professional segment showed exceptional growth of 114.3% (22.0% on a pro-forma basis), reaching €99 million and now representing 13% of total revenue.

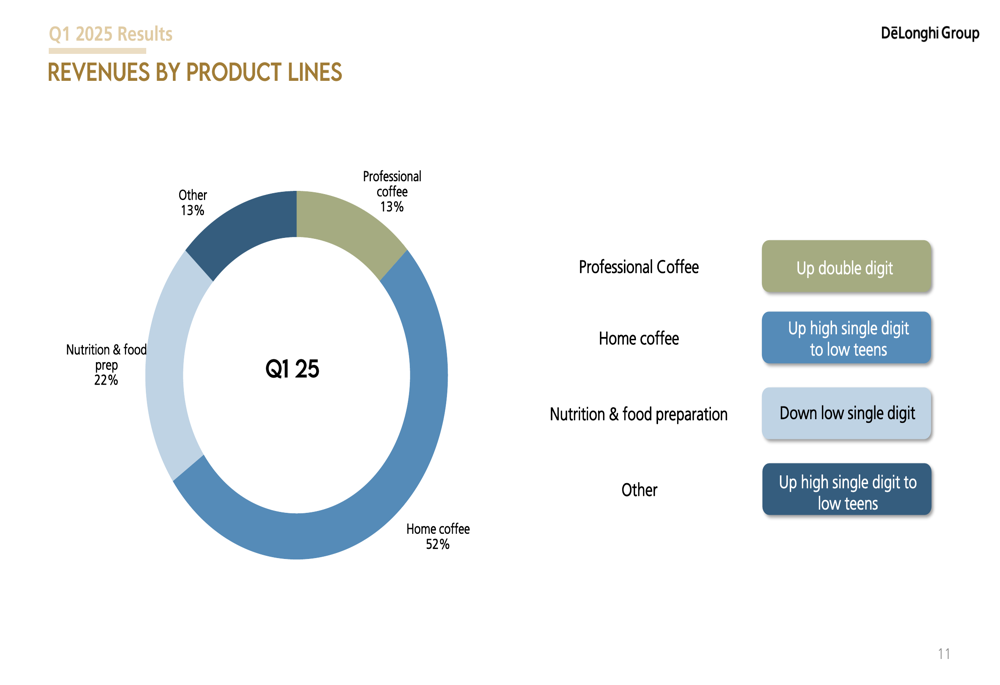

From a product perspective, coffee machines continue to be the company’s primary growth driver, with home coffee representing 52% of total revenue and professional coffee accounting for 13%:

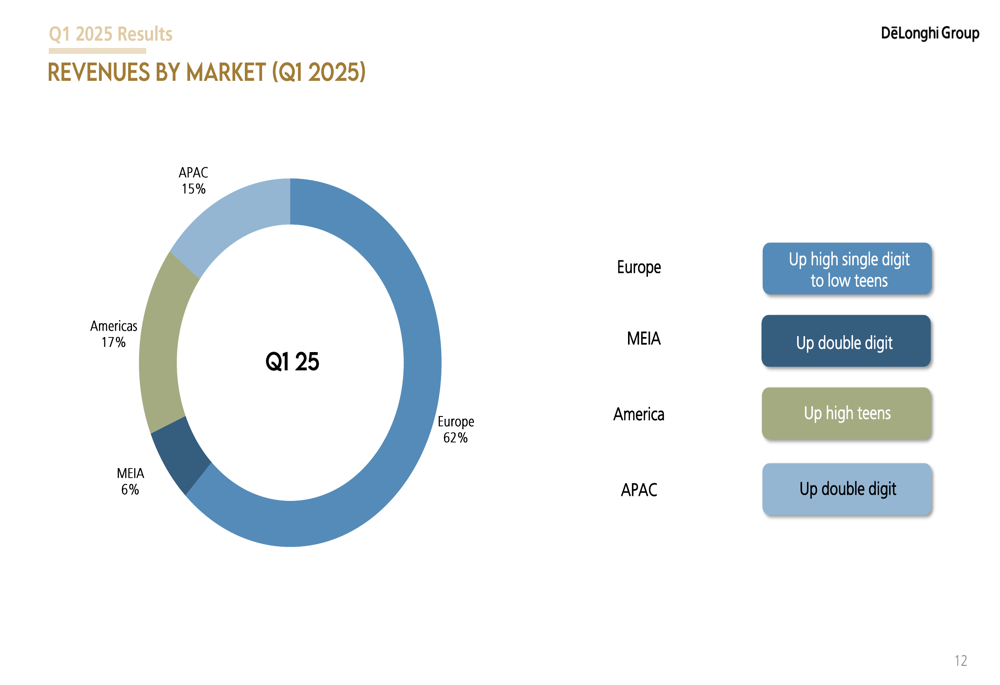

Geographically, Europe remains De’Longhi’s largest market, contributing 62% of total revenue with high single-digit to low-teens growth. The Americas region showed the strongest performance with high-teens growth, while both APAC and MEIA regions achieved double-digit growth:

Detailed Financial Analysis

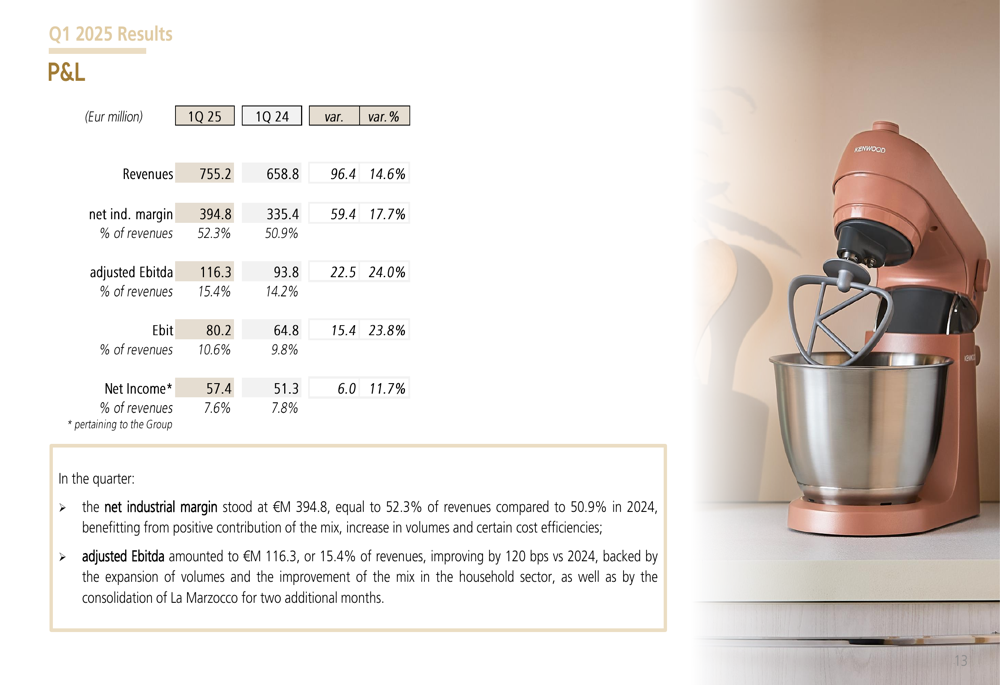

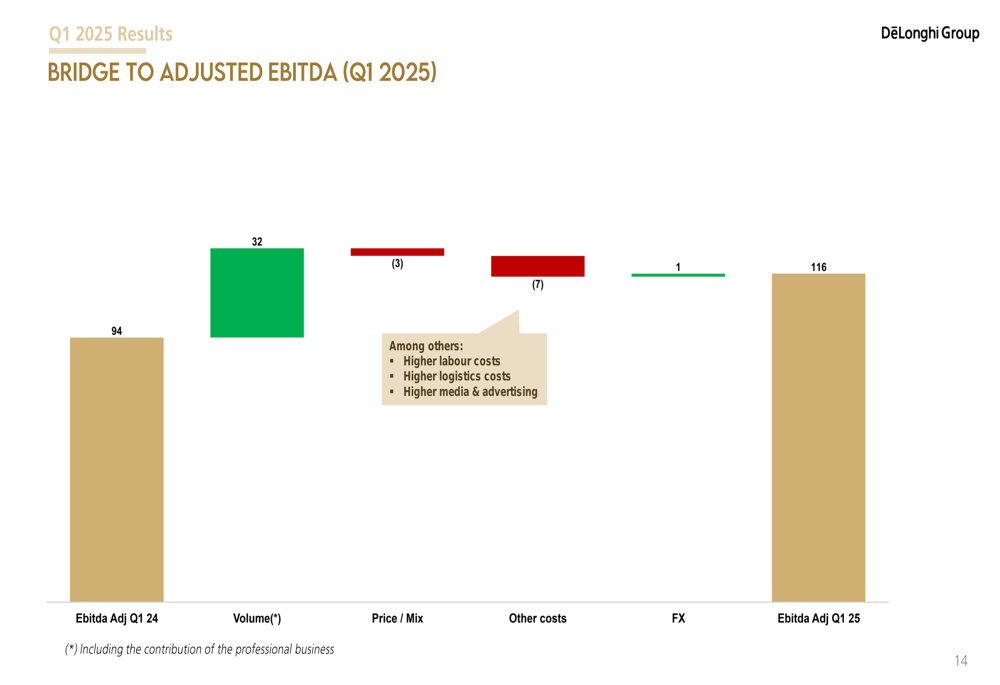

De’Longhi’s profitability showed significant improvement in Q1 2025, with adjusted EBITDA increasing by 24% to €116.3 million, representing a margin of 15.4% compared to 14.2% in Q1 2024. Net income rose by 11.7% to €57.4 million.

The company’s P&L statement highlights these improvements:

The primary drivers behind the EBITDA improvement were increased sales volumes, which contributed €32 million to the adjusted EBITDA growth. This was partially offset by a negative price/mix effect of €3 million and increased costs of €7 million, including higher labor, logistics, and advertising expenses:

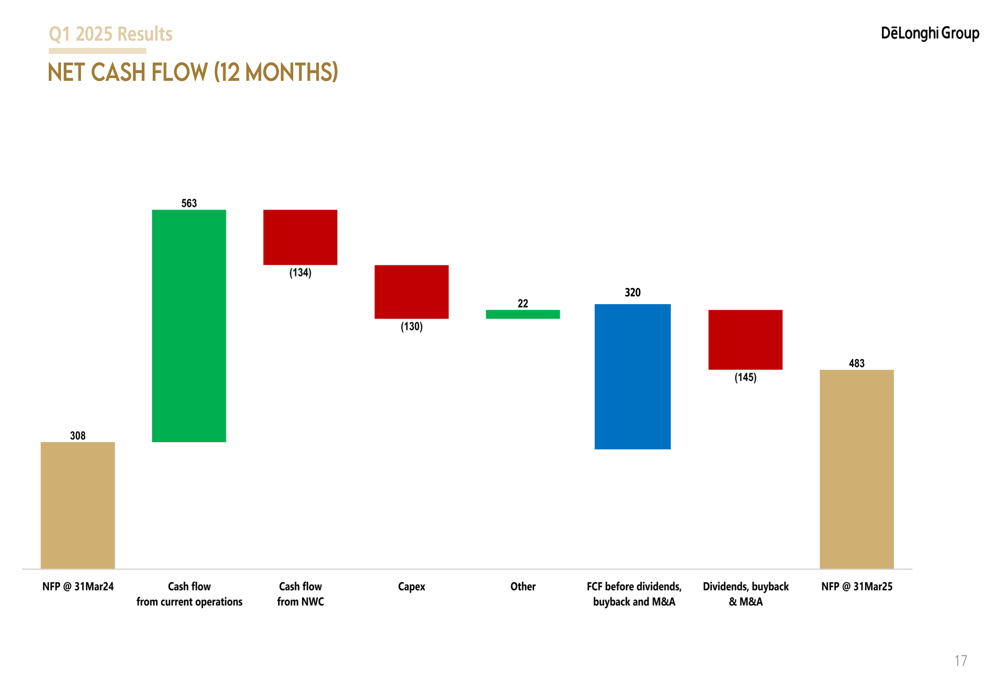

De’Longhi maintained a strong balance sheet with a net cash position of €482.8 million as of March 31, 2025, up from €307.6 million a year earlier, despite funding €36 million in share buybacks during the period. The company’s 12-month free cash flow before dividends, buybacks, and M&A reached €320 million.

The following chart illustrates the company’s cash flow over the past 12 months:

The company’s net working capital increased to €84.9 million (2.4% of revenues) from €36.4 million (1.2% of revenues) a year earlier. This increase was primarily due to a strategic decision to build up inventory to mitigate the impact of tariffs, particularly for the US market.

Strategic Initiatives

De’Longhi continues to emphasize product innovation and design excellence, starting 2025 with numerous design awards across its product portfolio. The company highlighted its success in receiving prestigious "reddot" and "iF Design" awards for products in its home coffee, nutrition and food preparation, and other appliance categories.

The company’s professional coffee business expansion remains a key strategic focus, with La Marzocco contributing significantly to growth. Management noted that the professional coffee segment benefits from "continuous structural market growth" and "targeted luxury home partnership."

In response to US tariffs, De’Longhi has demonstrated operational flexibility by adjusting its inventory management and leveraging its global manufacturing footprint. The company has also maintained its advertising and promotion investments to support brand strength and market position.

Forward-Looking Statements

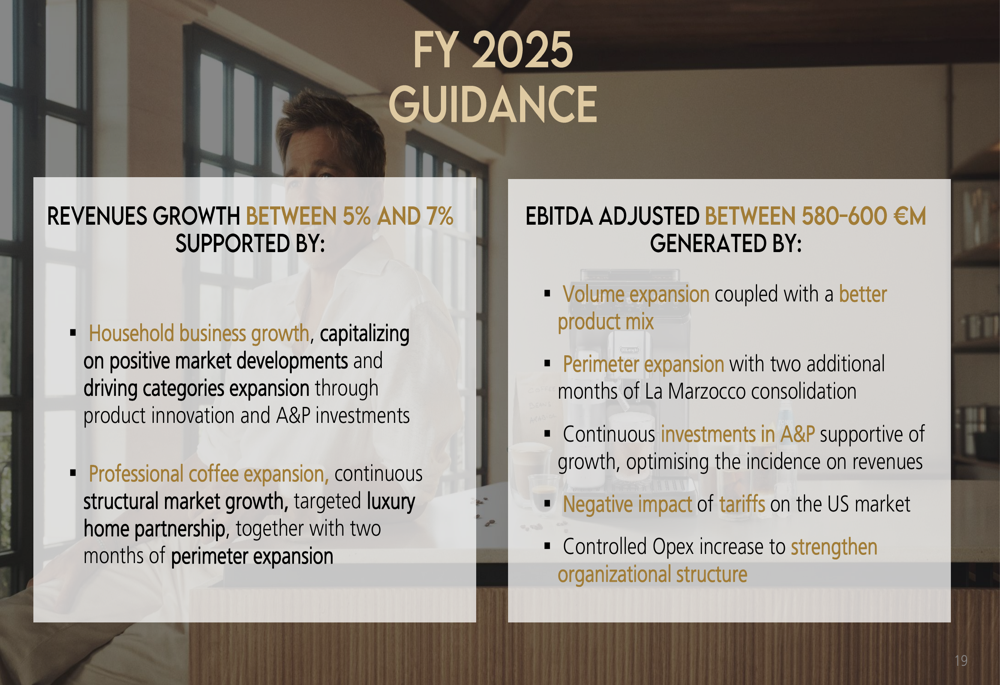

For the full year 2025, De’Longhi provided the following guidance:

The company expects revenue growth between 5% and 7%, supported by continued expansion in both household and professional segments. Adjusted EBITDA is projected to reach between €580-600 million, driven by volume expansion, improved product mix, and the full-year consolidation of La Marzocco.

Management acknowledged the negative impact of US tariffs but expressed confidence in their ability to mitigate these challenges through pricing strategies and cost management. The company plans to continue investing in advertising and promotion to support growth while optimizing the impact on revenues.

In the Q1 2025 presentation, CEO Fabio De’Longhi emphasized the company’s "positive momentum" in both household and professional divisions, highlighting the enhancement of adjusted EBITDA margin to 15.4% and the solid net cash position of approximately €500 million even after funding the share buyback program.

With its strong start to 2025, De’Longhi appears well-positioned to build on its 2024 performance and navigate potential challenges in the global market while continuing to expand its product portfolio and geographic reach.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.