Nvidia AI chips targeted in China customs crackdown- FT

Introduction & Market Context

Deluxe Corporation (NYSE:DLX) presented its first quarter 2025 earnings on April 30, 2025, highlighting modest overall revenue growth with standout performance in its Data Solutions segment. Despite reporting improved metrics across several key areas, the company’s stock declined 5.81% during the trading session, closing at $15.50.

The financial services and business technology company continues to execute its strategic shift from a legacy print-focused business toward higher-growth payments and data solutions. This transformation is gradually changing Deluxe’s revenue composition, though print products still represent the majority of its business.

Quarterly Performance Highlights

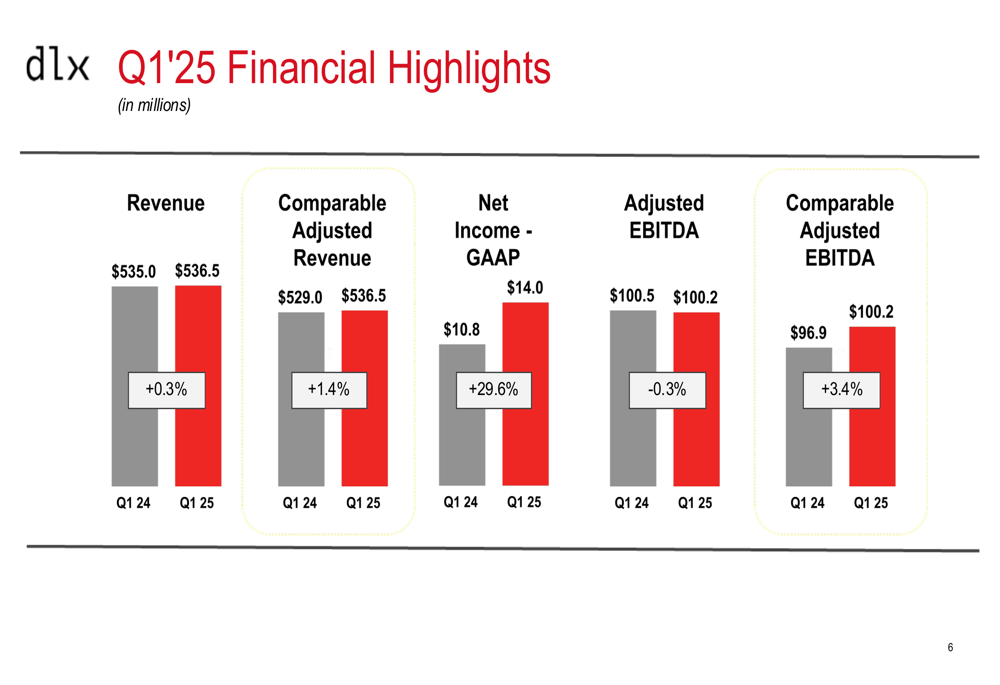

Deluxe reported Q1 2025 revenue of $536.5 million, a slight increase of 0.3% compared to Q1 2024. On a comparable adjusted basis, revenue grew 1.4% year-over-year. The company’s GAAP net income reached $14.0 million, representing a substantial 29.6% increase from the prior year’s $10.8 million.

As shown in the following financial highlights chart, Deluxe’s adjusted EBITDA remained relatively stable at $100.2 million, though comparable adjusted EBITDA increased by 3.4% year-over-year:

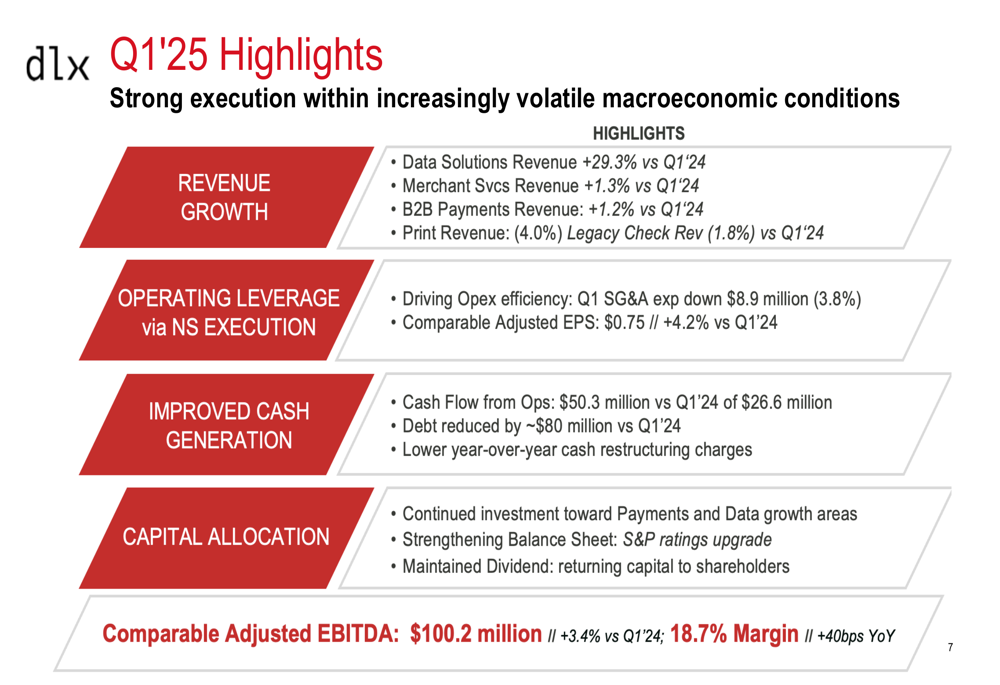

The company demonstrated strong execution amid challenging macroeconomic conditions, with notable improvements in operating efficiency. Selling, general, and administrative expenses decreased by $8.9 million (3.8%) compared to Q1 2024, contributing to margin expansion in several segments.

The following slide summarizes key achievements across revenue growth, operating leverage, cash generation, and capital allocation:

Segment Performance Analysis

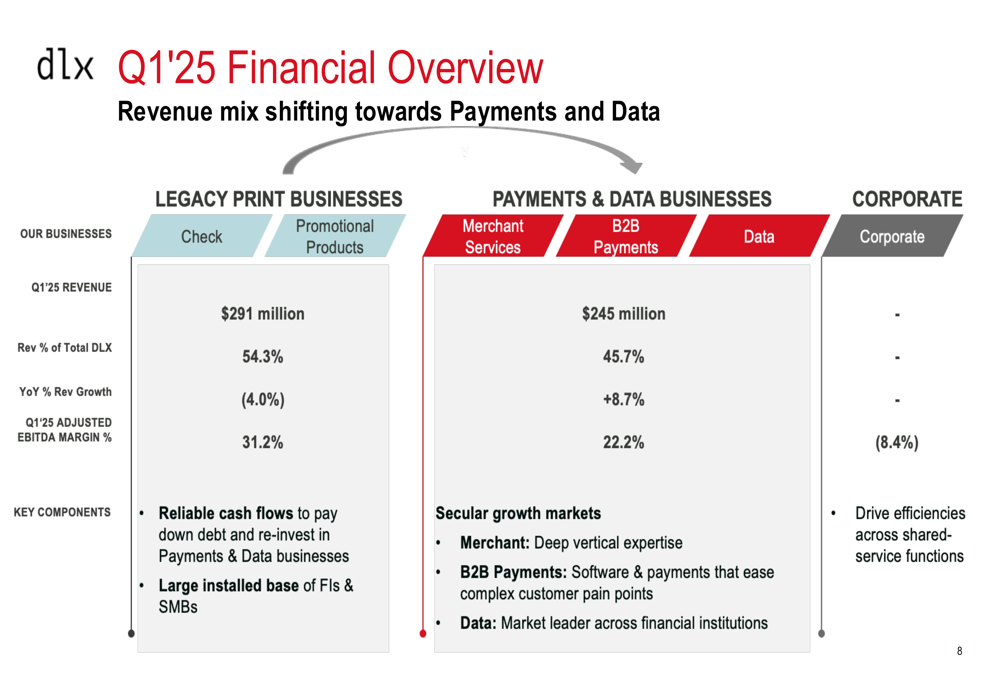

Deluxe’s business is increasingly shifting toward its Payments and Data segments, which now represent 45.7% of total revenue compared to 54.3% for legacy print businesses. This strategic pivot is illustrated in the following financial overview:

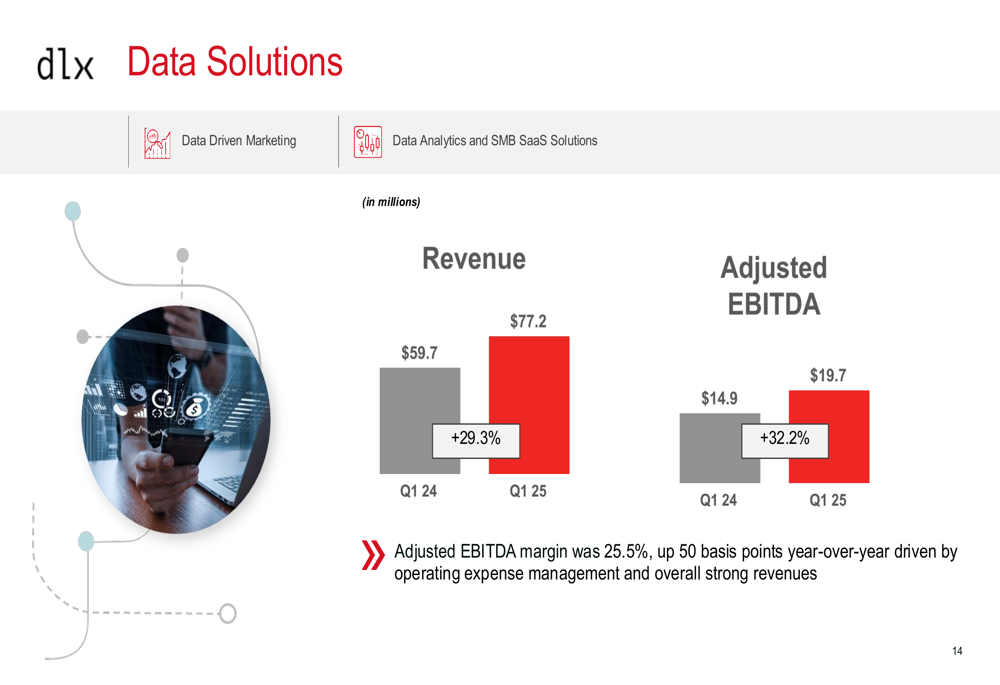

The standout performer was the Data Solutions segment, which posted impressive growth of 29.3% year-over-year, reaching $77.2 million in revenue. The segment’s adjusted EBITDA increased by 32.2% to $19.7 million, with margins expanding to 25.5%.

As shown in the Data Solutions performance slide, the segment benefited from strong revenue growth and effective operating expense management:

Merchant Services and B2B Payments segments showed modest growth of 1.3% and 1.2% respectively, while maintaining stable adjusted EBITDA figures. The legacy Print segment continued its expected decline, with revenue decreasing by 4.0% to $291.3 million. However, the Print segment still generated the highest adjusted EBITDA at $90.8 million with an impressive 31.2% margin, expanding 120 basis points year-over-year due to improved operating efficiency.

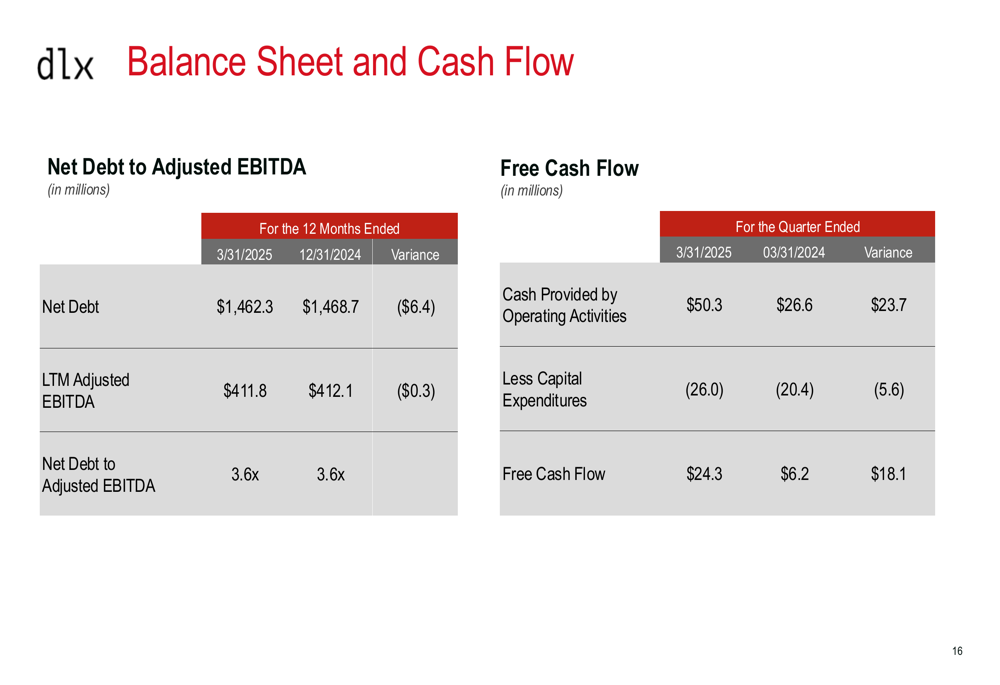

Balance Sheet and Cash Flow Improvements

Deluxe significantly improved its cash flow generation in Q1 2025. Cash provided by operating activities nearly doubled to $50.3 million compared to $26.6 million in Q1 2024. Free cash flow increased substantially to $24.3 million from $6.2 million in the prior year period, despite higher capital expenditures.

The following slide details the company’s balance sheet and cash flow metrics:

The company maintained its net debt to adjusted EBITDA ratio at 3.6x, unchanged from December 31, 2024. Deluxe reported debt reduction of approximately $80 million compared to Q1 2024 and noted an S&P ratings upgrade, reflecting its strengthened financial position.

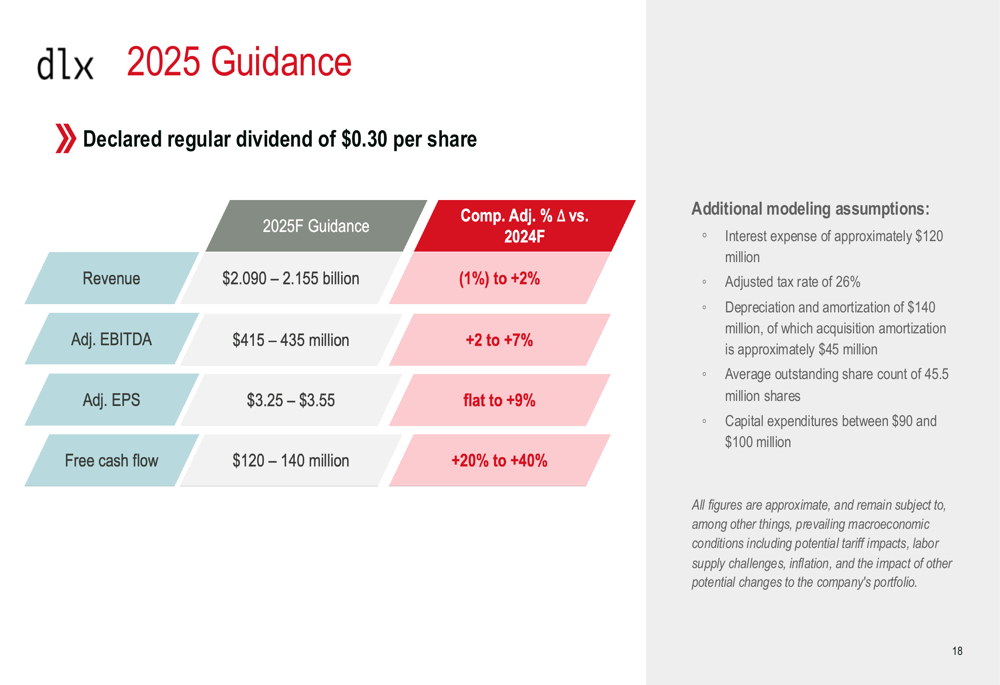

2025 Guidance and Long-term Strategy

Deluxe maintained its 2025 guidance, projecting revenue between $2.090 billion and $2.155 billion, representing a range of -1% to +2% growth compared to 2024. The company expects adjusted EBITDA of $415-435 million (+2% to +7%) and adjusted EPS of $3.25-$3.55 (flat to +9%).

The following slide outlines the company’s full-year guidance and key assumptions:

Free cash flow is projected to increase significantly to $120-140 million, representing 20% to 40% growth compared to 2024. Deluxe also declared a regular quarterly dividend of $0.30 per share, continuing its long history of returning capital to shareholders.

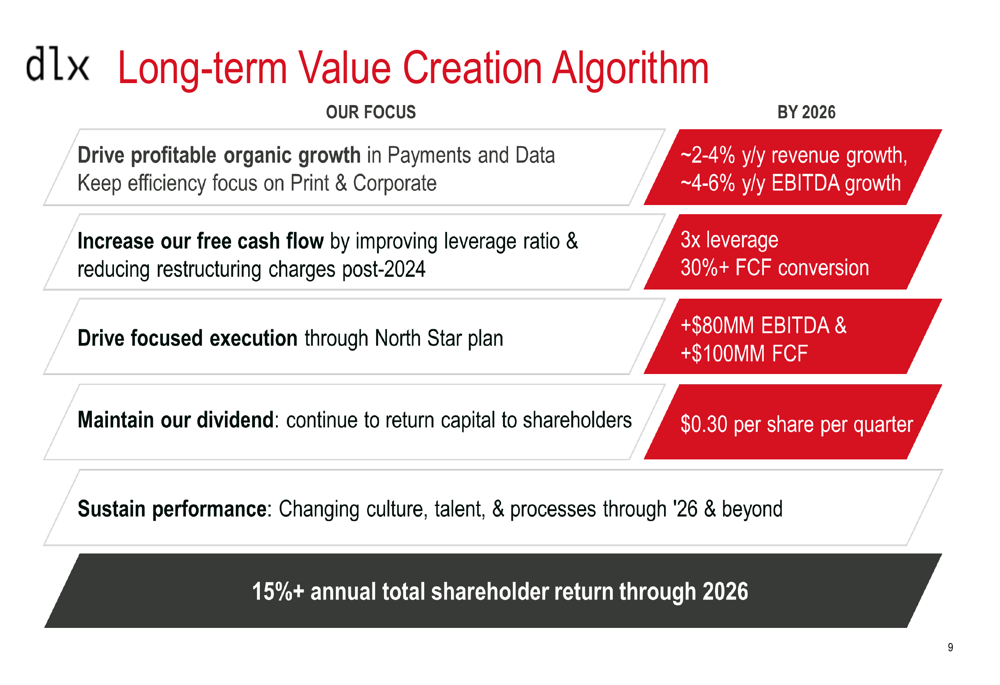

The company’s long-term value creation strategy focuses on driving profitable organic growth in Payments and Data segments while maintaining efficiency in Print operations. Deluxe aims to achieve 2-4% annual revenue growth and 4-6% annual EBITDA growth, with a target of 15% annual total shareholder return through 2026.

Market Reaction and Analyst Perspectives

Despite the positive narrative presented in the earnings slides, Deluxe’s stock declined 5.81% on the day of the earnings release. This negative market reaction contrasts with the previous quarter’s performance, when the stock rose 2.39% in after-hours trading following Q4 2024 results.

The disconnect between improving financial metrics and stock performance may reflect investor concerns about the pace of transformation. While Data Solutions showed impressive growth, the more modest performance in Merchant Services and B2B Payments segments could be raising questions about the company’s ability to accelerate growth in these areas.

Additionally, with Print still representing over half of Deluxe’s revenue and generating the majority of its adjusted EBITDA, the company remains dependent on a declining business segment. The continued secular decline in Print (-4.0% in Q1) creates an ongoing headwind that the growth segments must overcome.

Deluxe’s transformation story continues to evolve, with meaningful progress in shifting its revenue mix toward higher-growth segments. However, investors appear to be taking a cautious approach as they assess whether the company can successfully execute its long-term strategy while navigating challenging macroeconomic conditions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.