Bitcoin price today: dips below $112k, near 6-wk low despite Fed cut bets

Introduction & Market Context

Dentalcorp Holdings Ltd (TSX:DNTL), Canada’s largest dental network, delivered strong Q1 2025 results with significant revenue growth and margin expansion, according to the company’s latest investor presentation. The dental services provider continues to capitalize on its position in a highly fragmented Canadian dental market worth $22 billion, where only about 7% of practices are currently consolidated.

The company’s stock has responded positively to its consistent performance, trading at $8.81 as of May 9, 2025, up 0.57% and significantly above its 52-week low of $6.04, though still below its 52-week high of $10.50.

Quarterly Performance Highlights

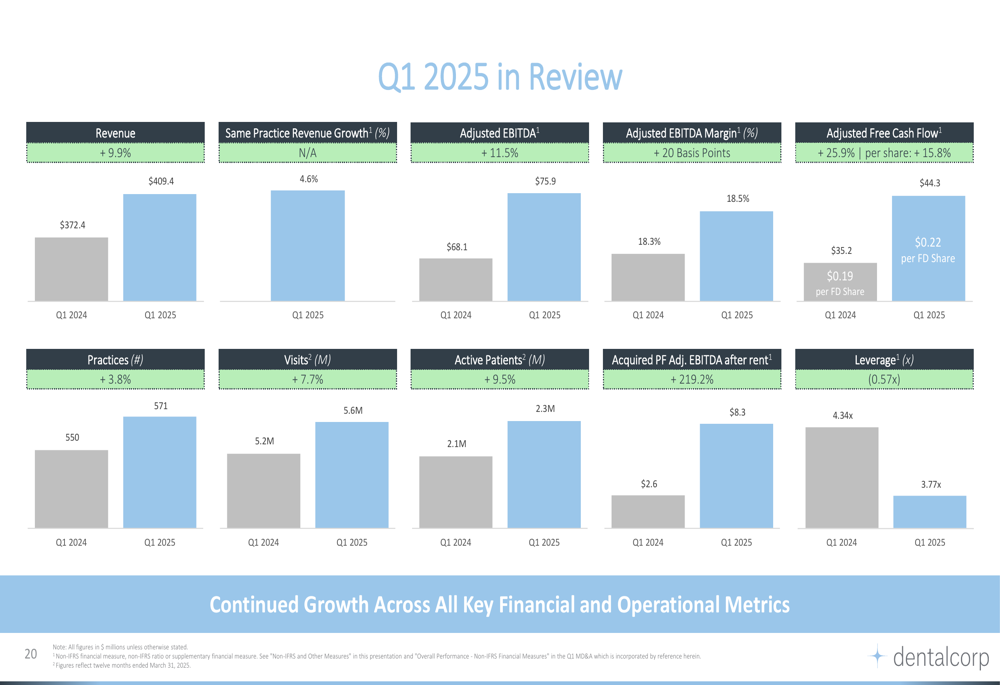

Dentalcorp reported impressive Q1 2025 results, with revenue reaching $409.4 million, representing a 9.9% increase year-over-year. Same practice revenue growth stood at 4.6%, exceeding the company’s medium-term target of 4%+. Adjusted EBITDA grew by 11.5% to $75.9 million, with margins expanding by 20 basis points to 18.5%.

The company’s quarterly performance summary highlights substantial growth across key metrics:

Adjusted free cash flow showed particularly strong momentum, increasing by 25.9% to $44.3 million ($0.22 per fully diluted share, up 15.8%). This robust cash generation supports the company’s acquisition strategy while maintaining its quarterly dividend of $0.025 per share.

Operationally, Dentalcorp continued to expand its footprint, reaching 571 practices (up 3.8%) and serving 2.3 million active patients (up 9.5%). The company completed 5.6 million patient visits during the period, representing a 7.7% increase year-over-year.

Consolidation Strategy

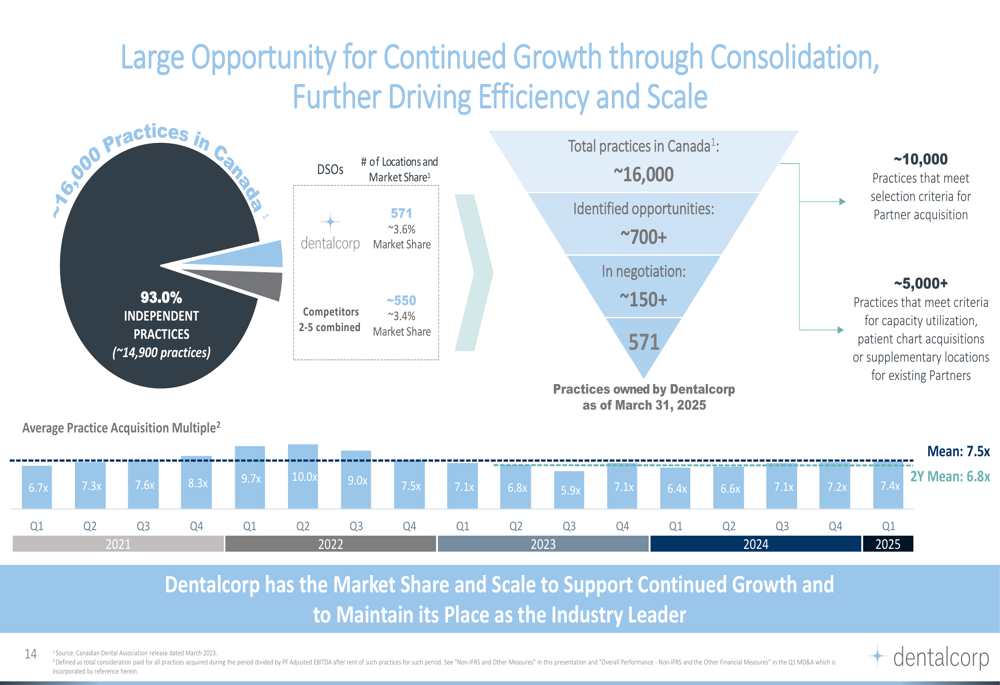

Dentalcorp’s growth strategy centers on consolidating Canada’s fragmented dental market, where approximately 14,900 practices (93% of the total market) remain independent. The company currently holds a 3.6% market share with its 571 locations but has identified over 700 acquisition opportunities and is actively negotiating with more than 150 potential targets.

The following chart illustrates the significant consolidation opportunity remaining in the Canadian dental market:

The company has deployed over $1 billion in acquisitions since its IPO, targeting a 15%+ return on invested capital from practice acquisitions. In Q1 2025 alone, Dentalcorp acquired practices expected to generate $8.3 million in pro forma adjusted EBITDA after rent, a 219.2% increase from the prior year.

Dentalcorp’s integration platform drives value creation through a structured approach that typically yields a 10-15% increase in visit frequency and 10-15%+ immediate practice-level EBITDA margin expansion through cost synergies.

Technology Investments

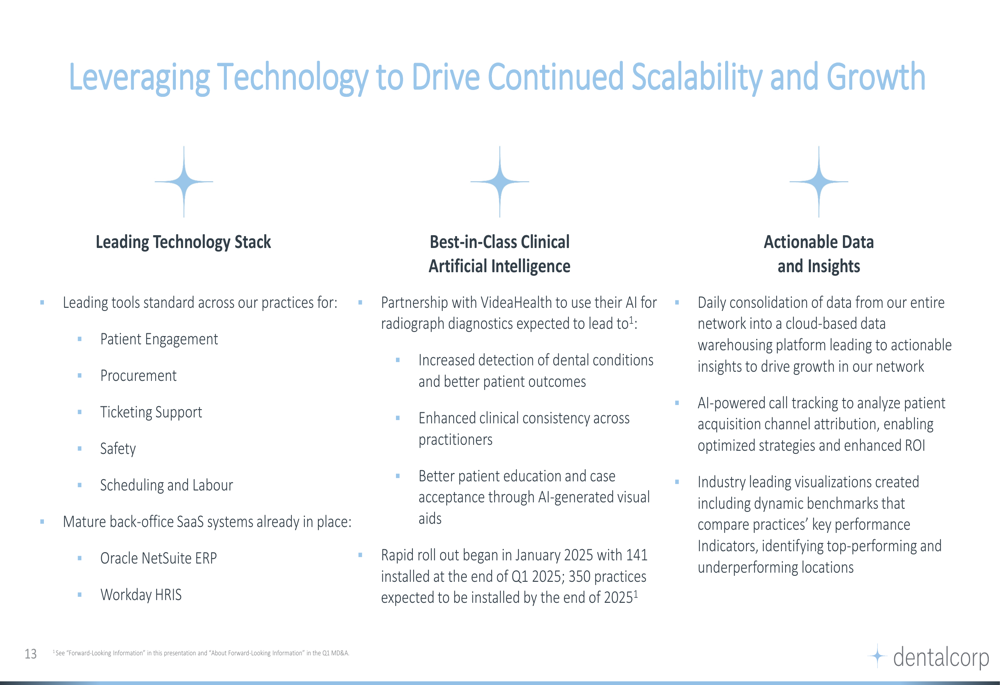

A key component of Dentalcorp’s strategy is leveraging technology to drive scalability and growth. The company is rapidly expanding its partnership with VideaHealth to implement AI-powered diagnostic tools across its network. As of Q1 2025, 141 practices had been equipped with this technology, with plans to reach 350 practices by the end of 2025.

The company’s technology implementation strategy is outlined in the following slide:

This technology investment is expected to enhance diagnostic capabilities, improve patient outcomes, and drive operational efficiencies. The company also utilizes AI-powered call tracking and maintains a cloud-based data warehousing platform that consolidates practice data daily, providing actionable insights for management.

Financial Profile and Deleveraging Progress

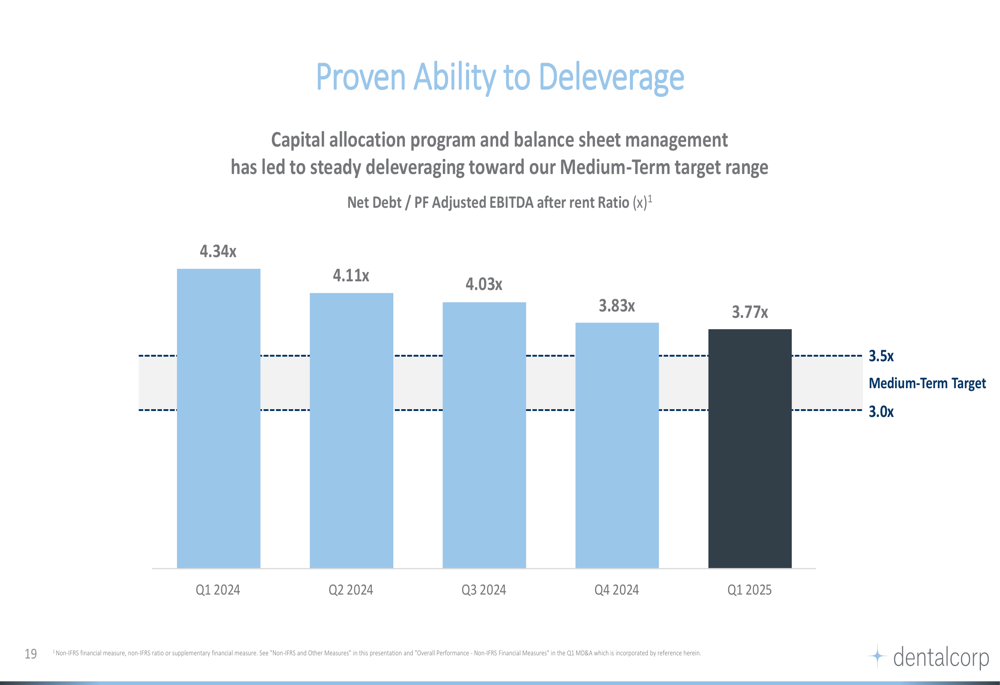

Dentalcorp has demonstrated a consistent ability to deleverage its balance sheet while pursuing growth. The company’s net debt to pro forma adjusted EBITDA after rent ratio decreased from 4.34x in Q1 2024 to 3.77x in Q1 2025, approaching its medium-term target of 3.5x.

The following chart illustrates Dentalcorp’s deleveraging progress:

The company’s financial profile is characterized by robust and expanding margins, low capital expenditure requirements, and capped interest rate exposure. With an average revenue per practice of $2.9 million and practice-level EBITDA after rent margins exceeding 22%, Dentalcorp generates substantial cash flow to support both its growth initiatives and deleveraging efforts.

Competitive Positioning and Valuation

Dentalcorp’s business model benefits from several competitive advantages, including its position as an essential healthcare provider with highly recurring revenue (92% recurring patient visits) and a private, cash-pay model with limited exposure to insurance companies or government programs.

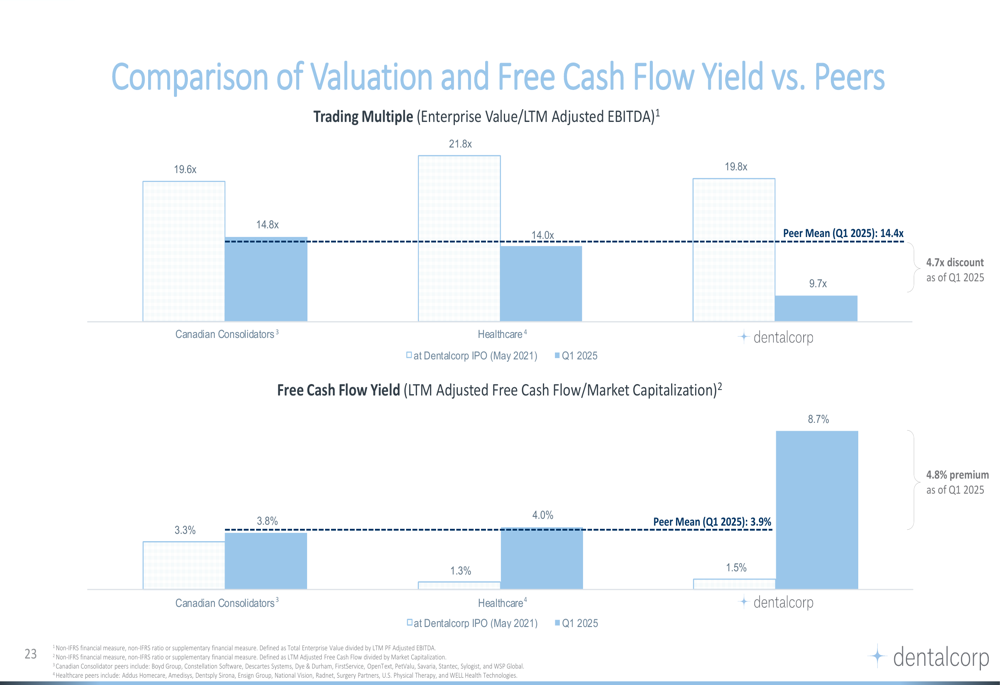

Despite its strong performance and growth trajectory, Dentalcorp trades at a valuation premium compared to peers, while offering a significantly higher free cash flow yield:

The company’s trading multiple of 19.8x represents a 4.7x premium to the peer average of 14.4x. However, Dentalcorp’s free cash flow yield of 8.7% is substantially higher than the peer average of 3.9%, potentially indicating an attractive investment opportunity based on cash generation capabilities.

Long-Term Growth Trajectory

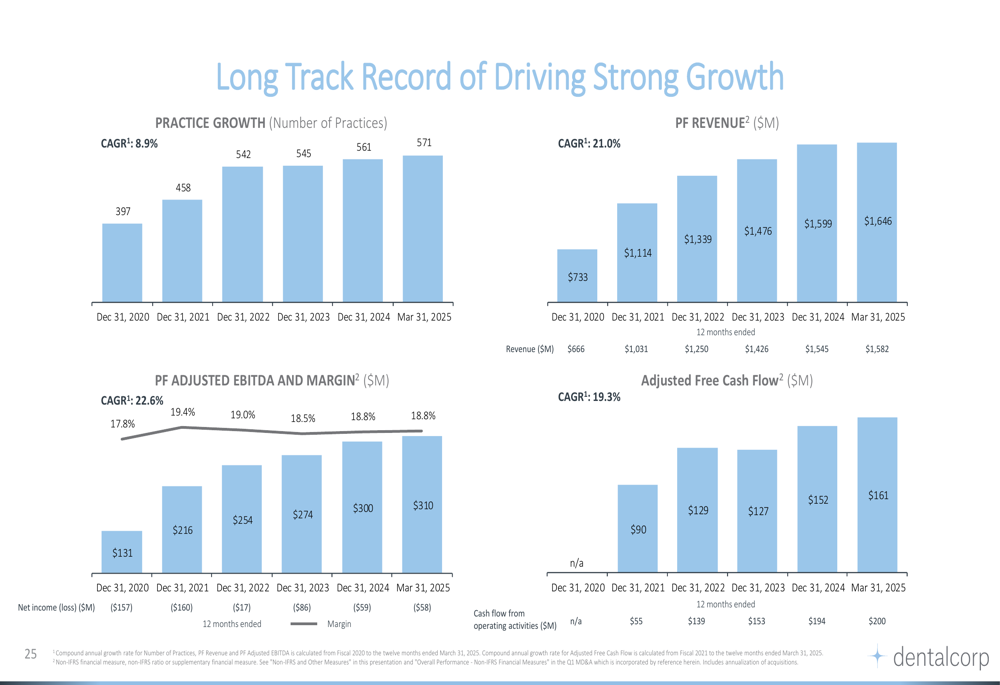

Dentalcorp has established a consistent track record of growth since 2020, with practices increasing from 397 to 571, pro forma revenue growing from $733 million to $1.646 billion, and pro forma adjusted EBITDA rising from $131 million to $310 million.

The following chart illustrates the company’s historical growth trajectory:

This performance translates to impressive compound annual growth rates: 19.3% for adjusted free cash flow, 21.0% for pro forma revenue, and 22.6% for pro forma adjusted EBITDA.

Forward-Looking Statements

Looking ahead, Dentalcorp aims to maintain its growth momentum through a balanced approach combining organic growth, operating productivity improvements, and strategic acquisitions. The company targets same-practice revenue growth of 3-5% for 2025, with total revenue growth of 10-11%.

Management expects modest EBITDA margin expansion of approximately 20 basis points and plans to continue its M&A activities, targeting over $25 million in pro forma adjusted EBITDA contribution from acquisitions in 2025.

CEO Graham Rosenberg has emphasized the company’s strong free cash flow position, stating, "We have more than sufficient free cash flow to support a $0.025 dividend," while CFO Nate Choklia highlighted the significance of their acquisition strategy, noting, "Our continued position as the acquirer of choice... has never been more significant than it is today."

As Dentalcorp continues to execute its consolidation strategy in a fragmented market, investors will be watching closely to see if the company can maintain its growth trajectory while progressing toward its medium-term financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.