Fubotv earnings beat by $0.10, revenue topped estimates

Introduction & Market Context

Dentsply Sirona Inc. (NASDAQ:XRAY) presented its second quarter 2025 earnings results on August 7, 2025, revealing a mixed performance characterized by declining sales but improved profitability metrics. The dental equipment and supplies manufacturer reported results during a period of leadership transition, with new CEO Dan Scavilla taking the helm on August 1, 2025.

The company’s stock closed at $13.68 on August 6, 2025, down 2.63% ahead of the earnings presentation, and has declined significantly from its 52-week high of $27.48. This performance reflects ongoing investor concerns about the company’s revenue challenges, despite improvements in operational efficiency.

Quarterly Performance Highlights

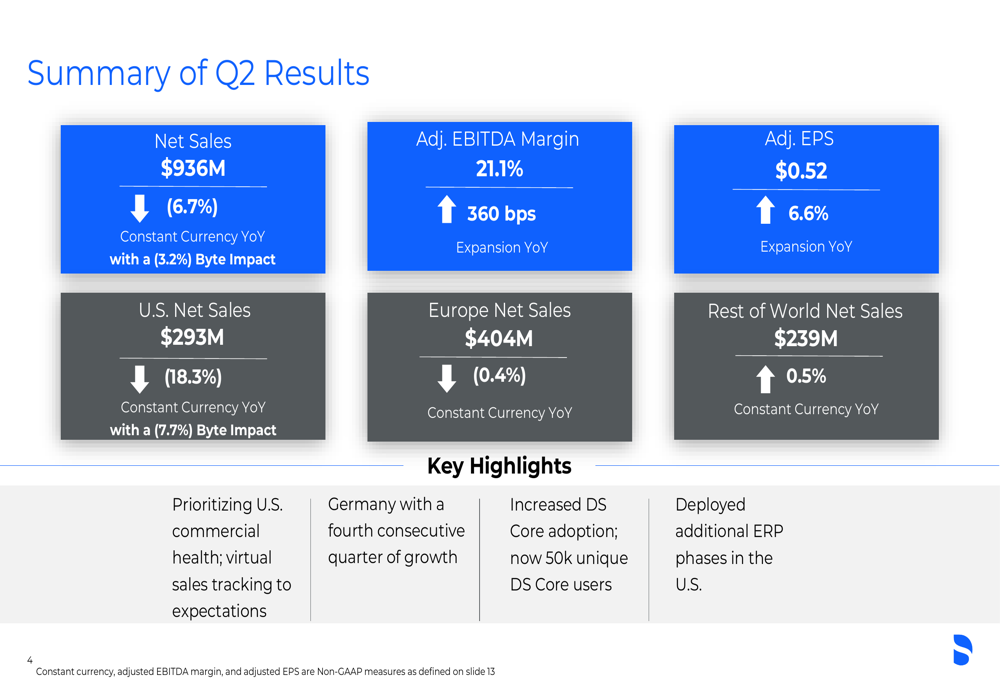

Dentsply Sirona reported Q2 2025 net sales of $936 million, representing a 6.7% year-over-year decrease on a constant currency basis, with 3.2 percentage points of the decline attributed to the Byte business. Despite the revenue challenges, the company achieved notable improvements in profitability metrics.

As shown in the following summary of Q2 results:

The company’s adjusted EBITDA margin expanded significantly to 21.1%, representing a 360 basis point improvement compared to the same period last year. Adjusted earnings per share increased by 6.6% year-over-year to $0.52, demonstrating the company’s ability to enhance profitability despite top-line pressures.

Regional performance varied considerably, with U.S. net sales declining 18.3% on a constant currency basis (including a 7.7% Byte impact), while European sales remained relatively stable with a modest 0.4% decrease. The Rest of World region was the only geography to show growth, with sales increasing 0.5% year-over-year on a constant currency basis.

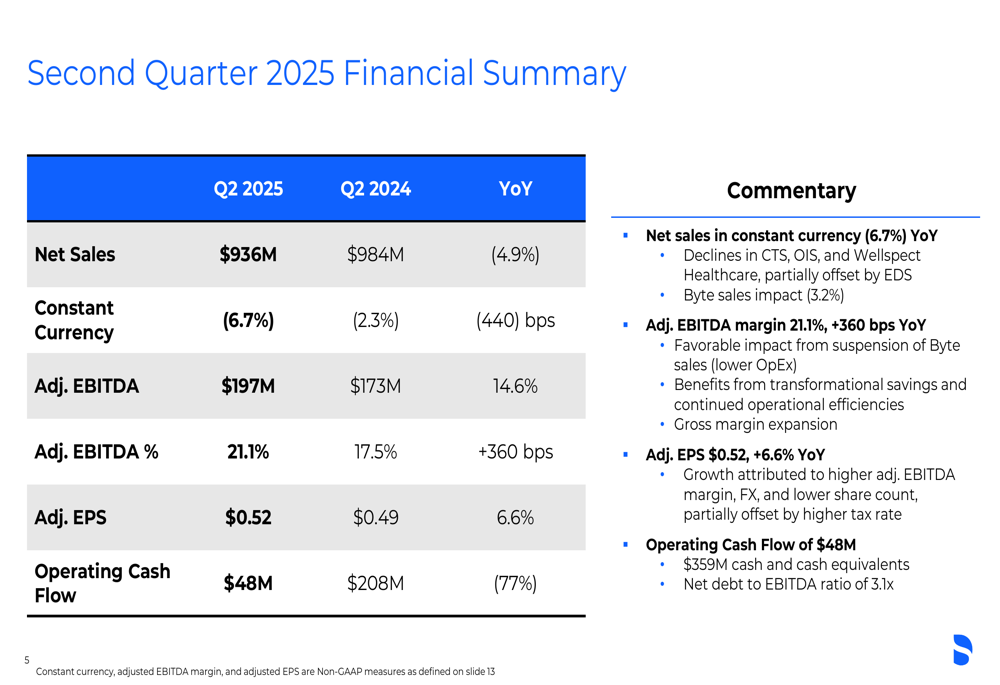

A more detailed financial comparison with the prior year quarter reveals significant margin expansion despite revenue challenges:

Operating cash flow declined substantially to $48 million in Q2 2025 from $208 million in Q2 2024, representing a 77% decrease. This significant reduction in cash generation could present challenges for the company’s financial flexibility if the trend continues.

Segment Performance

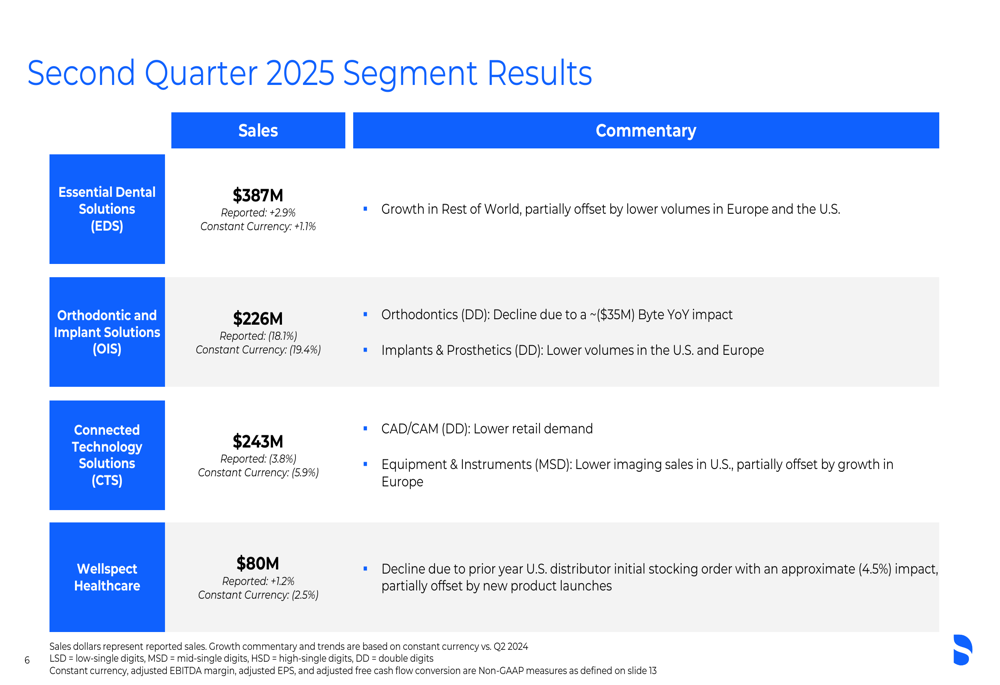

Dentsply Sirona’s business segments delivered varied results, with Essential Dental Solutions showing growth while other segments experienced declines:

The Essential Dental Solutions (EDS) segment reported sales of $387 million, growing 1.1% on a constant currency basis, driven by growth in Rest of World markets that offset lower volumes in Europe and the U.S.

The Orthodontic and Implant Solutions (OIS) segment experienced the steepest decline, with sales falling 19.4% on a constant currency basis to $226 million. This decline was attributed to the year-over-year impact from Byte and lower volumes in both the U.S. and European markets.

Connected Technology Solutions (CTS (NYSE:CTS)) reported sales of $243 million, declining 5.9% on a constant currency basis, primarily due to lower retail demand for CAD/CAM products and reduced imaging sales in the U.S., partially offset by growth in Europe.

The Wellspect Healthcare segment generated $80 million in sales, declining 2.5% on a constant currency basis, impacted by a prior year U.S. distributor initial stocking order, though partially offset by new product launches.

Leadership Transition

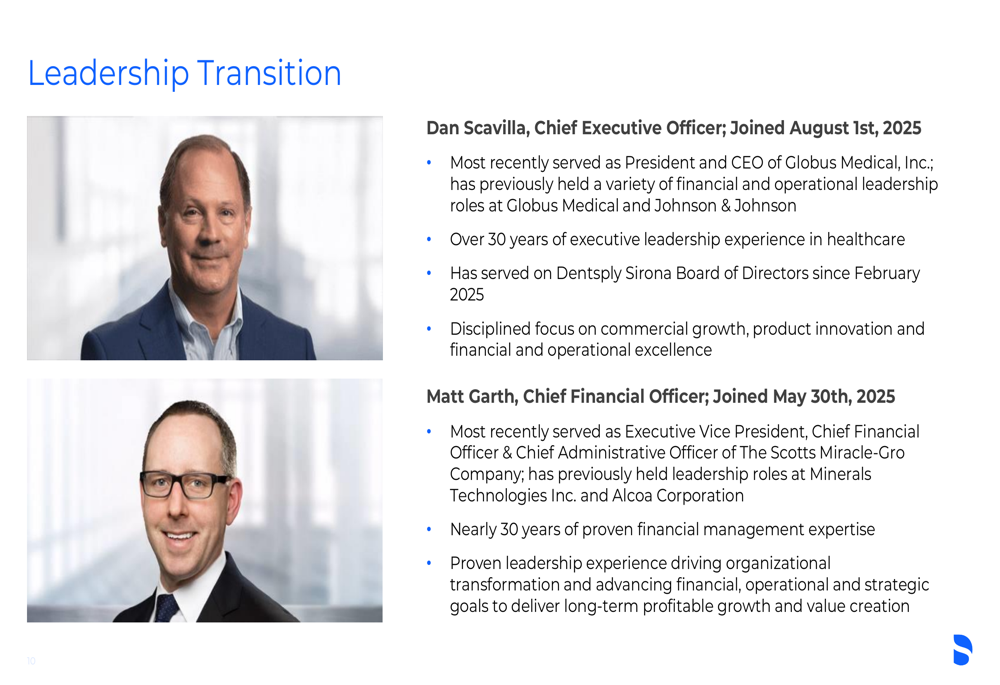

A significant development for Dentsply Sirona is the recent leadership transition, with Dan Scavilla joining as Chief Executive Officer on August 1, 2025, and Matt Garth assuming the role of Chief Financial Officer on May 30, 2025:

This new leadership team faces immediate challenges in stabilizing the organization and improving commercial execution, particularly in the U.S. market where sales declined most significantly. The company’s near-term priorities under the new leadership include driving commercial execution, engaging with stakeholders, stabilizing the organization through change, and accelerating results through focused investment.

Strategic Initiatives

Dentsply Sirona outlined its strategic roadmap focused on growth and operational efficiency:

The company’s strategy centers on achieving annual growth and margin commitments, enhancing and sustaining profitability, accelerating enterprise digitalization, winning in high-growth categories, and driving a high-performance culture. Key growth accelerators include innovation, clinical education, and commercial excellence, while foundational initiatives focus on ERP modernization, supply chain transformation, and SKU optimization.

This strategic approach appears to be yielding results on the margin front, as evidenced by the 360 basis point expansion in adjusted EBITDA margin, despite ongoing revenue challenges. The company’s focus on operational improvements and financial discipline is helping to offset top-line pressures.

Forward-Looking Statements

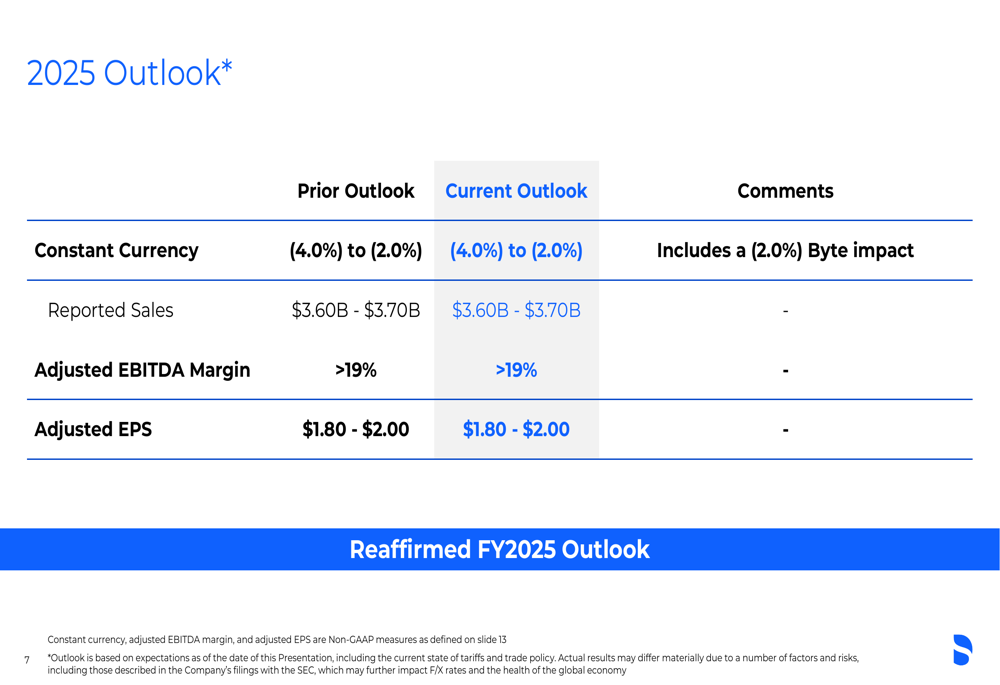

Dentsply Sirona maintained its full-year 2025 outlook despite the mixed Q2 results:

The company continues to project a constant currency sales decline of 2% to 4% for the full year, including a 2% impact from Byte. Reported sales are expected to range between $3.60 billion and $3.70 billion, with an adjusted EBITDA margin exceeding 19% and adjusted EPS between $1.80 and $2.00.

This maintained guidance suggests management confidence in the company’s ability to continue delivering margin expansion and EPS growth despite ongoing sales challenges. The outlook aligns with the company’s Q1 2025 guidance, indicating stability in its full-year expectations.

Conclusion

Dentsply Sirona’s Q2 2025 results present a mixed picture, with significant sales challenges, particularly in the U.S. market, offset by substantial improvements in profitability metrics. The company’s ability to expand margins and grow EPS despite revenue declines demonstrates effective cost management and operational efficiency.

The new leadership team faces the immediate challenge of stabilizing U.S. sales while maintaining the positive momentum in margin expansion. Investors will likely focus on whether the company can return to sales growth while sustaining its improved profitability metrics in upcoming quarters.

With the stock trading well below its 52-week high, market sentiment appears cautious despite the company’s operational improvements, suggesting investors remain concerned about the path to sustainable top-line growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.