Bitcoin set for a rebound that could stretch toward $100000, BTIG says

Introduction & Market Context

Desert Control AS (EURONEXT:DSRT) presented its Q2 2025 financial results on August 15, 2025, revealing a significant revenue decline despite ongoing expansion efforts in key markets. The company, which specializes in soil enhancement technology through its Liquid NanoClay (LNC) solution, saw its stock drop 11.89% following the announcement, closing at $4.88 near its 52-week low of $4.21.

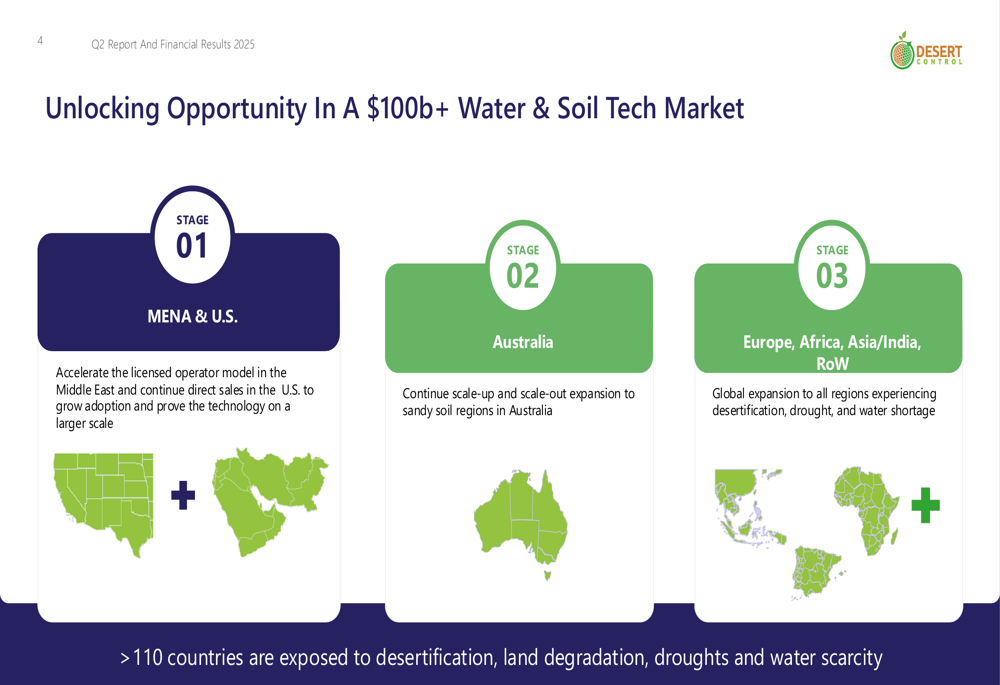

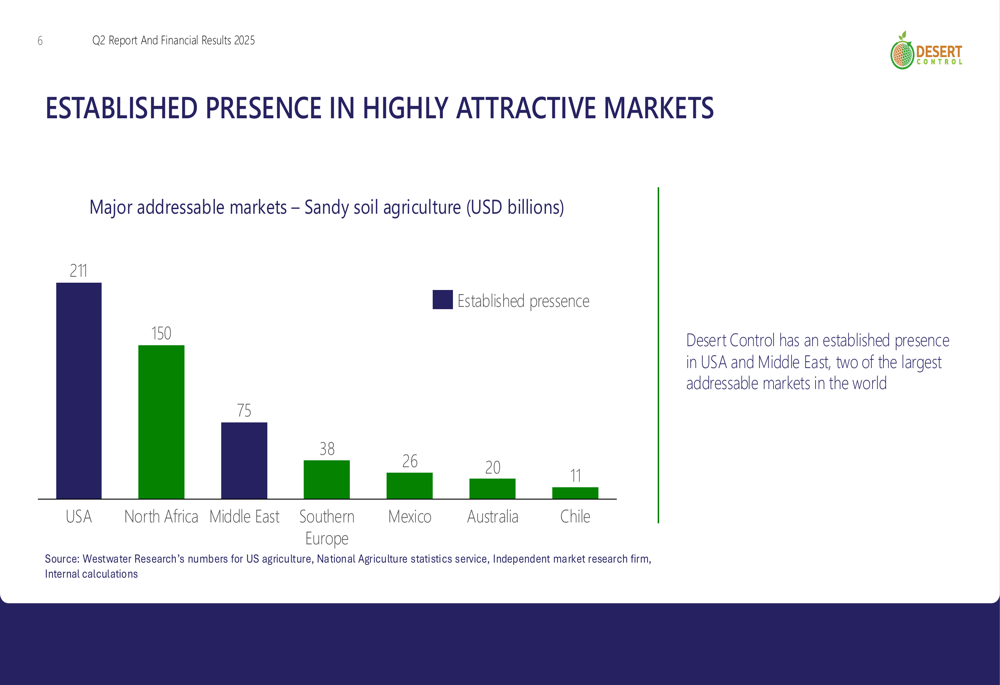

Desert Control positions itself in a substantial global market, targeting regions with sandy soils and water scarcity issues. The company's technology aims to improve soil structure, increase water efficiency, and enhance plant health across multiple sectors including agriculture, forestry, and landscaping.

As shown in the following global market opportunity breakdown:

The company is pursuing a phased expansion strategy, initially focusing on the Middle East and United States (Stage 1), followed by Australia (Stage 2), and eventually expanding to Europe, Africa, Asia, and other regions experiencing desertification and water shortages (Stage 3).

Quarterly Performance Highlights

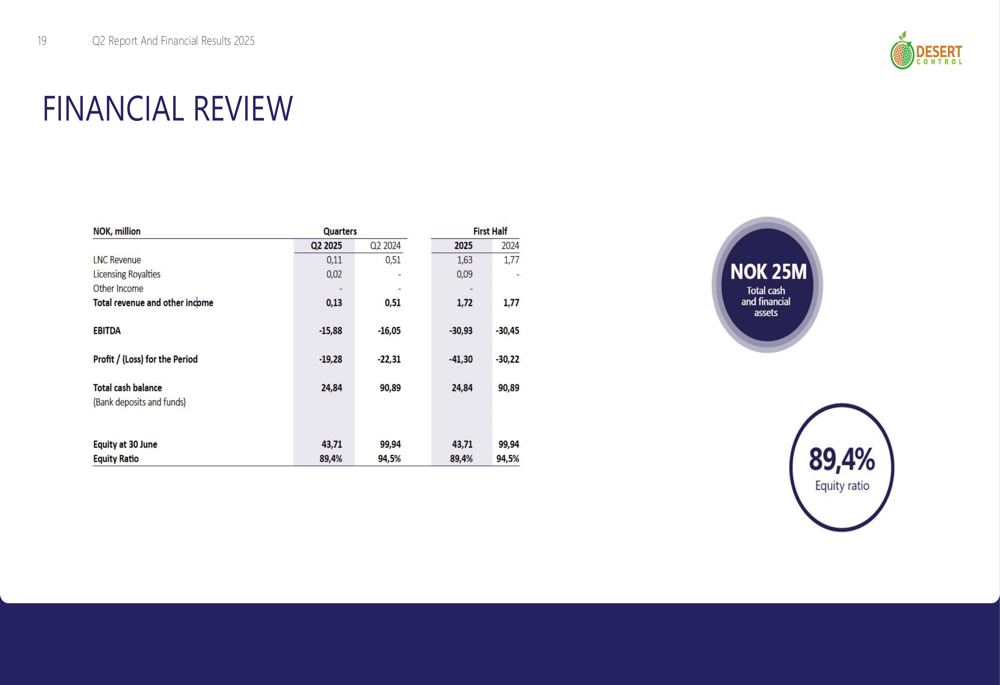

Desert Control's Q2 2025 financial results showed significant underperformance compared to both forecasts and year-over-year comparisons. The company reported total revenue of just $128,000 for the quarter, representing a 96.8% miss against the forecast of $4 million and a substantial decline from $507,000 in Q2 2024.

The financial results table below illustrates the company's performance metrics:

Key financial highlights include:

- LNC Revenue: $0.11 million in Q2 2025, down from $0.51 million in Q2 2024

- Total revenue: $0.13 million in Q2 2025, compared to $0.51 million in Q2 2024

- EBITDA: -$15.88 million in Q2 2025, slightly improved from -$16.05 million in Q2 2024

- Loss for the period: $19.28 million in Q2 2025, reduced from $22.31 million in Q2 2024

- Cash balance: $24.84 million, significantly down from $90.89 million in Q2 2024

Despite the revenue challenges, the company maintains a strong equity ratio of 89.4%, though this has decreased from 94.5% in the same period last year. The rapid cash burn rate remains a concern for investors, with cash reserves declining by approximately $66 million year-over-year.

Strategic Initiatives

Desert Control continues to focus on expanding its presence in the United States and Middle East markets, which represent significant addressable opportunities. The company highlighted several commercial applications and pilot projects during the quarter:

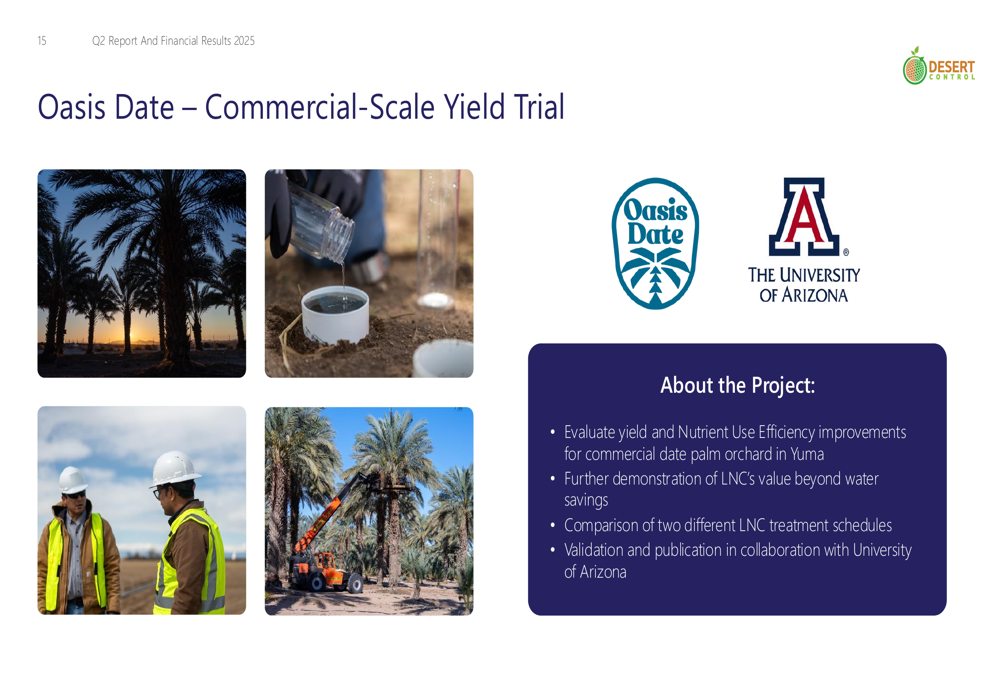

In the United States, Desert Control is targeting high-value agricultural segments in California and Arizona, including vineyards, tree nuts, and high-value crops, along with golf courses and landscaping applications. Key projects include:

- Anthony Vineyards: LNC application via drip irrigation system

- Oasis Date: Commercial-scale yield improvement trial in collaboration with University of Arizona

- California Almonds: First trial scheduled for Q3

- Multiple golf course applications including Woodland Hills Country Club and Mesa del Sol

The company's detailed project with Oasis Date demonstrates its focus on commercial validation:

In the Middle East, Desert Control's licensing partner Saudi Desert Control (SDC) completed its first revenue-generating application at Atlas Turf Arabia's turf farm outside Riyadh, marking a commercial entry into the Saudi market:

Detailed Financial Analysis

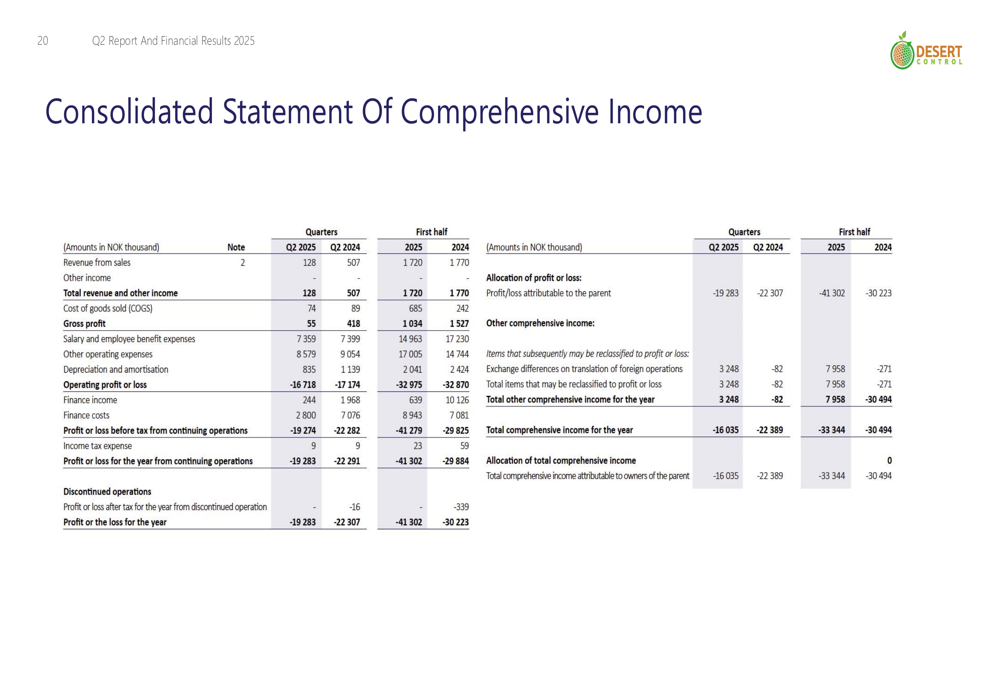

A deeper analysis of Desert Control's financial statements reveals concerning trends despite some positive indicators. The consolidated statement of comprehensive income shows the extent of the company's operating losses:

The company's operating loss for Q2 2025 stood at $16.72 million, slightly improved from $17.17 million in Q2 2024. However, the total loss for the period was $19.28 million, representing a burn rate that continues to deplete the company's cash reserves.

The balance sheet position, while still showing a strong equity ratio, reflects the ongoing cash consumption:

Total assets decreased from $97.32 million in Q2 2024 to $36.75 million in Q2 2025, primarily due to the reduction in cash and financial assets. This significant cash burn underscores the importance of accelerating commercial revenue generation to ensure long-term sustainability.

Forward-Looking Statements

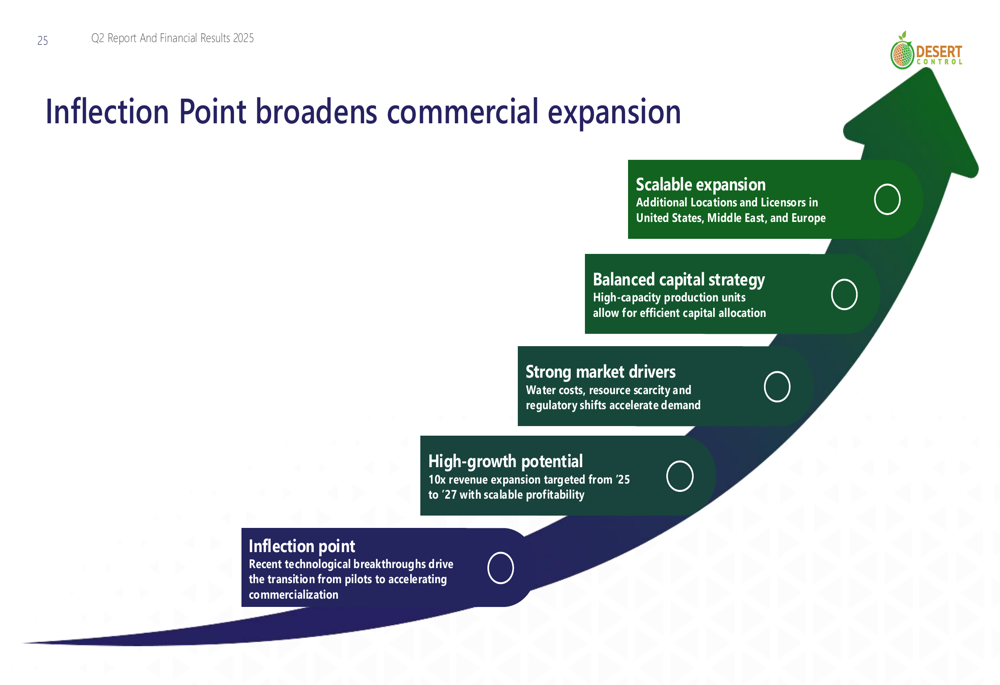

Despite current challenges, Desert Control maintains an optimistic outlook for future growth. The company is positioning itself at an "inflection point" for broader commercial expansion:

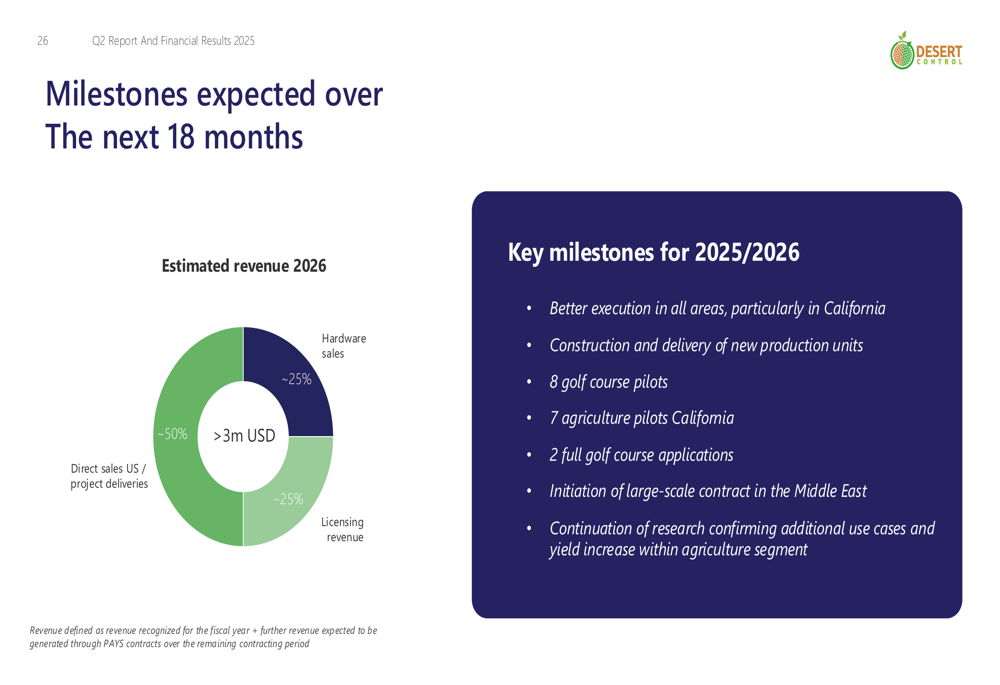

For 2026, Desert Control projects revenue exceeding $3 million, with approximately 50% coming from direct sales in the US, 25% from licensing revenue, and 25% from hardware sales:

Key milestones expected over the next 18 months include:

- Improved execution across all areas, particularly in California

- Construction and delivery of new production units

- 8 golf course pilots and 7 agricultural pilots in California

- 2 full golf course applications

- Initiation of large-scale contracts in the Middle East

- Continued research confirming additional use cases and yield increases

The company's strategic priorities for 2025/2026 focus on expanding its footprint in U.S. golf and landscaping, scaling deployments in high-value permanent crops, growing licensing revenues in the Middle East, and executing the commercial launch of next-generation production systems.

However, given the significant revenue miss in Q2 2025 and the rapid cash burn rate, investors may question the feasibility of these projections. The company will need to demonstrate accelerated commercial traction to achieve its ambitious revenue targets for 2026 and justify its current market positioning in what it describes as a $100+ billion addressable market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.