Street Calls of the Week

Introduction & Market Context

Devyser Diagnostics AB (STO:DVYSR) presented its second quarter 2025 earnings results on July 22, revealing a significant return to profitability alongside robust revenue growth. The diagnostic solutions provider has successfully executed on its reorganization strategy initiated in February, resulting in improved operational efficiency without compromising growth.

The company’s stock has seen a slight pullback of 0.67% since the earnings announcement, trading at 148.6 SEK as of August 15, though this follows an initial 8.03% surge immediately after the results were released. The current price remains close to its 52-week high of 155 SEK, reflecting continued investor confidence in Devyser’s growth trajectory.

Quarterly Performance Highlights

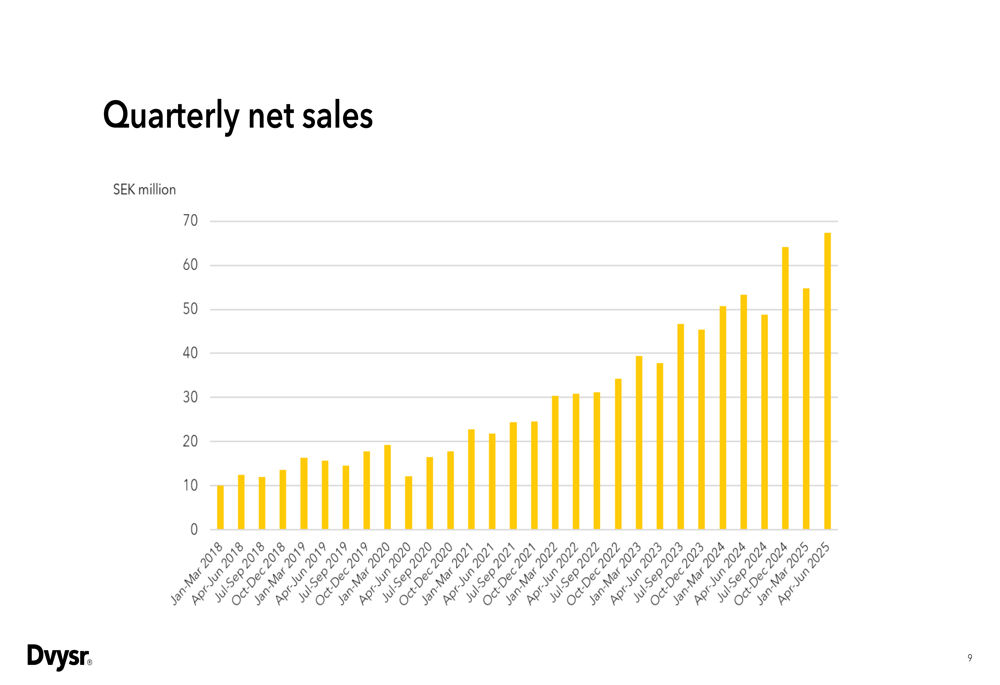

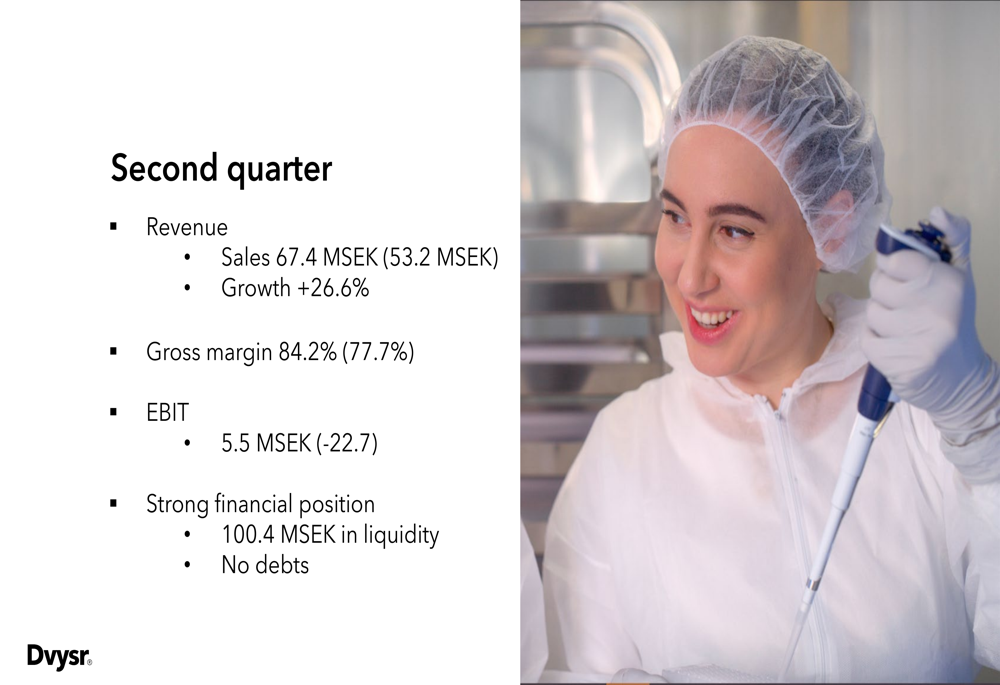

Devyser reported second quarter revenue of 67.4 MSEK, representing a 27% year-over-year increase from 53 MSEK in Q2 2024. This performance exceeded analyst expectations of 61.93 MSEK. The company also achieved a gross margin of 84.2%, a significant improvement from 77.7% in the same period last year.

In a major turnaround, Devyser posted an EBIT of 5.5 MSEK, including 1.8 MSEK in one-off expenses, compared to a loss of 22.7 MSEK in Q2 2024. The company maintains a strong financial position with 100.4 MSEK in cash and no debt.

As shown in the following chart of quarterly net sales, Devyser has maintained a consistent upward trajectory in revenue growth since 2018:

Geographic Sales Analysis

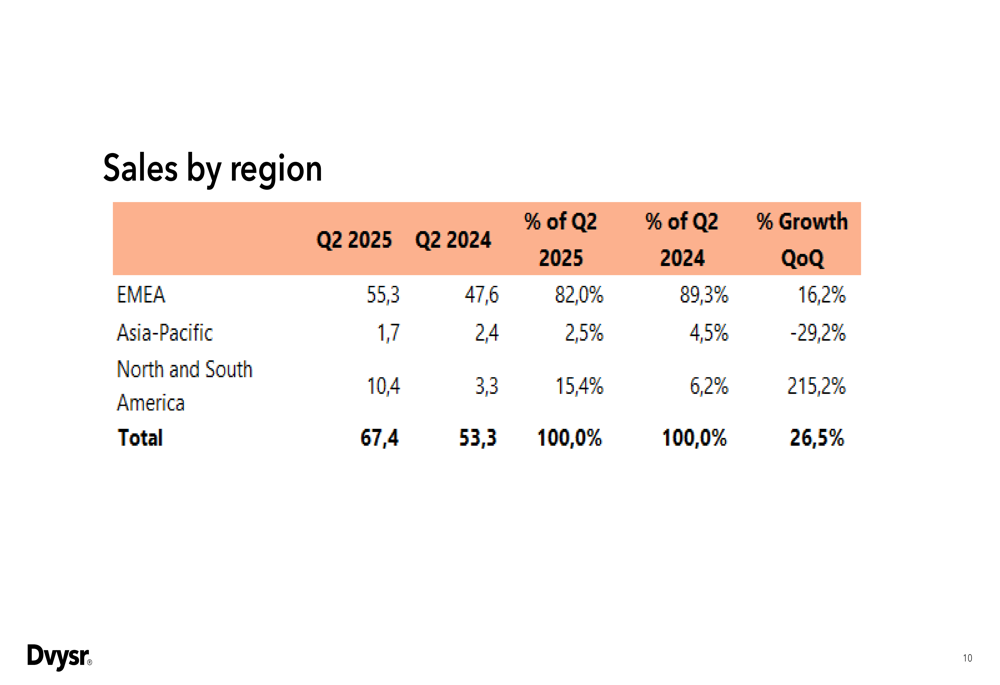

Devyser’s geographic sales breakdown reveals contrasting performance across regions. While EMEA remains the company’s largest market at 82% of total sales with 16.2% year-over-year growth, the most dramatic expansion occurred in the Americas, where sales surged by 215.2% compared to Q2 2024.

The regional sales breakdown is illustrated in this detailed table:

The North American market has become increasingly important to Devyser’s growth strategy. The company’s Atlanta-based Devyser Genomic Laboratories is progressing with its timeline for reimbursement, while the RHD testing solution is positioned as a potential "gamechanger" in the US market, targeting approximately 550,000 patients annually.

Meanwhile, the Asia-Pacific region experienced a 29.2% decline in sales, representing just 2.5% of total revenue in Q2 2025, down from 4.5% in the same period last year.

Sales Channel Performance

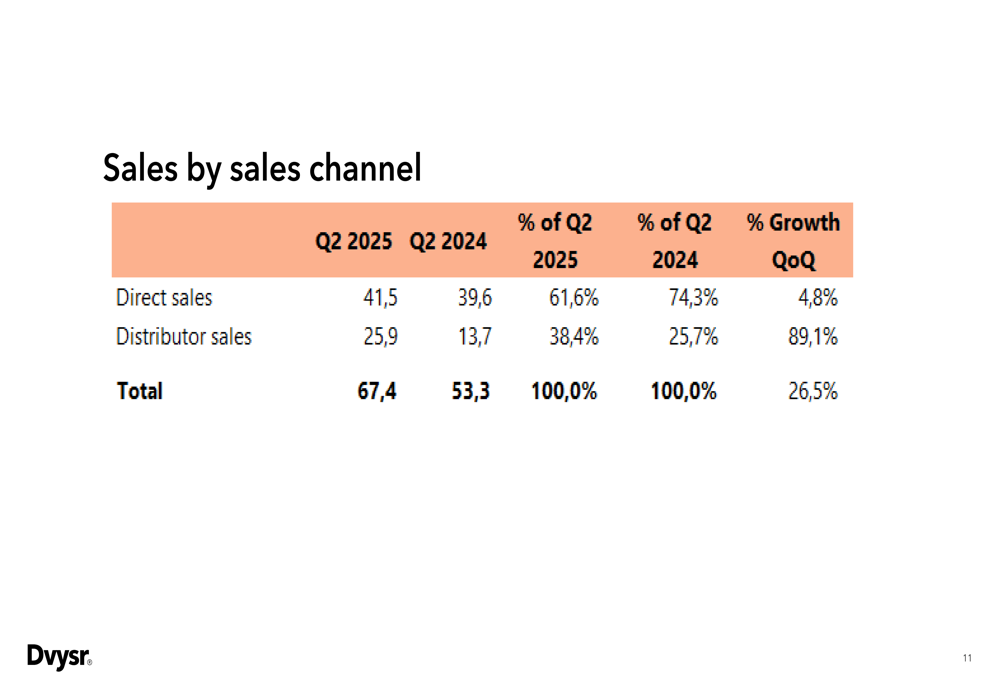

Devyser’s sales channel analysis reveals a significant shift in distribution strategy, with distributor sales growing by 89.1% year-over-year while direct sales increased by a more modest 4.8%. This changing sales mix is evident in the following breakdown:

Despite the stronger growth in distributor sales, direct sales still account for the majority (61.6%) of Devyser’s revenue. The robust growth in distributor channels suggests successful expansion of the company’s partner network, particularly in new markets.

Product Launch Strategy

The second quarter saw Devyser launch three significant new products, enhancing its market offerings:

1. RHD IVDR (June 3): Achieved the highest risk classification under EU regulation, demonstrating capability to support the development of any IVD product regardless of risk class.

2. HLA loss (June 26): Addresses important clinical needs in patients with malignant disease after stem cell transplantation.

3. Genetic Blood Typing (June 30): Offers potential to transform the field of transfusion medicine.

These product launches are part of Devyser’s comprehensive commercial strategy, which has yielded several positive outcomes as summarized in this commercial recap:

Strategic Partnerships

Devyser’s collaboration with Thermo Fisher Scientific continues to strengthen, with Q2 showing strong order intake and revenue contribution. The partnership, focused on transplantation products, has increased customer confidence through joint presence at industry events and growing data evidence supporting ddcfDNA testing.

The companies are also making progress on regulatory approvals, as outlined in this partnership update:

In the US market, Devyser is pursuing multiple strategic initiatives, including commercializing its RHD test through one of the largest service companies during Q3 and advancing partnerships for its CLIA lab service.

Forward-Looking Statements

Looking ahead, Devyser’s management emphasized three key priorities: executing on its updated strategy, continuing to improve organizational efficiency, and maintaining its path to profitability and positive cash flow.

The company’s comprehensive financial summary highlights both its current performance and foundation for future growth:

Fredrik Dahl, Interim CEO, stated during the earnings call that the company is "turning around towards profitability" following the completion of its reorganization initiative. The updated product roadmap and improved internal processes are expected to create "an organization that is better balanced and efficient - without compromising growth."

With its strong cash position, expanding product portfolio, and growing presence in the North American market, Devyser appears well-positioned to continue its growth trajectory while improving profitability metrics in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.