Five things to watch in markets in the week ahead

DexCom Inc (NASDAQ:DXCM) reported accelerating revenue growth in its first quarter of 2025, though the continuous glucose monitoring (CGM) leader faces margin pressures as it expands its product portfolio. The company’s shares rose 2.48% to $72 in after-hours trading following the May 1 release.

Quarterly Performance Highlights

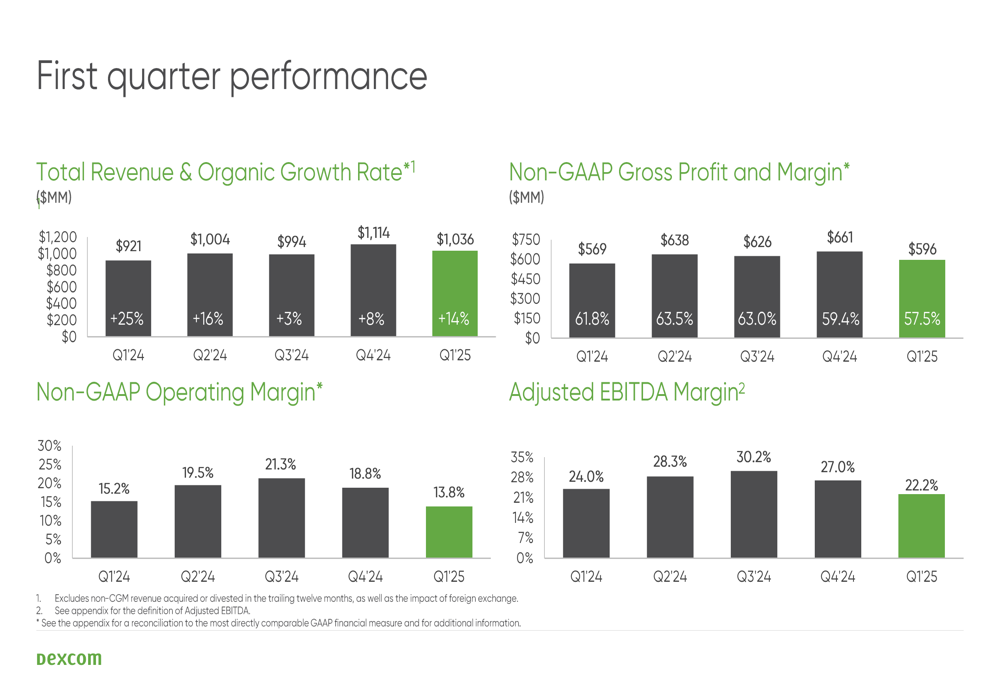

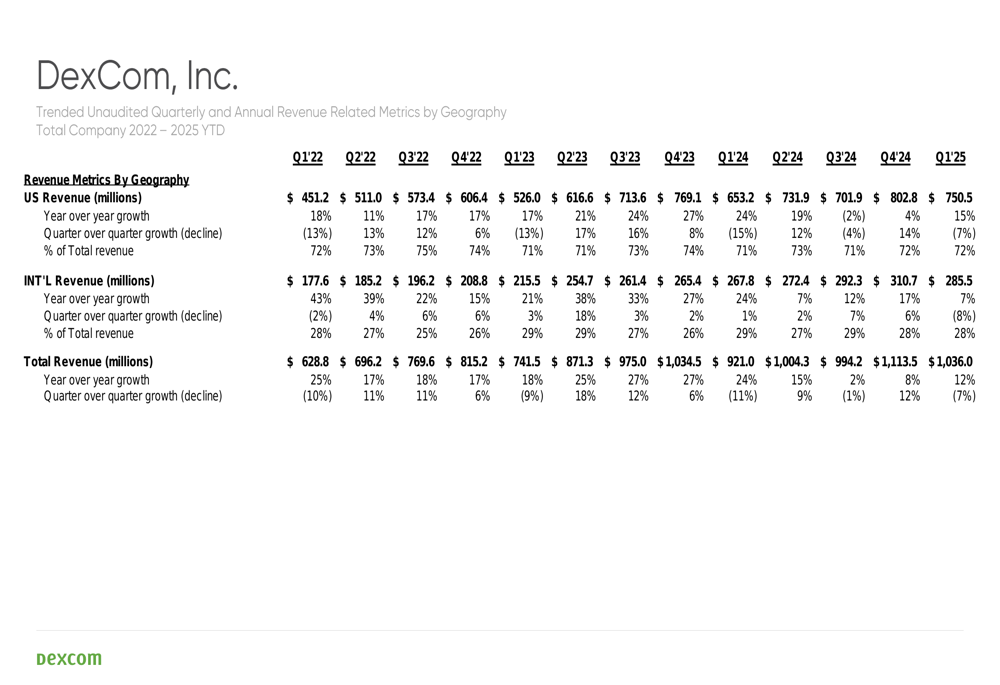

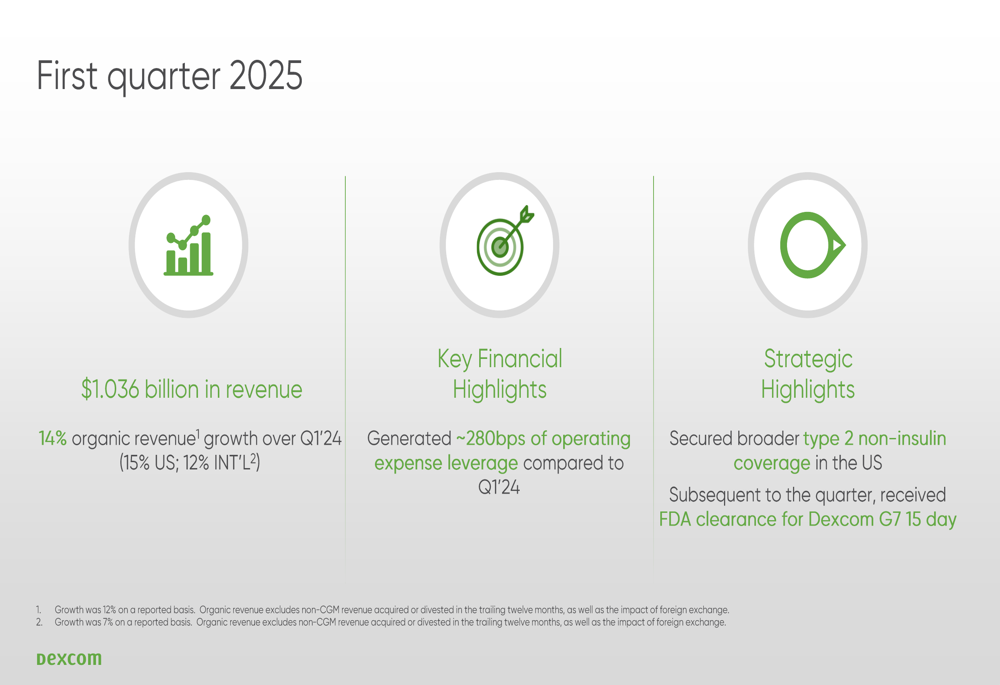

DexCom delivered $1.036 billion in revenue for Q1 2025, representing 14% organic growth compared to the same period last year. This marks a significant acceleration from the 8% organic growth reported in Q4 2024. U.S. revenue, which accounts for 72.4% of the total, grew 15% year-over-year, while international revenue increased by 12% on an organic basis.

The company highlighted two key strategic achievements during the quarter: securing broader coverage for type 2 non-insulin patients in the U.S. market and receiving FDA clearance for its extended-wear Dexcom G7 15-day version shortly after the quarter ended.

As shown in the following quarterly performance chart, DexCom’s revenue growth has rebounded from the slower growth seen in mid-2024:

Detailed Financial Analysis

Despite the strong revenue growth, DexCom experienced margin pressure across several metrics. The non-GAAP gross profit margin declined to 57.5% in Q1 2025 from 61.8% in the same period last year. Similarly, non-GAAP operating margin fell to 13.8% from 15.2% year-over-year, while adjusted EBITDA margin decreased to 22.2% from 24.0%.

The company did report an improvement in operating expense leverage by approximately 280 basis points compared to Q1 2024, suggesting efforts to control costs amid the margin challenges.

GAAP net income for the quarter was $105.4 million, down from $146.4 million in Q1 2024, resulting in diluted earnings per share of $0.27 compared to $0.36 a year ago. On a non-GAAP basis, net income was relatively stable at $127.7 million versus $128.2 million in Q1 2024, with diluted EPS unchanged at $0.32.

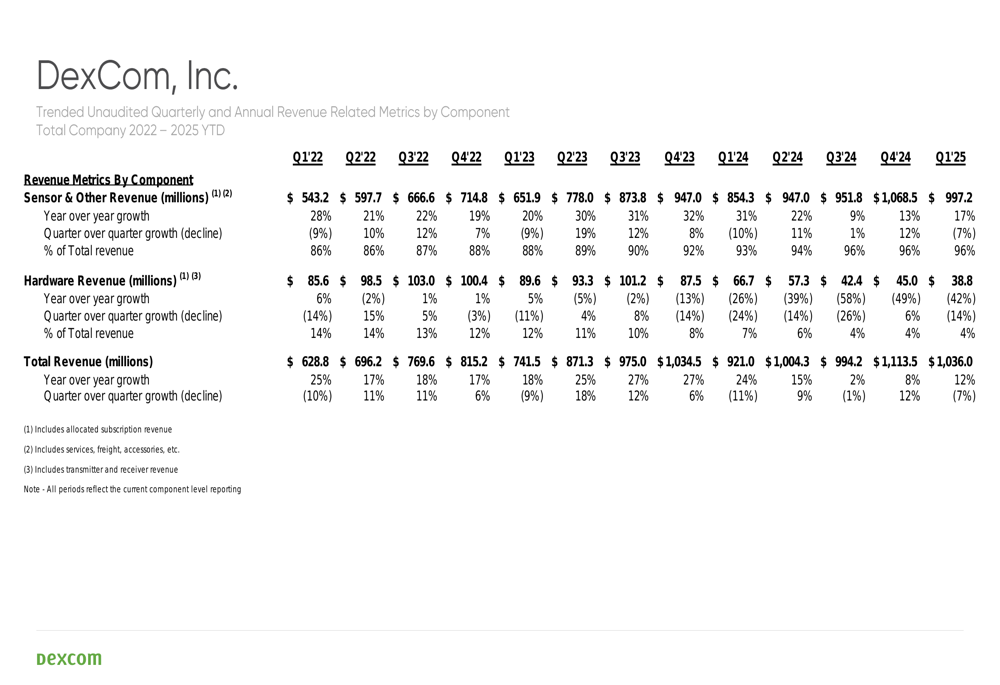

A closer examination of revenue components reveals divergent trends. Sensor and other revenue, which constitutes 96.3% of total revenue, grew 17% year-over-year to $997.2 million. However, hardware revenue declined significantly by 42% to $38.8 million, reflecting the company’s business model shift toward recurring sensor revenue.

The following chart breaks down DexCom’s revenue by geography, showing the company’s continued strong performance in both domestic and international markets:

Strategic Initiatives

DexCom continues to expand its addressable market by targeting different segments of the diabetes population. The company’s efforts to secure broader coverage for type 2 non-insulin patients in the U.S. represent a significant opportunity, as this patient population is substantially larger than the traditional insulin-using market.

The FDA clearance for the extended-wear Dexcom G7 15-day version is another strategic milestone. This longer-lasting sensor could improve user convenience and potentially reduce costs, enhancing the company’s competitive position in the increasingly crowded CGM market.

DexCom is also advancing its Stelo product, which targets adults with pre-diabetes or type 2 diabetes who don’t use insulin. This represents a substantial market expansion opportunity, though the previous earnings call noted that initial usage had not shown significant conversions from pre-diabetes to Type 2 diabetes.

The following chart illustrates the company’s revenue breakdown by product component, highlighting the growing dominance of sensor revenue:

Forward-Looking Statements

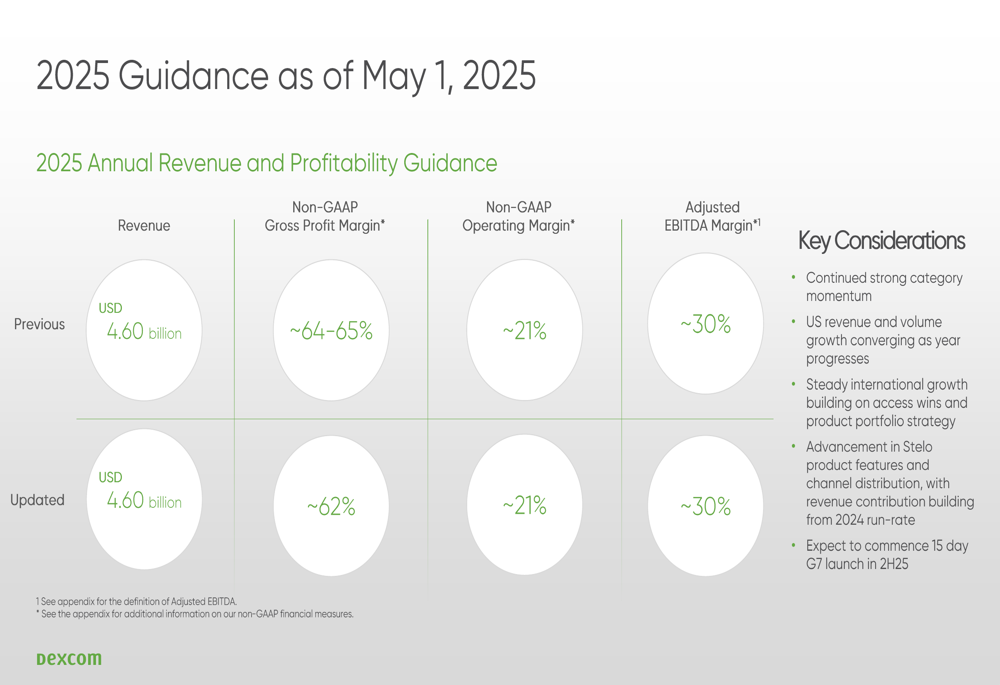

DexCom maintained its 2025 annual revenue guidance of $4.60 billion but revised its non-GAAP gross profit margin expectations downward to approximately 62% from the previous guidance of 64-65%. The company kept its non-GAAP operating margin and adjusted EBITDA margin guidance unchanged at approximately 21% and 30%, respectively.

The company highlighted several key considerations for its 2025 outlook, including continued strong category momentum, U.S. revenue and volume growth, steady international growth, advancement in Stelo product features and distribution, and plans to commence the 15-day G7 launch in the second half of 2025.

As shown in the following guidance slide, DexCom’s profitability expectations have been adjusted to reflect current market conditions:

DexCom’s Q1 2025 results demonstrate the company’s ability to accelerate revenue growth despite competitive pressures in the CGM market. However, the declining margins suggest challenges in maintaining profitability while expanding into new market segments. The upcoming launch of the 15-day G7 sensor and continued expansion of coverage for type 2 non-insulin patients could provide additional growth catalysts in the coming quarters.

The company’s first quarter highlights, including key financial metrics and strategic achievements, are summarized in the following slide:

With the CGM market continuing to expand beyond traditional insulin-using patients, DexCom appears well-positioned to capitalize on the broader opportunity. However, investors will likely focus on the company’s ability to improve margins while maintaining its growth trajectory in the increasingly competitive diabetes technology landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.