Tonix Pharmaceuticals stock halted ahead of FDA approval news

Introduction & Market Context

DNB Group, Norway’s largest financial services group, presented its first quarter 2025 results on May 7, showcasing continued strong performance amid a robust Norwegian economic backdrop. The bank reported a return on equity of 15.9% for the quarter, with earnings per share reaching NOK 7.04, up 8.6% from the same period last year.

CEO Kjerstin R. Braathen highlighted the bank’s strategic positioning in a Norwegian economy characterized by moderate growth and declining inflation. "We are one of the most robust and best capitalized banks operating in one of the most resilient economies in the world," Braathen noted during the presentation.

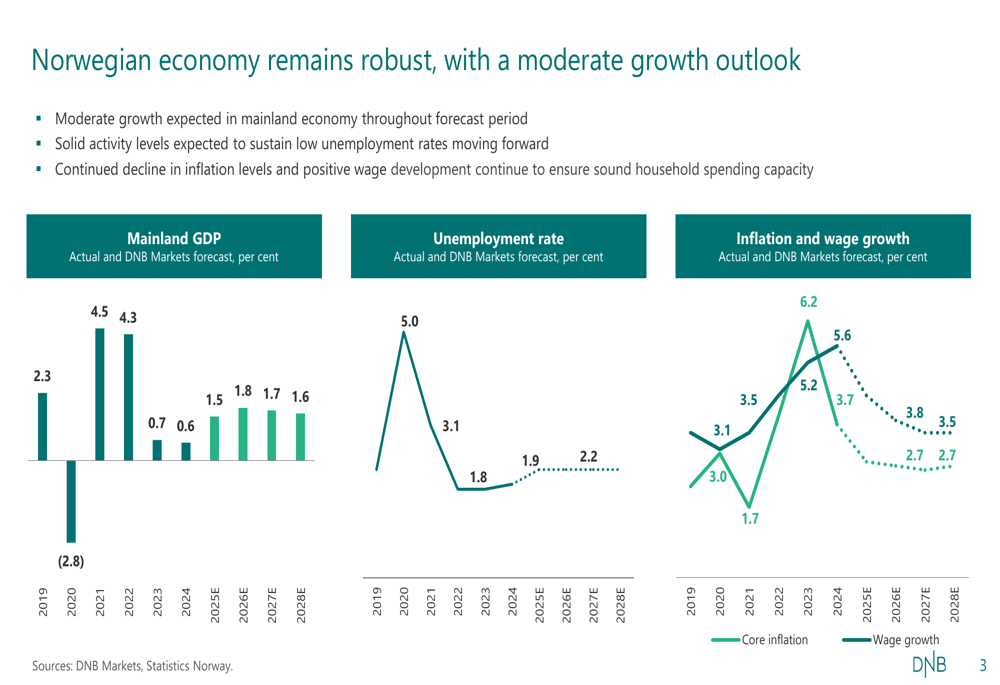

The Norwegian economy continues to show stability with mainland GDP growth expected to moderate to 1.6% by 2026, while unemployment remains low at around 2.2%. This economic resilience provides a solid foundation for DNB’s operations.

Quarterly Performance Highlights

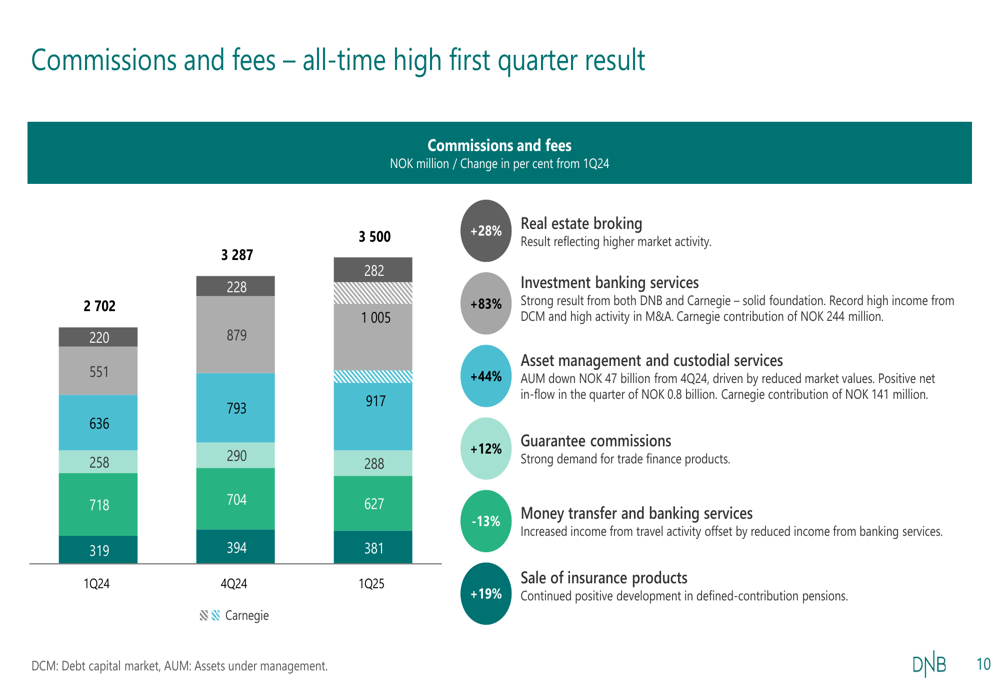

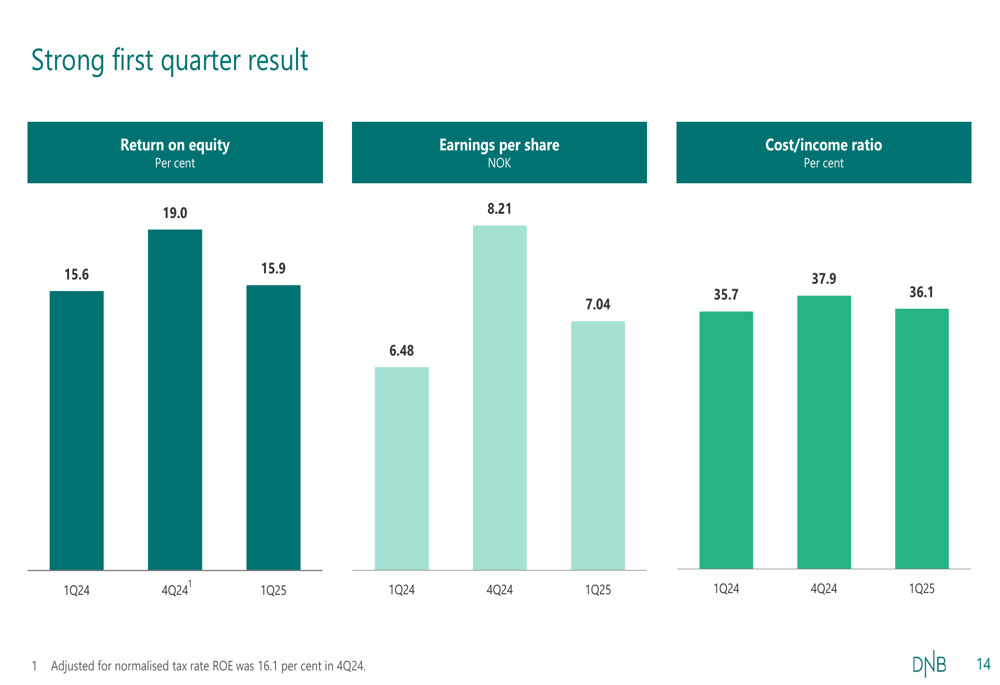

DNB delivered a profit of NOK 10.8 billion for Q1 2025, maintaining a strong return on equity of 15.9% despite slight pressure on net interest income. The bank’s performance was bolstered by significant growth in commission and fee income, which reached an all-time high for a first quarter.

Net interest income decreased 1.8% from the previous quarter but increased 5.7% year-over-year. This quarterly decline was primarily attributed to fewer interest days and reduced treasury contributions, partially offset by profitable volume growth.

The standout performer was net commissions and fees, which surged 29.5% compared to Q1 2024, driven by exceptional growth across multiple business lines. Investment banking services saw the most dramatic increase at 83%, while real estate broking and asset management services grew by 28% and 44% respectively.

As shown in the following chart of commission and fee income:

The bank maintained operational efficiency with a cost-to-income ratio of 36.1%, slightly higher than the 35.7% reported in Q1 2024 but improved from 37.9% in Q4 2024. Operating expenses reflected both the integration of Carnegie costs for one month and ongoing efficiency measures.

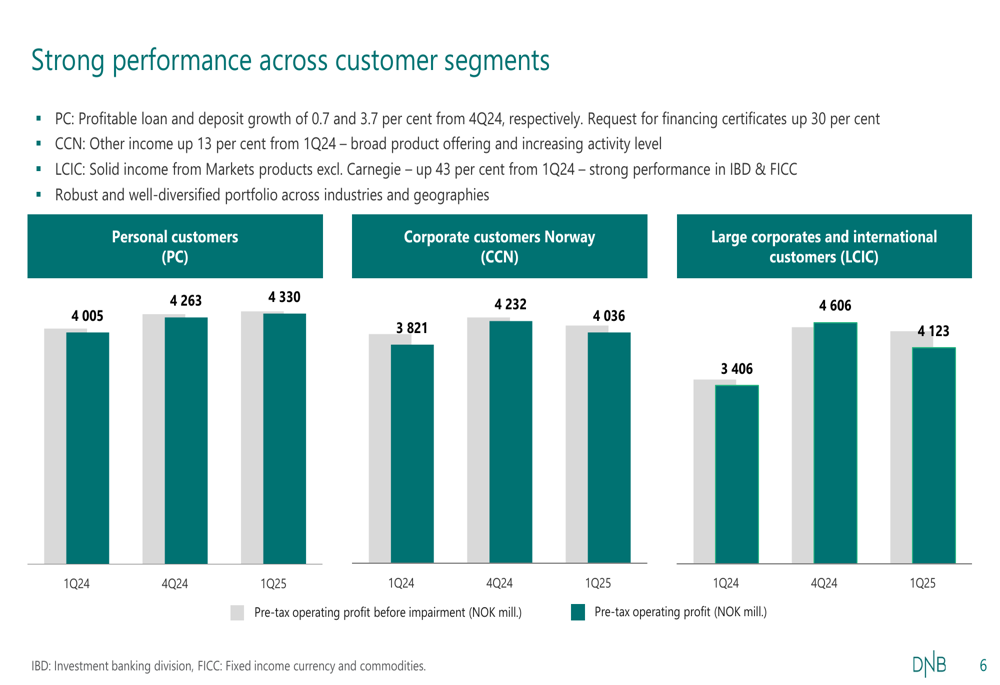

Pre-tax operating profit improved across all customer segments compared to the previous year, with particularly strong growth in the Large Corporates and International Customers segment, which saw a 21% increase from Q1 2024.

Strategic Initiatives

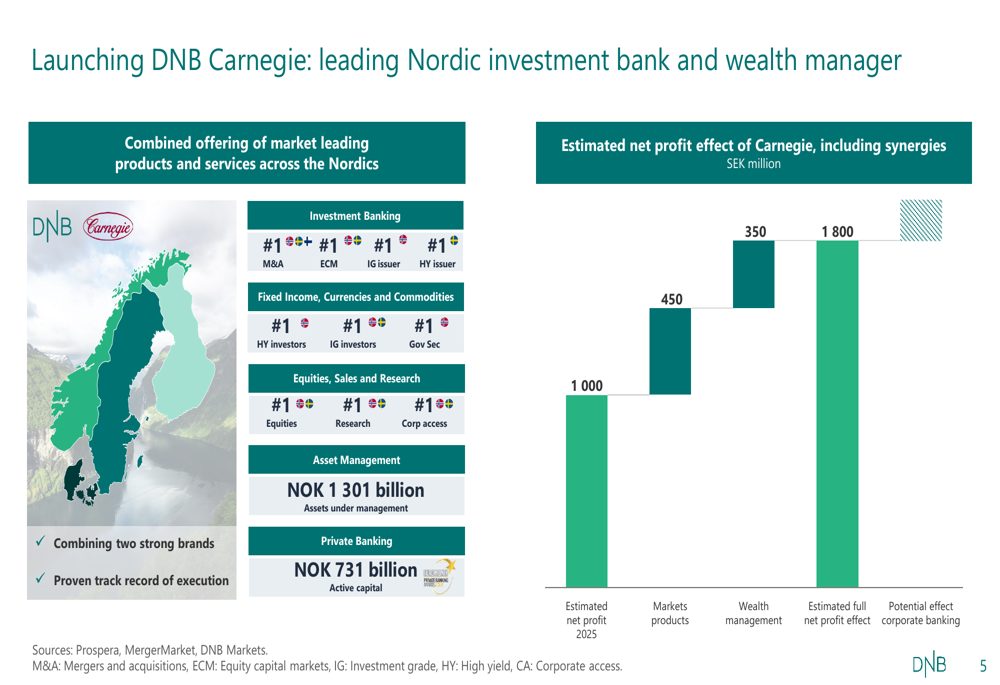

The quarter marked a significant milestone for DNB with the completion of the Carnegie acquisition and the launch of DNB Carnegie, positioned as a leading Nordic investment bank and wealth manager. This strategic move establishes DNB as a top player across various investment banking categories throughout the Nordic region.

The combined entity brings together DNB’s strong banking capabilities with Carnegie’s investment expertise, creating a powerhouse with NOK 1,301 billion in asset management and NOK 731 billion in private banking active capital. Management projects substantial profit growth from this acquisition, with estimated net profit effect including synergies expected to grow from 1,000 to 1,800 (in unspecified units, likely NOK million).

The following image illustrates the strategic positioning and expected benefits of the DNB Carnegie launch:

CFO Ida Lerner addressed the financial impact of the acquisition, noting: "The Carnegie transaction is expected to yield revenue synergies of SEK 800 million over the next 2-3 years, with estimated one-off costs of approximately $250 million related to the integration."

Detailed Financial Analysis

DNB maintained a solid balance sheet with modest growth in both loans and deposits. Currency-adjusted loan growth was 0.5% for the quarter, while currency-adjusted deposit growth reached a more robust 3.8%.

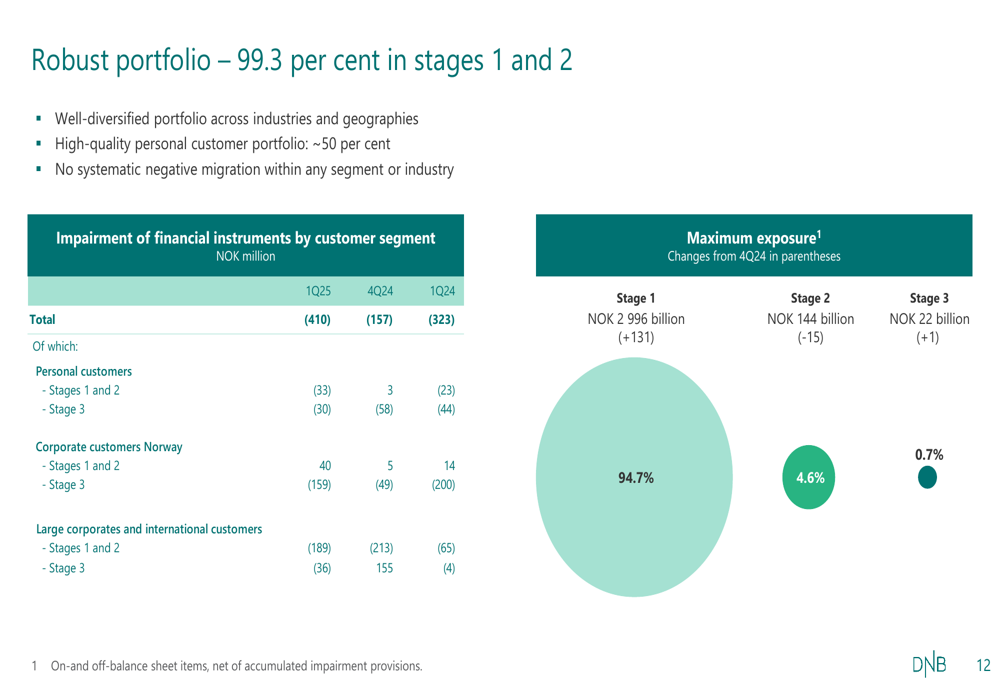

The bank’s loan portfolio remained well-diversified across industries and geographies, with 99.3% classified in stages 1 and 2, indicating strong credit quality. Impairment provisions for the quarter totaled NOK 410 million, reflecting the bank’s prudent risk management in an uncertain economic environment.

The following chart demonstrates the robust quality of DNB’s portfolio:

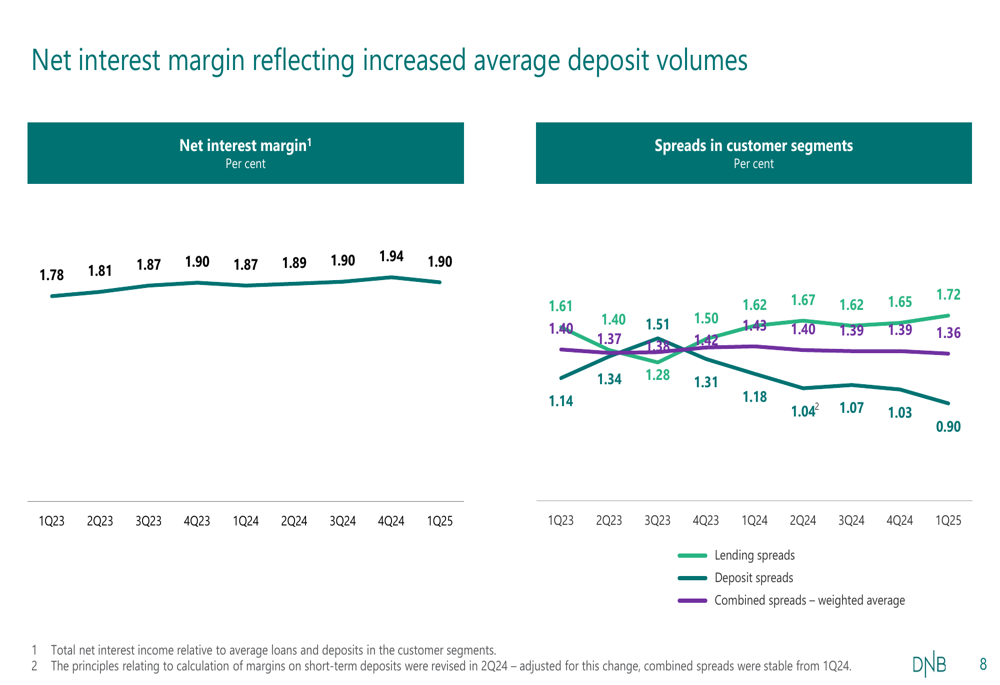

Net interest margin showed slight compression, continuing a trend observed in recent quarters as competitive pressures and market conditions affected spreads. The combined spread (weighted average) declined from 1.14% to 0.90% over the period shown.

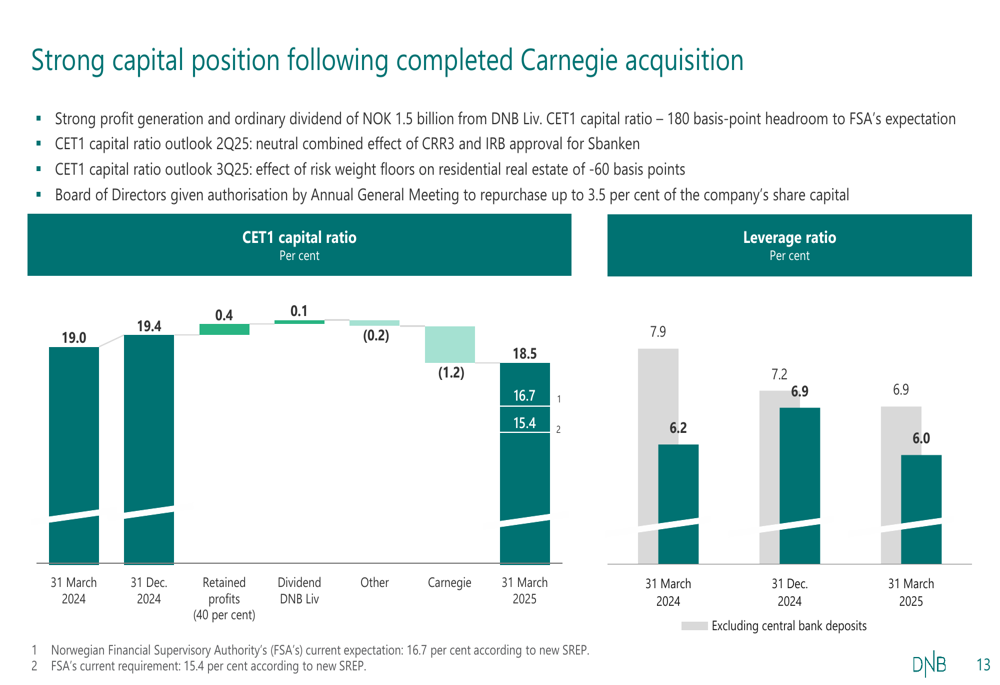

Capital ratios remained strong despite the impact of the Carnegie acquisition. The CET1 capital ratio stood at 18.5% as of March 31, 2025, compared to 19.4% at the end of 2024 and 19.0% a year earlier. This positions DNB well above regulatory requirements and provides flexibility for potential share buybacks, for which the board has received authorization.

Forward-Looking Statements

Looking ahead, DNB expressed confidence in its strategic positioning while acknowledging potential challenges. The bank anticipates continued growth in fees and commissions, expecting an annual increase of over 9%, particularly as the full benefits of the Carnegie acquisition materialize.

Management highlighted several areas of focus for the coming quarters:

1. Integration of Carnegie operations to realize projected synergies

2. Preparation for regulatory changes in residential real estate risk weights

3. Planned application for a share buyback of up to 1%

4. Continued commitment to the bank’s dividend policy

The bank’s performance metrics show consistent improvement over time, with earnings per share growing from NOK 6.48 in Q1 2024 to NOK 7.04 in Q1 2025, despite a sequential decline from the exceptionally strong Q4 2024 (NOK 8.21).

DNB remains well-positioned in the Norwegian market, with built-in economic stabilizers providing a buffer against potential global economic headwinds. The bank’s diversified revenue streams, particularly the growing contribution from fee-based income, offer resilience against potential pressure on interest margins as central banks potentially adjust policy rates.

As CFO Ida Lerner noted, "We continue to see that the majority of our customers stick to their long-term savings schemes," indicating stable customer relationships that should support ongoing growth in the bank’s wealth management and investment banking operations.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.