JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Donegal Group Inc. (NASDAQ:DGICA) released its first quarter 2025 investor presentation on April 24, showcasing significant improvements in profitability metrics and continued progress on its strategic initiatives. The regional insurer, which operates across Mid-Atlantic, Midwestern, Southern, and Southwestern states through approximately 2,100 independent agencies, reported a dramatic turnaround in performance compared to the same period last year.

The company’s stock closed at $18.55 on April 23, 2025, near its 52-week high of $19.87, with after-market trading showing a 3.34% increase to $19.17. This positive market reaction reflects the strong quarterly results detailed in the presentation.

Quarterly Performance Highlights

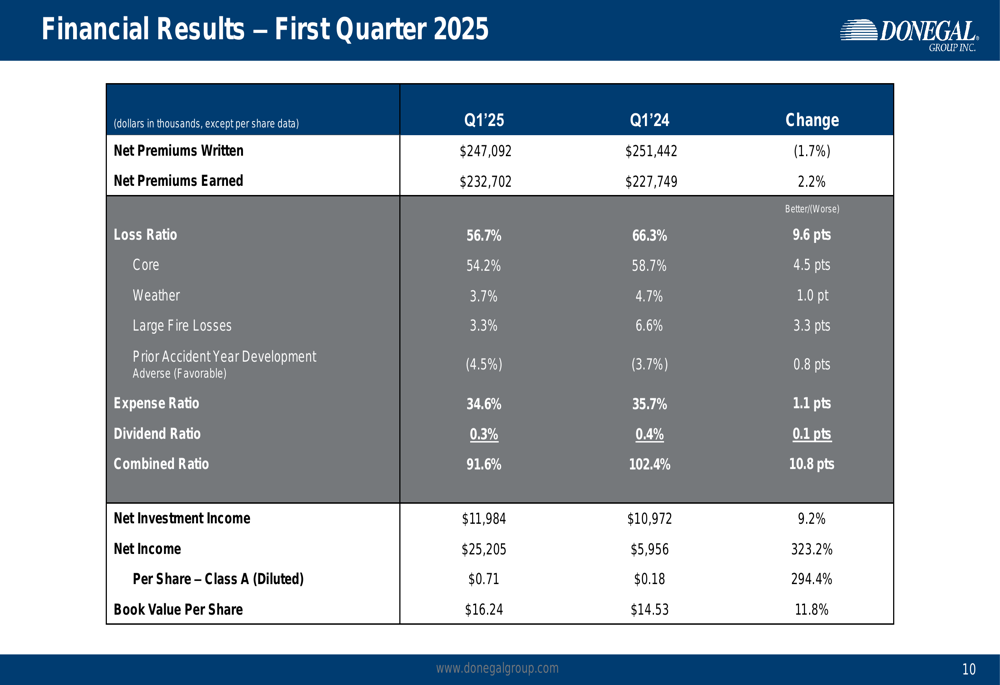

Donegal Group reported exceptional first quarter results, with net income soaring to $25.2 million, representing a 323.2% increase from $6.0 million in Q1 2024. Diluted earnings per Class A share reached $0.71, up 294.4% from $0.18 in the prior-year period.

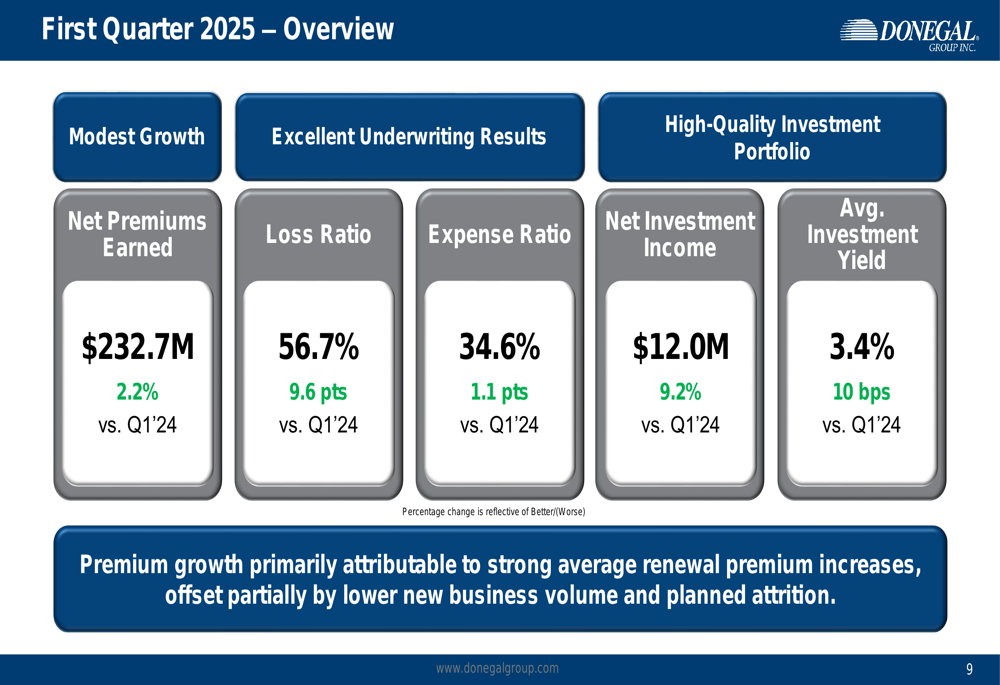

This remarkable improvement was driven by a significantly enhanced combined ratio of 91.6%, a 10.8 percentage point improvement from 102.4% in Q1 2024. The loss ratio decreased by 9.6 points to 56.7%, while the expense ratio improved by 1.1 points to 34.6%.

As shown in the following comprehensive financial results table:

Net premiums earned increased by 2.2% to $232.7 million, while net investment income grew by 9.2% to $12.0 million. The book value per share rose to $16.24, an 11.8% increase from $14.53 in Q1 2024, reflecting both operational improvements and investment gains.

The first quarter overview highlights these key metrics and their year-over-year changes:

Business Mix and Strategic Direction

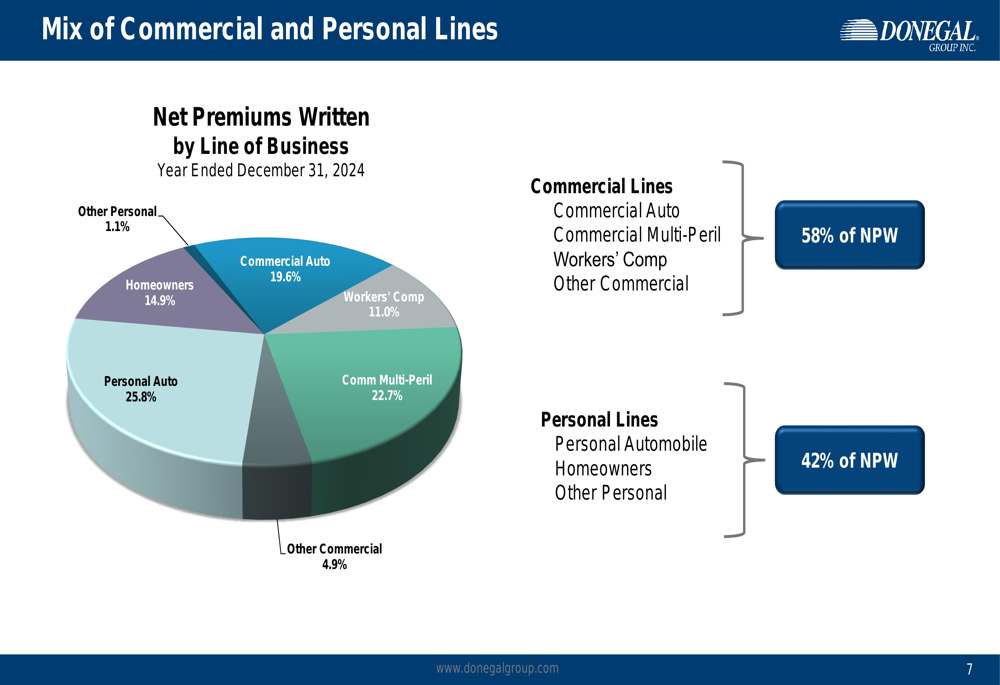

Donegal continues to execute its strategy of emphasizing commercial lines growth while maintaining a profitable personal lines book. Commercial lines now represent 58% of net premiums written, with personal lines accounting for 42%. This distribution reflects the company’s ongoing strategic shift.

The following chart illustrates the company’s business mix by line:

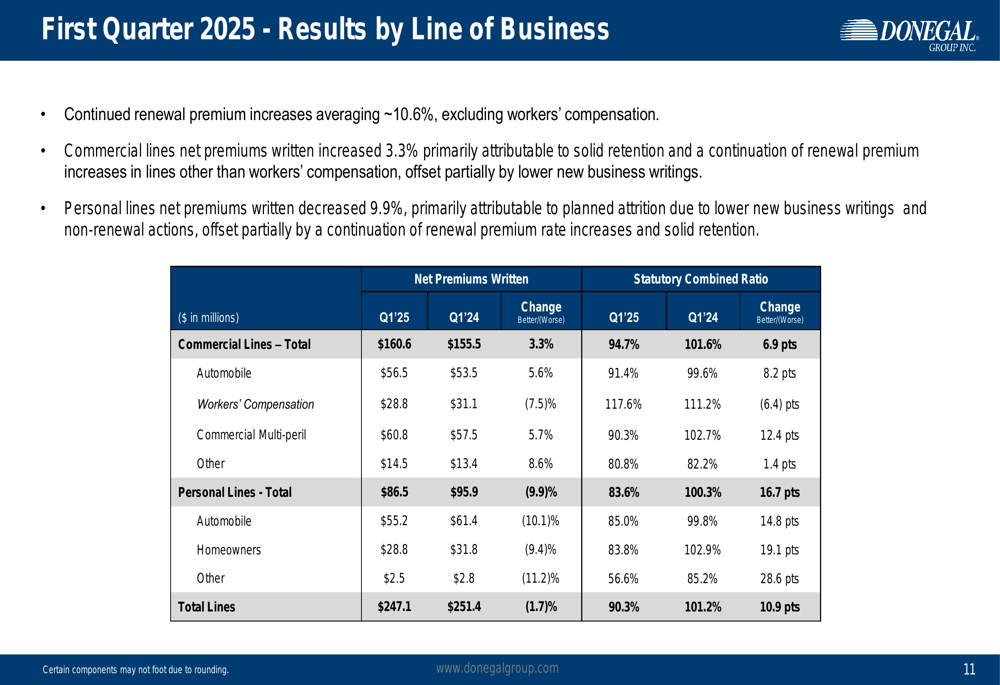

In Q1 2025, commercial lines net premiums written increased by 3.3% to $160.6 million, while personal lines decreased by 9.9% to $86.5 million. This decline in personal lines was described as "planned attrition" in the presentation, consistent with the company’s strategic direction.

The statutory combined ratio for commercial lines improved to 94.7% from 101.6% in Q1 2024, while the personal lines combined ratio showed an even more dramatic improvement to 83.6% from 100.3%.

The detailed breakdown by line of business reveals these improvements:

The company reported renewal premium increases averaging approximately 10.6% (excluding workers’ compensation), which contributed to the improved underwriting results. Donegal also noted that it completed strategic non-renewal actions in Georgia and Alabama during 2024, continuing the geographic repositioning mentioned in previous earnings reports.

Investment Strategy and Results

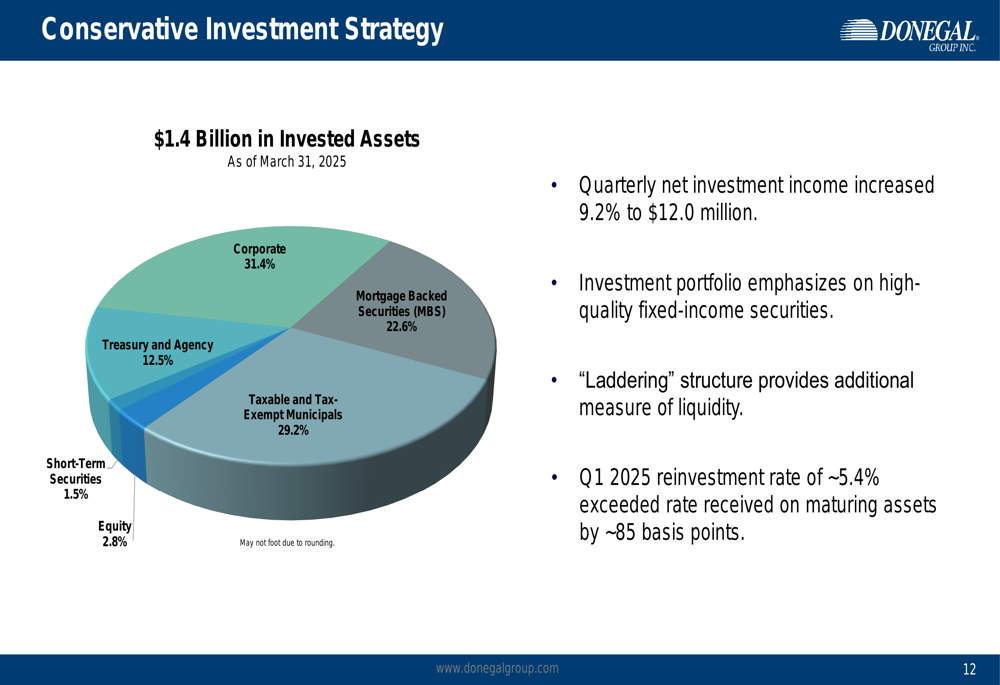

Donegal maintains a conservative investment approach, with a portfolio valued at $1.4 billion as of March 31, 2025. The investment strategy emphasizes high-quality fixed-income securities with a "laddering" structure to provide additional liquidity.

The company’s asset allocation is illustrated in the following chart:

The investment portfolio generated $12.0 million in quarterly income, a 9.2% increase from Q1 2024. The average investment yield rose to 3.4%, up 10 basis points year-over-year. Management highlighted that the Q1 2025 reinvestment rate of approximately 5.4% exceeded the rate received on maturing assets by about 85 basis points, suggesting continued improvement in investment income in future quarters.

Valuation and Competitive Position

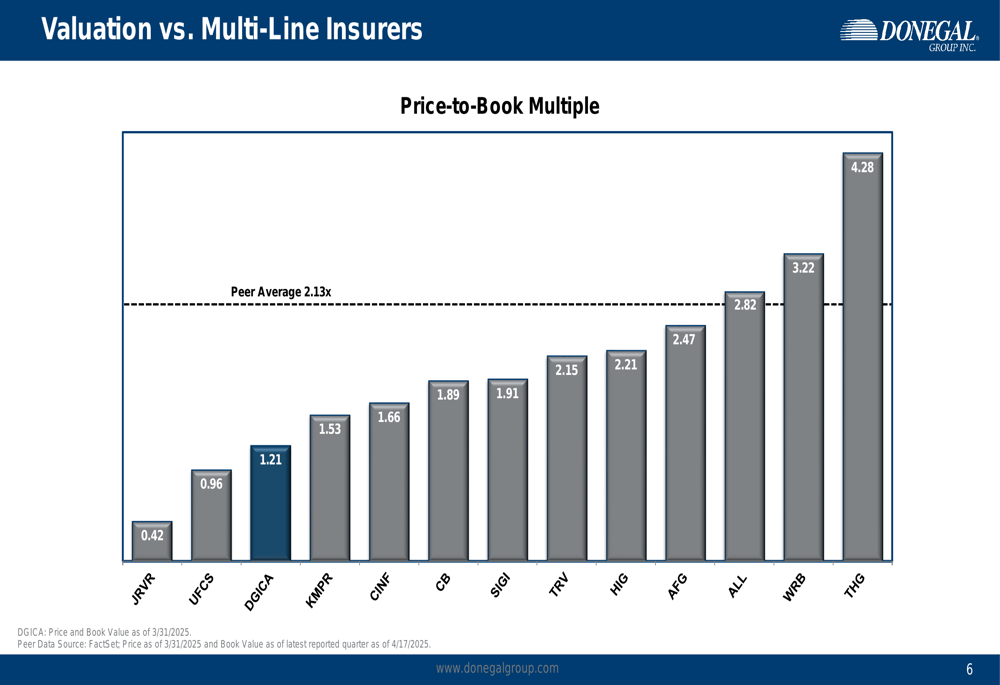

Despite the strong performance, Donegal continues to trade at a discount to its peers. The presentation highlighted that the company’s price-to-book multiple of 1.21x is significantly below the peer average of 2.13x, potentially indicating an undervaluation relative to comparable insurers.

The following chart compares Donegal’s valuation to other multi-line insurers:

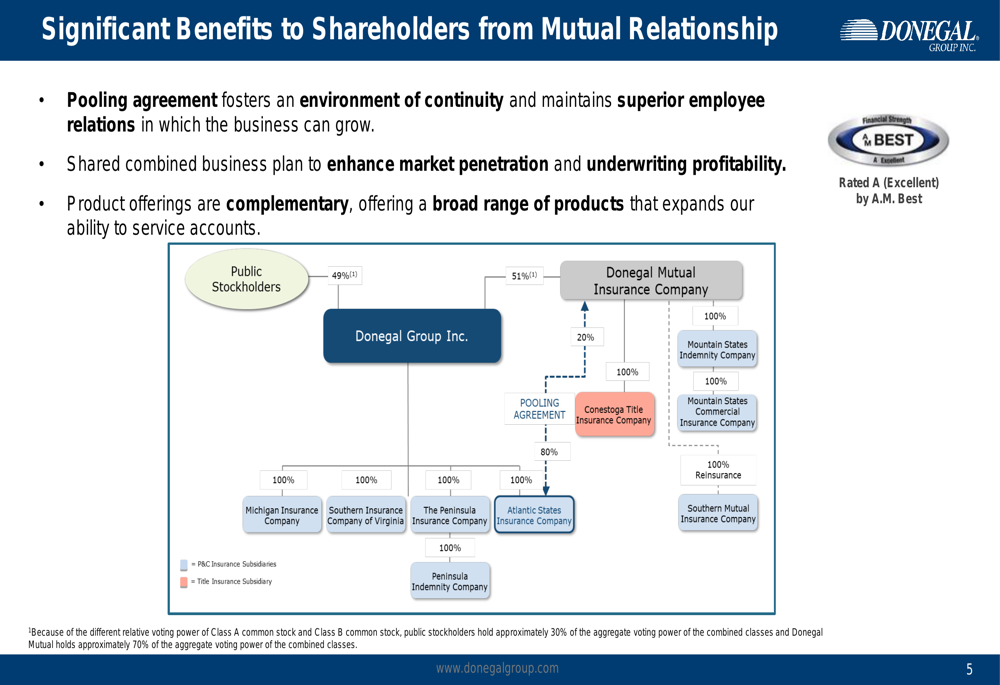

The company maintains an A (Excellent) rating from A.M. Best, reflecting its strong financial position. Donegal’s mutual holding company structure, with Donegal Mutual Insurance Company holding approximately 70% of the aggregate voting power, provides stability and continuity for operations.

This relationship structure is illustrated in the following diagram:

Forward-Looking Statements

Looking ahead, Donegal outlined several strategic initiatives aimed at maintaining its positive momentum. These include:

1. Achieving sustained excellent financial performance through underwriting discipline and data analytics

2. Strategically modernizing operations through new systems implementation and process excellence

3. Capitalizing on opportunities to grow profitably within existing markets

4. Providing superior experiences to agents, policyholders, and employees

The company appears to be making progress on its expense reduction goals mentioned in previous earnings calls, with the expense ratio improving by 1.1 percentage points year-over-year. Management had previously targeted a two-point improvement in the expense ratio by the end of 2025.

Donegal’s focus on commercial lines growth, coupled with its disciplined approach to personal lines, positions the company to potentially continue its improved performance through 2025, assuming normal weather patterns and stable economic conditions.

The significant improvement in Q1 2025 results represents a continuation of the positive trends seen in the latter part of 2024, with the company’s strategic initiatives appearing to yield tangible financial benefits for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.