These are top 10 stocks traded on the Robinhood UK platform in July

Introduction & Market Context

Dorman Products , Inc. (NASDAQ:DORM) reported its first quarter 2025 financial results on May 6, 2025, showcasing strong overall performance despite challenges in some business segments. The automotive parts supplier demonstrated significant earnings growth and margin expansion, primarily driven by its Light Duty segment, while navigating headwinds in its Heavy Duty and Specialty Vehicle divisions.

The company’s stock closed at $114.95 on May 5, 2025, and saw a modest 0.48% increase in premarket trading following the earnings release. Dorman’s shares have traded between $87.05 and $146.60 over the past 52 weeks, indicating some volatility in investor sentiment.

Quarterly Performance Highlights

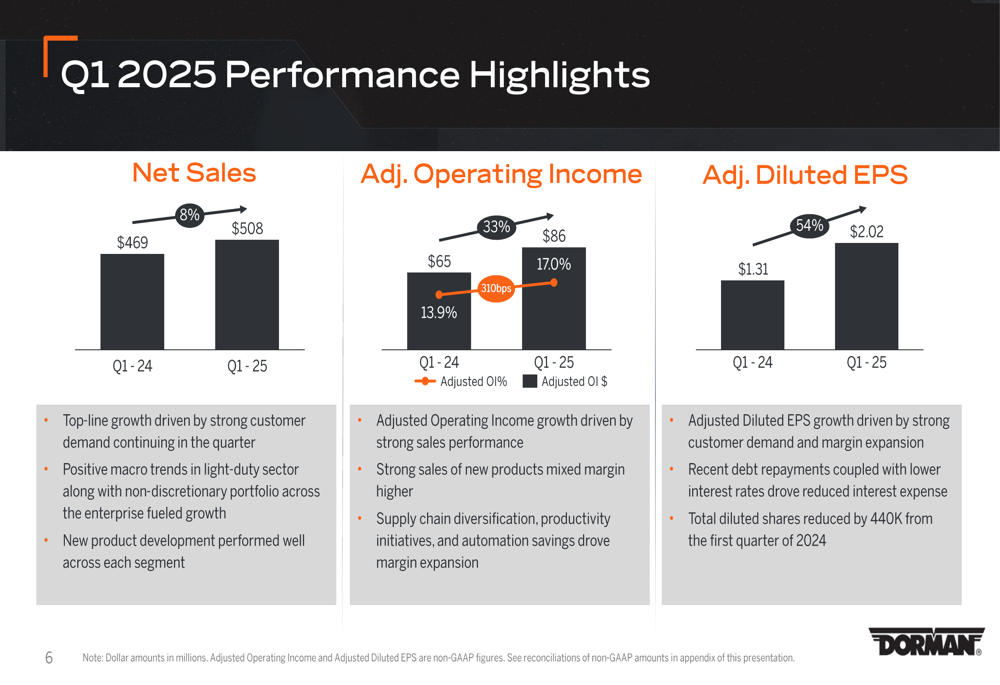

Dorman reported net sales of $508 million for Q1 2025, representing an 8.3% increase compared to the same period last year. More impressively, the company achieved an adjusted operating margin of 17.0%, a substantial 310 basis points improvement over Q1 2024. This margin expansion contributed to adjusted diluted earnings per share of $2.02, a remarkable 54% increase year-over-year.

As shown in the following summary of key financial metrics:

The company attributed these strong results to robust customer demand, positive macro trends, and successful new product development initiatives. Margin expansion was driven by favorable new product mix, supply chain diversification efforts, and productivity and automation initiatives.

A more detailed breakdown of the performance metrics shows the significant growth across key financial indicators:

Segment Analysis

Dorman’s performance varied significantly across its three business segments, with Light Duty emerging as the clear growth driver while Heavy Duty and Specialty Vehicle faced challenges.

The Light Duty segment, which represents Dorman’s largest business unit, delivered exceptional results with net sales increasing from $359 million in Q1 2024 to $409 million in Q1 2025. Operating margin in this segment expanded impressively from 16.1% to 19.9%, a 380 basis point improvement. The company cited strong point-of-sale performance and new product introductions as key factors driving this outperformance.

The Light Duty segment’s strong performance is illustrated in the following chart:

In contrast, the Heavy Duty segment experienced a decline, with net sales decreasing from $58 million to $52 million year-over-year. Operating margin deteriorated slightly from 0.0% to -0.3%. Dorman attributed this weakness to freight demand fluctuations, trucking overcapacity, and uncertainty created by tariff implementations, though it noted early signs of stabilization that began in Q4 2024 continued into Q1 2025.

The Heavy Duty segment’s challenges are reflected in these results:

Similarly, the Specialty Vehicle segment faced headwinds, with net sales declining from $52 million to $47 million and operating margin decreasing from 13.9% to 10.2%. The company cited softened consumer sentiment as the primary factor impacting this segment’s performance, while maintaining its focus on new product development.

Balance Sheet and Cash Flow

Dorman maintained strong financial discipline during the quarter, generating $40 million in free cash flow, which was deployed to repay $20 million of debt and repurchase $12 million of common stock. The company also invested $11 million in capital expenditures.

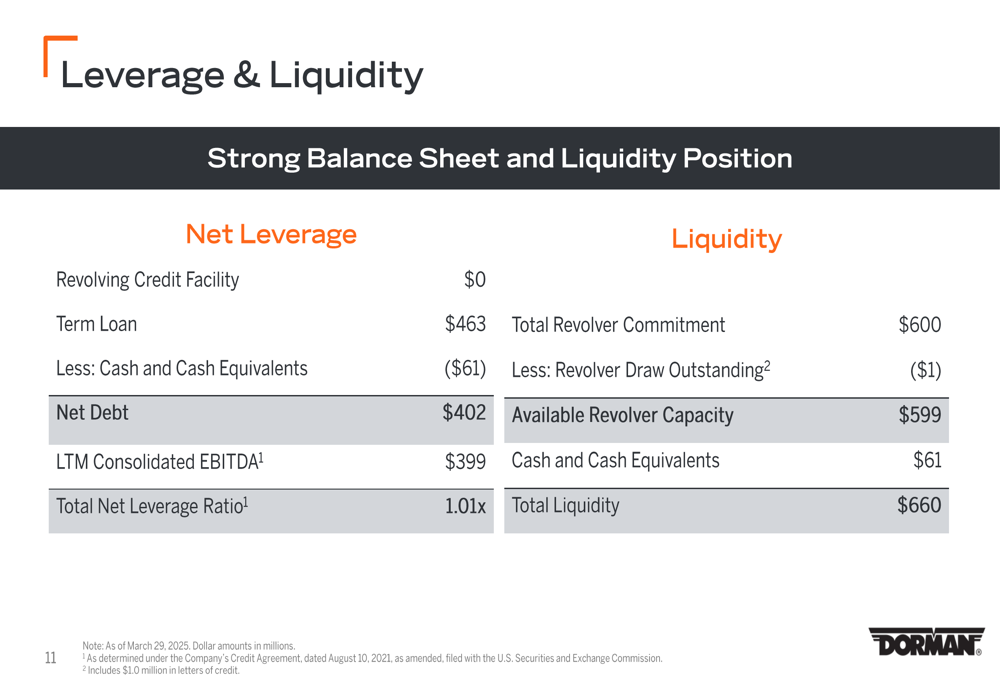

As of March 29, 2025, Dorman reported a robust balance sheet with total liquidity of $660 million, including $61 million in cash and cash equivalents and $599 million in available revolver capacity. The company’s net leverage ratio stood at a conservative 1.01x, indicating significant financial flexibility.

The company’s strong financial position is highlighted in this summary:

Forward Guidance and Outlook

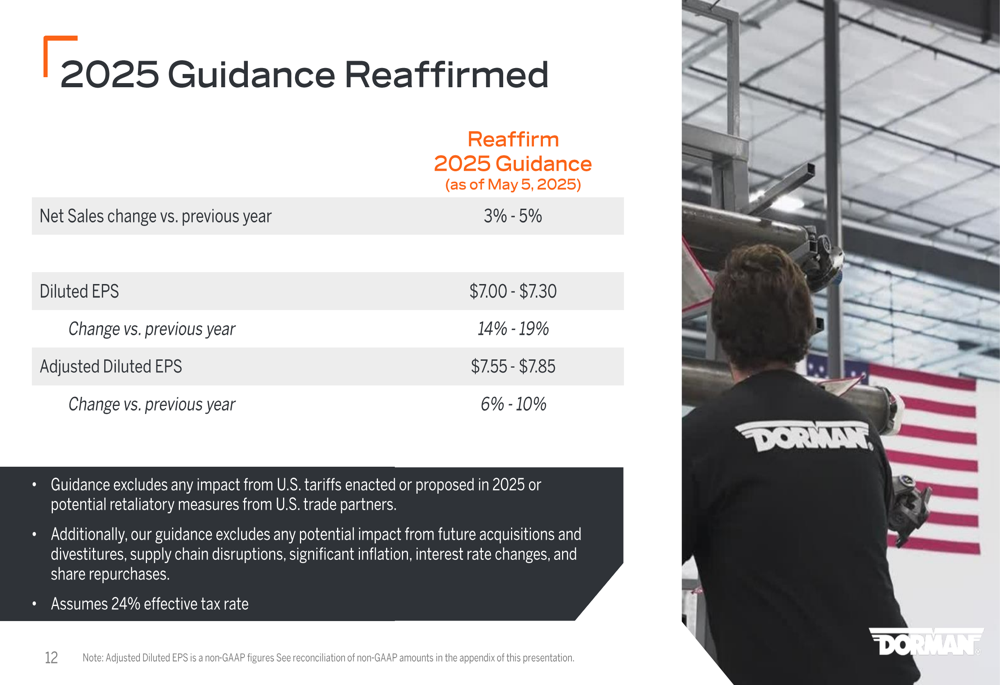

Despite mixed segment performance, Dorman reaffirmed its full-year 2025 guidance, projecting net sales growth of 3% to 5% compared to 2024. The company expects diluted earnings per share of $7.00 to $7.30 (14% to 19% growth) and adjusted diluted earnings per share of $7.55 to $7.85 (6% to 10% growth).

Importantly, this guidance excludes any impact from U.S. tariffs enacted or proposed in 2025 or potential retaliatory measures, which represents a significant uncertainty factor for the company’s outlook.

The company’s guidance is summarized in the following chart:

Dorman highlighted its strategic positioning to navigate tariff challenges through five key areas of resilience: a diversified supply chain, strong supplier relationships, focus on critical non-discretionary products, innovation and brand power, and a strong financial position.

In the segment outlook, Dorman noted that macro trends remain strong for the Light Duty segment, with increasing vehicle miles traveled supporting demand. For Heavy Duty, the company acknowledged persistent soft market conditions but pointed to early signs of stabilization. In the Specialty Vehicle segment, Dorman observed softened consumer sentiment impacting customer demand, though enthusiasm in UTV/ATV ridership remains strong.

Overall, Dorman’s Q1 2025 results demonstrate the company’s ability to deliver strong financial performance despite challenges in certain segments, with its Light Duty business serving as the primary growth engine. The company’s focus on new product development, supply chain diversification, and operational efficiency positions it well to navigate potential tariff-related headwinds in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.