Still betting on Nvidia? Our AI picked this stock instead; it’s up 96%+ THIS MONTH

Dorman Products , Inc. (NASDAQ:DORM) shares jumped 8% in premarket trading following the release of its second quarter 2025 earnings presentation on August 5, 2025, which revealed stronger-than-expected performance and raised full-year guidance.

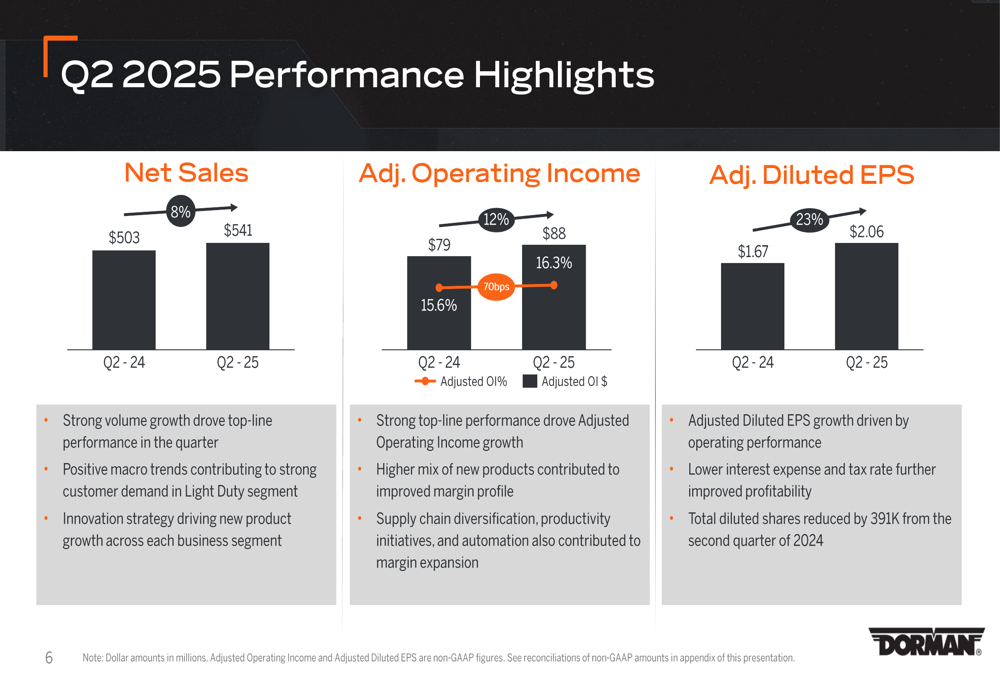

Quarterly Performance Highlights

Dorman reported net sales of $541 million for Q2 2025, representing a 7.6% increase compared to the same period last year. The company’s adjusted operating margin improved by 70 basis points to 16.3%, while adjusted diluted earnings per share surged 23% to $2.06.

These results continue the strong momentum seen in Q1 2025, when the company reported a 54% year-over-year increase in adjusted EPS and an 8% rise in consolidated net sales.

As shown in the following performance highlights from the presentation:

"We delivered strong results in the quarter with Net Sales and Adjusted Diluted EPS growth exceeding expectations," noted the company in its presentation summary slide. The performance was driven by strong volume growth, positive macro trends, and the company’s innovation strategy.

The detailed performance metrics show significant improvement across key financial indicators:

Segment Analysis

Dorman’s performance varied significantly across its three business segments, with Light Duty showing the strongest results.

The Light Duty segment, which represents the largest portion of Dorman’s business, posted impressive growth with net sales increasing from $385 million in Q2 2024 to $424 million in Q2 2025. Operating margin in this segment improved by 140 basis points to 18.5%. The company attributed this performance to strong customer demand, a higher mix of new products, and supply chain and productivity initiatives.

In contrast, the Heavy Duty segment faced challenges, with only a modest 1% increase in net sales to $62 million, while operating margin declined significantly from 4.4% to 0.8%. Dorman cited "mixed market signals" and "lower volume through trucking and freight recession" as key factors affecting this segment’s performance.

The Specialty Vehicle segment also experienced headwinds, with net sales declining 3% to $55 million and operating margin decreasing by 50 basis points to 17.3%. The company noted that "softened consumer sentiment due to tariffs has impacted customer demand," though it emphasized that "UTV/ATV ridership activity remains strong."

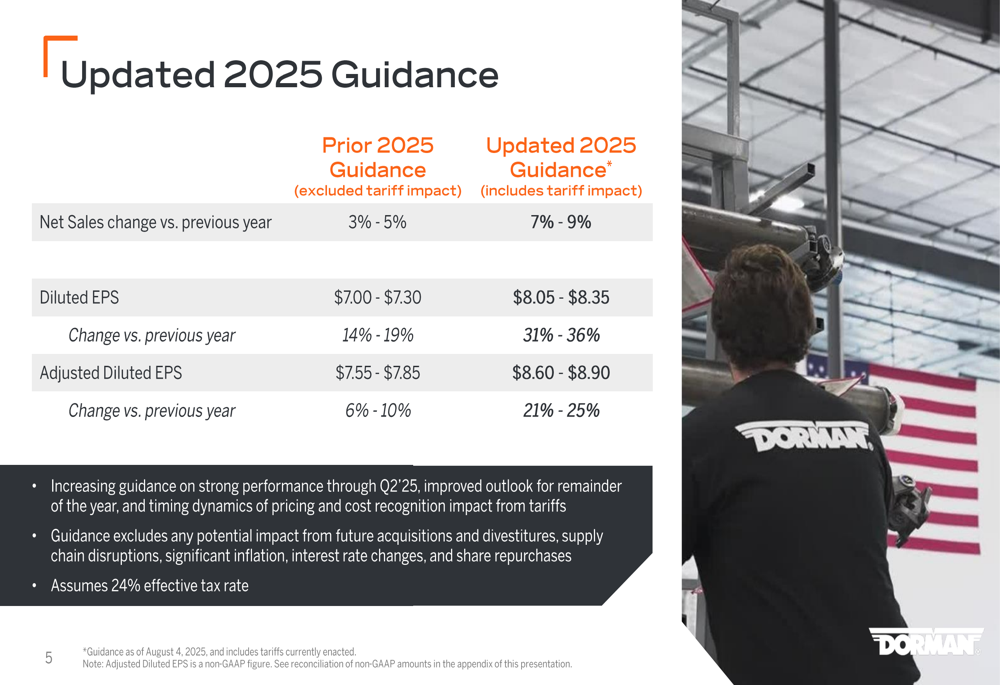

Updated Guidance

Based on the strong first-half performance and improved outlook, Dorman has significantly raised its full-year 2025 guidance. The company now expects net sales growth of 7%-9% (including tariff impact), up from the previous guidance of 3%-5% (excluding tariff impact).

Adjusted diluted EPS is now projected to be between $8.60 and $8.90, representing a 21%-25% increase year-over-year, compared to the previous guidance of $7.55-$7.85 (6%-10% growth).

The updated guidance table clearly shows the substantial upward revisions:

The company noted that this guidance includes tariffs currently enacted but excludes potential impacts from future acquisitions and divestitures, supply chain disruptions, inflation, interest rate changes, and share repurchases.

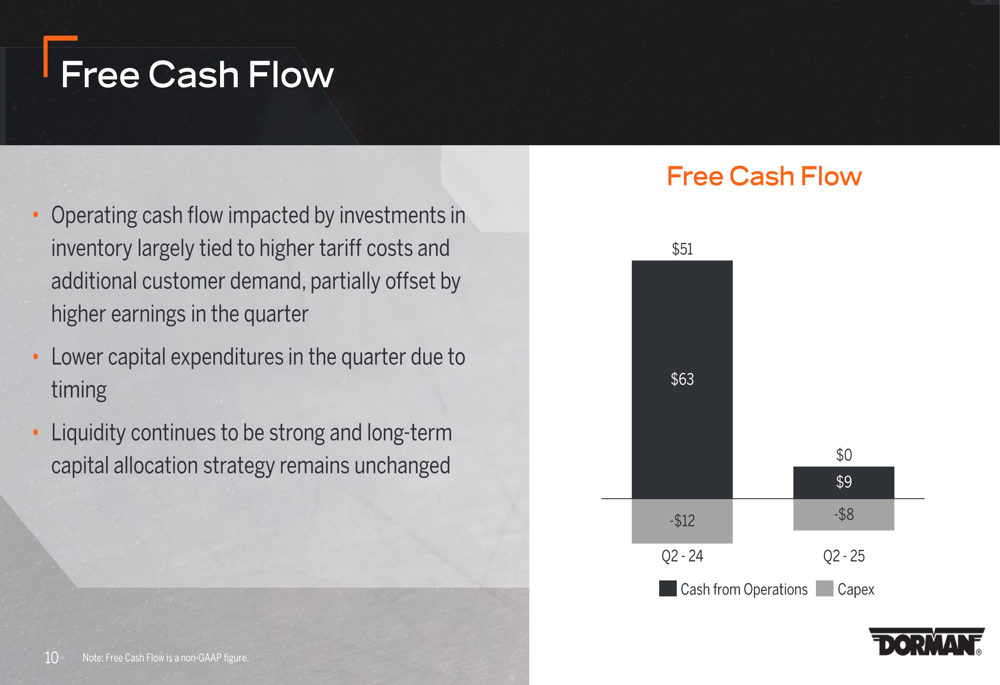

Financial Position & Cash Flow

Despite strong operational performance, Dorman’s cash flow was significantly impacted by inventory investments related to tariffs. Operating cash flow decreased from $63 million in Q2 2024 to just $9 million in Q2 2025.

The company explained that "operating cash flow was impacted by investments in inventory due to higher tariff costs and additional customer demand." However, it emphasized that "liquidity remains strong, and capital allocation strategy remains unchanged."

Indeed, Dorman’s balance sheet remains solid with total liquidity of $656 million as of June 28, 2025, including $599 million in available revolver capacity and $57 million in cash and cash equivalents. The company’s net debt stands at $406 million, resulting in a total net leverage ratio of 1.00x.

Forward-Looking Statements

Dorman remains optimistic about its future prospects despite some segment-specific challenges. The company stated it is "well-positioned to drive long-term growth" and is committed to investing in non-discretionary parts and expanding channel opportunities to capture market share.

For the Heavy Duty segment, which faced the most significant challenges, Dorman noted that "initiatives are in place for long-term growth through new product development and digital customer experience."

In the Specialty Vehicle segment, the company plans to focus on "investing in non-discretionary parts and expanding channel opportunities to capture market share and drive long-term growth" despite current headwinds from tariffs and softened consumer sentiment.

The overall positive outlook is supported by continuing favorable macro trends in the Light Duty segment, including increasing vehicle miles traveled and aging vehicle fleets, which typically drive demand for aftermarket parts.

As Dorman continues to execute its strategy focused on innovation and operational efficiency, investors will be watching closely to see if the company can maintain its momentum in the second half of 2025 while navigating tariff-related challenges and segment-specific market dynamics.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.