Gold soars to record high over $3,900/oz amid yen slump, US rate cut bets

Introduction & Market Context

Douglas Emmett (NYSE:DEI), a $2.94 billion market cap real estate company, recently presented its investor overview for Q2 2025, highlighting its strategic focus on high-barrier markets in Los Angeles and Honolulu. The presentation comes after DEI reported strong Q1 2025 earnings that significantly beat analyst expectations, with an EPS of $0.24 against a forecast of -$0.03.

The company’s stock has shown positive momentum, trading at $15.12 as of August 5, 2025, up 2.02% and continuing to recover from its 52-week low of $12.39. This upward trend reflects growing investor confidence in DEI’s strategy of focusing on premium markets with limited new supply.

Strategic Positioning

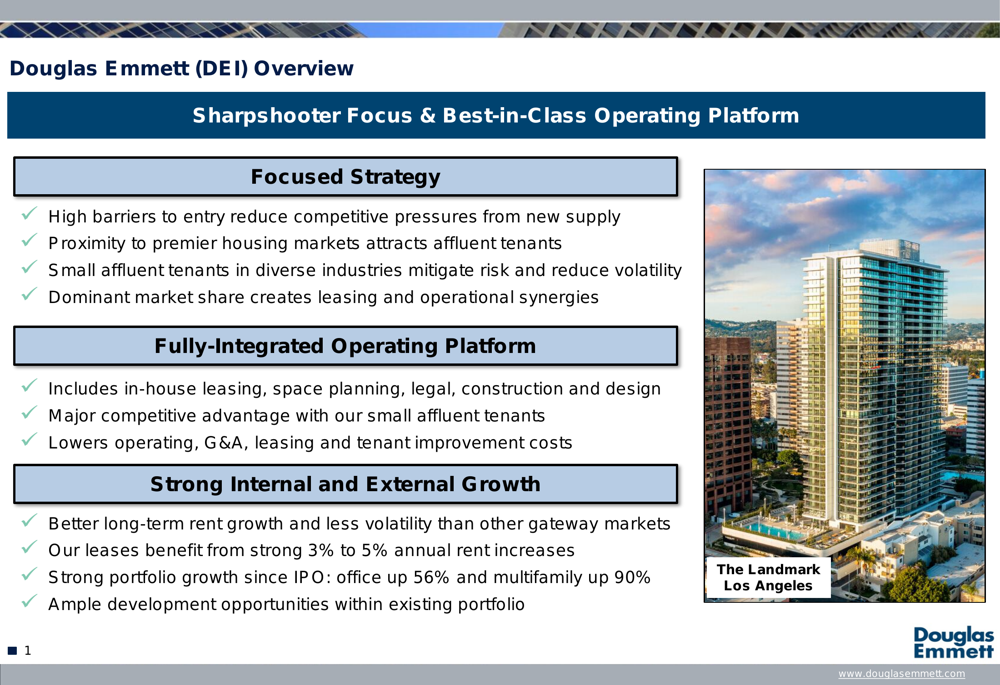

Douglas Emmett’s presentation emphasized its "sharpshooter focus" on high-barrier markets, highlighting the company’s dominant position in premium Los Angeles and Honolulu submarkets. With approximately 39% average market share of Class A office space in its regions, DEI has established itself as the largest office landlord in both Los Angeles and Honolulu.

As shown in the following comprehensive overview of the company’s strategy:

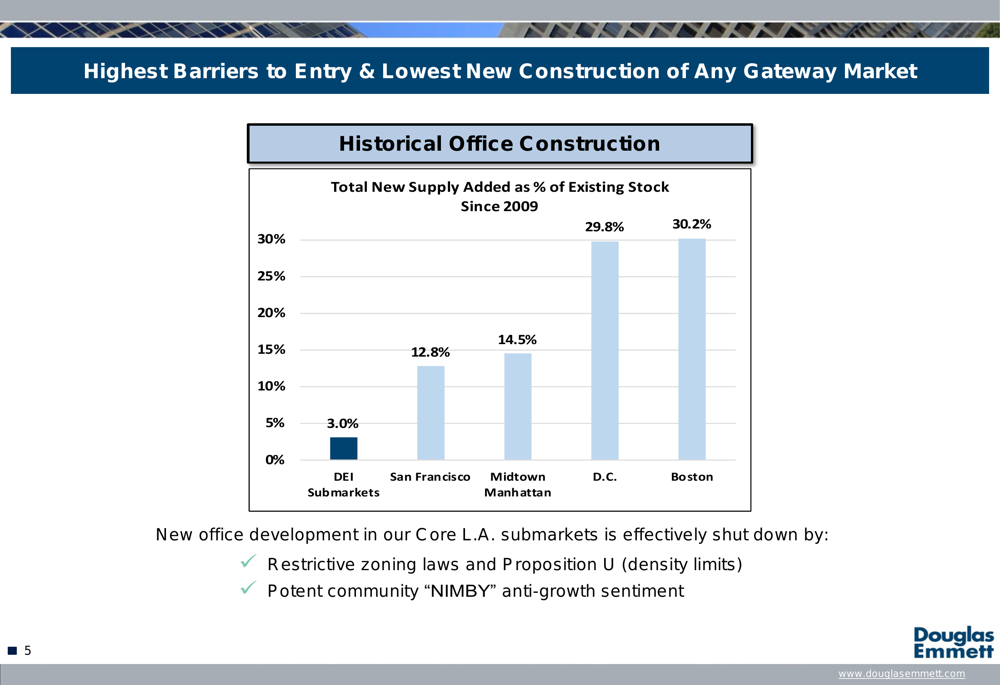

A key competitive advantage highlighted in the presentation is the severely limited new construction in DEI’s core markets. Historical data shows that DEI’s submarkets have experienced only 3.0% new supply added as a percentage of existing stock since 2009, compared to 12.8% in San Francisco, 14.5% in Midtown Manhattan, 29.8% in D.C., and 30.2% in Boston.

This limited supply is attributed to restrictive zoning laws, density limits from Proposition U, and strong community anti-growth sentiment, creating significant barriers to entry for competitors.

As illustrated in this comparative chart of new construction across major markets:

Another strategic advantage for DEI is Los Angeles’ notorious traffic congestion, which effectively segments the market and limits competition between submarkets. The presentation showed that average daily round-trip commute times from Westside residential neighborhoods to the closest DEI submarket is just 21 minutes, compared to 71 minutes to Hollywood and 80 minutes to Downtown.

Portfolio Performance

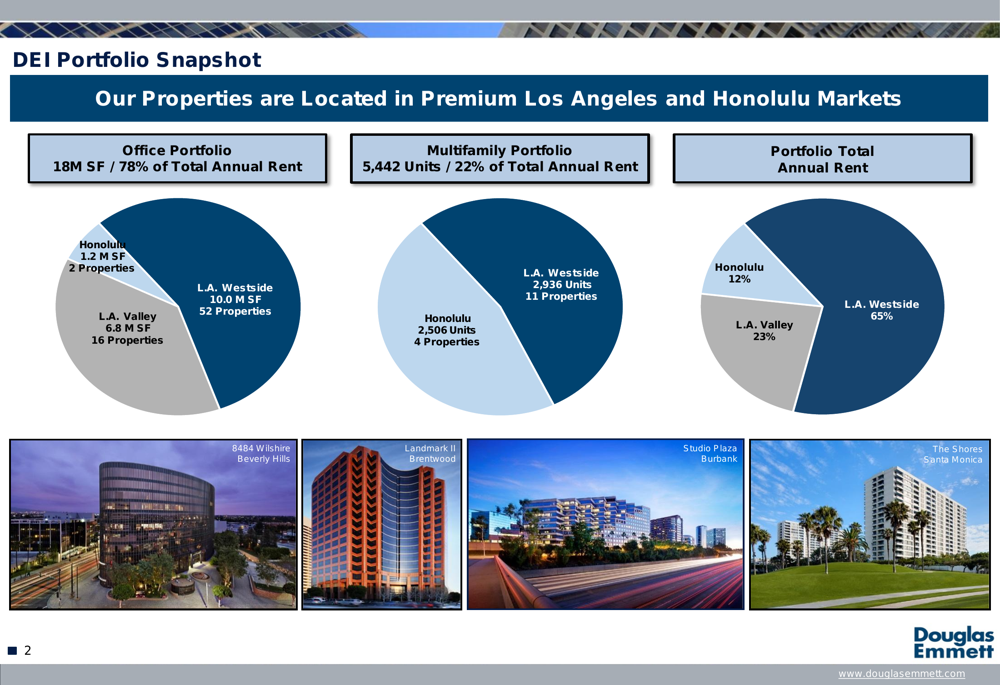

Douglas Emmett’s portfolio consists of 18 million square feet of office space (generating 78% of total annual rent) and 5,442 multifamily units (providing 22% of total annual rent). The portfolio is geographically concentrated in premium markets, with 65% of annual rent coming from LA Westside, 23% from LA Valley, and 12% from Honolulu.

The following portfolio snapshot illustrates this concentration:

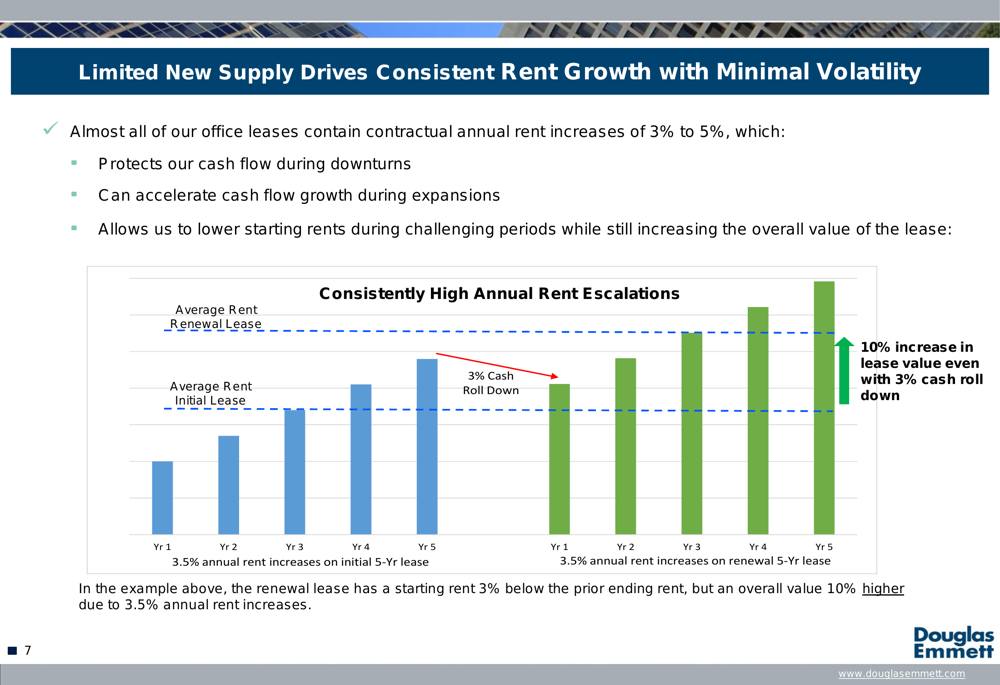

A standout feature of DEI’s portfolio is its consistent rent growth through multiple market cycles. The presentation highlighted that almost all of DEI’s office leases contain contractual annual rent increases of 3% to 5%, which protects cash flow during downturns and can accelerate growth during expansions.

This rent escalation strategy is visualized in the following graphic:

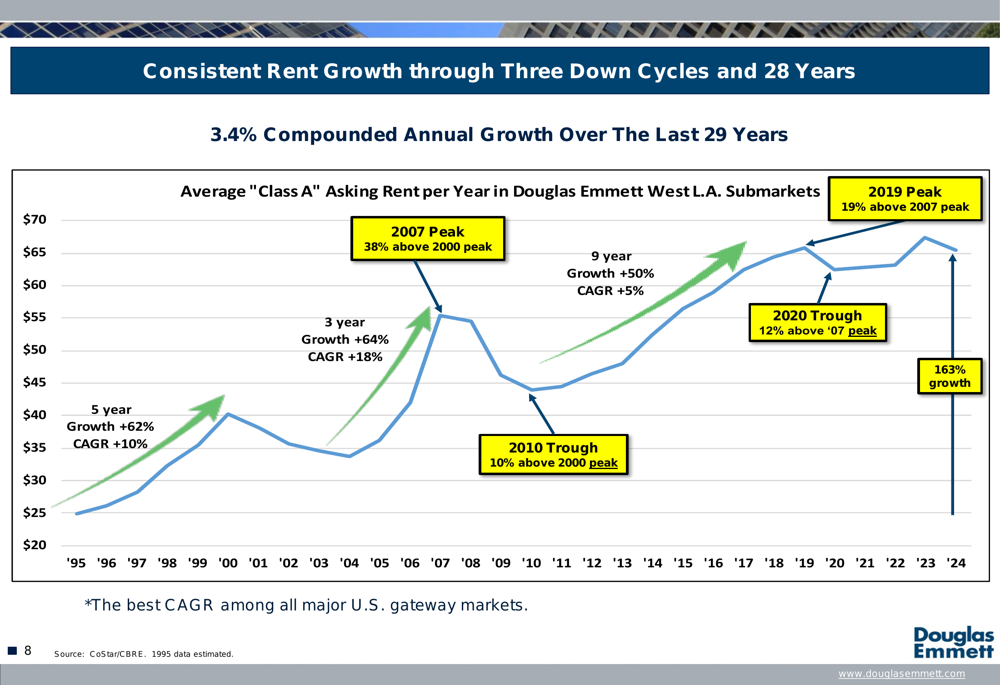

Historical data supports DEI’s claims of superior rent growth. Over the past 29 years, the company has achieved 163% growth in average Class A asking rents in its West LA submarkets, demonstrating resilience through three down cycles. The 2007 peak was 38% above the 2000 peak, while the 2010 trough remained 10% above the 2000 peak, illustrating the market’s strength even during downturns.

As shown in this historical rent growth chart:

DEI’s tenant base is highly diversified across industries, with legal (19.6%), financial services (16.4%), and real estate (13.4%) representing the largest segments. The company focuses on small tenants, with 96% of leases (2,549 out of 2,656) under 20,000 square feet. According to management, these smaller tenants are willing to pay a premium for proximity, typically have decision-makers working on-site, and require lower tenant improvement costs.

Operational Efficiency

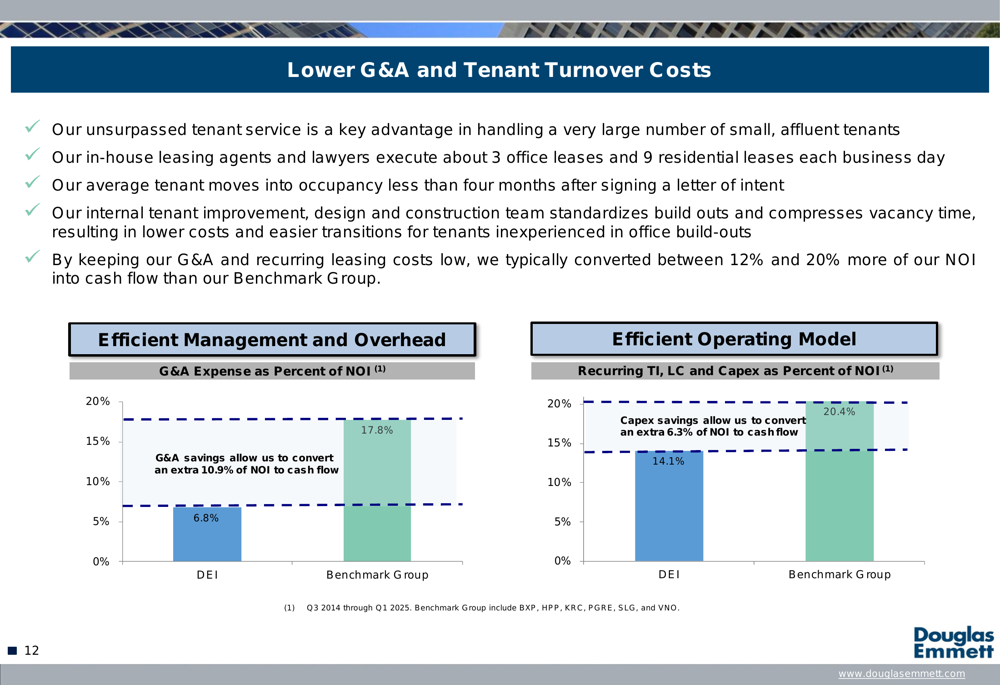

A core competitive advantage highlighted in the presentation is DEI’s fully integrated operating platform, which includes in-house leasing, space planning, legal, construction, and design services. This integration allows the company to execute approximately three office leases and nine residential leases each business day, with tenants typically moving in less than four months after signing a letter of intent.

The operational efficiency translates into significant cost advantages. DEI’s G&A expenses represent just 6.8% of NOI, compared to 17.8% for its benchmark group. Similarly, recurring tenant improvements, leasing costs, and capital expenditures account for 14.1% of NOI versus 20.4% for the benchmark group.

These efficiency metrics are illustrated in the following comparison:

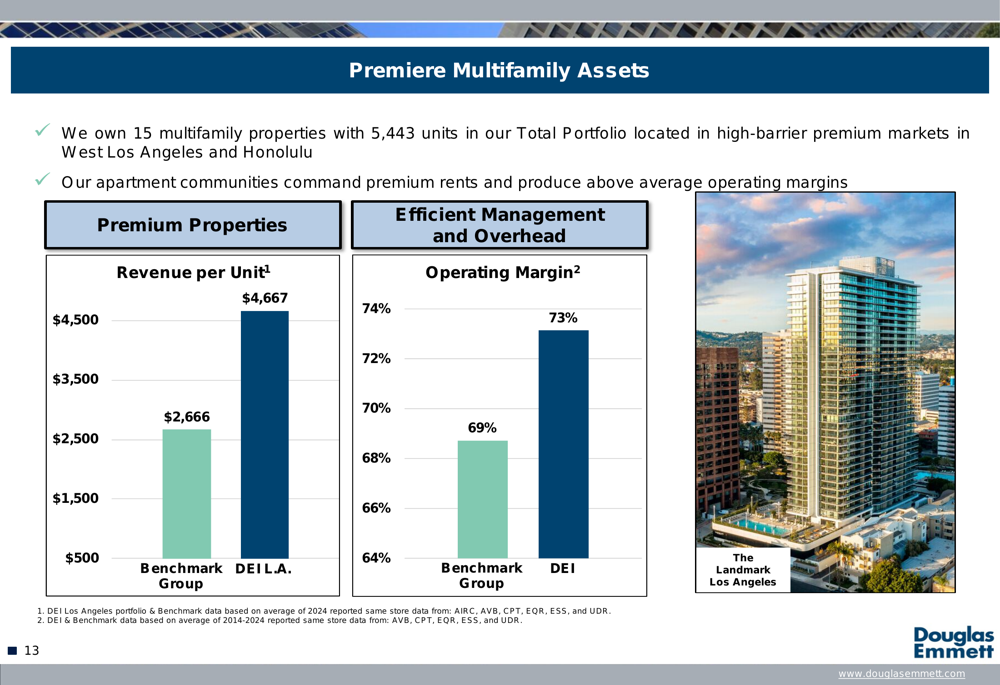

In the multifamily segment, DEI’s properties command premium rents and produce above-average operating margins. The presentation showed revenue per unit of $4,667 for DEI’s LA properties versus $2,666 for the benchmark group, while operating margins stand at 73% compared to 69% for peers.

As shown in this multifamily performance comparison:

Financial Outlook

Douglas Emmett’s financial strategy focuses on property-level, non-recourse debt without corporate or rating agency covenants. This approach provided flexibility during the global financial crisis, with the company noting it was "one of only a few REITs which was not forced to issue dilutive equity" during that period.

The company’s debt maturities are well-staggered, with no maturities in 2025, $1,381 million in 2026, $888 million in 2027, and decreasing amounts in subsequent years. This structure provides DEI with refinancing flexibility and helps manage interest rate risk.

In its Q1 2025 earnings report, DEI provided guidance for 2025 net income per share between $0.07 and $0.13, with FFO per fully diluted share expected to range from $1.42 to $1.48. Despite anticipating an increase in debt costs by 100-200 basis points, management expressed optimism about potential rental rate acceleration as the economy recovers.

Forward-Looking Statements

The presentation highlighted DEI’s commitment to sustainability, with goals to keep at least 80% of stabilized eligible office space "ENERGY STAR Certified" and reduce greenhouse gas emissions by 30% across the portfolio by 2035 compared to 2019. The company reported exceeding its ENERGY STAR goal with 84% of eligible space certified as of December 2024, and is ahead of schedule on emissions reduction with a 13% decrease versus 2019.

CEO Jordan Kaplan emphasized the company’s resilience during the Q1 earnings call, stating, "Our operating platform is built to weather storms." He also highlighted four strategic avenues for restoring and exceeding pre-pandemic FFO levels, including redevelopment projects.

With its focused strategy on high-barrier markets, operational efficiency, and diverse tenant base, Douglas Emmett appears well-positioned to capitalize on the ongoing recovery in premium office and multifamily markets. However, investors should monitor potential challenges including rising debt costs, market vacancy pressures, and execution risks associated with redevelopment projects.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.