Stock market today: Stocks fall as investors rotate out of tech into Jackson Hole

Introduction & Market Context

Dover Corporation (NYSE:DOV) reported strong second-quarter 2025 results on July 24, showcasing robust performance across its diversified industrial portfolio. The company’s shares responded positively in premarket trading, rising 1.1% to $193, building on the previous day’s close of $190.90.

The Q2 results demonstrate continued momentum following Dover’s solid first quarter, when the company exceeded EPS expectations despite slight revenue challenges. This quarter’s performance reflects Dover’s successful execution of its strategic initiatives and operational efficiency improvements.

Quarterly Performance Highlights

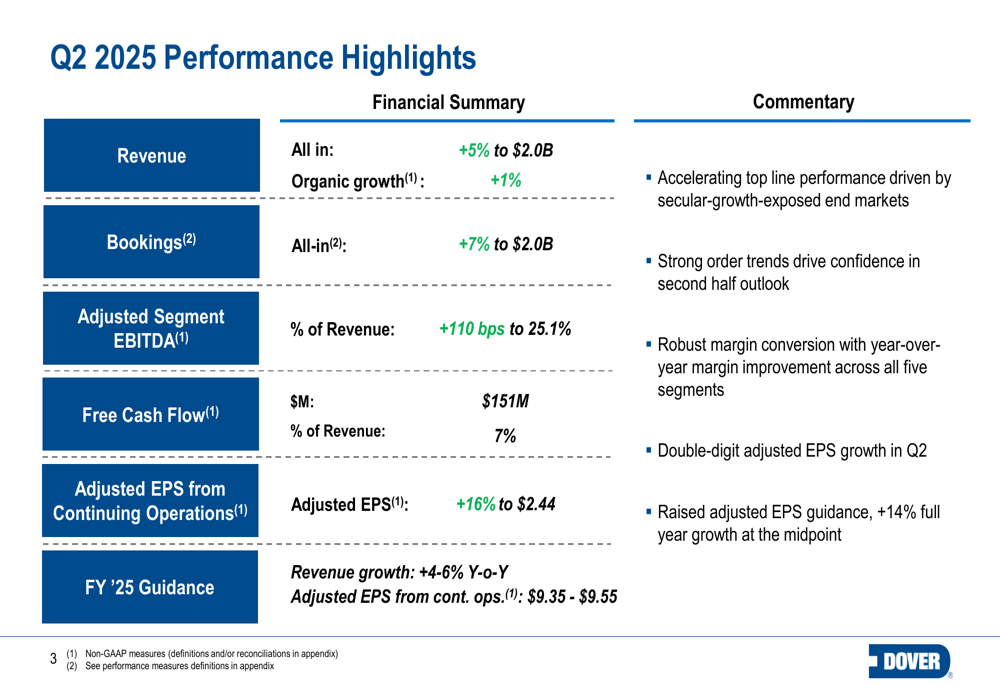

Dover reported impressive financial results for Q2 2025, with revenue increasing 5% year-over-year to $2.0 billion. While organic growth contributed 1%, acquisitions added 3% and favorable currency translation provided an additional 1% boost.

As shown in the following comprehensive performance overview, adjusted EPS from continuing operations grew 16% to $2.44, while adjusted segment EBITDA margin expanded 110 basis points to 25.1%:

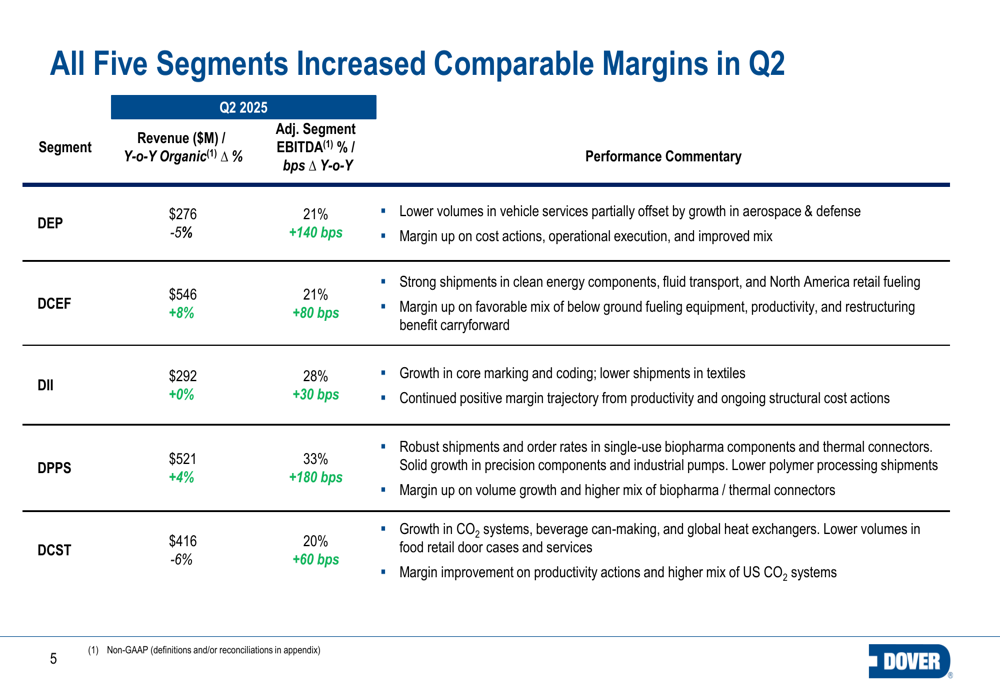

The company demonstrated strong margin performance across all five business segments, with each reporting year-over-year margin improvement. The Pumps & Process Solutions segment led with the highest adjusted EBITDA margin at 33%, representing a 180 basis point improvement driven by robust shipments in biopharma components and thermal connectors.

The following breakdown illustrates each segment’s performance:

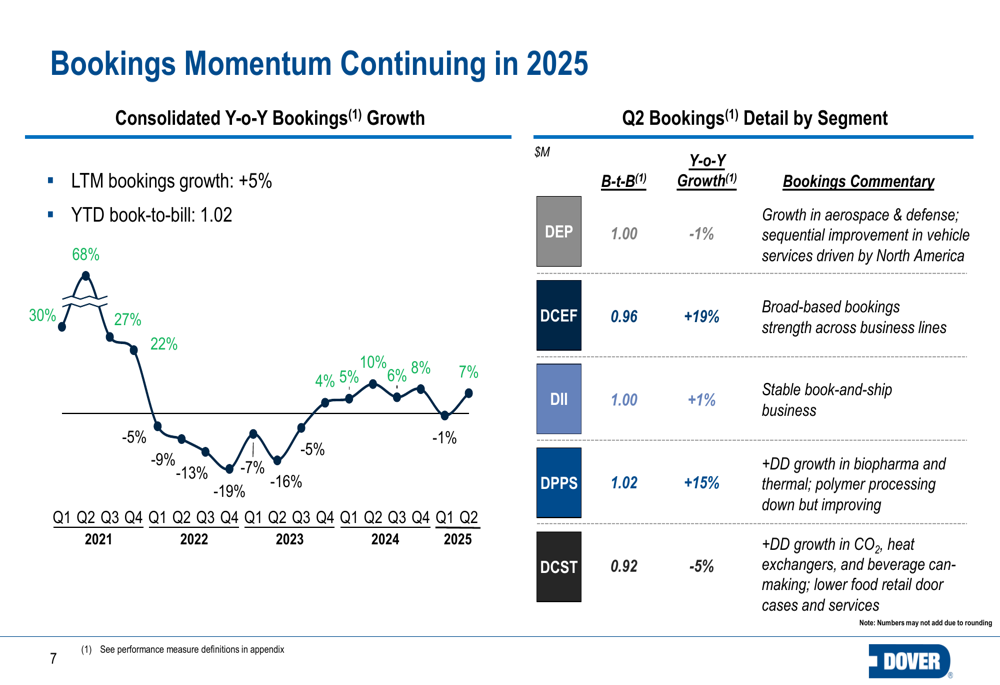

Bookings momentum remained strong, with total bookings up 7% year-over-year to $2.0 billion. The year-to-date book-to-bill ratio stands at 1.02, with all five segments maintaining ratios above 1.0. This trend provides confidence in Dover’s second-half outlook.

The bookings trend is visualized in this chart showing continued momentum:

Strategic Initiatives

Dover continues to focus on high-growth secular platforms that drive long-term performance. The company highlighted five key areas: Clean Energy Components, Precision Components, Single-Use Biopharma, Liquid Cooling, and CO2 Systems. These platforms are benefiting from structural tailwinds including energy transition, biopharma innovation, and data center expansion.

The following image details these growth platforms and recent investments:

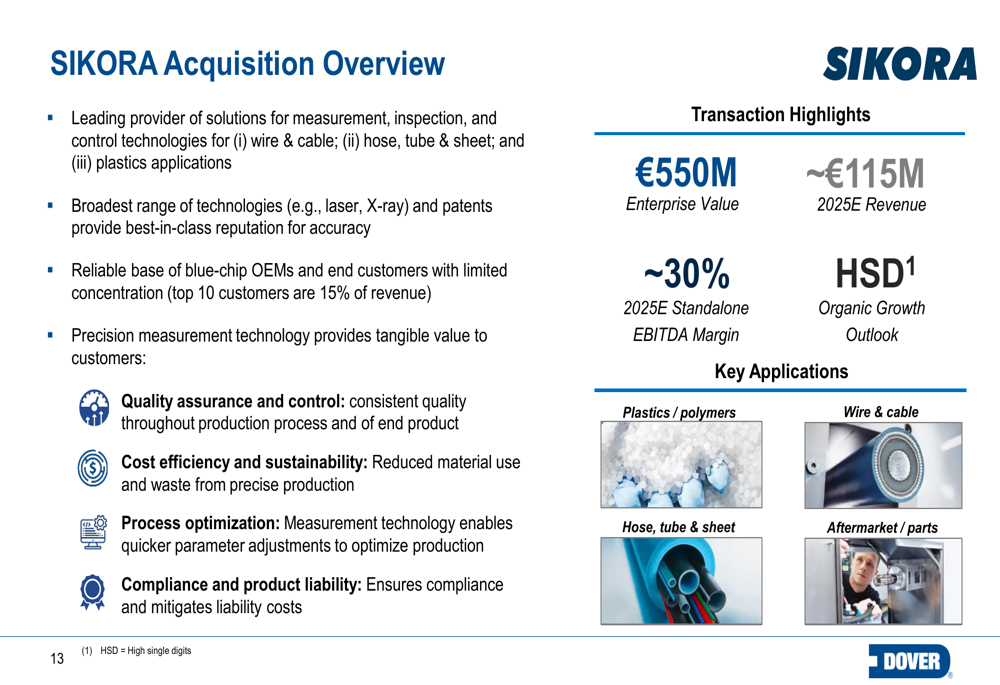

A significant strategic development is Dover’s acquisition of SIKORA, a leading provider of measurement, inspection, and control technologies for wire & cable, hose, tube & sheet, and plastics applications. The €550 million acquisition brings approximately €115 million in expected 2025 revenue with an attractive ~30% EBITDA margin.

The SIKORA acquisition details are outlined here:

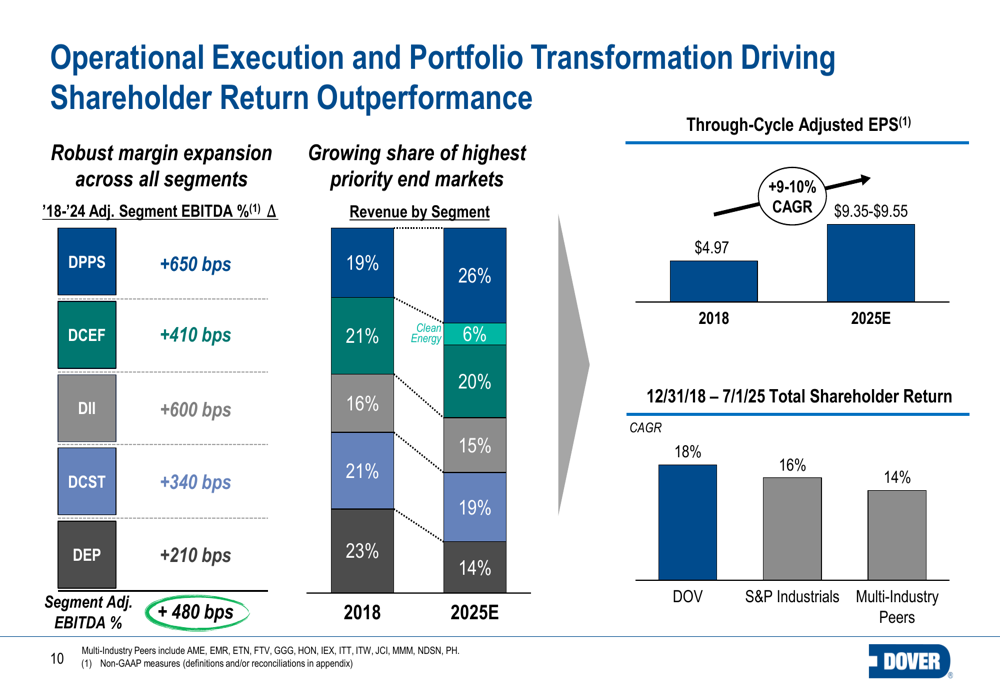

Dover’s long-term transformation has significantly improved its business mix and operational performance. Since 2018, the company has expanded adjusted segment EBITDA margins by 480 basis points, with the most substantial improvements in the Pumps & Process Solutions (+650 bps) and Imaging & Identification (+600 bps) segments.

This operational execution has translated into superior shareholder returns, as illustrated in the following chart:

Forward-Looking Statements

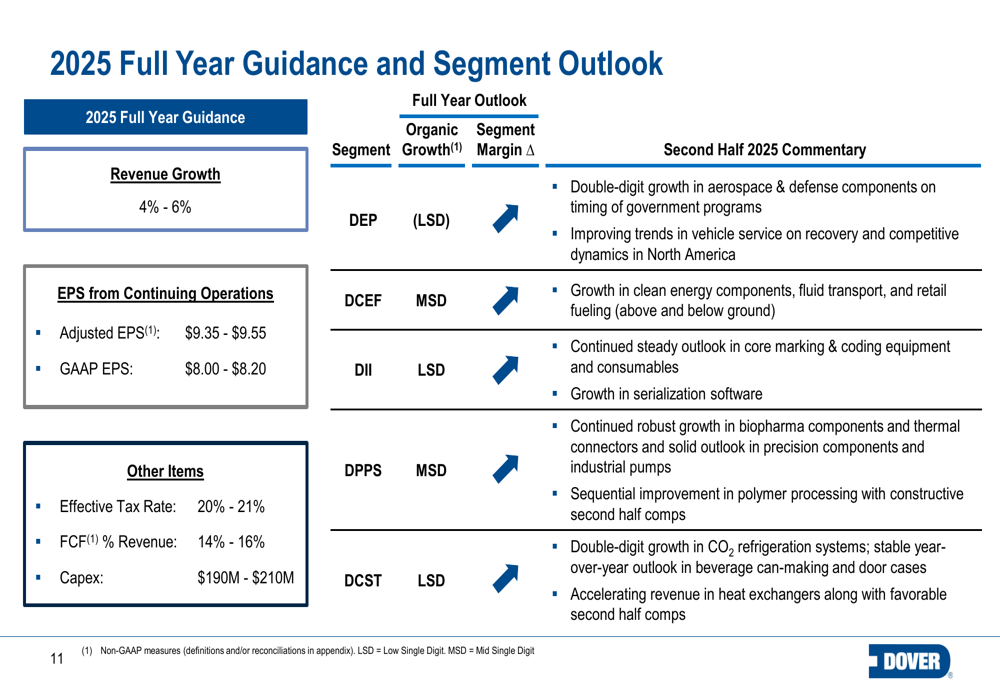

Based on strong first-half performance and continued bookings momentum, Dover raised its full-year 2025 guidance. The company now expects revenue growth of 4-6% year-over-year and adjusted EPS from continuing operations of $9.35-$9.55, representing 14% growth at the midpoint.

The detailed guidance and segment outlook are presented below:

For the second half of 2025, Dover anticipates continued strength in several key areas:

- Double-digit growth in aerospace & defense components

- Mid-single-digit growth in clean energy components, fluid transport, and retail fueling

- Continued robust growth in biopharma components and thermal connectors

- Double-digit growth in CO2 refrigeration systems

The company expects free cash flow to reach 14-16% of revenue for the full year, with capital expenditures projected at $190-210 million.

Conclusion

Dover’s Q2 2025 results demonstrate the company’s successful execution of its strategic initiatives and operational efficiency improvements. With margin expansion across all segments, strong bookings momentum, and raised full-year guidance, Dover appears well-positioned for continued growth.

The company’s focus on secular growth platforms and strategic acquisitions like SIKORA should provide long-term tailwinds, while operational execution continues to drive shareholder returns that outpace both the S&P Industrials index and multi-industry peers.

As Dover enters the second half of 2025, its diversified portfolio, margin expansion initiatives, and exposure to high-growth markets provide a solid foundation for continued performance, despite potential macroeconomic uncertainties.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.