Intel, Ford and Target rise premarket; Deckers slumps

Dow Inc. (NYSE:DOW) presented its third quarter 2025 results on October 23, showing sequential improvement across business segments despite year-over-year challenges. The company’s stock responded positively, rising 11.11% to $24.11 during the trading session following a 6.68% gain in premarket trading.

Quarterly Performance Highlights

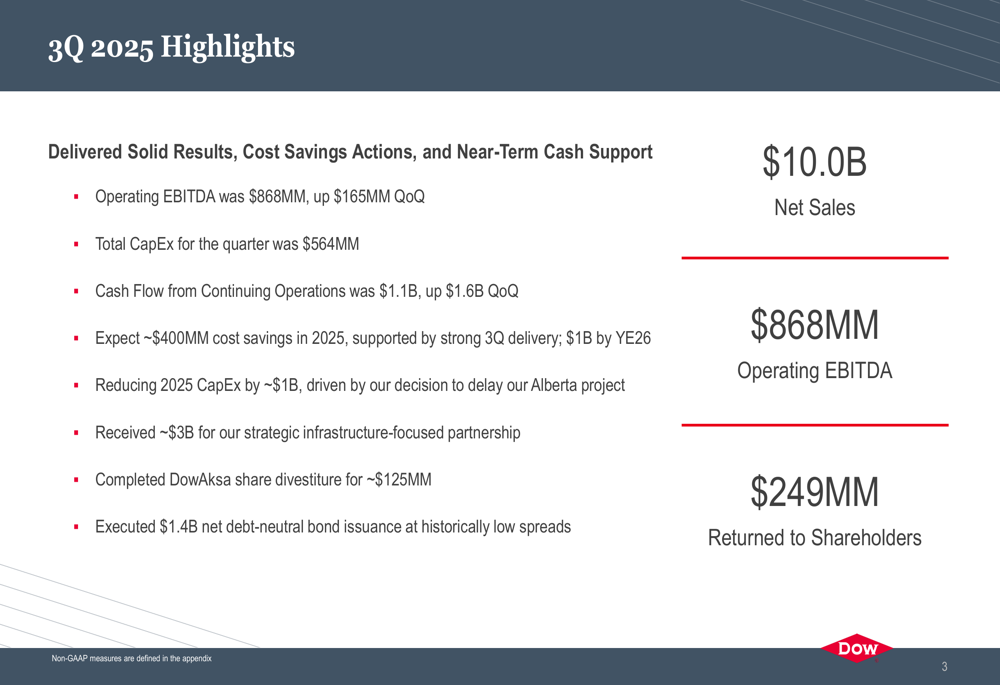

Dow reported operating EBITDA of $868 million for the third quarter, representing a $165 million increase from the previous quarter. Cash flow from continuing operations reached $1.1 billion, a substantial improvement of $1.6 billion compared to Q2. The company reported net sales of $10.0 billion and returned $249 million to shareholders.

As shown in the following quarterly highlights slide, Dow is implementing significant cost-saving measures and strategic actions to enhance financial flexibility:

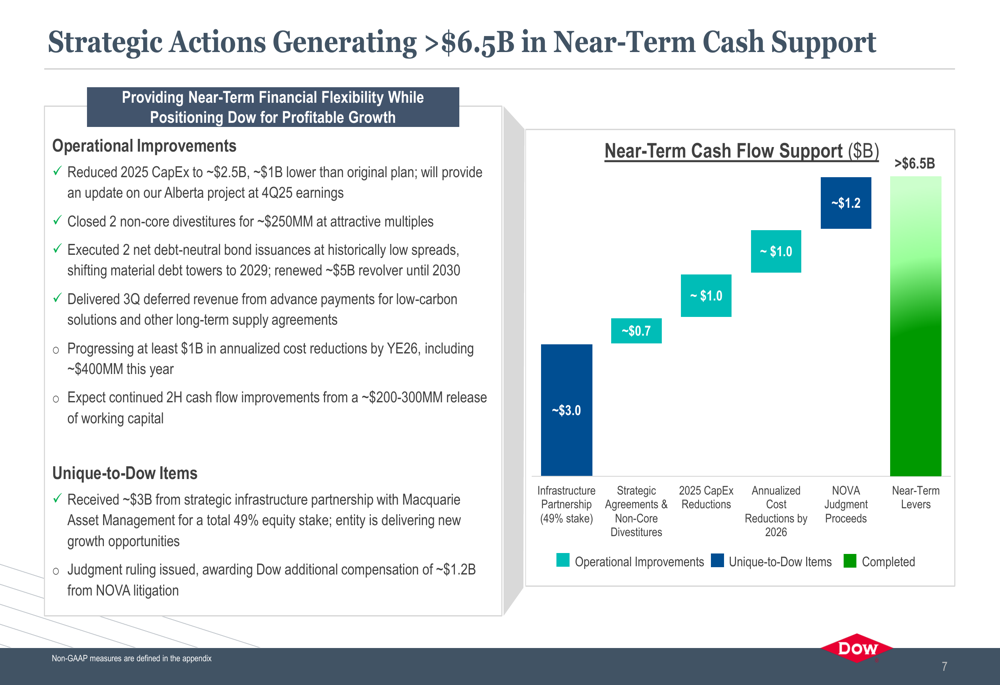

The company expects approximately $400 million in cost savings for 2025, with plans to reach $1 billion in annualized cost reductions by the end of 2026. Additionally, Dow has reduced its 2025 capital expenditure plan by approximately $1 billion, primarily by delaying its Alberta project.

Segment Performance

Dow’s three main business segments showed sequential improvement despite mixed year-over-year comparisons.

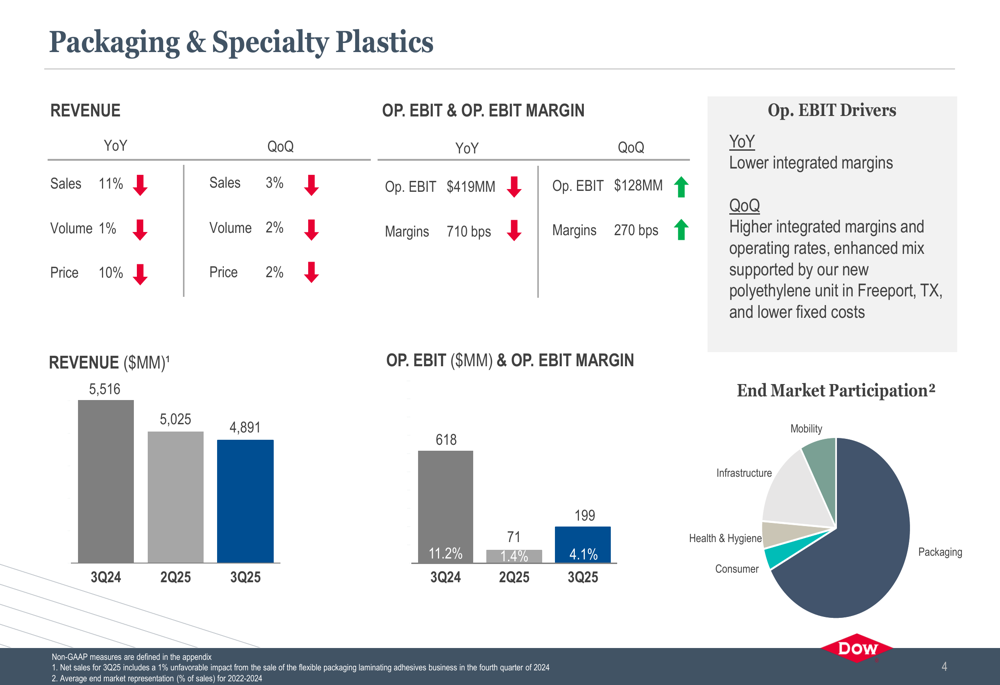

The Packaging & Specialty Plastics segment reported sales of $4.89 billion, down 11% year-over-year but up 3% quarter-over-quarter. Operating EBIT for this segment was $199 million, representing a significant sequential improvement of $128 million, though still down $419 million compared to Q3 2024.

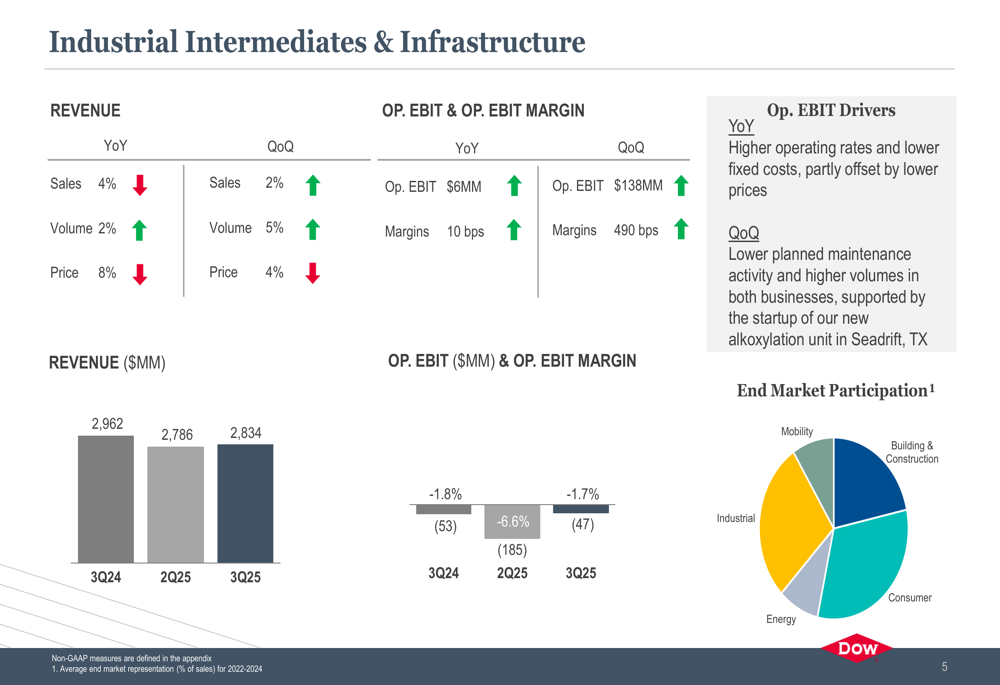

The Industrial Intermediates & Infrastructure segment showed more positive trends with revenue of $2.83 billion, up 4% year-over-year and 2% quarter-over-quarter. While still operating at a loss, the segment’s operating EBIT improved by $138 million sequentially to -$47 million.

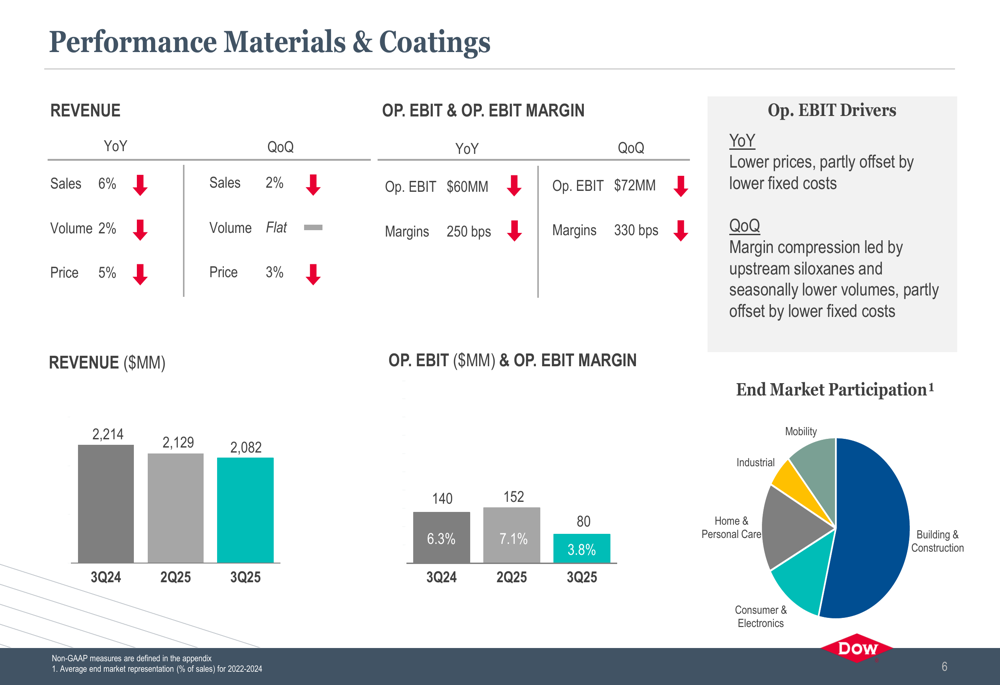

Performance Materials & Coatings generated $2.08 billion in revenue, down 6% year-over-year but up 2% sequentially. Operating EBIT for this segment was $80 million, improving by $72 million from the previous quarter.

These results align with the earnings report that showed Dow’s earnings per share of -$0.19 beat analyst expectations of -$0.31, despite revenue slightly missing forecasts.

Strategic Initiatives & Cash Generation

A key focus of Dow’s presentation was its strategic actions to generate near-term cash support. The company highlighted initiatives expected to provide over $6.5 billion in financial flexibility.

Notable among these actions was the completion of a strategic infrastructure-focused partnership that generated approximately $3 billion in proceeds. Dow also completed the DowAksa share divestiture for approximately $125 million and executed a $1.4 billion net debt-neutral bond issuance at historically low spreads.

Additionally, the company expects to receive approximately $1.2 billion from a favorable judgment in litigation with NOVA in the fourth quarter of 2025.

Industry Outlook & Competitive Position

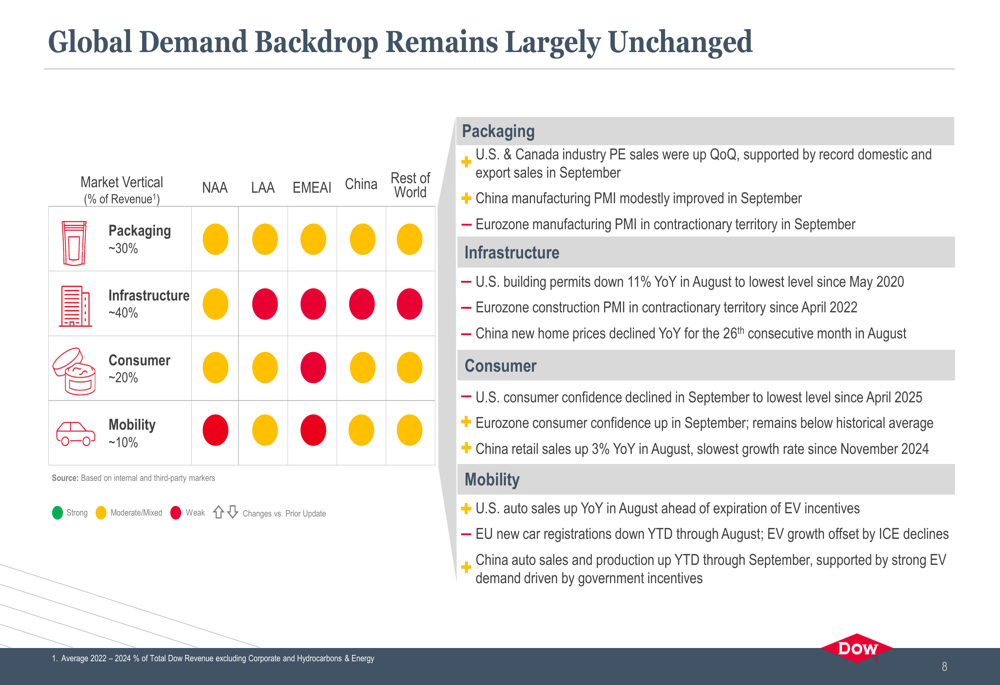

Dow’s presentation indicated that the global demand backdrop remains largely unchanged, with varying conditions across different markets and regions. The company provided a detailed assessment of demand conditions in packaging, infrastructure, consumer, and mobility sectors across different geographic regions.

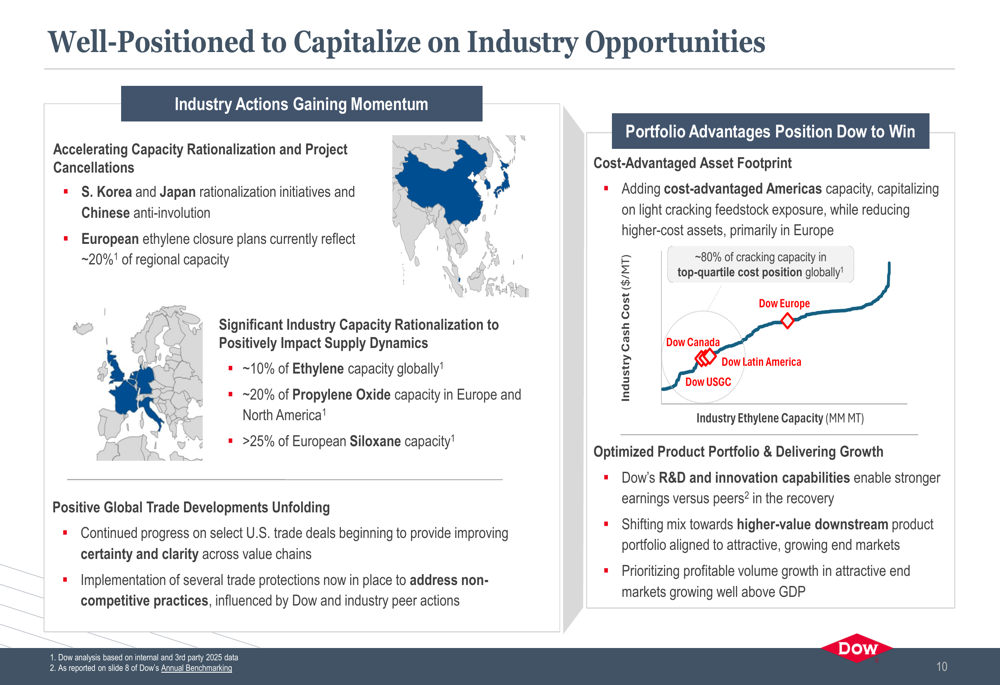

The company highlighted industry-wide capacity rationalization as a positive development that could improve supply-demand dynamics. According to Dow, approximately 10% of global ethylene capacity, 20% of propylene oxide capacity in Europe and North America, and over 25% of European siloxane capacity is being rationalized.

Dow emphasized its cost-advantaged asset footprint, noting that approximately 80% of its cracking capacity is positioned in the top quartile for cost efficiency.

Forward Guidance

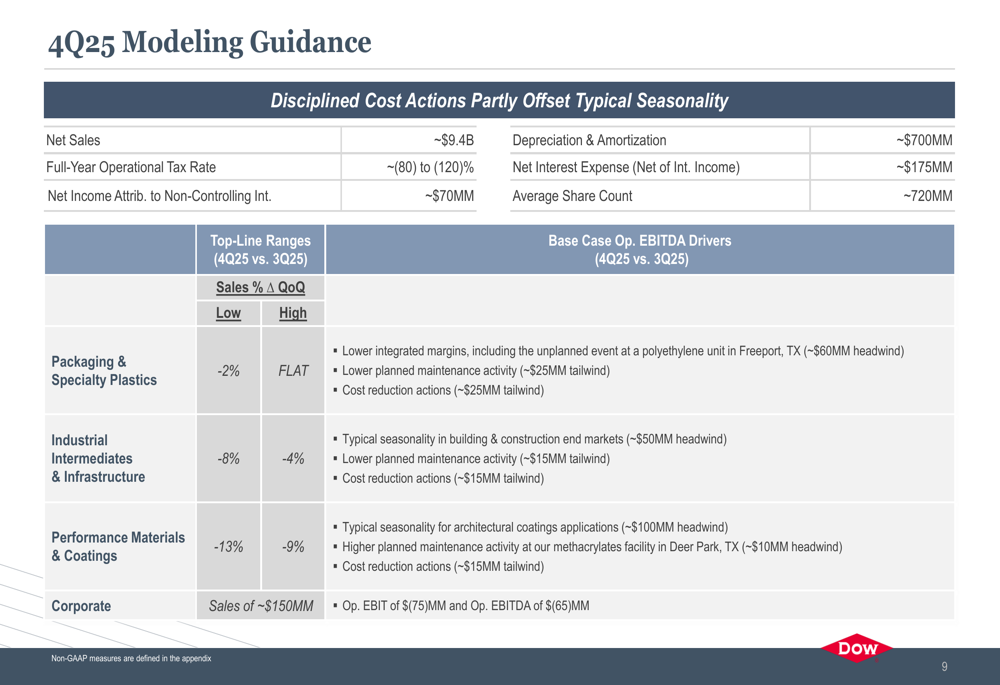

Looking ahead to the fourth quarter of 2025, Dow provided guidance for net sales of approximately $9.4 billion. The company expects typical seasonal patterns to affect performance, partially offset by disciplined cost actions.

Dow anticipates lower integrated margins in Packaging & Specialty Plastics, seasonal weakness in building and construction end markets for Industrial Intermediates & Infrastructure, and higher planned maintenance activity in Performance Materials & Coatings.

The company’s focus on operational and financial discipline, alongside strategic actions to generate cash, positions it to navigate the current challenging market environment while preparing for potential industry improvement as capacity rationalization takes effect globally.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.