Gold prices steady, holding sharp gains in wake of soft U.S. jobs data

DraftKings Inc (NASDAQ:DKNG) reported strong first-quarter results while reducing its full-year outlook due to unfavorable sports betting outcomes, according to the company’s Q1 2025 earnings presentation released on May 8.

The sports betting and iGaming operator saw its shares rise 1.67% to $35.94 in Thursday’s pre-market trading following the release.

Quarterly Performance Highlights

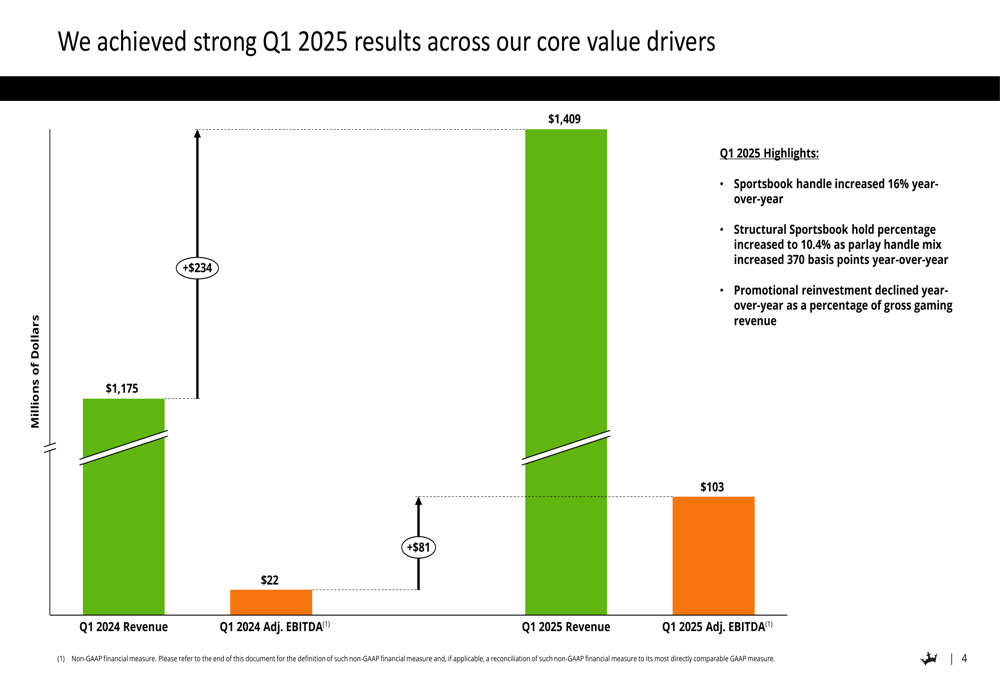

DraftKings delivered significant growth in Q1 2025, with revenue increasing 19.9% year-over-year to $1.41 billion, up from $1.18 billion in the same period last year. Adjusted EBITDA showed even more dramatic improvement, surging to $103 million from $22 million in Q1 2024, representing a 368% increase.

As shown in the following chart of quarterly performance:

The company attributed these strong results to several key factors, including a 16% year-over-year increase in Sportsbook handle, an improved structural Sportsbook hold percentage of 10.4%, and reduced promotional spending as a percentage of gross gaming revenue.

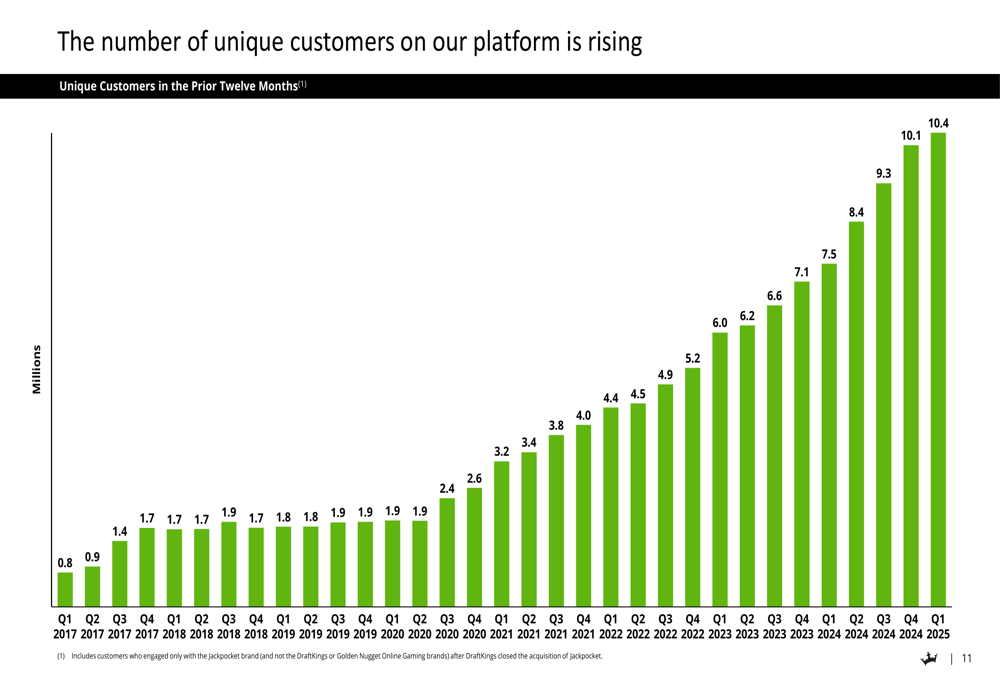

DraftKings’ customer base continued to expand, with unique customers reaching 10.4 million in Q1 2025, continuing a steady upward trend that has been evident since 2017:

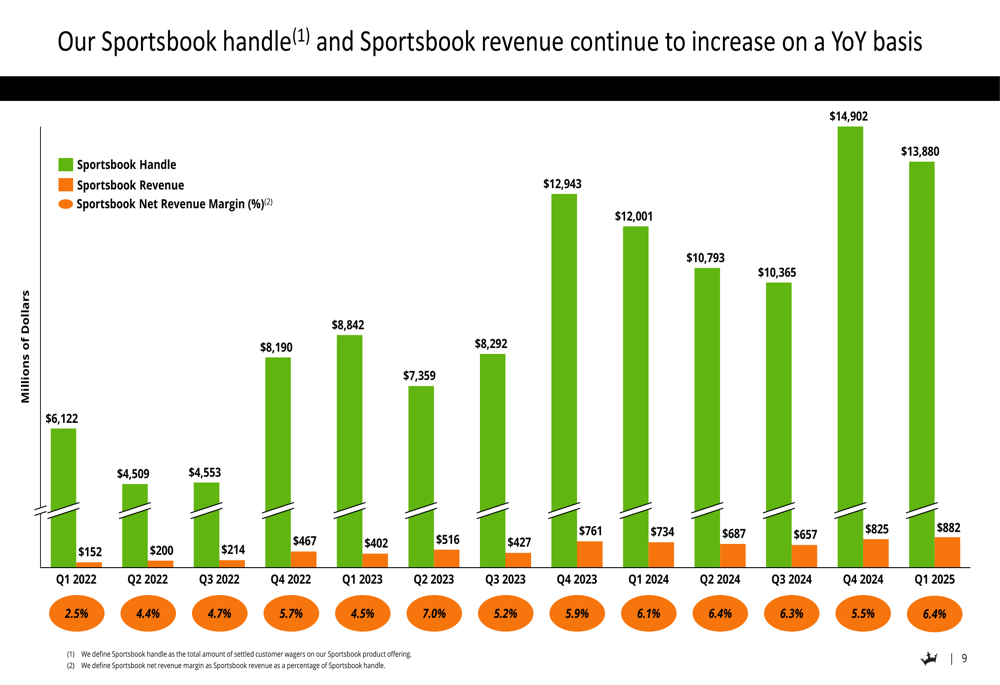

The company’s Sportsbook segment showed particularly strong performance, with handle reaching $13.88 billion and revenue climbing to $882 million in Q1 2025, maintaining a net revenue margin of 6.4%:

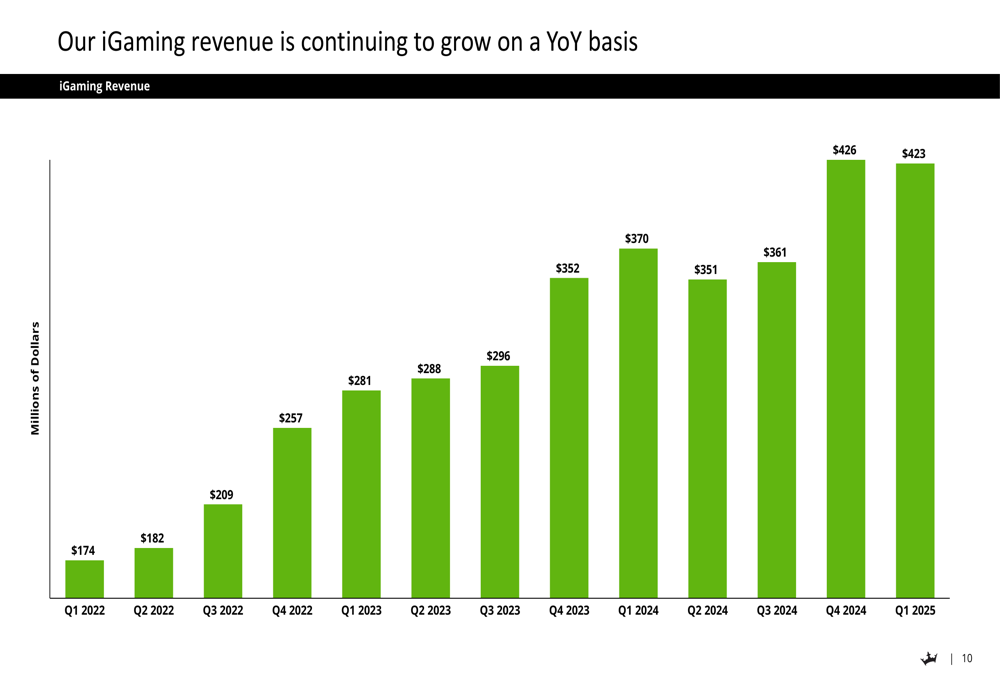

Meanwhile, the iGaming segment maintained its consistent growth trajectory, with revenue reaching $423 million in Q1 2025:

Guidance Revision and Challenges

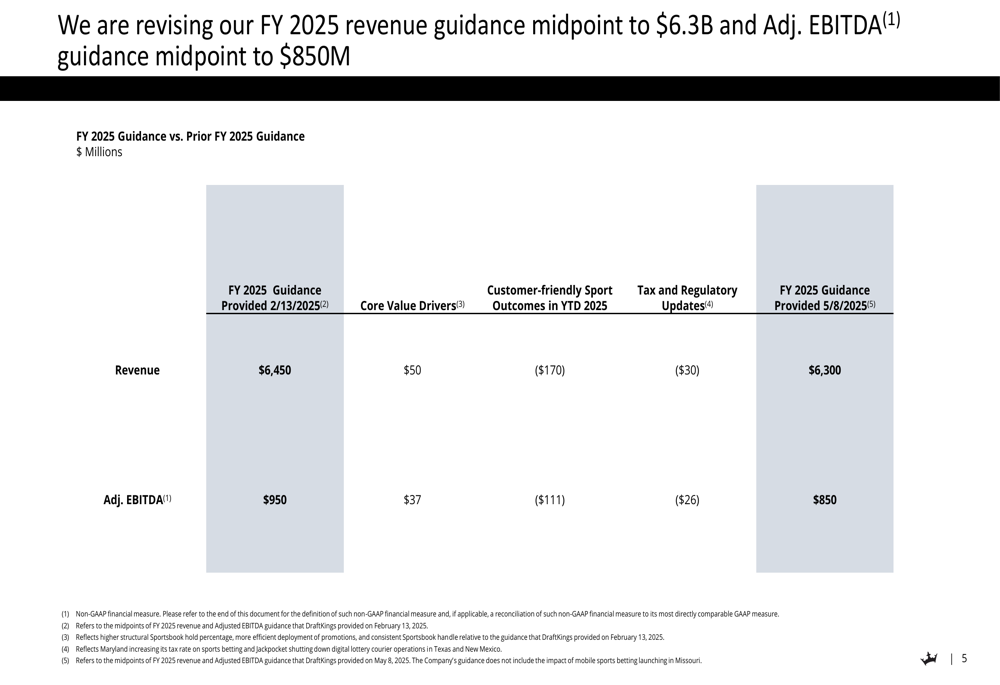

Despite the strong quarterly performance, DraftKings revised its full-year 2025 guidance downward, primarily due to customer-friendly sports outcomes. The company now expects full-year revenue of $6.3 billion, down from its previous forecast of $6.45 billion, and adjusted EBITDA of $850 million, reduced from $950 million.

The following chart breaks down the factors contributing to this guidance revision:

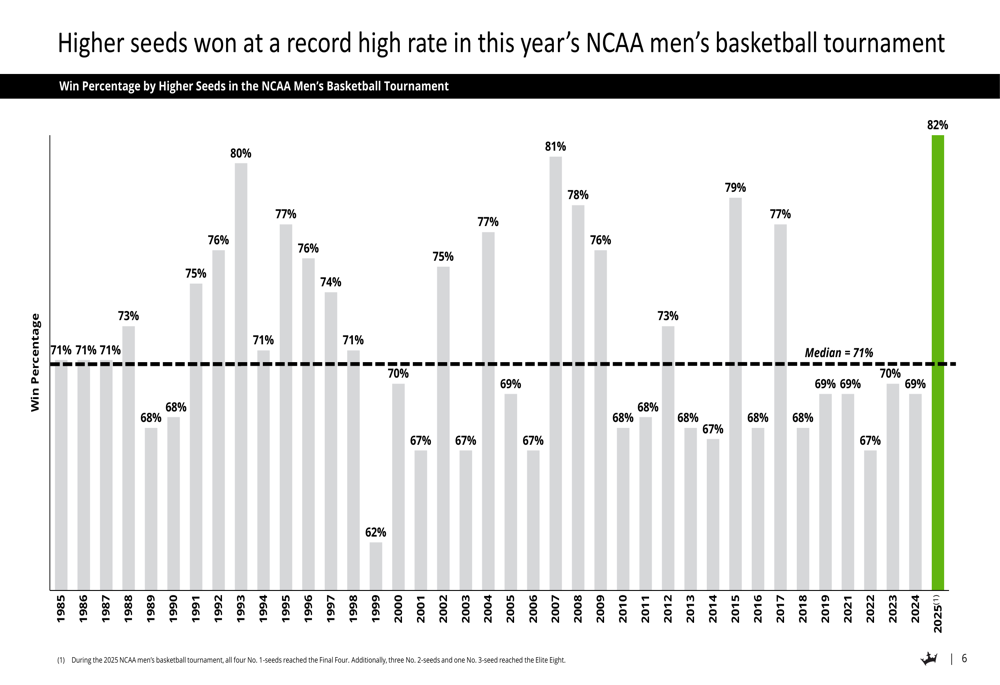

A significant factor in the guidance reduction was the unprecedented success of higher-seeded teams in the NCAA Men’s Basketball Tournament, where the win percentage by higher seeds reached a record 82% in 2025, well above the historical median of 71%:

"If not for customer-friendly outcomes in March, FY 2025 revenue and Adj. EBITDA guidance would be raised," the company stated in its presentation, noting that core value drivers were actually outperforming expectations.

Strategic Initiatives and Positioning

DraftKings highlighted its strong financial position, reporting $1.1 billion in cash after repurchasing 3.7 million shares in Q1 2025 under its existing stock repurchase program.

The company is emphasizing an "AI-first" mindset to "unlock greater speed, efficiency, and scale across the business," though specific AI initiatives were not detailed in the presentation.

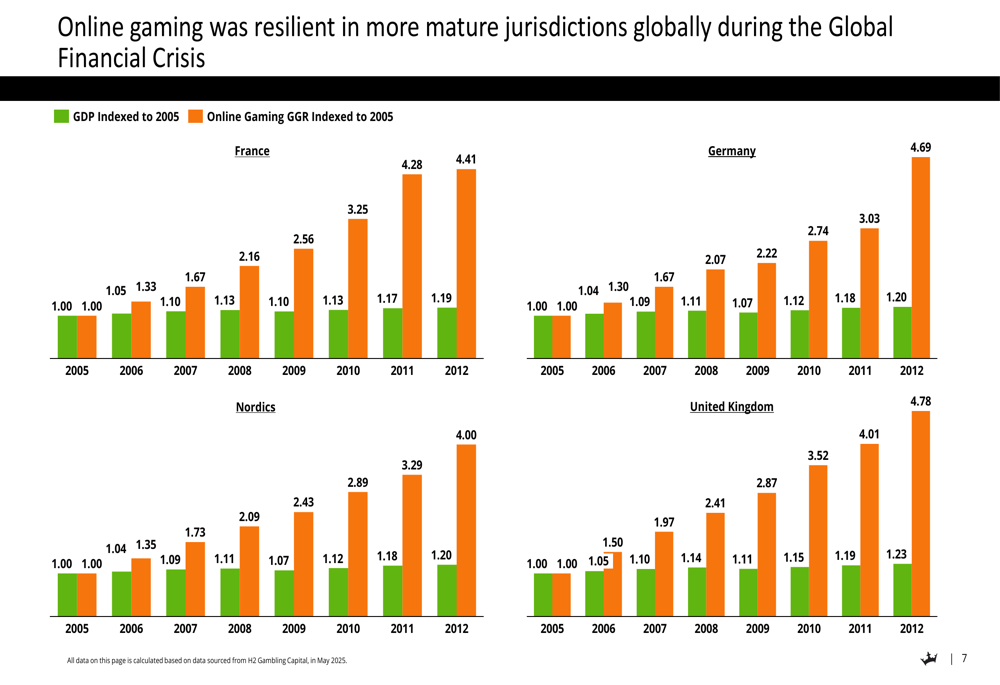

In anticipation of potential economic challenges, DraftKings presented historical data showing that online gaming remained resilient during the Global Financial Crisis in mature jurisdictions:

Detailed Financial Analysis

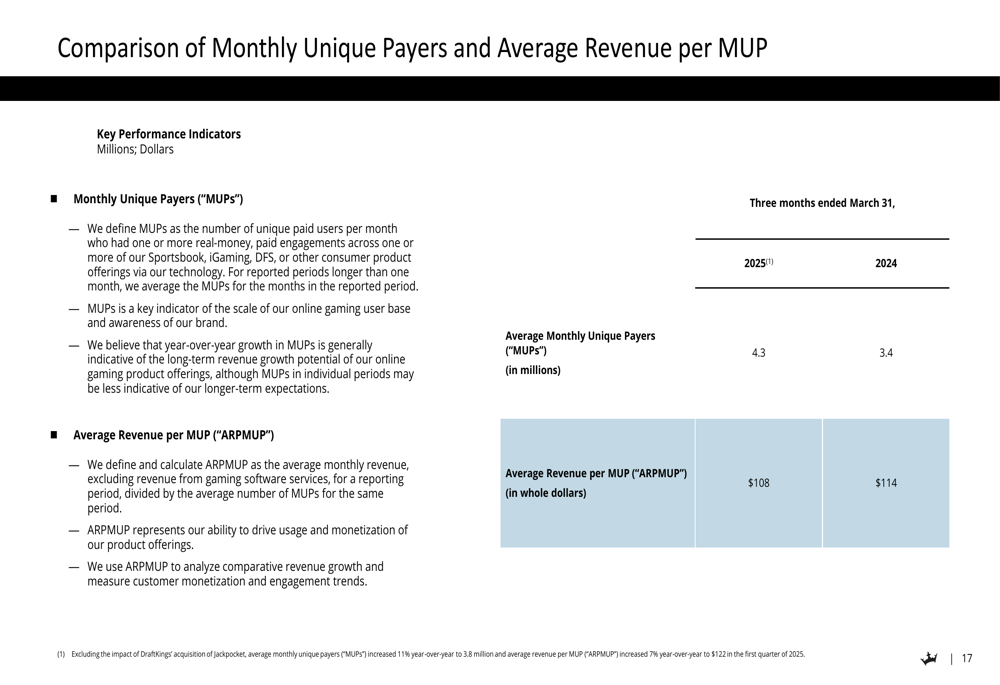

DraftKings’ monthly unique payers (MUPs) increased to 4.3 million in Q1 2025, up from 3.4 million in Q1 2024. However, average revenue per MUP decreased slightly to $108 from $114 in the prior year. The company noted that excluding the impact of its Jackpocket acquisition, average monthly unique payers increased 11% year-over-year to 3.8 million, and average revenue per MUP increased 7% year-over-year to $122.

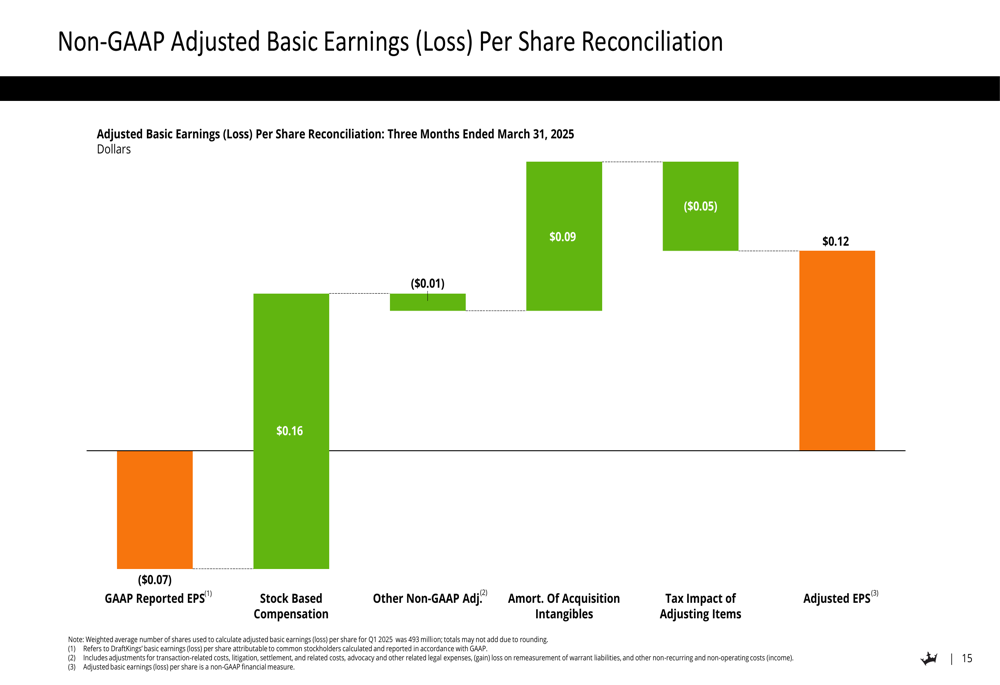

On a non-GAAP basis, DraftKings reported adjusted earnings per share of $0.12 for Q1 2025, compared to a GAAP reported EPS of -$0.07. The reconciliation shows significant adjustments for stock-based compensation ($0.16) and amortization of acquisition intangibles ($0.09):

Forward-Looking Statements

Despite the guidance reduction, DraftKings maintains an optimistic outlook on its core business. The company emphasized that structural improvements in its Sportsbook hold percentage and promotional efficiency improved year-over-year in Q1 2025.

The revised full-year 2025 guidance of $6.3 billion in revenue and $850 million in adjusted EBITDA still represents significant growth over previous years, though investors will likely focus on the impact of sports outcomes on the company’s profitability.

DraftKings’ emphasis on its resilience during economic downturns suggests the company is positioning itself defensively while continuing to pursue growth opportunities through improved operational efficiency and strategic initiatives like its AI-first approach.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.