Can anything shut down the Gold rally?

Introduction & Market Context

Dragonfly Energy Holdings Corp (NASDAQ:DFLI) presented its Q2 2025 investor update on August 14, highlighting the company’s continued recovery and strategic initiatives in the energy storage market. The lithium-ion battery developer, which focuses on deep-cycle applications, reported its sixth consecutive quarter of improving year-over-year performance trends.

The presentation comes as the company faces significant challenges, with its stock down over 90% year-to-date despite recent improvements in financial metrics. With a market capitalization of just $16.67 million, Dragonfly Energy is working to convince investors of its long-term viability in the competitive battery technology space.

Quarterly Performance Highlights

Dragonfly Energy reported Q2 2025 net sales of $16.2 million, representing a 23% increase year-over-year. This continues a recovery trend that began in Q4 2024, following several quarters of declining revenue.

As shown in the following quarterly revenue chart:

The company has demonstrated consistent improvement in year-over-year performance over the past six quarters, progressing from a 34% decline in Q1 2024 to 23% growth in the most recent quarter. Additionally, Dragonfly Energy reported a net loss of $7 million for Q2 2025, a significant improvement from the $13.6 million loss in the same period last year.

Other financial highlights include:

- Gross profit of $4.6 million, a 45.4% increase year-over-year

- Gross margin expansion of 430 basis points to 28.3%

- Adjusted EBITDA improvement to negative $2.2 million from negative $6.2 million

The company is targeting adjusted EBITDA breakeven by Q4 2025, a key milestone in its path to profitability.

Strategic Initiatives

Dragonfly Energy’s presentation emphasized its expansion beyond its traditional RV market stronghold into higher-growth sectors. The company identified significant market opportunities across three key segments:

As illustrated in this market opportunity breakdown:

The company is targeting a total addressable market of $56.8 billion across leisure, heavy-duty trucking, and industrial power applications. While the leisure segment (including RV, marine, and off-grid) represents a $1.7 billion opportunity, the industrial and remote power market offers substantially larger potential at $53.9 billion.

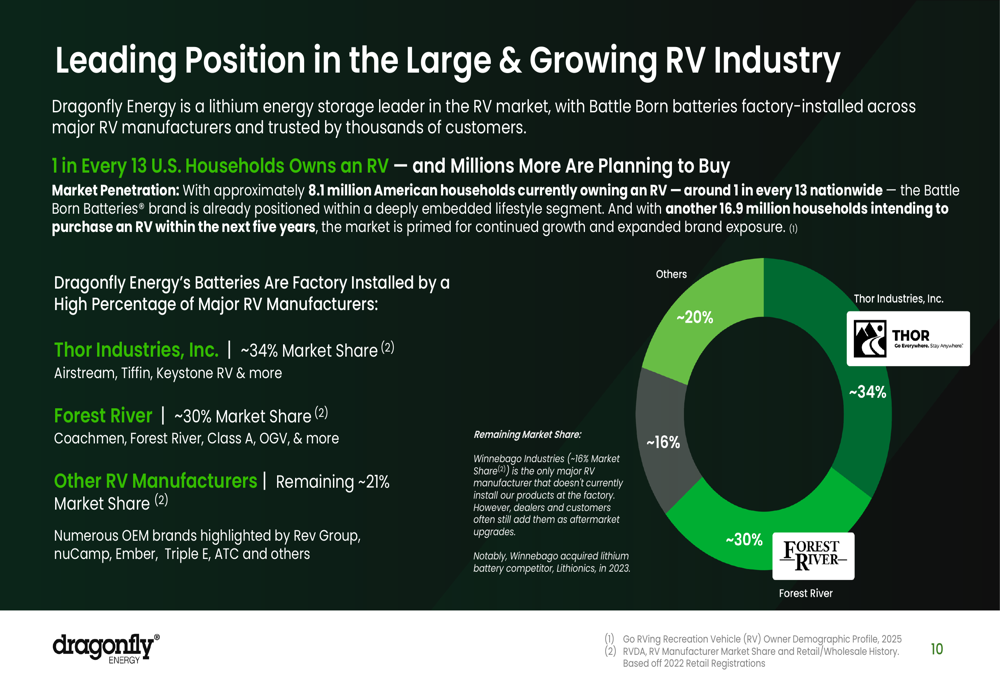

In the RV sector, Dragonfly Energy has established a dominant position with approximately 85% market share across major manufacturers:

The company’s strategic expansion into heavy-duty trucking focuses on all-electric auxiliary power units (APUs) that eliminate the need for diesel-powered idling. This addresses both regulatory concerns, as over 30 states have anti-idling laws, and operational efficiency by reducing fuel consumption.

"OEMs are coming to us for complete energy storage solutions," noted Wade Sieberg, CCO, during the recent earnings call, highlighting the company’s growing reputation as a comprehensive solution provider rather than just a battery manufacturer.

Competitive Industry Position

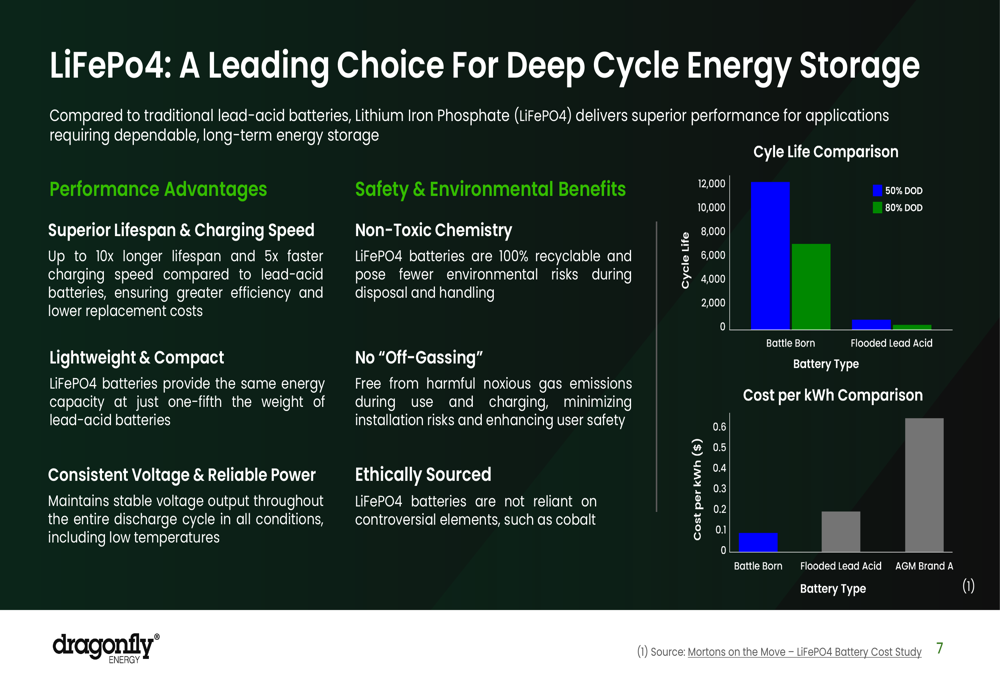

Dragonfly Energy’s presentation highlighted its technological advantages in the lithium-ion battery space, particularly its focus on lithium iron phosphate (LiFePO4) chemistry for deep-cycle applications. The company emphasized the performance and safety benefits compared to traditional lead-acid batteries:

A key differentiator for Dragonfly Energy is its intellectual property portfolio, which includes over 90 granted, filed, and pending patents across 12 countries. This patent protection covers battery chemistry, manufacturing processes, design, and system components.

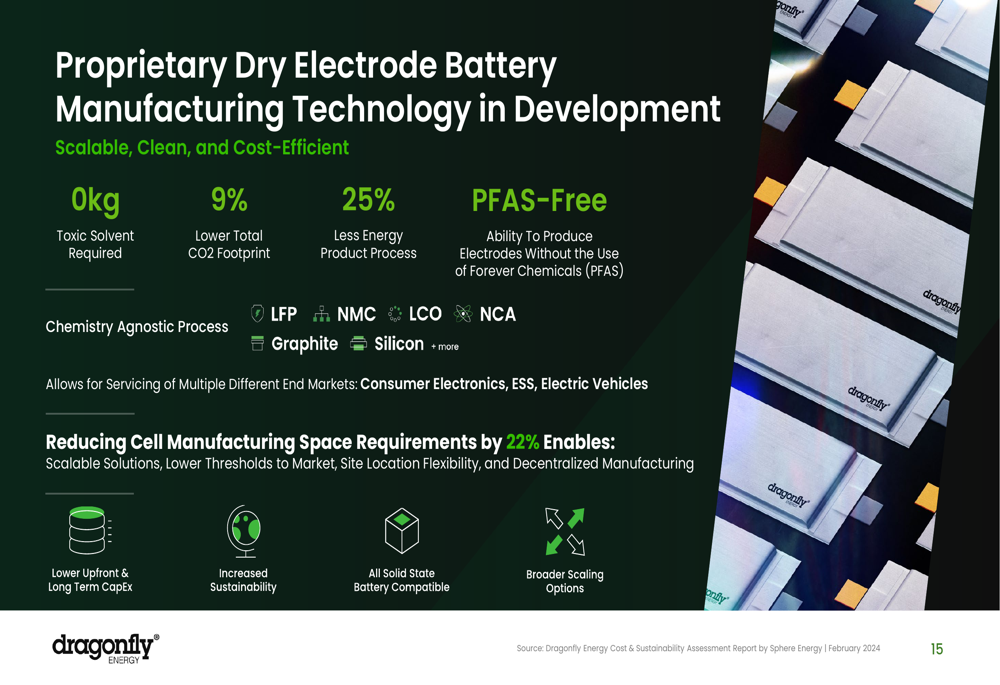

The company is also developing proprietary dry electrode battery manufacturing technology, which it claims offers significant advantages over conventional methods:

This solvent-free process reportedly reduces energy consumption by 25% and has a 9% lower total CO2 footprint compared to traditional manufacturing methods. The company positions this technology as enabling more cost-effective and environmentally friendly battery production in the United States.

Forward-Looking Statements

Dragonfly Energy’s presentation outlined several key initiatives aimed at achieving profitability by the end of 2025. The company is targeting 25% year-over-year growth for Q3 2025, with projected net sales of $15.9 million and an adjusted EBITDA of negative $2.7 million.

The company highlighted its investment thesis with five key points:

Long-term growth potential was emphasized through the company’s development of solid-state battery technology, which has demonstrated over 1,000 successful cycles in testing. This non-flammable battery technology eliminates liquid electrolytes, potentially offering significant safety advantages for energy storage applications.

CEO Dennis Farris expressed confidence in the company’s foundation during the earnings call, stating, "We believe we have the right foundation in place." However, the company faces ongoing challenges including macroeconomic uncertainties affecting consumer spending, supply chain complexities, and intense competition in the energy storage sector.

Despite the positive messaging in the presentation, investors should note that Dragonfly Energy remains in a precarious financial position with its small market capitalization and continued operating losses. The company’s ability to execute its expansion strategy while achieving its profitability targets will be crucial for long-term viability in an increasingly competitive market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.