Bitcoin price today: falls to 2-week low below $113k ahead of Fed Jackson Hole

Introduction & Market Context

Dropbox Inc. (NASDAQ:DBX) recently presented its Q1 2025 financial results, showcasing improved profitability metrics despite stagnant revenue growth. The cloud storage and collaboration company reported mixed results, with an earnings beat offset by a slight revenue miss against analyst expectations. Dropbox stock closed at $29.69 on May 9, 2025, down 0.13% from the previous day, following a 1.28% decline in after-hours trading immediately after the earnings announcement.

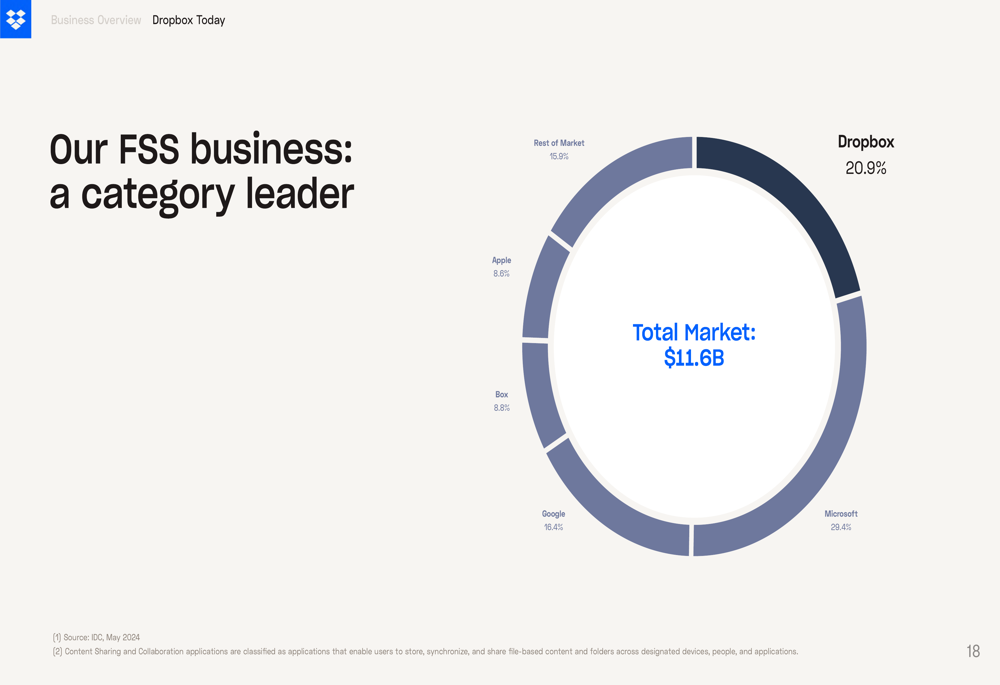

The company continues to maintain its position as the second-largest player in the File Sync and Share (FSS) market with a 20.9% share, trailing only Microsoft (NASDAQ:MSFT)’s 29.4% but ahead of Google (NASDAQ:GOOGL)’s 16.4%.

Quarterly Performance Highlights

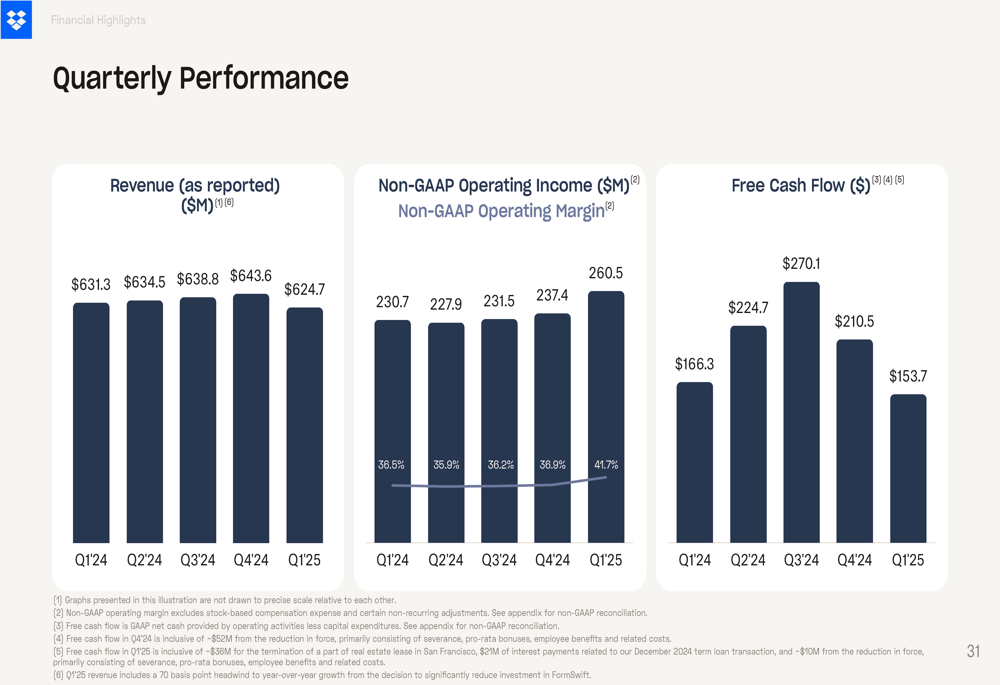

Dropbox reported Q1 2025 revenue of $624.7 million, representing a 1% year-over-year decline and falling short of analyst expectations of $630.83 million. Despite the revenue shortfall, the company delivered strong profitability with non-GAAP earnings per share of $0.70, exceeding the forecasted $0.63 by 11%.

As shown in the following quarterly performance chart, Dropbox has significantly improved its operating margins while maintaining relatively stable revenue:

The company’s non-GAAP operating margin expanded impressively to 41.7% in Q1 2025, up from 36.5% in the same period last year, representing a 500 basis point improvement. However, free cash flow declined from $166.3 million in Q1 2024 to $153.7 million in Q1 2025.

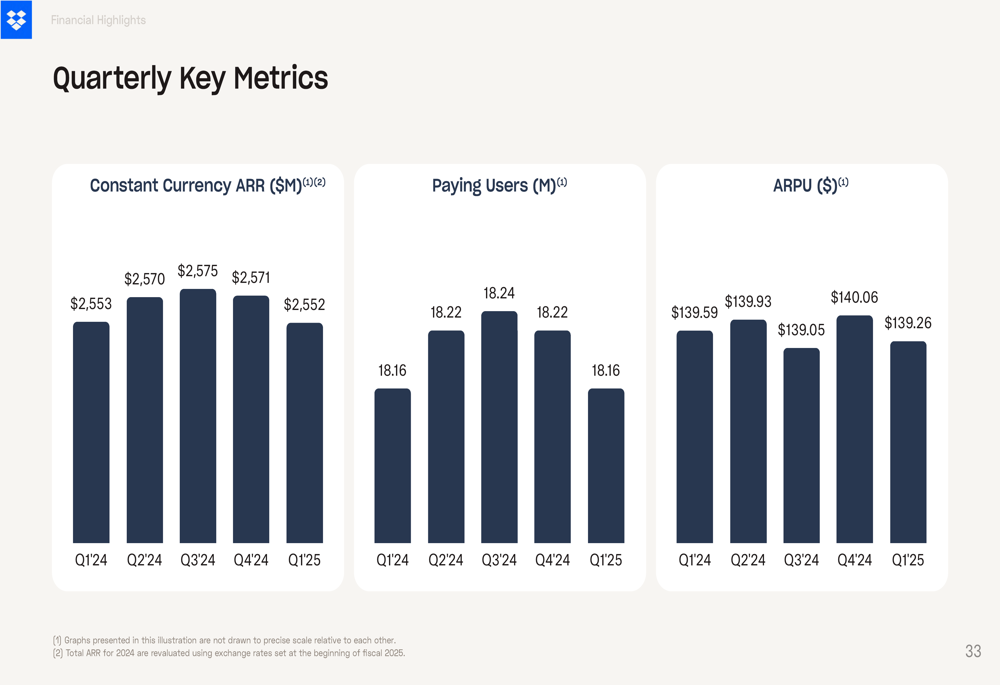

Dropbox’s user metrics remained relatively flat, with paying users holding steady at 18.16 million, though the earnings call revealed a sequential decline of 60,000 users. Average revenue per user (ARPU) was $139.26, showing a slight decrease from $139.59 in the previous quarter.

Financial Position and Capital Allocation

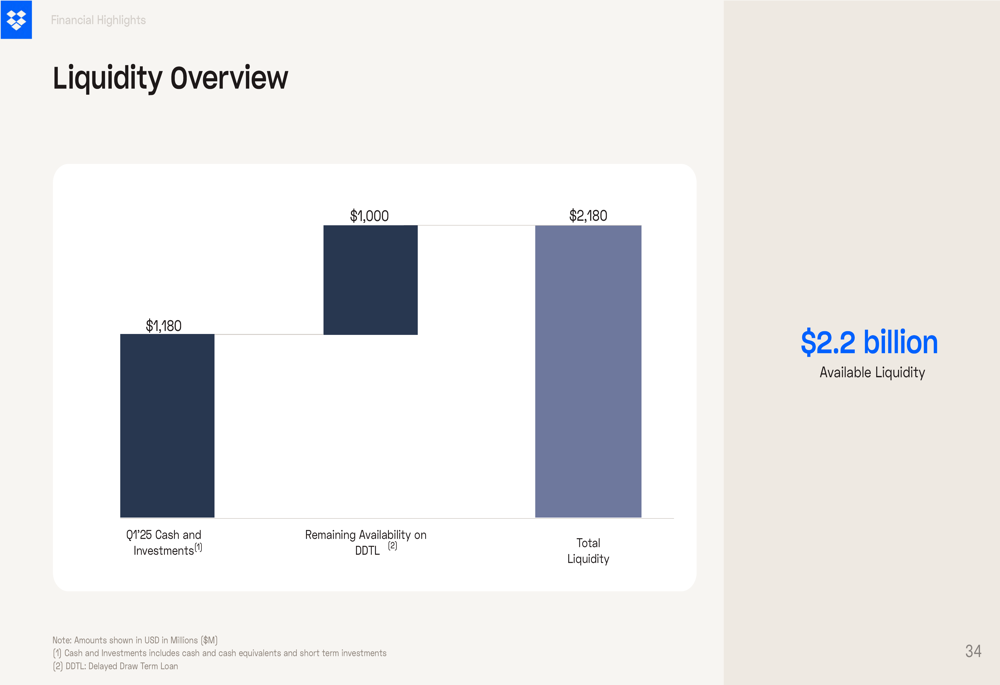

Dropbox maintains a strong financial position with $1.18 billion in cash and investments as of Q1 2025, providing substantial liquidity for operations and strategic initiatives. The company also has access to an additional $1 billion in debt facilities, bringing total liquidity to $2.2 billion.

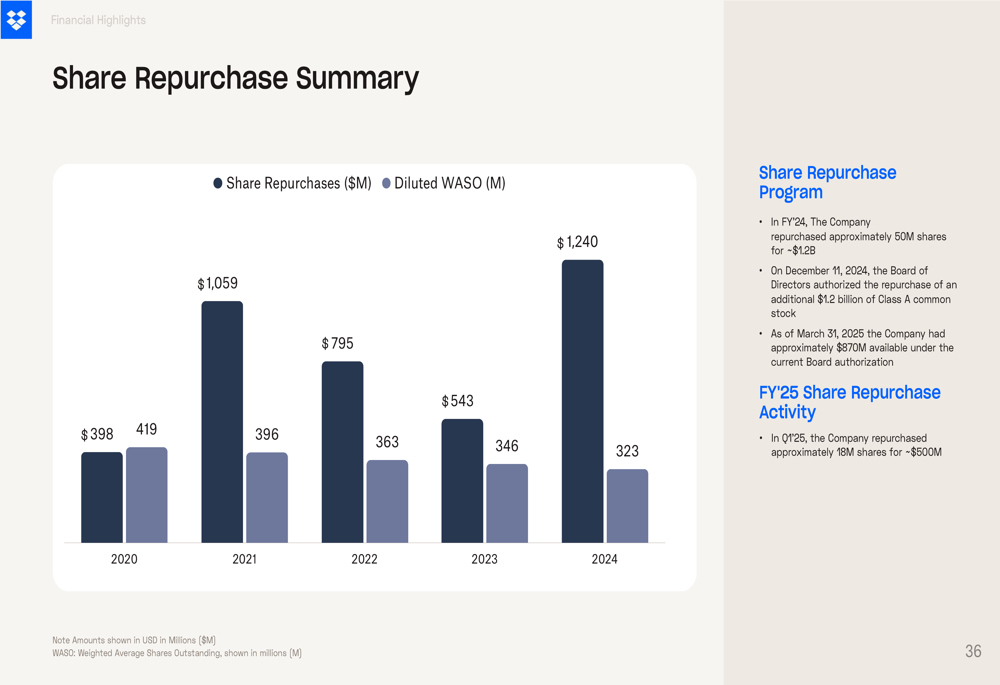

The company has demonstrated a commitment to returning capital to shareholders through an aggressive share repurchase program. As illustrated in the following chart, Dropbox has significantly increased its buyback activity in recent years, with $1.24 billion spent on repurchases in 2024 alone:

Strategic Initiatives

Dropbox’s presentation highlighted its strategic focus on expanding beyond traditional file storage and sharing into AI-powered content organization and discovery through its Dash for Business product. The company describes Dash as a solution that combines "universal search and organization with content access control," allowing users to "find anything, protect everything."

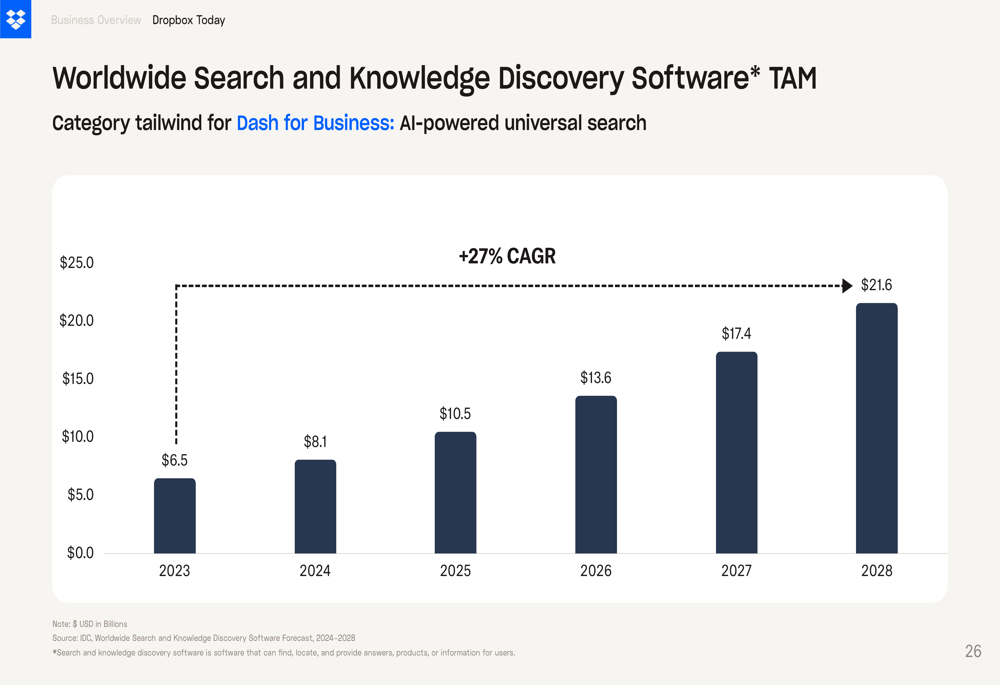

The presentation emphasized the substantial market opportunity for Dash, with the worldwide Search and Knowledge Discovery (NASDAQ:WBD) Software (ETR:SOWGn) total addressable market projected to grow from $6.5 billion in 2023 to $21.6 billion in 2028, representing a 27% compound annual growth rate:

During the earnings call, CEO Drew Houston emphasized the company’s strategic focus, stating, "We’re focused on what we can control, and we’ll continue refining our execution as we pursue the DASH opportunity." This underscores Dropbox’s commitment to this new growth vector amid challenges in its core business.

Competitive Industry Position

Dropbox maintains a strong position in the File Sync and Share market, with the second-largest market share at 20.9%. The company operates in a competitive landscape dominated by tech giants Microsoft, Google, and Apple (NASDAQ:AAPL), along with direct competitor Box:

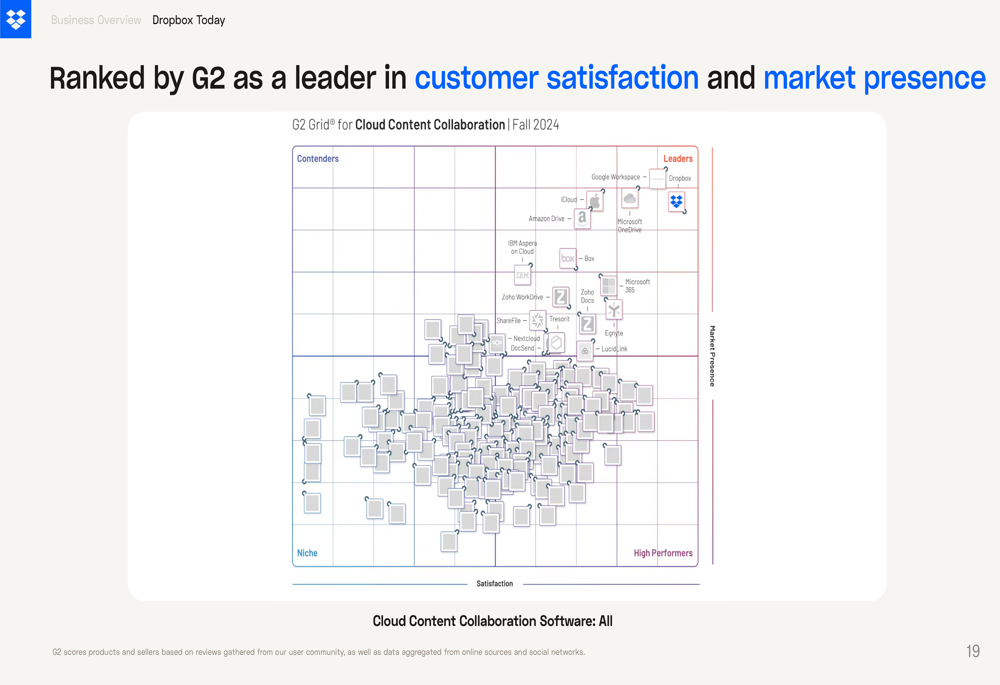

The company’s competitive strength is further validated by its position in the "Leaders" quadrant of the G2 Grid for Cloud Content Collaboration as of Fall 2024, placing it among top industry performers in terms of market presence and customer satisfaction.

Dropbox’s infrastructure spans the globe, with the company noting that it secures and organizes over 1 trillion pieces of content. Total (EPA:TTEF) customer storage has more than doubled from 2,100 petabytes in 2020 to 4,700 petabytes in 2024, demonstrating the growing reliance on its platform despite relatively flat user growth.

Forward-Looking Statements

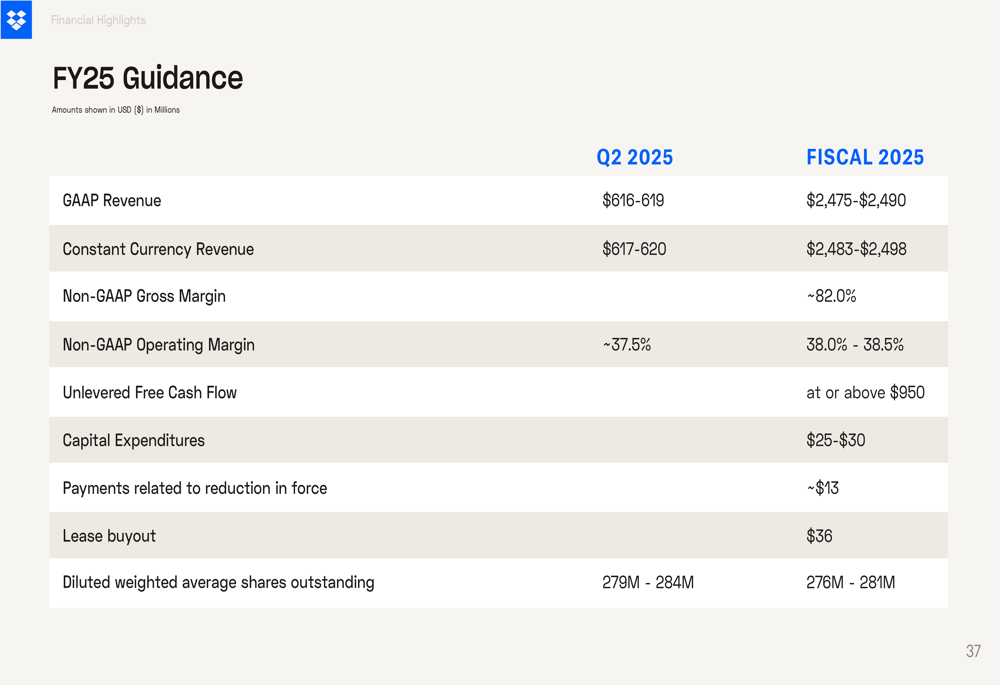

For the full year 2025, Dropbox provided guidance for revenue between $2.475 billion and $2.490 million, with Q2 2025 revenue projected at $616-619 million. The company also raised its non-GAAP operating margin guidance to 38-38.5% and expects unlevered free cash flow to be at or above $950 million.

Management anticipates a decline in paying users by approximately 300,000 for the full year, highlighting ongoing challenges in user growth. However, the company remains focused on improving profitability and efficiency while investing in new opportunities like Dash.

CFO Tim Regan noted during the earnings call, "We are executing well against our strategy of generating higher levels of efficiency across our core file ticket share and document workflow businesses," reinforcing the company’s focus on operational excellence amid revenue challenges.

Investment Considerations

Dropbox’s presentation highlighted several key investment considerations, including its scaled platform, subscription-based recurring revenue model, high margins, strong free cash flow conversion, and consistent capital return to shareholders:

With a price-to-earnings ratio of 20.95 and strong free cash flow yield of 10%, Dropbox presents a potentially attractive valuation for investors focused on profitability and cash generation rather than top-line growth. The company’s financial health score is rated as "GREAT" according to InvestingPro data, with impressive gross profit margins of 82.63%.

However, investors should consider the challenges in user growth and revenue expansion, as well as increasing competition in the cloud storage and collaboration space. The company’s strategic pivot toward AI-powered solutions like Dash represents both an opportunity and execution risk as Dropbox seeks new growth vectors in an increasingly competitive market.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.