Robinhood reports August 2025 customer and trading metrics

Introduction & Market Context

Ducommun Incorporated (NYSE:DCO), a leading aerospace and defense supplier, presented its Q2 2025 earnings results on August 7, 2025, showcasing solid performance despite mixed market conditions. The company’s stock has shown remarkable strength this year, currently trading at $91.37, up significantly from $61.15 following its Q1 results.

The presentation highlighted Ducommun’s ability to navigate ongoing commercial aerospace challenges through its diversified business model, with defense segment growth offsetting weakness in commercial programs. This performance comes amid continued production rate uncertainties at major customers like Boeing (NYSE:BA), while defense spending remains robust.

Quarterly Performance Highlights

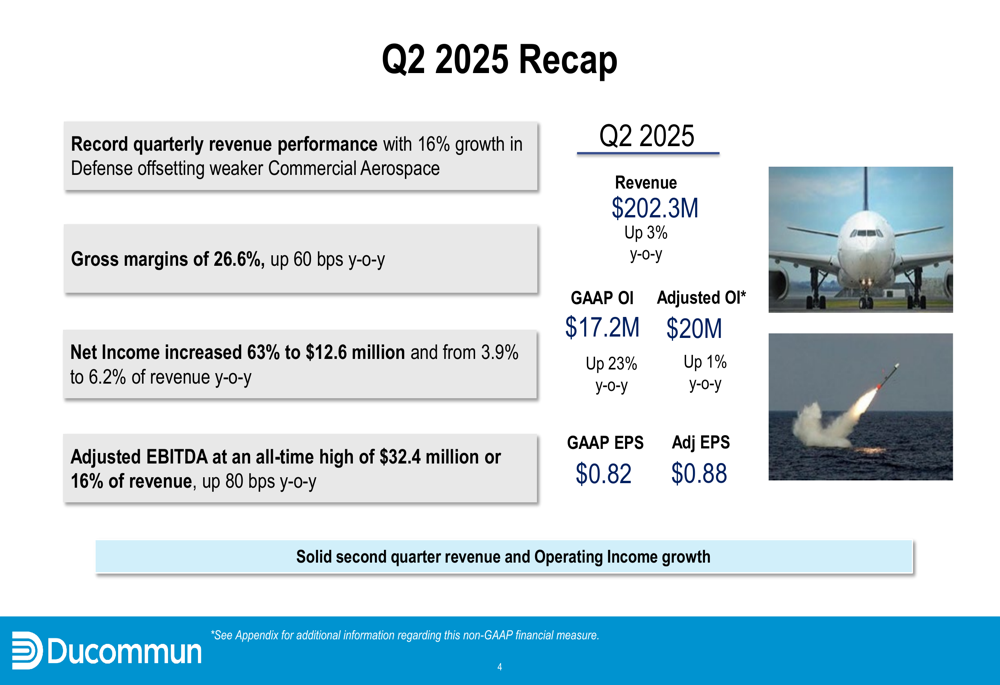

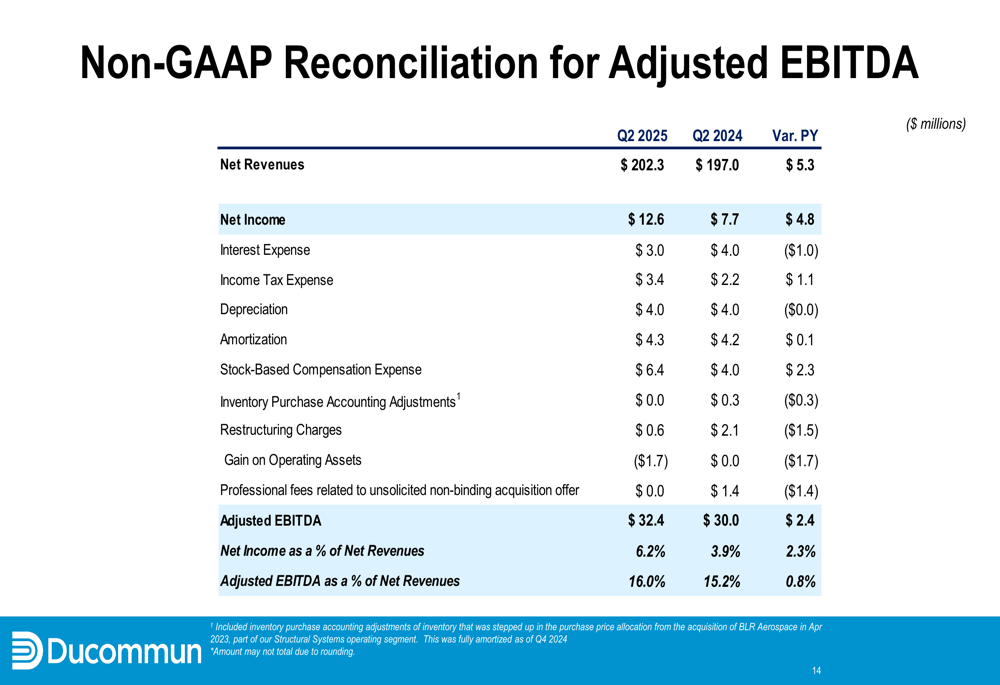

Ducommun reported record quarterly revenue of $202.3 million, representing a 3% year-over-year increase. More impressively, net income surged 63% to $12.6 million, improving from 3.9% to 6.2% of revenue compared to the same period last year.

As shown in the following comprehensive performance summary:

The company achieved an all-time high Adjusted EBITDA of $32.4 million or 16% of revenue, an 80 basis point improvement year-over-year. Gross margins improved to 26.6%, up 60 basis points from Q2 2024. Operating income showed strong growth with GAAP operating income up 23% to $17.2 million, while adjusted operating income increased 1% to $20 million.

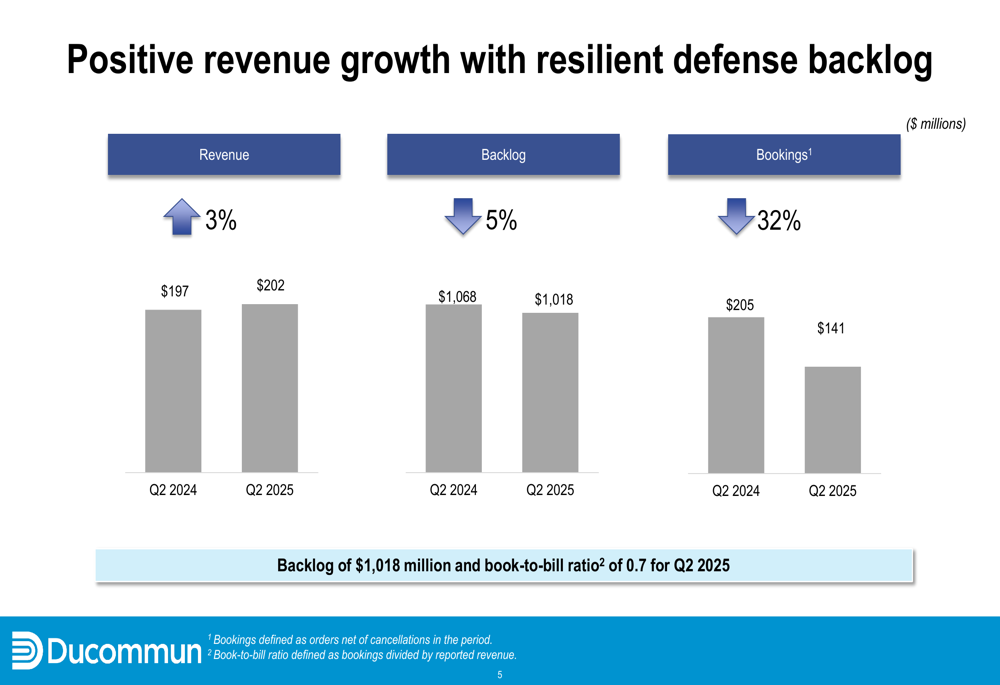

However, the company’s backlog decreased 5% year-over-year to $1.018 billion, with bookings down 32% to $141 million, resulting in a book-to-bill ratio of 0.7 for the quarter.

Segment Analysis

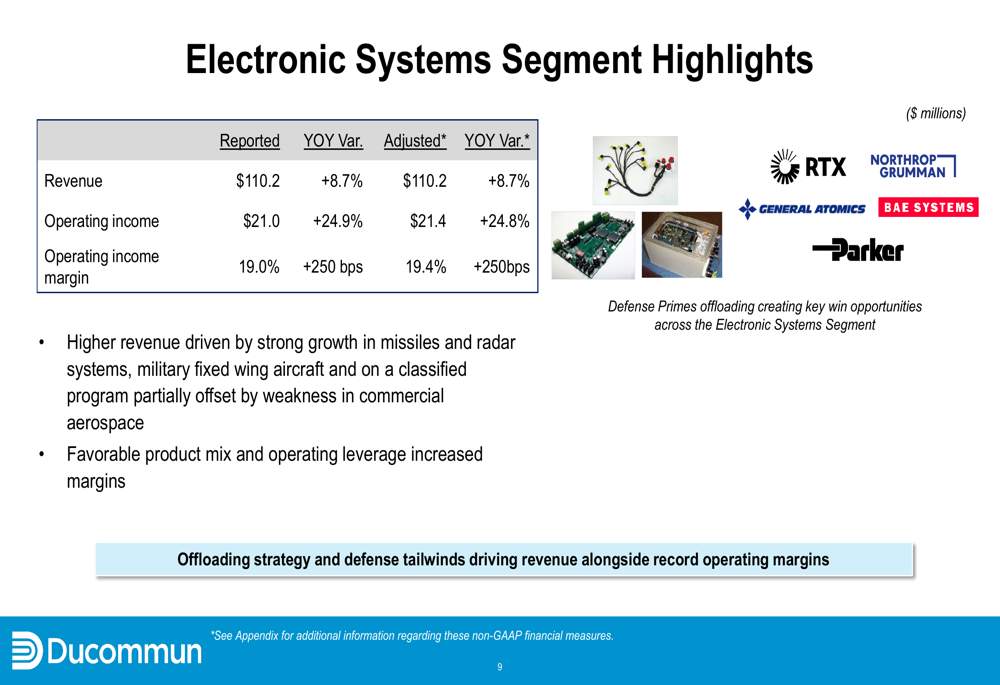

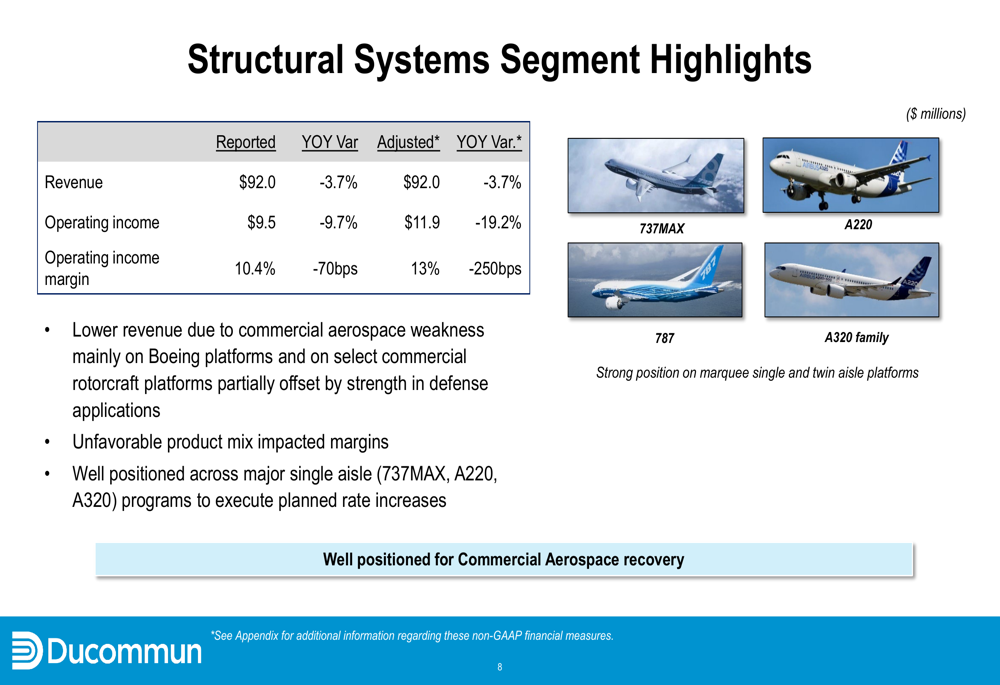

Ducommun’s performance revealed a tale of two segments, with Electronic Systems showing remarkable strength while Structural Systems faced headwinds.

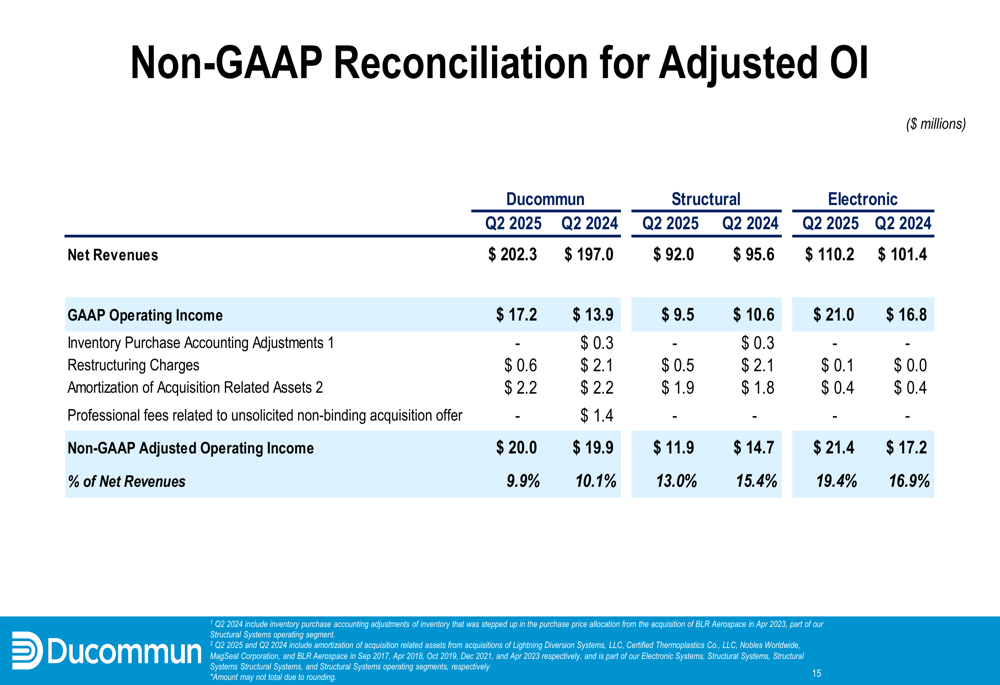

The Electronic Systems segment delivered impressive results with revenue of $110.2 million, up 8.7% year-over-year. Even more notable was the operating income increase of 24.9% to $21.0 million, with margins expanding 250 basis points to 19.0%. This growth was primarily driven by strong demand in missiles, radar systems, military fixed-wing aircraft, and classified programs.

In contrast, the Structural Systems segment experienced challenges with revenue declining 3.7% to $92.0 million and operating income dropping 9.7% to $9.5 million. The company attributed this weakness to commercial aerospace challenges, particularly on Boeing platforms and select commercial rotorcraft programs. Despite these near-term headwinds, management emphasized that the segment remains well-positioned across major single-aisle aircraft programs to benefit from planned production rate increases.

Restructuring Progress

A key focus of the presentation was Ducommun’s ongoing restructuring initiatives, which have made significant progress. The company has completed the cessation of all production activities at both Monrovia, California and Berryville, Arkansas facilities, with the Berryville facility already sold in the second quarter.

The restructuring is expected to yield substantial benefits, with anticipated annualized run-rate savings of $11 million to $13 million. During Q2 2025, the company recorded $0.6 million in restructuring charges and estimates an additional $0.5-1.0 million in product requalification and facility consolidation costs through the remainder of 2025.

Outlook and Vision 2027 Targets

Ducommun reiterated its full-year 2025 revenue growth outlook of mid-single digits, with growth expected to accelerate through year-end. Specifically, management anticipates mid-single-digit growth in Q3 and low double-digit growth in Q4, driven by continued defense momentum.

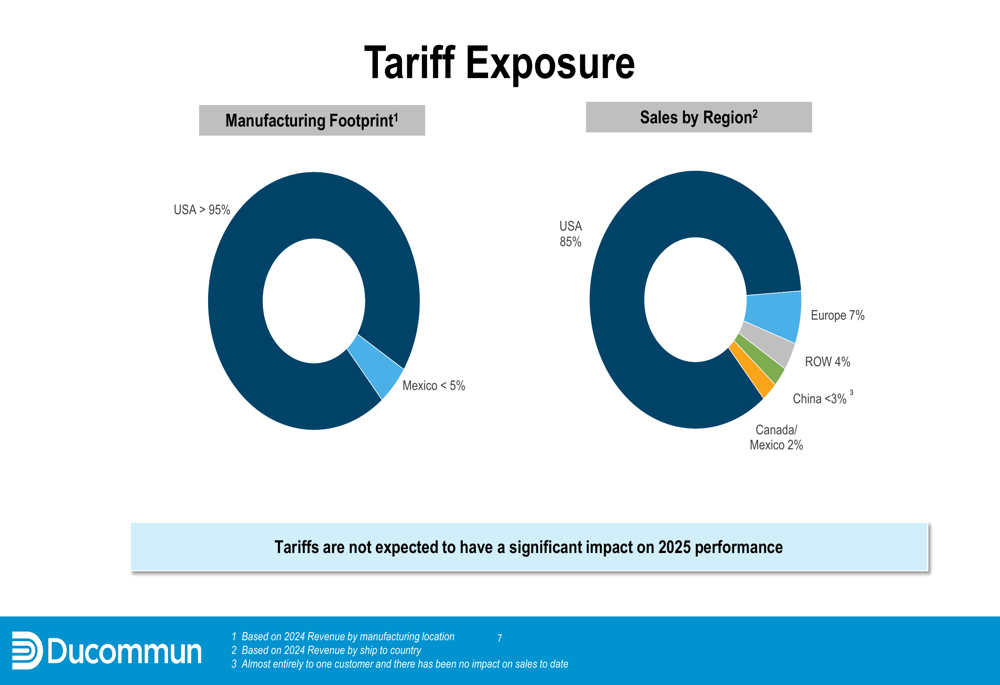

The company also addressed potential tariff concerns, noting minimal exposure with over 95% of manufacturing located in the USA and less than 3% of sales to China. This positioning should insulate Ducommun from significant trade-related disruptions.

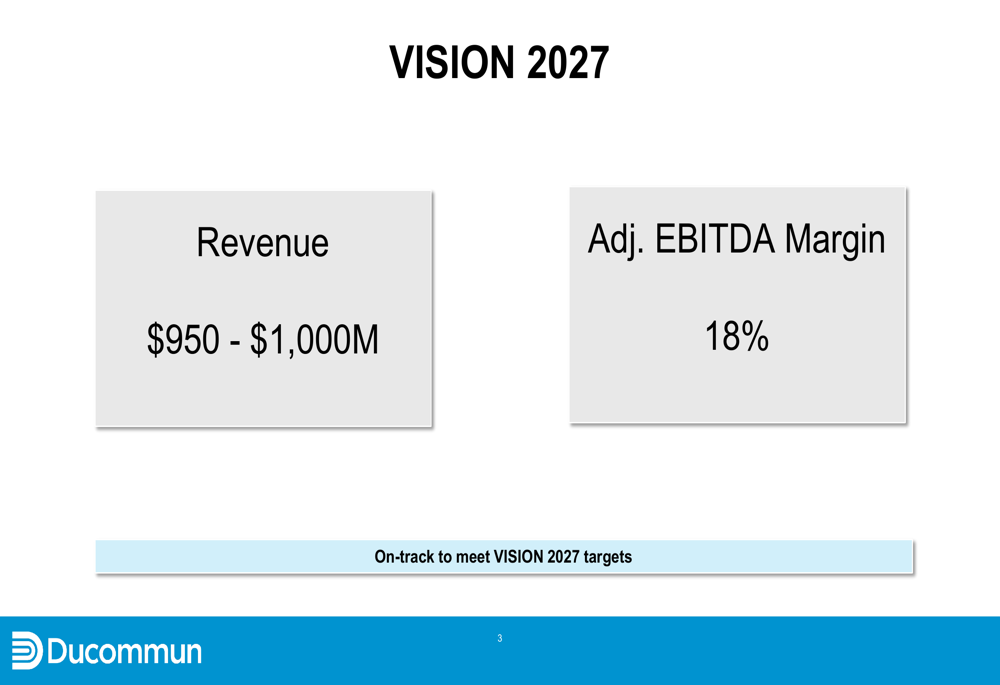

Looking further ahead, management confirmed they remain on track to meet their Vision 2027 targets, which include revenue of $950 million to $1 billion and an adjusted EBITDA margin of 18%. These targets represent significant growth from current levels and suggest continued confidence in the company’s long-term strategy.

The detailed reconciliation of GAAP to non-GAAP measures provides transparency into Ducommun’s financial performance. Adjusted EBITDA of $32.4 million (16.0% of revenue) represents a significant improvement from $30.0 million (15.2% of revenue) in Q2 2024.

Similarly, the segment-level adjusted operating income breakdown shows the strength of the Electronic Systems segment, with margins of 19.4% compared to 13.0% for Structural Systems.

Despite near-term challenges in commercial aerospace, Ducommun’s Q2 2025 results demonstrate the company’s resilience through its diversified business model, operational efficiency improvements, and strategic restructuring initiatives. With defense growth momentum and anticipated commercial aerospace recovery, the company appears well-positioned to achieve its long-term financial targets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.