Gold bars to be exempt from tariffs, White House clarifies

Introduction & Market Context

Duke Energy Corporation (NYSE:DUK) presented its Q2 2025 earnings review and business update on August 5, 2025, revealing strategic transactions designed to fund an ambitious capital plan while delivering solid quarterly results. The company reported adjusted earnings per share (EPS) of $1.25, exceeding analysts’ expectations of $1.21 and representing a 3.31% positive surprise.

Following the announcement, Duke Energy’s stock rose by 1.47% in pre-market trading to $126, reflecting investor confidence in the company’s performance and strategic direction. The utility giant reaffirmed its 2025 EPS guidance range of $6.17 to $6.42 and maintained its long-term growth rate of 5-7% through 2029.

Strategic Transactions

The presentation highlighted two major transactions that will generate approximately $7.5 billion in net proceeds at premium valuations, strengthening Duke Energy’s credit profile and funding future capital investments.

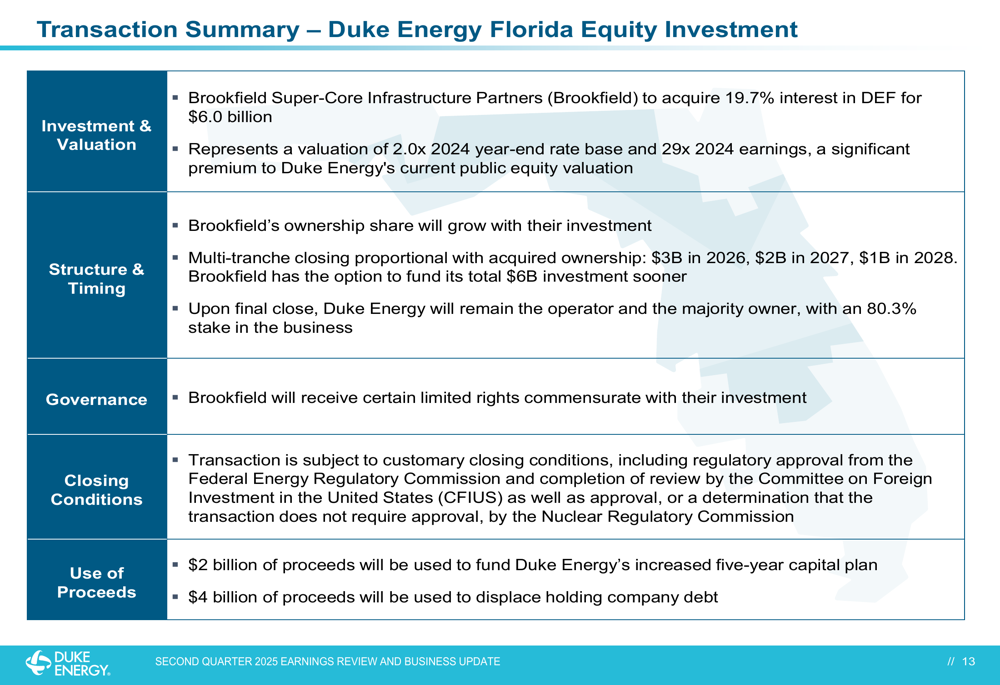

As shown in the following transaction summary, Brookfield Super-Core Infrastructure Partners will acquire a 19.7% interest in Duke Energy Florida for $6.0 billion, representing a valuation of 2.0x 2024 year-end rate base and 29x 2024 earnings:

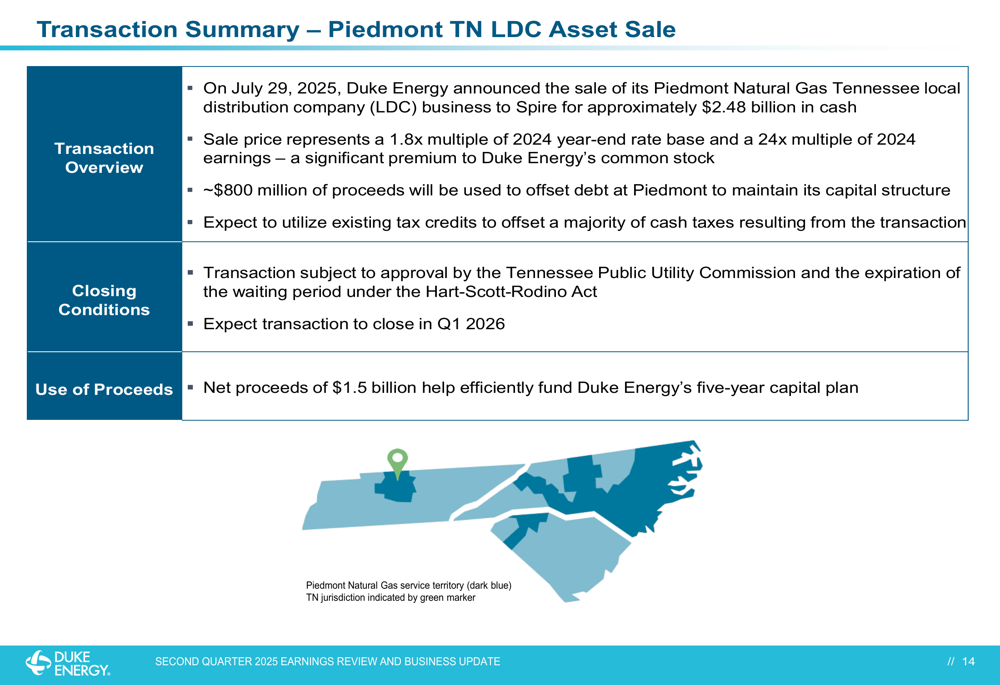

The second transaction involves the sale of Piedmont Natural Gas Tennessee local distribution company business to Spire (NYSE:SR) for approximately $2.48 billion, representing a 1.8x multiple of 2024 year-end rate base:

Duke Energy plans to use the combined net proceeds to offset $1.5 billion in common equity, fund $2 billion of its increased $87 billion five-year capital plan, and displace $4 billion of holding company debt. CEO Harry Sideris emphasized the strategic importance of these transactions, stating, "These transactions allow us to efficiently finance the record growth ahead of us."

Quarterly Performance Highlights

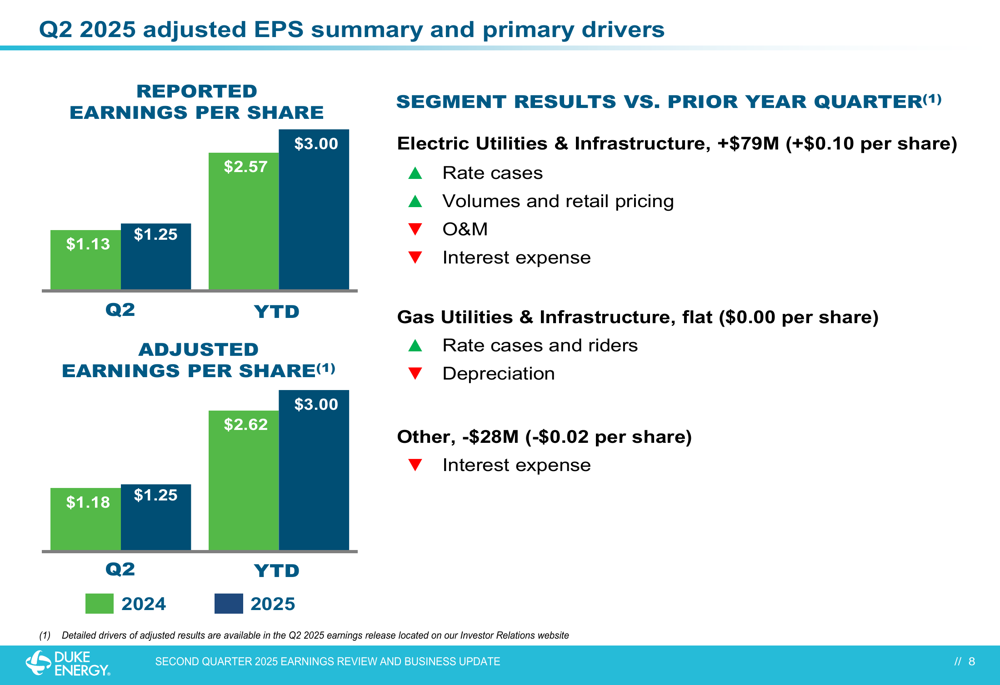

Duke Energy’s Q2 2025 adjusted EPS of $1.25 represented an increase from $1.13 in Q2 2024, driven primarily by strong performance in the Electric Utilities & Infrastructure segment. Year-to-date adjusted EPS reached $3.00, compared to $2.57 for the same period in 2024.

The following chart details the primary drivers behind the quarterly results:

The Electric Utilities & Infrastructure segment contributed an additional $0.10 per share year-over-year, driven by rate cases, increased volumes, retail pricing, and operational efficiencies. The Gas Utilities & Infrastructure segment remained flat, while the Other segment decreased by $0.02 per share primarily due to higher interest expenses.

Growth Initiatives

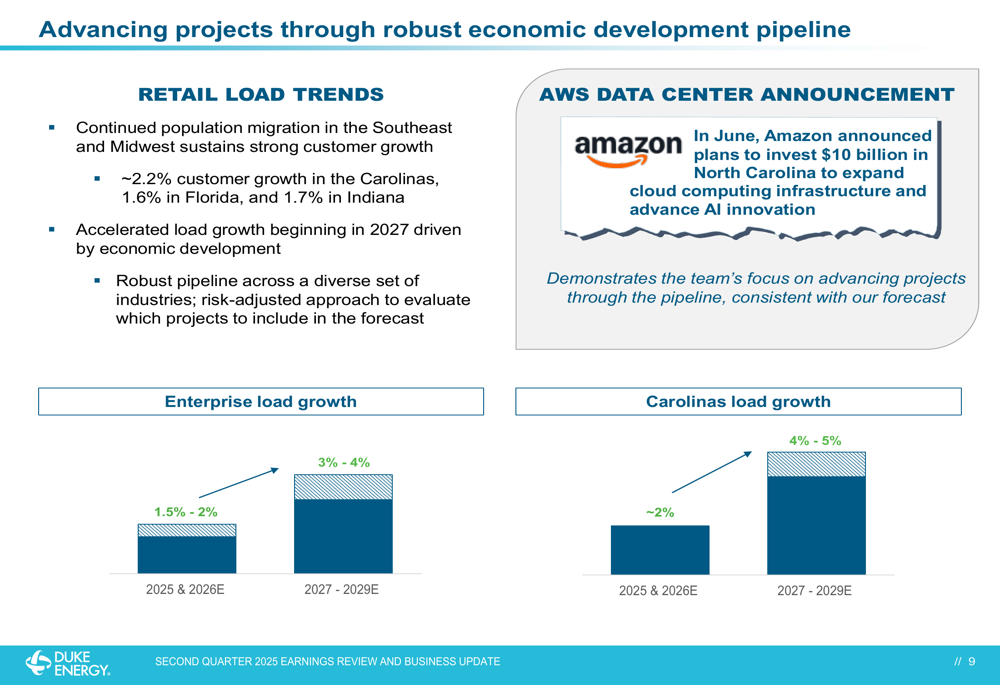

Duke Energy highlighted significant economic development opportunities driving future growth, particularly in the data center sector. Amazon (NASDAQ:AMZN) Web Services announced a $10 billion investment in North Carolina to expand its cloud computing infrastructure, which is expected to accelerate load growth beginning in 2027.

As illustrated in the following chart, Duke Energy projects enterprise load growth of 1.5%-2% in 2025-2026, accelerating to 3%-4% in 2027-2029, with even stronger growth in the Carolinas:

To meet this growing demand, Duke Energy is advancing over 8 GW of new dispatchable generation, including maximizing its existing fleet through uprates and progressing more than 7 GW of new gas generation. The company has secured turbines and contracted gas supply for all announced plants:

Financial Outlook

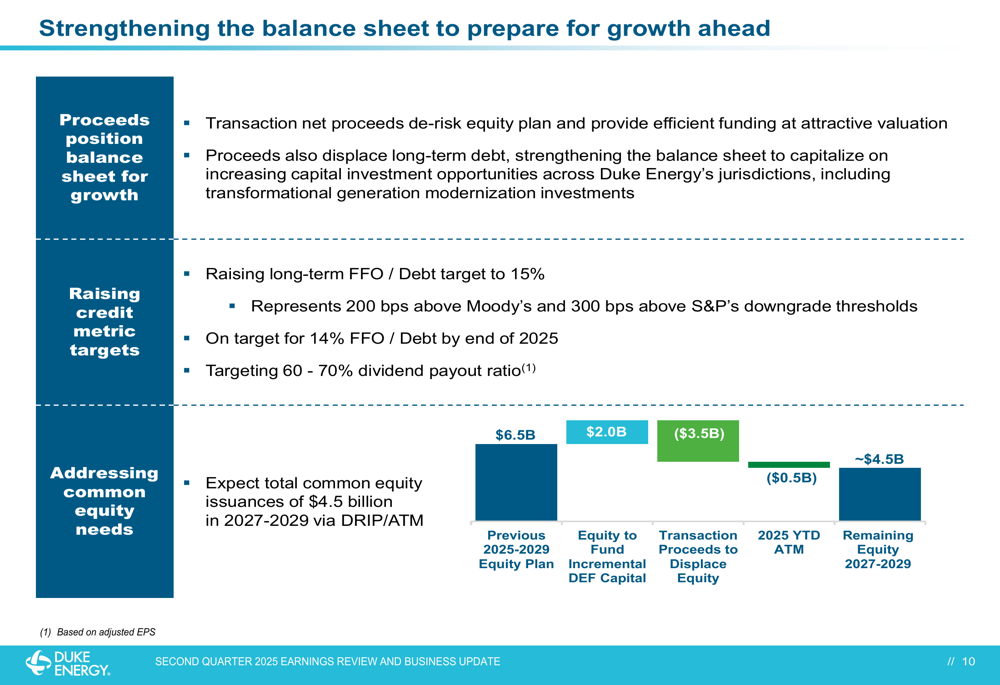

Duke Energy is strengthening its balance sheet to support its growth initiatives, raising its long-term funds from operations (FFO) to debt target to 15%, a 100 basis point increase from its previous target. The company has also revised its equity issuance plans, as shown in the following chart:

The strategic transactions have allowed Duke Energy to reduce its common equity needs, with expected total issuances of $4.5 billion in 2027-2029 via DRIP/ATM, down from the previous plan of $6.5 billion for 2025-2029.

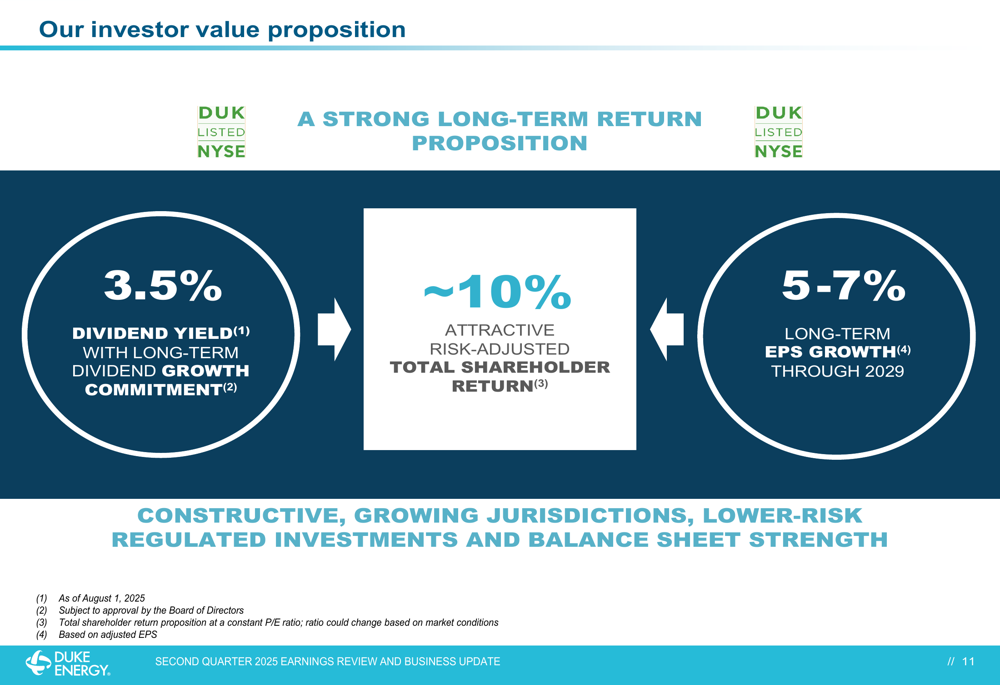

For investors, Duke Energy presents a compelling value proposition combining dividend yield, earnings growth, and total shareholder return:

The company offers a 3.5% dividend yield with a commitment to long-term dividend growth, 5-7% long-term EPS growth through 2029, and an attractive risk-adjusted total shareholder return of approximately 10%.

Regulatory Environment and Service Territory

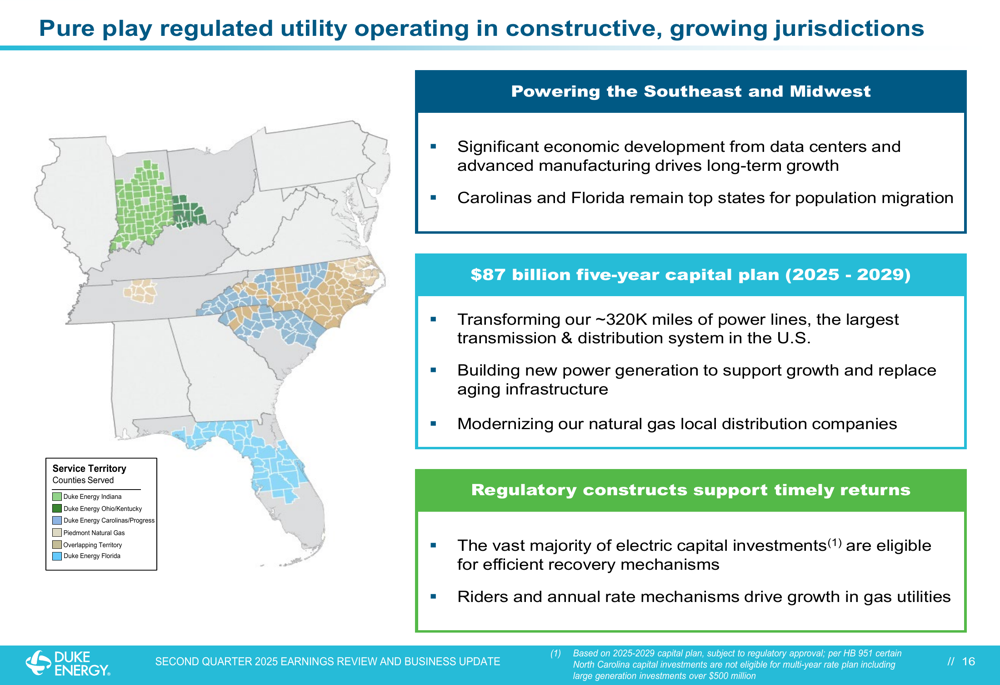

As a pure-play regulated utility, Duke Energy operates in constructive, growing jurisdictions primarily in the Southeast and Midwest. The company’s $87 billion five-year capital plan (2025-2029) focuses on transforming its extensive transmission and distribution system, building new power generation, and modernizing natural gas infrastructure.

The following map illustrates Duke Energy’s service territory, which benefits from significant economic development and population growth:

The company continues to benefit from constructive regulatory mechanisms, with the vast majority of electric capital investments eligible for efficient recovery through riders, rate cases with forecasted test years, and multi-year rate plans. This regulatory environment helps mitigate regulatory lag and supports timely returns on investments.

Duke Energy’s strategic positioning, robust capital plan, and strengthened balance sheet provide a solid foundation for delivering on its financial targets while meeting the growing energy needs of its service territories. With significant economic development opportunities on the horizon and strategic transactions enhancing financial flexibility, the company appears well-positioned to execute its long-term growth strategy.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.