Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

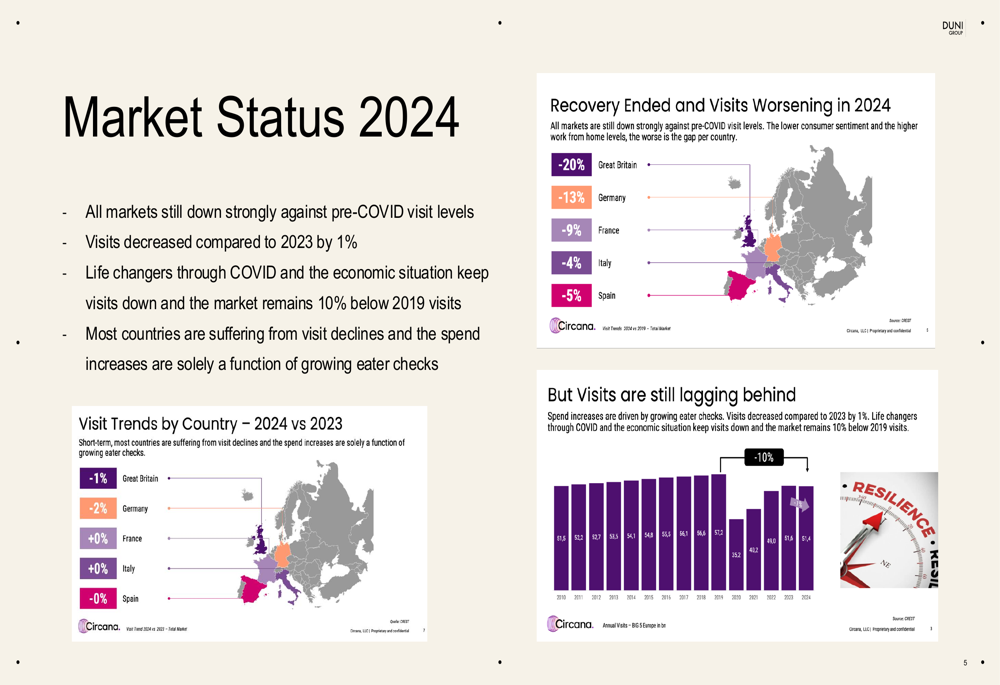

Duni AB (DUNI) presented its Q1 2025 interim results on April 25, 2025, highlighting growth achievements despite challenging market conditions across Europe. The company’s presentation emphasized that European restaurant markets remain significantly below pre-pandemic levels, with visits down 10% compared to 2019 and a further 1% decline compared to 2023.

The foodservice industry continues to face headwinds with consumer confidence hitting recent lows in March, as illustrated by market data presented by the company. Countries including Great Britain (-20%), Germany (-13%), and France (-9%) showed notable declines in restaurant visits compared to the previous year.

"All markets are still down strongly against pre-COVID visit levels," the company noted in its presentation, attributing this to lasting behavioral changes from the pandemic and ongoing economic pressures. Business sentiment continues to be affected by macroeconomic uncertainty, creating a challenging operating environment.

Quarterly Performance Highlights

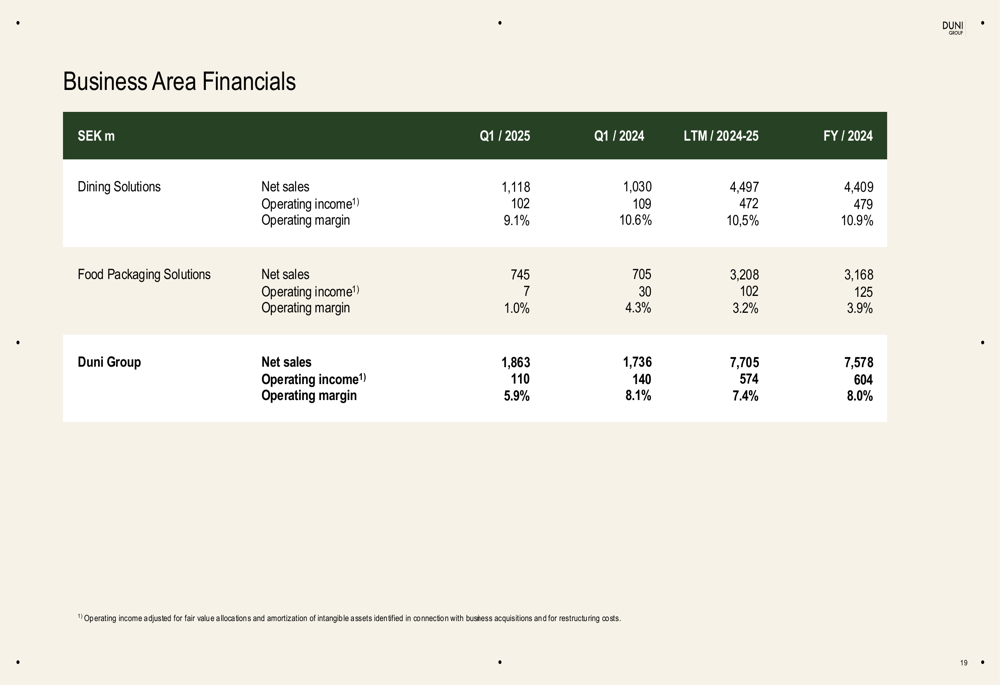

Duni reported net sales of SEK 1,863 million for Q1 2025, representing a 7.4% increase from SEK 1,736 million in the same period last year. However, operating income declined to SEK 110 million from SEK 140 million, resulting in an operating margin contraction to 5.9% from 8.1% in Q1 2024.

The company’s growth came from two sources: acquisitions contributed SEK 107 million to sales, while organic growth was modest at 1.5%. Duni emphasized that this growth occurred despite "slight negative volumes development to the restaurant sector in Europe."

A significant factor impacting profitability was currency effects. The strengthening of the Swedish krona against the euro by 5.6% resulted in negative revaluation effects of SEK 15 million, compared to positive effects of SEK 10 million in Q1 2024 – a SEK 25 million swing that substantially affected the bottom line.

Detailed Financial Analysis

Duni’s business is divided into two main segments, which showed divergent performance in the quarter:

The Dining Solutions segment, which focuses on napkins, table coverings, and related products, reported net sales of SEK 1,118 million (up from SEK 1,030 million) and operating income of SEK 102 million (down slightly from SEK 109 million). This segment maintained a relatively strong operating margin of 9.1%, though down from 10.6% in the prior year.

The Food Packaging (NYSE:PKG) Solutions segment, which provides sustainable packaging for food service, showed more significant margin pressure. While net sales increased to SEK 745 million from SEK 705 million, operating income plummeted to SEK 7 million from SEK 30 million, with operating margin falling sharply to 1.0% from 4.3%.

The company noted that the Dining Solutions segment benefited from strong performance outside Europe, where operating income increased by more than 25%. However, both segments faced challenges in Europe, with customers "placing lower priority on premium products" in Dining Solutions and volume declines in Food Packaging Solutions despite price increases aimed at offsetting inflation.

The company’s financial position remains solid, with the presentation highlighting a strong balance sheet despite recent acquisitions. Net debt stood at SEK 1,586 million as of March 2025, up from SEK 915 million in December 2024, reflecting acquisition activity.

Strategic Initiatives

Duni continues to emphasize its sustainability strategy, branded as "Our Decade of Action (WA:ACT) 2030," which focuses on three main pillars: becoming circular at scale, going net zero, and living the change.

The company reported progress on several sustainability initiatives, including the launch of napkins made from unbleached paper fiber, the establishment of a cross-functional "Circular Action Team," and a reduction in single-use plastics. Duni also highlighted its EcoVadis sustainability rating score of 79, placing it in the top 3% of companies assessed.

In addition to sustainability efforts, Duni announced it is initiating a transformation of its sales and marketing organization to improve efficiency and customer focus. This aligns with the company’s broader strategy for growth, which aims to position Duni as "A Trusted Sustainability Leader in our Industry by 2030."

Forward-Looking Statements

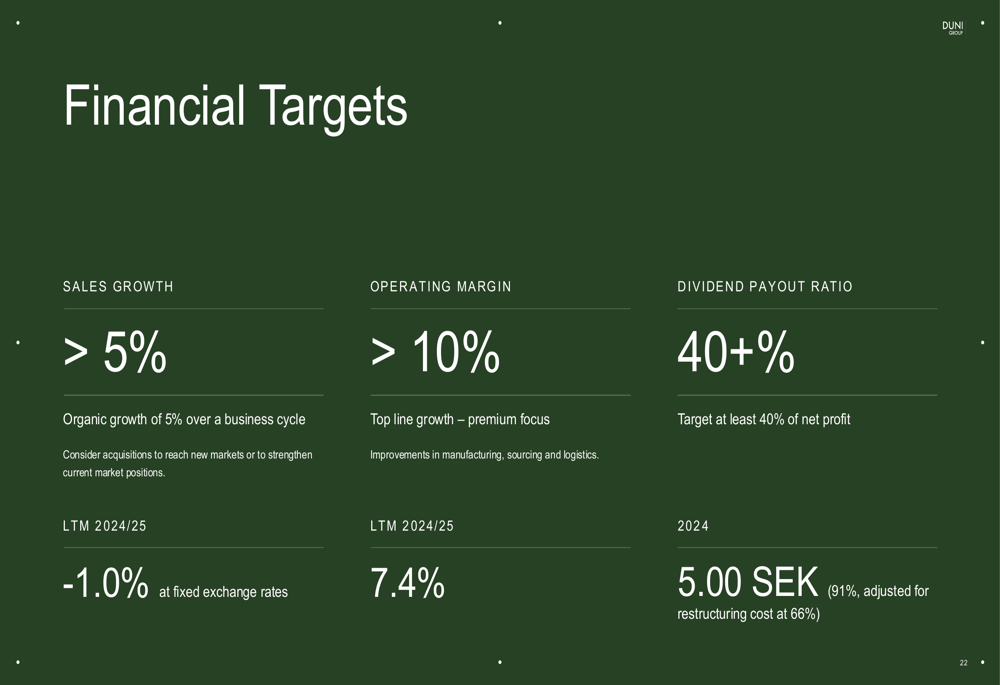

Looking ahead, Duni acknowledged the challenging market environment but maintained its long-term financial targets, which include organic sales growth exceeding 5%, an operating margin above 10%, and a dividend payout ratio of at least 40% of net profit.

The company’s current performance falls short of these targets, with last twelve months (LTM) sales growth at -1.0% and operating margin at 7.4%. Management indicated that the transformation of the sales and marketing organization is part of efforts to improve performance and achieve these targets.

The presentation summary suggests that while Duni expects continued headwinds in the European market, it remains focused on growth opportunities outside Europe and on leveraging its sustainability positioning to drive long-term value creation.

Duni AB closed at SEK 96.6 on April 24, 2025, with shares showing a minor decline of 0.1% ahead of the earnings presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.