IonQ CRO Alameddine Rima sells $4.6m in shares

Introduction & Market Context

Dustin Group AB (STO:DUST) presented its Q4 2024/25 results on October 8, 2025, revealing improved profitability despite modest sales growth in a challenging market environment. The company's stock, which has declined 84.65% year-to-date according to recent data, showed mixed investor reaction following the presentation, initially rising 11.43% in pre-market trading before settling at $2.03, down 2.96% from the previous close.

The IT solutions provider, which operates primarily across Nordic and Benelux regions, has implemented significant efficiency measures to counter market headwinds, with particular focus on improving segment margins and reducing operational costs.

Quarterly Performance Highlights

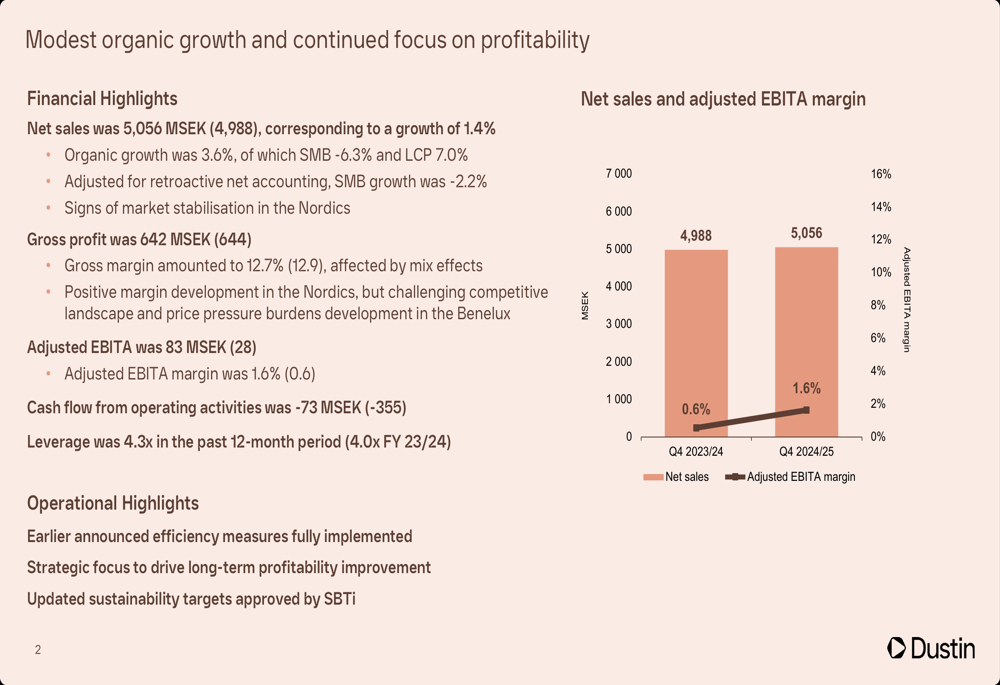

Dustin reported net sales of 5,056 MSEK for Q4 2024/25, representing a 1.4% increase from the previous year's 4,988 MSEK, with organic growth reaching 3.6%. More significantly, the company's adjusted EBITA rose substantially to 83 MSEK from 28 MSEK in the prior year, improving the adjusted EBITA margin to 1.6% from 0.6%.

As shown in the following chart of quarterly financial performance:

Despite the improved EBITA, gross profit slightly decreased to 642 MSEK from 644 MSEK, with gross margin contracting to 12.7% from 12.9%. This aligns with concerns about weak gross profit margins highlighted in recent financial analyses of the company.

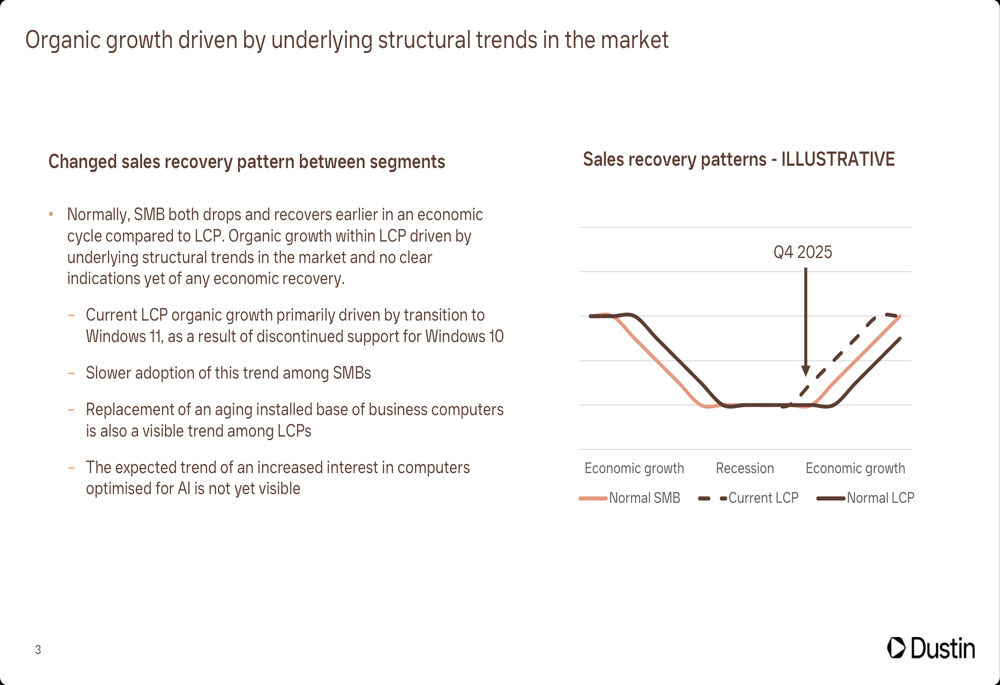

The quarter's results reflect divergent recovery patterns between business segments, with the company noting that SMB (Small and Medium-sized Businesses) typically experiences faster drops and recoveries compared to LCP (Large Corporate and Public) customers:

Segment Analysis

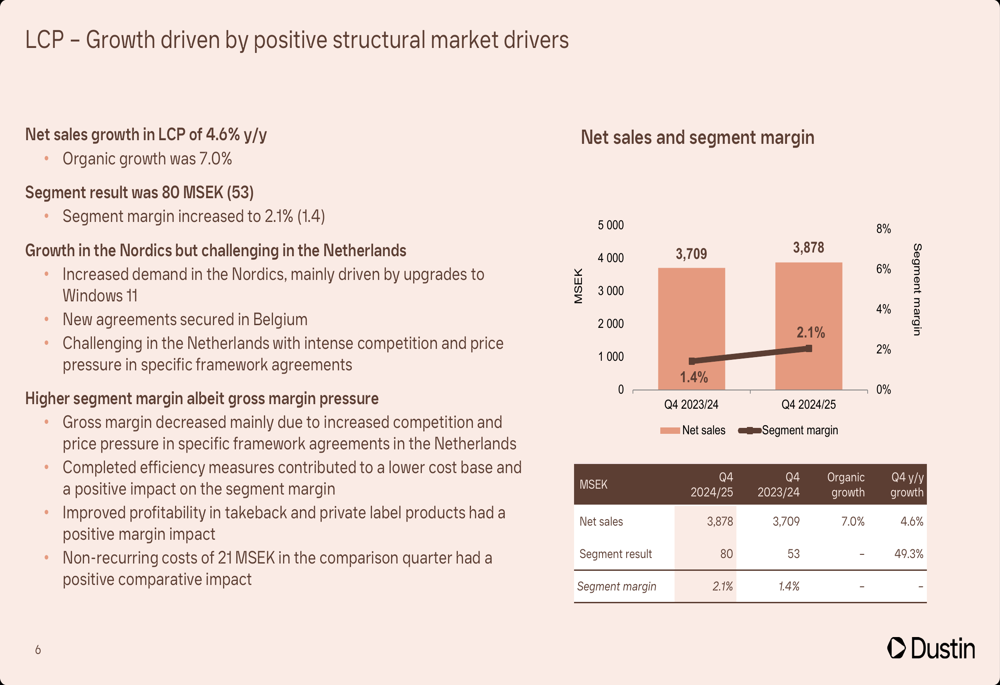

The LCP segment demonstrated strong performance with organic growth of 7.0% year-over-year, driven largely by the ongoing Windows 11 transition. Net sales increased to 3,878 MSEK from 3,709 MSEK, while segment result improved to 80 MSEK from 53 MSEK, expanding the segment margin to 2.1% from 1.4%.

The following chart illustrates LCP's sales growth and margin improvement:

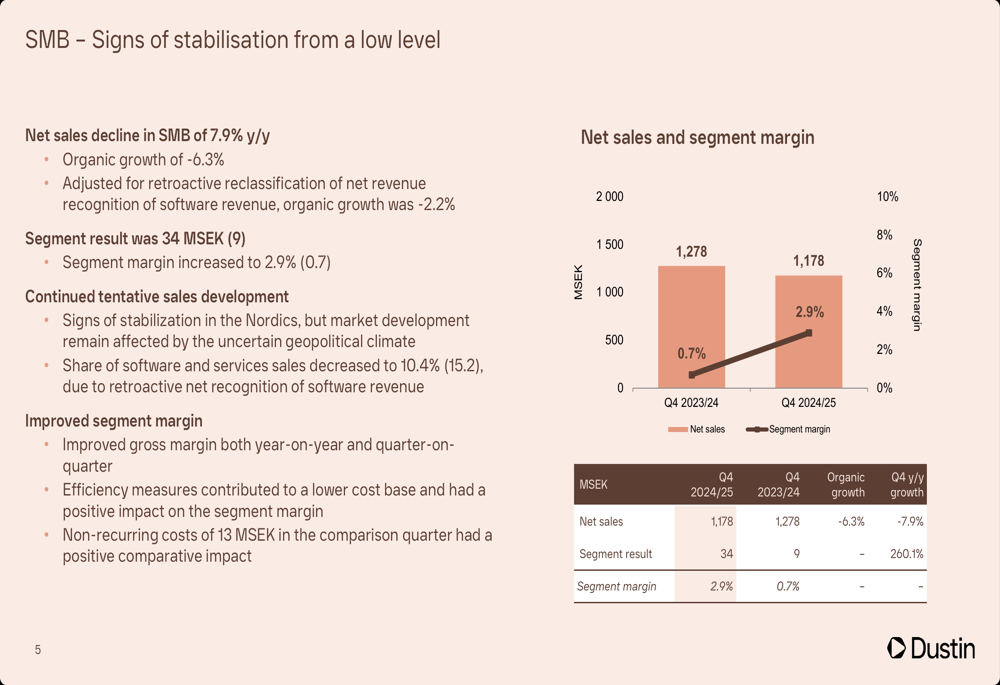

Meanwhile, the SMB segment showed signs of stabilization despite a 6.3% organic sales decline. Net sales decreased to 1,178 MSEK from 1,278 MSEK, but segment result improved dramatically to 34 MSEK from 9 MSEK, with segment margin rising to 2.9% from 0.7%.

The SMB performance metrics are visualized in this chart:

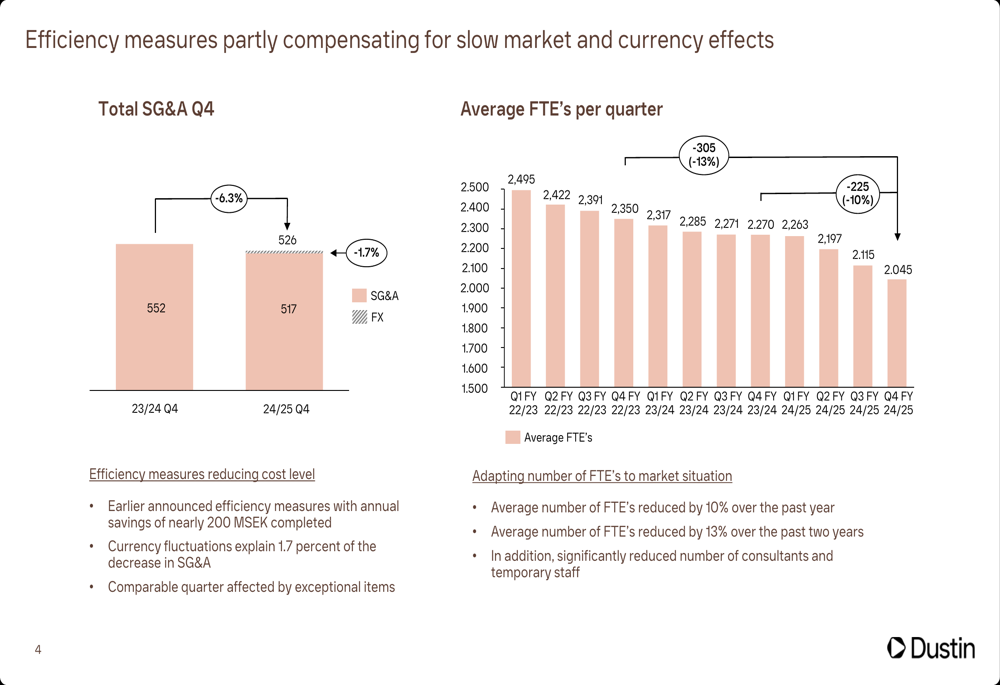

Efficiency Initiatives

A key driver of Dustin's improved profitability has been its focus on operational efficiency. The company reported a 6.3% decrease in SG&A expenses for Q4, with average full-time equivalent employees (FTEs) reduced by 10% year-over-year and 13% over two years.

The following chart demonstrates the consistent reduction in headcount:

These efficiency measures align with Dustin's strategic focus on strengthening profitability through organizational restructuring, process improvements, and harmonization of its European B2B customer offering.

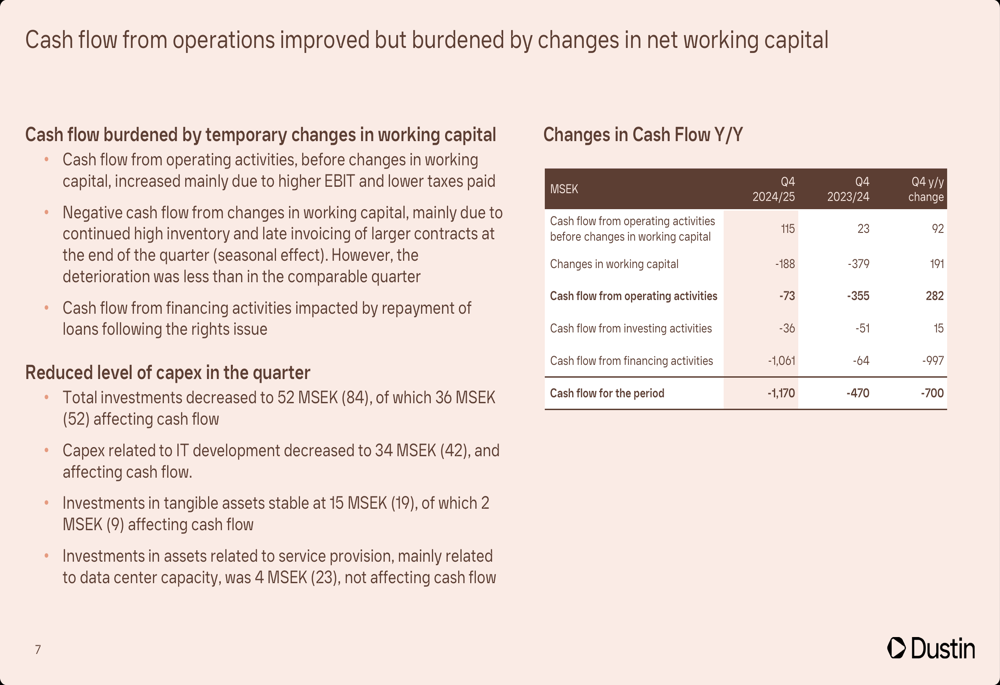

Cash Flow and Working Capital Challenges

Despite operational improvements, Dustin continues to face cash flow challenges. Cash flow from operating activities was -73 MSEK for the quarter, though this represents a significant improvement from -355 MSEK in the prior year. The negative cash flow was primarily attributed to temporary changes in working capital.

Net working capital increased to 477 MSEK from 175 MSEK, with inventory rising by 260 MSEK to 1,086 MSEK. This working capital expansion remains an area of concern, as noted in the earnings call where improving working capital was highlighted as a priority for Q1.

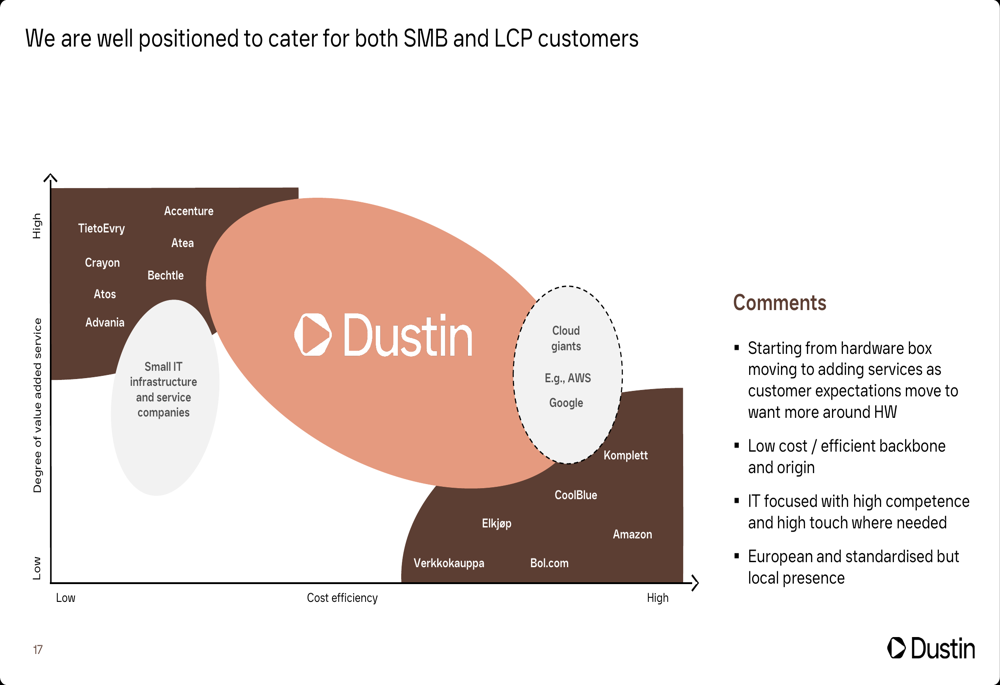

Strategic Focus and Outlook

Dustin maintains its medium-term financial targets, including segment margin goals of >6.5% for SMB and >4.5% for LCP by FY25/26. The company's strategic positioning in the market balances value-added services with cost efficiency:

The company has also strengthened its sustainability commitments by joining the Science Based Targets initiative (SBTi) in 2024, with targets including a 50% reduction in Scope 1 and 2 emissions and a 51.6% reduction in CO2e intensity in Scope 3 by 2029/30.

Looking ahead, Dustin anticipates market recovery driven by the Windows 11 transition, AI PCs, and aging IT equipment. However, investors should note the significant gap between the company's improved operational metrics and its financial performance, as evidenced by the 68.15% EPS miss reported in recent earnings.

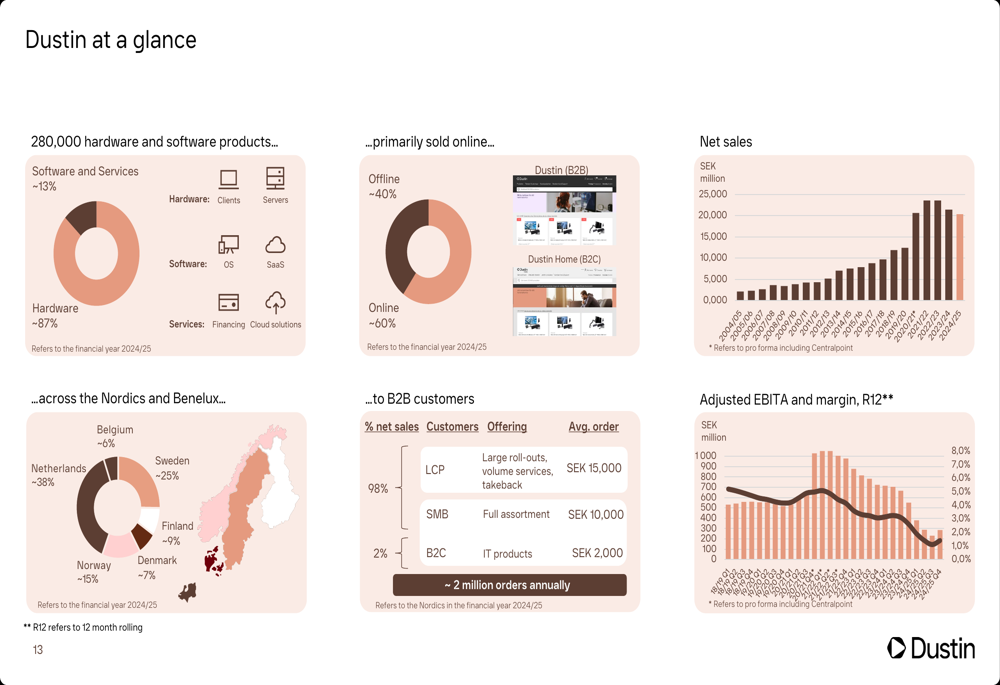

The company's comprehensive business overview provides context for understanding its market position and future growth potential:

While Dustin's Q4 presentation highlights operational improvements and strategic initiatives, the company's negative cash flow, working capital challenges, and significant year-to-date stock decline indicate ongoing hurdles that will require continued focus on efficiency and margin improvement to overcome.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.