Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Introduction & Market Context

Dustin Group AB (DUST) reported its fourth quarter results for fiscal year 2024/25, showing modest sales growth but significantly improved profitability driven by extensive cost-cutting measures. The IT solutions provider, operating primarily across the Nordics and Benelux regions, continues to navigate a challenging market environment with divergent performance across its business segments.

The company's stock has struggled in recent trading, closing at 1.76 SEK on November 18, 2025, down 2.78% for the day and sitting near its 52-week low of 1.55 SEK – far below its 52-week high of 6.90 SEK. This performance reflects ongoing investor concerns despite operational improvements highlighted in the company's presentation.

Quarterly Performance Highlights

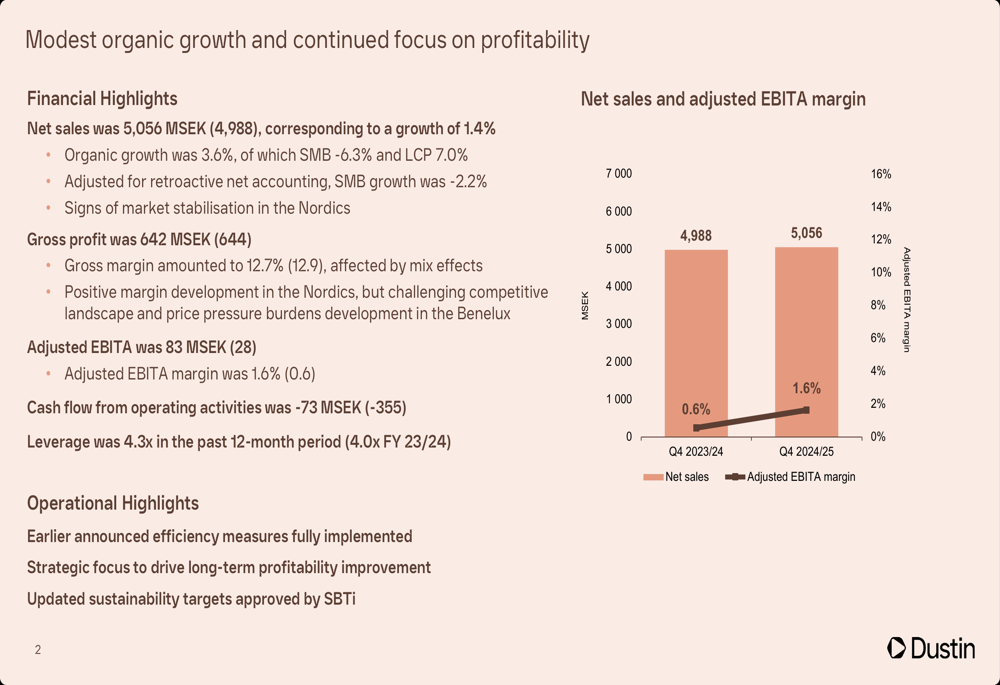

Dustin reported net sales of 5,056 MSEK for Q4 2024/25, representing a modest 1.4% increase compared to 4,988 MSEK in the same period last year. Organic growth was more robust at 3.6%, indicating that currency effects partially offset underlying business growth.

More notably, the company's adjusted EBITA surged to 83 MSEK from 28 MSEK in the prior-year quarter, with the adjusted EBITA margin expanding to 1.6% from 0.6%. This significant profitability improvement came despite a slight decline in gross profit to 642 MSEK from 644 MSEK.

As shown in the following chart of quarterly financial performance:

Cash flow from operating activities improved substantially to -73 MSEK, compared to -355 MSEK in the prior year period, though it remained negative. The company's leverage ratio increased to 4.3x, up from 4.0x at the end of fiscal year 2023/24, indicating higher relative debt levels.

Segment Analysis

Dustin's performance varied significantly between its two main business segments, reflecting different market dynamics and recovery patterns.

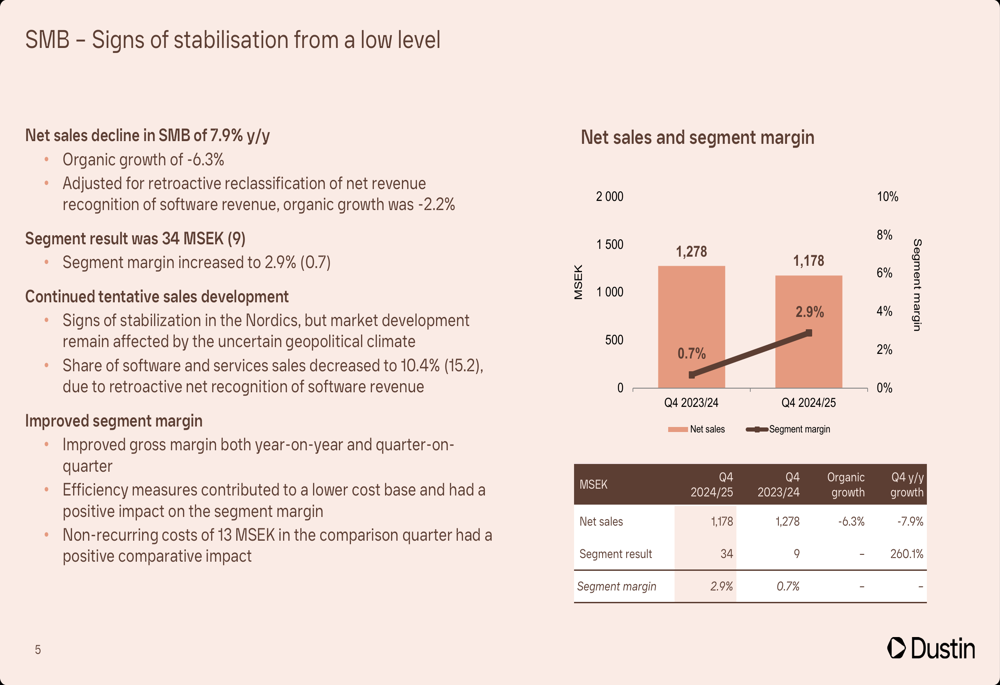

The Small and Medium Business (SMB) segment showed signs of stabilization, though from a low level. Net sales declined by 7.9% year-over-year to 1,178 MSEK, with organic growth at -6.3%. However, when adjusted for retroactive reclassification of net revenue, organic growth was -2.2%. Despite the sales decline, segment profitability improved dramatically, with segment result increasing to 34 MSEK from 9 MSEK and segment margin expanding to 2.9% from 0.7%.

The following chart illustrates the SMB segment's performance:

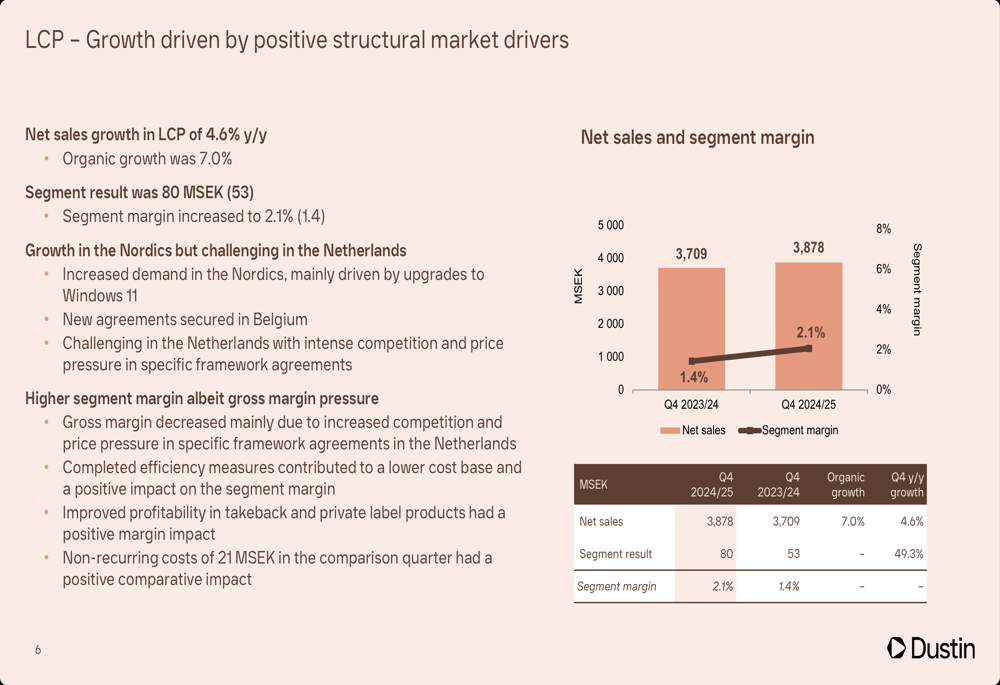

In contrast, the Large Corporate and Public (LCP) segment demonstrated solid growth, with net sales increasing by 4.6% year-over-year to 3,878 MSEK and organic growth of 7.0%. Segment result improved to 80 MSEK from 53 MSEK, with segment margin expanding to 2.1% from 1.4%. This growth was primarily driven by upgrades to Windows 11 in the Nordic region.

The following chart details the LCP segment's performance:

Dustin's presentation highlighted different recovery patterns between segments, noting that SMB typically drops and recovers faster than LCP during economic cycles. The current market dynamics show LCP growth driven by the transition to Windows 11 and computer replacements, while SMB remains in an earlier stage of recovery.

Cost Efficiency Initiatives

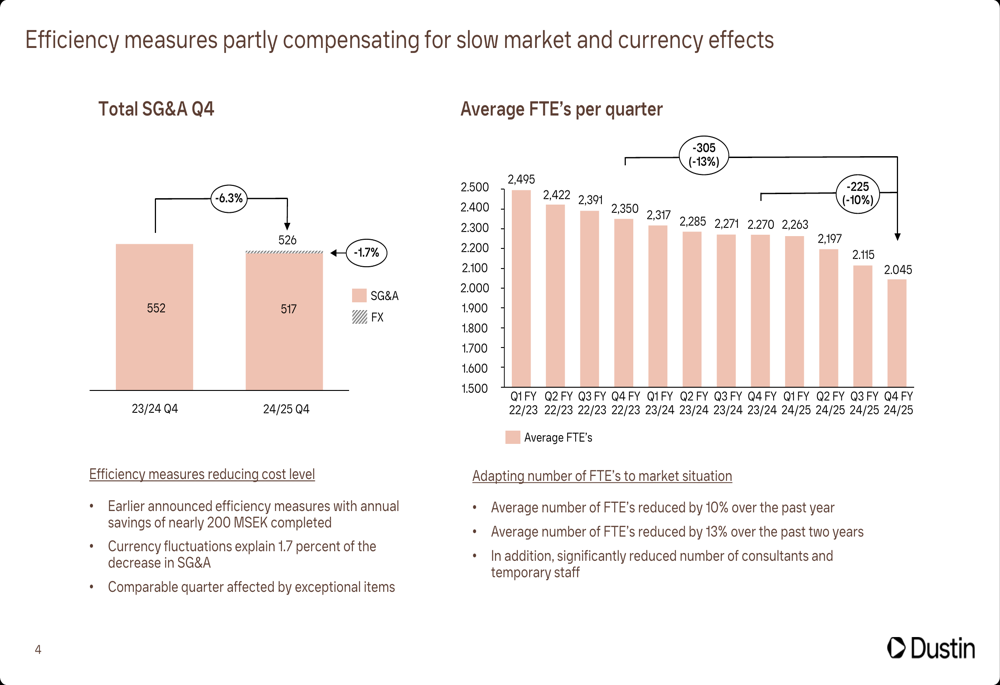

A key driver of Dustin's improved profitability was its extensive efficiency measures, which have compensated for slow market conditions and negative currency effects. Total SG&A expenses in Q4 decreased by 6.3% year-over-year, from 552 MSEK to 517 MSEK, with currency fluctuations accounting for -1.7% of this change.

The company has significantly reduced its workforce, with average full-time employees (FTEs) decreasing by 13% from 2,422 in Q1 FY 22/23 to 2,045 in Q4 FY 24/25. These efficiency measures have resulted in annual savings of nearly 200 MSEK.

The following chart illustrates the company's headcount reduction and cost-cutting progress:

Cash flow analysis reveals that while operations improved, changes in working capital continued to be a burden. Cash flow from operating activities, before changes in working capital, increased year-over-year, but was offset by negative cash flow from changes in working capital.

Strategic Outlook & Sustainability

Dustin emphasized its strategic focus on improving profitability through several key initiatives, including implementing a new organizational structure, focusing on efficiency, transforming with a strategic focus on business customers, creating a harmonized European B2B customer offering, and pursuing automation and operational improvements.

In 2024, Dustin joined the Science Based Targets initiative (SBTi) and received approval for updated sustainability targets. The company has established climate, circularity, and social impact targets for 2029/30 and 2049/50, aligning its business strategy with broader environmental goals.

Looking ahead, Dustin anticipates market recovery driven by Windows exchanges, AI PCs, and the renewal of aging IT equipment. The company is targeting a 6.5% margin in the SMB segment and a 4.5% margin in the LCP segment, though achieving these targets may prove challenging in the current competitive environment, particularly in the Netherlands where price competition remains intense.

Despite operational improvements, investors appear cautious about Dustin's near-term prospects, as reflected in the stock's proximity to its 52-week low. The company's ability to maintain its efficiency gains while driving sales growth across both business segments will be crucial for restoring investor confidence in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.