Stifel maintains Buy rating on Contineum Therapeutics stock despite MS trial failure

Introduction & Market Context

DXC Technology (NYSE:DXC) presented its first quarter fiscal year 2026 earnings on July 31, 2025, revealing a company in transition that continues to face revenue challenges while showing improvements in bookings and financial discipline. The IT services provider reported results that generally met or exceeded guidance, though organic revenue decline persists.

The presentation comes after DXC’s stock experienced significant pressure following its Q4 FY25 earnings report, when shares dropped 13.52% despite beating expectations. The company’s current stock price of $13.73 remains near its 52-week low of $13.44, reflecting ongoing investor concerns about its ability to reverse an eight-year revenue decline trend.

Quarterly Performance Highlights

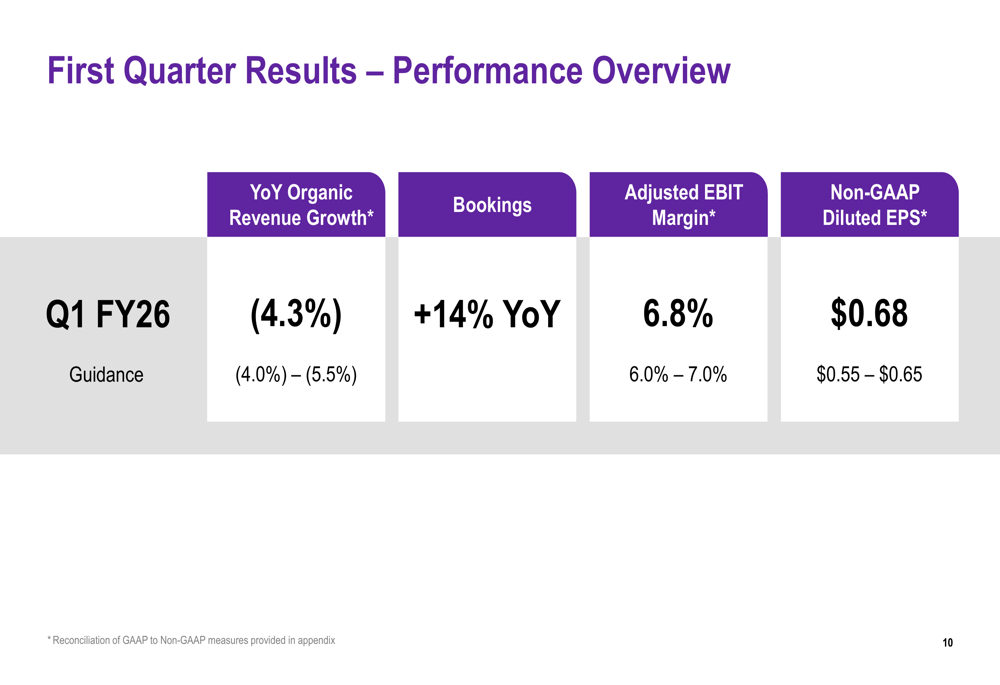

DXC Technology reported mixed results for Q1 FY26, with performance generally within or exceeding guidance ranges. The company posted an organic revenue decline of 4.3%, which was within the guided range of 4.0% to 5.5% decline. However, the company showed strength in other key metrics.

As shown in the following performance overview chart:

Non-GAAP diluted EPS reached $0.68, exceeding the guidance range of $0.55 to $0.65, while adjusted EBIT margin came in at 6.8%, near the high end of the 6.0% to 7.0% guidance. Most notably, bookings increased by 14% year-over-year, marking the third consecutive quarter of double-digit growth.

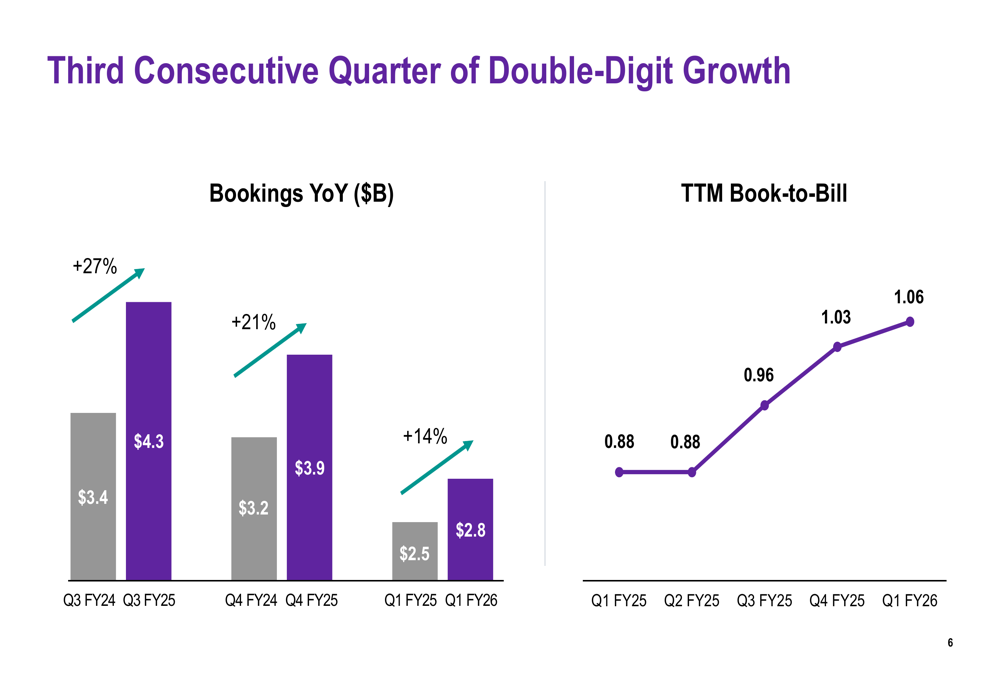

The company’s book-to-bill ratio continues to improve, reaching 1.06 in Q1 FY26, up from 0.88 in the same quarter last year. This positive trend is illustrated in the following chart:

This improving book-to-bill ratio above 1.0 suggests that DXC is securing more new business than it is recognizing in current revenue, potentially indicating future revenue stabilization if the company can effectively convert these bookings.

Segment Performance Analysis

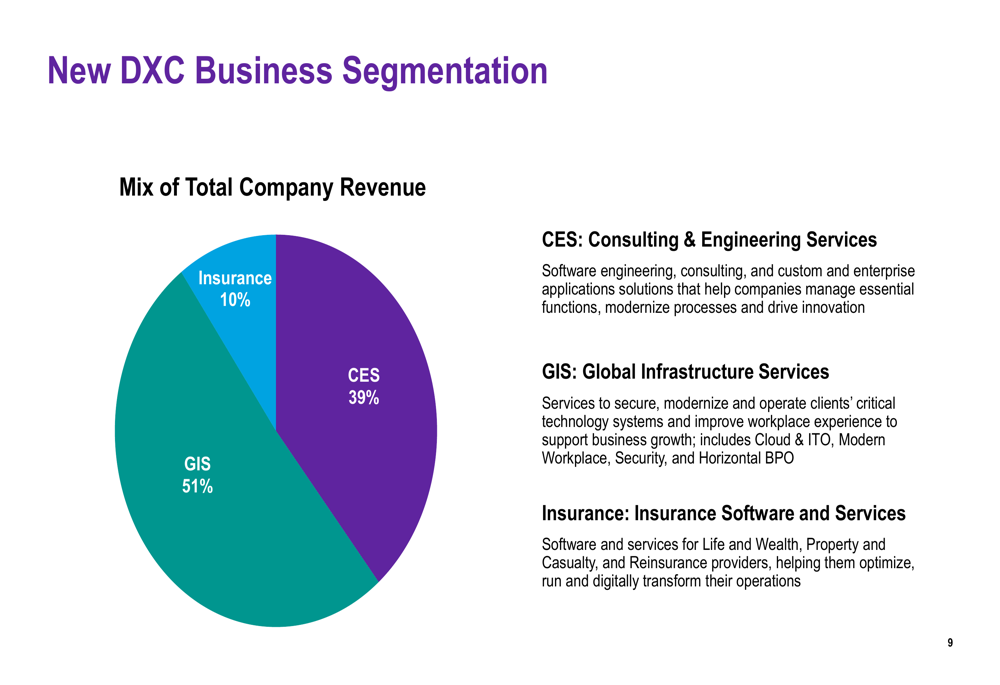

DXC Technology has implemented a new business segmentation structure, dividing operations into three main segments: Global Infrastructure Services (GIS), Consulting & Engineering Services (CES), and Insurance Software (ETR:SOWGn) and Services.

The following chart illustrates the revenue distribution across these segments:

GIS represents the largest portion at 51% of total company revenue, followed by CES at 39% and Insurance at 10%. This segmentation aims to better align with market opportunities and provide clearer visibility into performance.

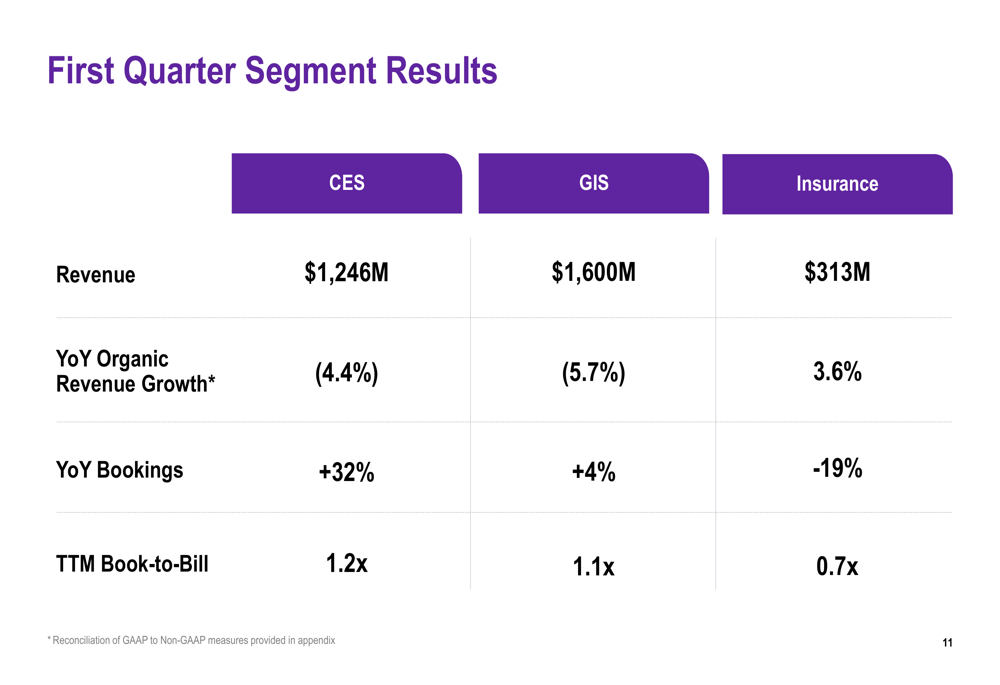

Segment performance varied significantly in Q1 FY26, as shown in the detailed breakdown:

The Insurance segment was the only one to deliver positive organic revenue growth at 3.6%, while CES declined by 4.4% and GIS by 5.7%. However, CES showed the strongest bookings growth at 32% year-over-year, compared to 4% for GIS and a 19% decline for Insurance. The trailing twelve-month book-to-bill ratios for CES (1.2x) and GIS (1.1x) are encouraging, while Insurance lags at 0.7x.

Strategic Initiatives and Leadership

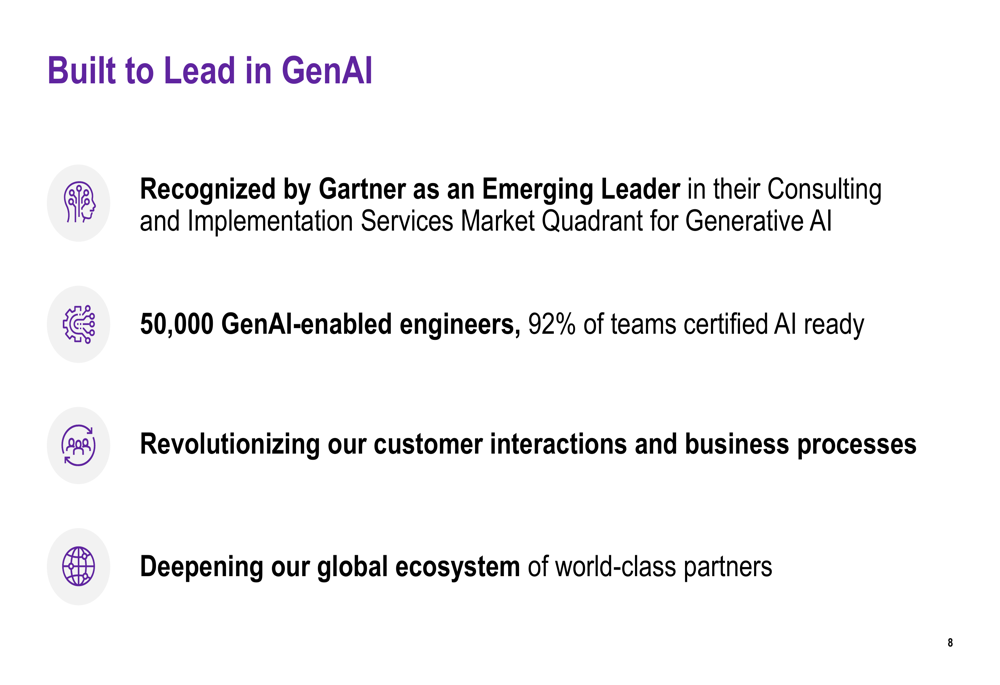

DXC Technology continues to emphasize its strategic focus on artificial intelligence, particularly generative AI capabilities. The company highlighted its recognition by Gartner (NYSE:IT) as an Emerging Leader in Consulting and Implementation Services for Generative AI.

As illustrated in the following strategic overview:

The company has built a substantial AI workforce with 50,000 GenAI-enabled engineers and claims that 92% of its teams are certified AI ready. This focus on AI capabilities appears to be central to DXC’s strategy for reversing its revenue decline and capturing new market opportunities.

To strengthen its leadership team, DXC has brought on Ramnath Venkataraman as President of Consulting & Engineering Services. Venkataraman brings approximately 30 years of global experience from Accenture (NYSE:ACN), with expertise in launching and growing businesses internationally, particularly in cutting-edge technologies like GenAI.

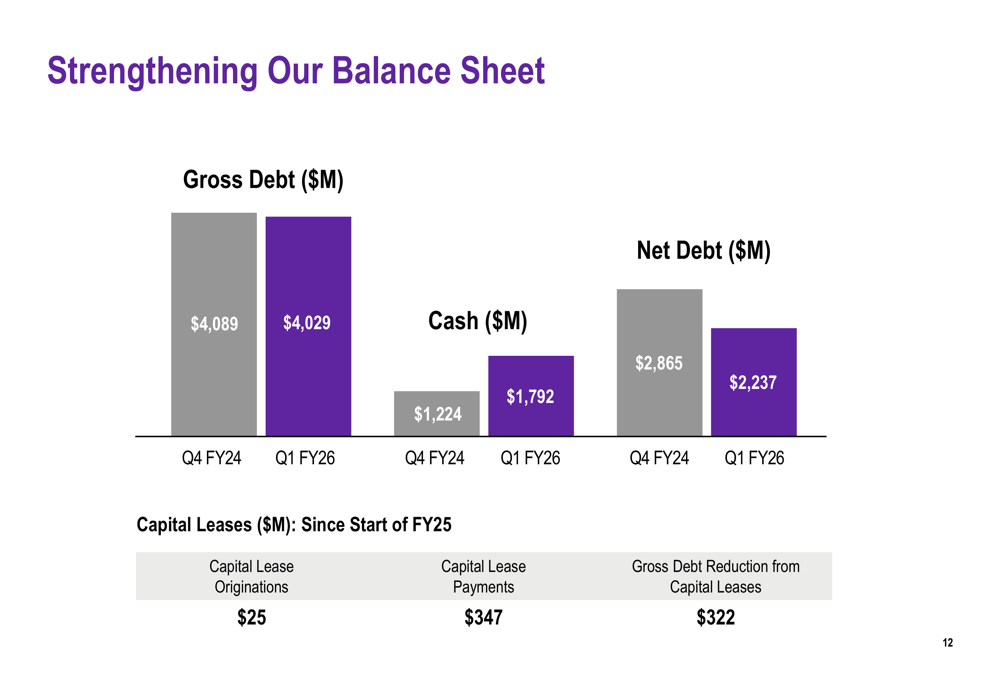

Balance Sheet Improvements

A significant bright spot in DXC’s presentation was the strengthening of its balance sheet, with notable improvements in both debt reduction and cash position:

Gross debt decreased from $4,089 million in Q4 FY24 to $4,029 million in Q1 FY26, while cash increased substantially from $1,224 million to $1,792 million. As a result, net debt declined by approximately $628 million to $2,237 million. The company has also made progress in reducing capital lease obligations, with payments of $347 million since the start of FY25 compared to originations of just $25 million.

Free cash flow for Q1 FY26 was $97 million, a significant improvement from negative $75 million in the same quarter two years ago. This enhanced financial flexibility may provide DXC with more options for investments in growth initiatives or shareholder returns.

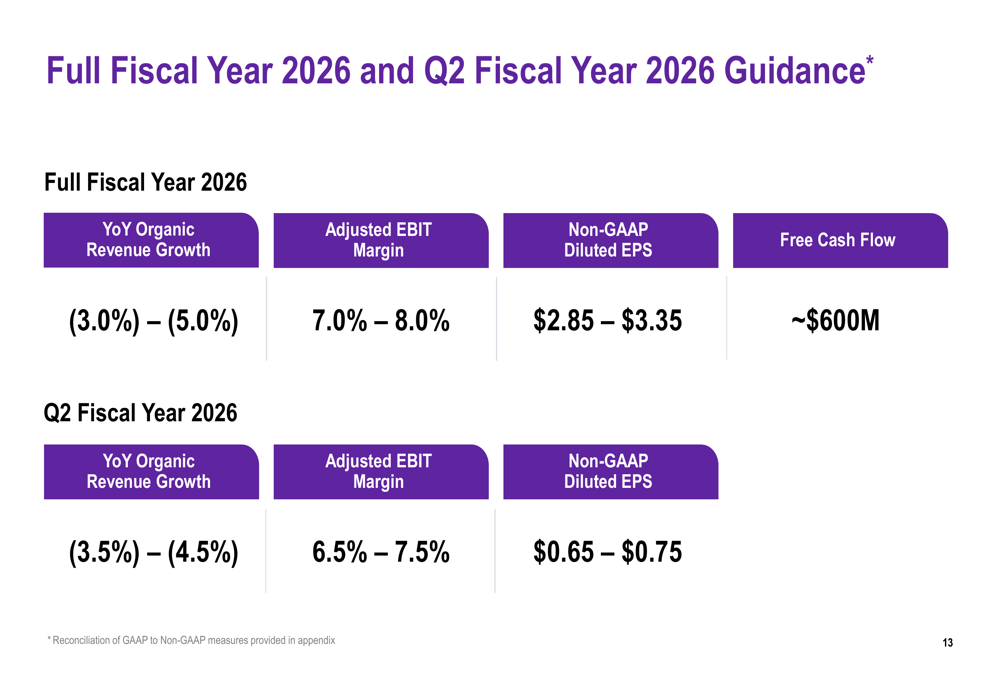

Forward Guidance

DXC Technology provided guidance for both the full fiscal year 2026 and the upcoming second quarter:

For the full year, the company expects organic revenue growth between -3.0% and -5.0%, suggesting a potential improvement from the -4.3% reported in Q1. Adjusted EBIT margin is projected to be between 7.0% and 8.0%, while non-GAAP diluted EPS is expected to range from $2.85 to $3.35. Free cash flow is anticipated to be approximately $600 million.

For Q2 FY26, DXC forecasts organic revenue growth between -3.5% and -4.5%, adjusted EBIT margin between 6.5% and 7.5%, and non-GAAP diluted EPS between $0.65 and $0.75.

Conclusion

DXC Technology’s Q1 FY26 presentation reveals a company making progress in several areas while still grappling with its core challenge of revenue decline. The positive trends in bookings growth, book-to-bill ratio, and balance sheet metrics provide some encouragement, but the persistent organic revenue decline across most segments remains a significant concern.

The company’s strategic focus on GenAI capabilities and its new business segmentation structure demonstrate efforts to position for future growth. However, as evidenced by the stock’s proximity to its 52-week low, investors appear to remain skeptical about DXC’s ability to translate these initiatives into sustainable revenue growth.

The coming quarters will be critical for DXC to demonstrate that its improving bookings can successfully convert to revenue stabilization and eventual growth, while maintaining the financial discipline that has strengthened its balance sheet.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.