JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

Dye & Durham Ltd (TSX:DND) presented its third-quarter fiscal 2025 results on May 13, 2025, showcasing stable revenue despite macroeconomic challenges affecting the legal technology sector. The company’s stock responded positively, closing at $9.47, up 4.33% following the presentation, as investors appeared to welcome the company’s strategic initiatives and focus on contracted revenue growth.

The legal technology provider, which operates across Canada, the UK, Australia, and South Africa, continues to navigate a challenging environment while implementing a multi-year strategic plan centered on customer retention, product transformation, and portfolio optimization.

Quarterly Performance Highlights

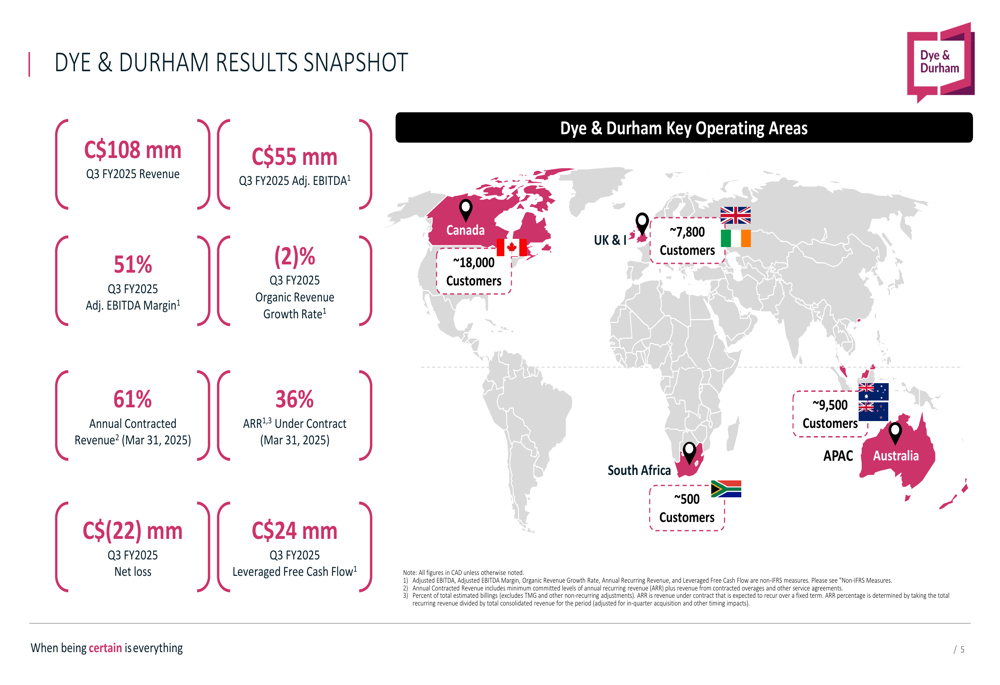

Dye & Durham reported revenue of C$108 million for Q3 FY2025, representing a modest 1% year-over-year increase. While organic revenue declined by 2%, the company maintained a strong adjusted EBITDA of C$55 million with a 51% margin, within its target range of 50-55%.

As shown in the following snapshot of the company’s Q3 FY2025 results:

The company reported a net loss of C$(22) million for the quarter, though its leveraged free cash flow rebounded to C$24 million. This cash flow recovery aligns with management’s focus on improving financial flexibility and reducing debt.

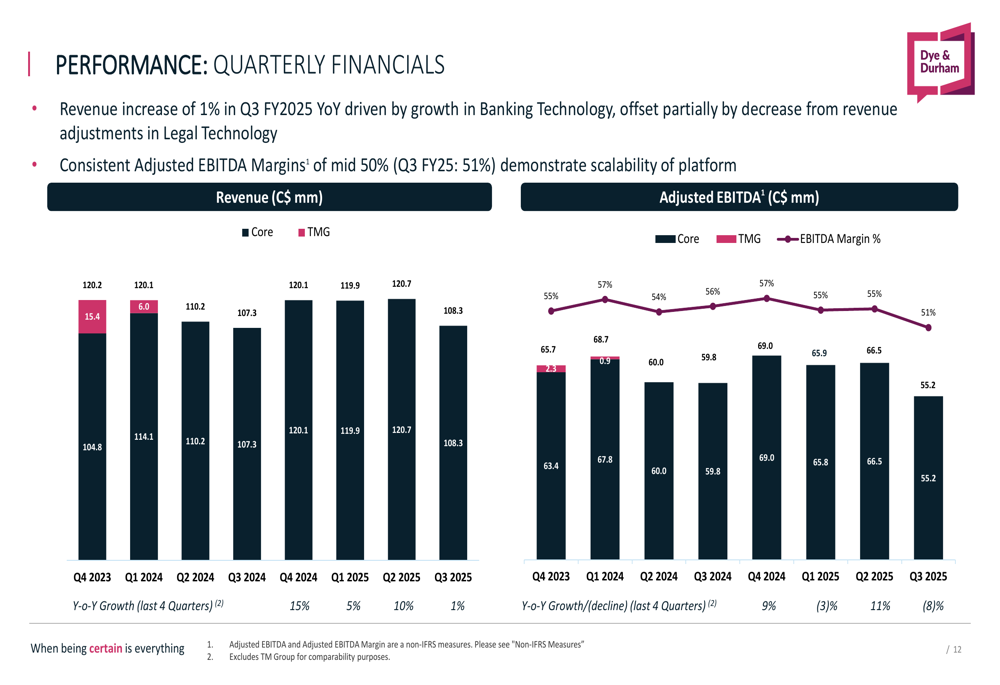

The quarterly financial trends demonstrate the company’s ability to maintain consistent EBITDA margins despite revenue fluctuations:

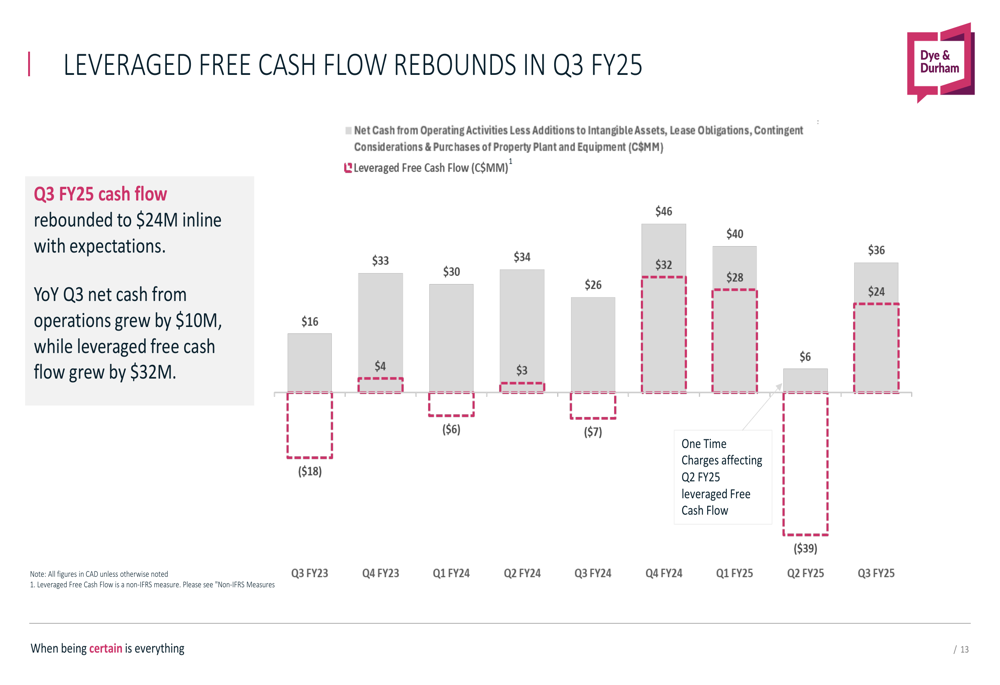

A significant bright spot in the quarterly results was the recovery in leveraged free cash flow, which rebounded to C$24 million in Q3 FY2025:

Strategic Initiatives

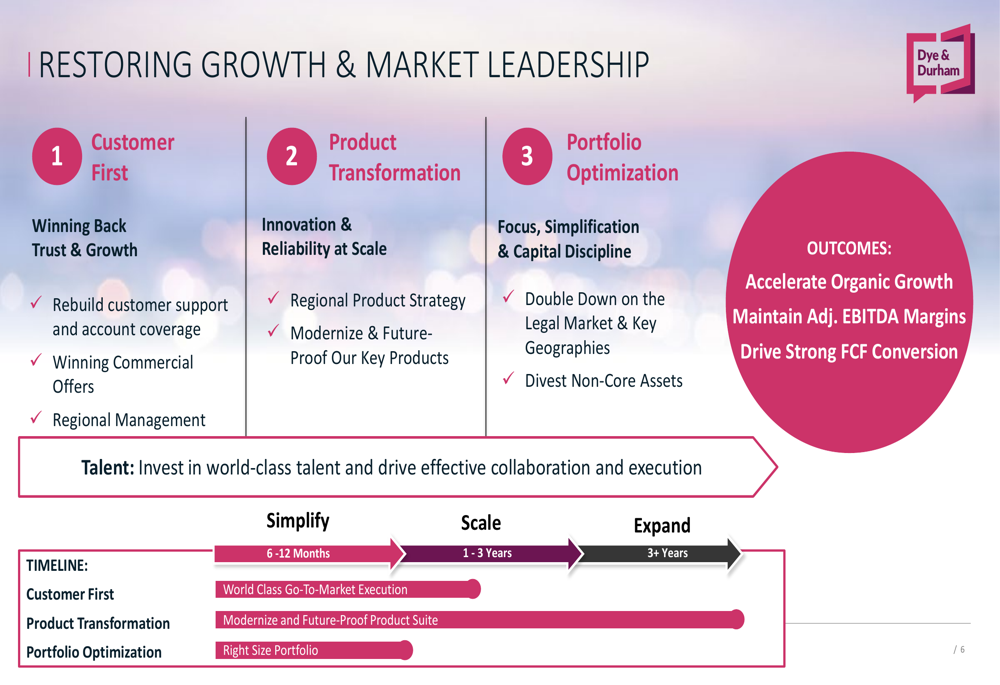

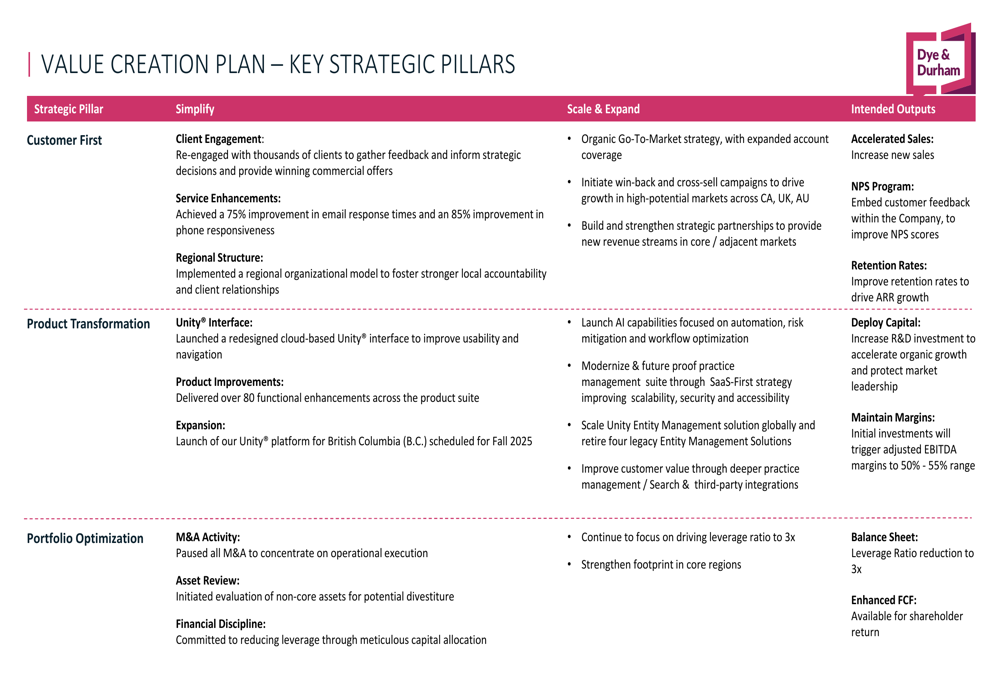

Dye & Durham outlined a comprehensive strategic plan focused on three key pillars: Customer First, Product Transformation, and Portfolio Optimization. This strategy aims to restore growth and market leadership over a multi-year horizon.

The company’s strategic roadmap is designed to address immediate challenges while positioning for long-term growth:

The value creation plan provides more detailed initiatives under each strategic pillar, with specific intended outcomes:

These strategic initiatives reflect Dye & Durham’s response to market challenges and its commitment to rebuilding customer trust. Interim CEO Sid Singh emphasized this focus during the earnings call, stating, "We are actively rebuilding trust and credibility with our customers."

Revenue Model and Growth Drivers

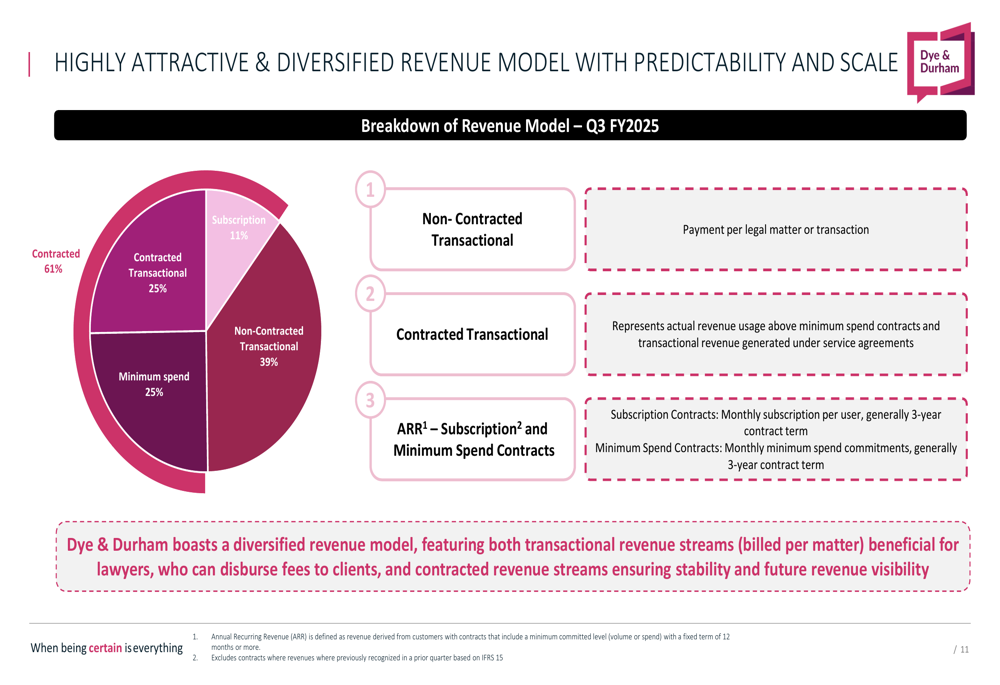

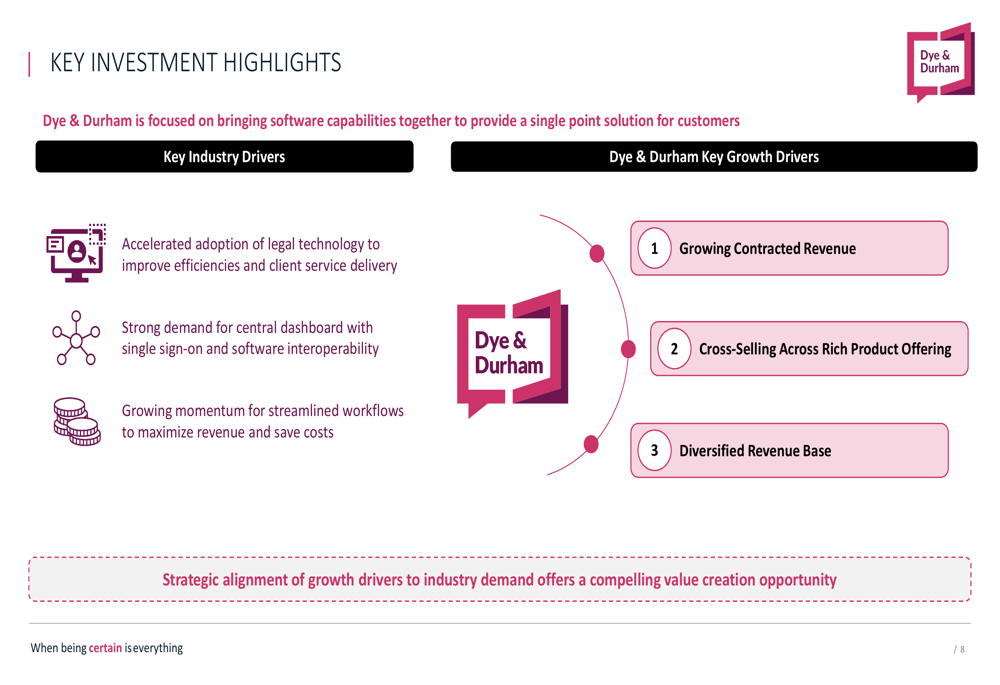

A key strength highlighted in the presentation is Dye & Durham’s diversified revenue model, with 61% of revenue coming from contracted sources. This provides stability and predictability in an uncertain market environment.

The breakdown of the company’s revenue model demonstrates this diversification:

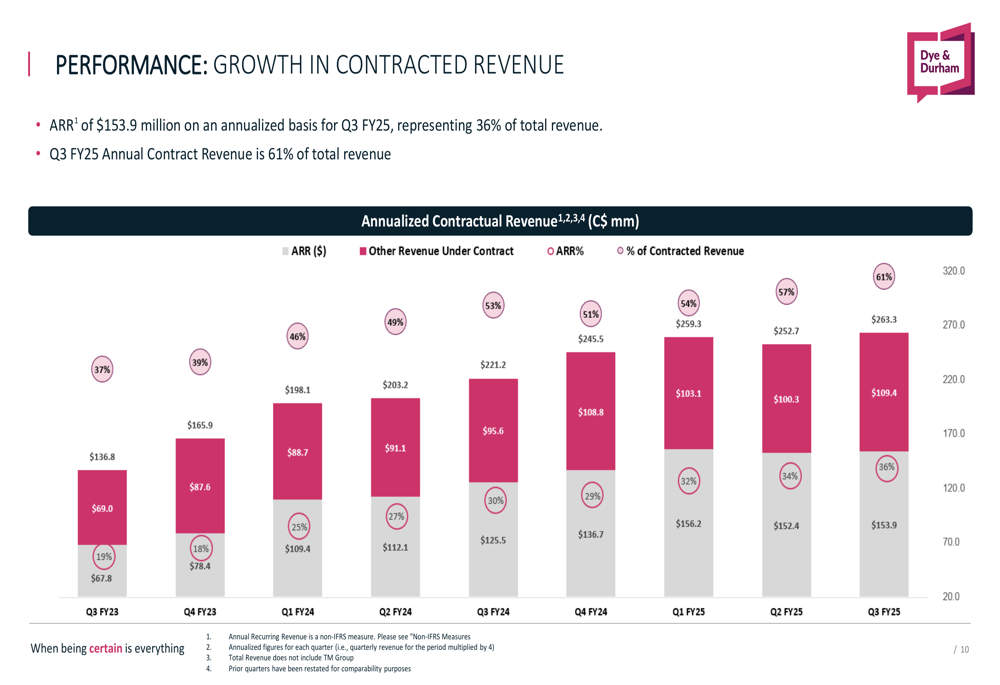

The company has made significant progress in growing its annual recurring revenue (ARR), which reached C$153.9 million in Q3 FY2025, representing 36% of total revenue. This marks substantial growth from C$69.0 million in Q3 FY2023:

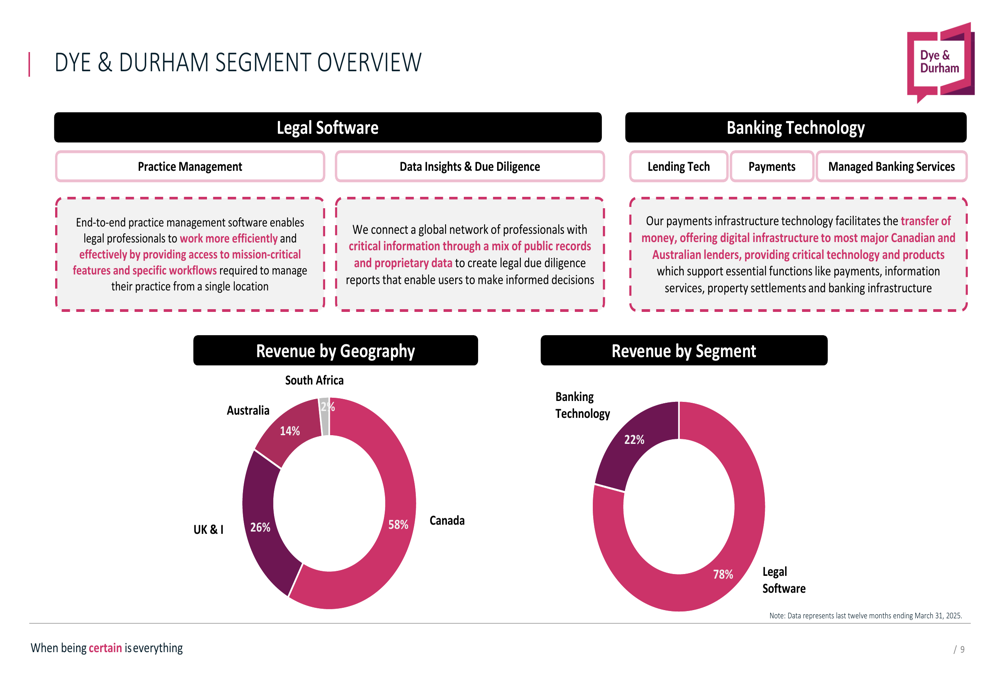

Dye & Durham’s business is primarily focused on legal software, which accounts for 78% of revenue, with banking technology contributing the remaining 22%. Geographically, Canada remains the largest market at 58% of revenue, followed by the UK and Ireland at 26%, and Australia at 14%.

The company highlighted several key investment attributes that support its growth strategy, emphasizing its position as a provider of integrated software solutions for legal professionals:

Management Outlook and Forward Guidance

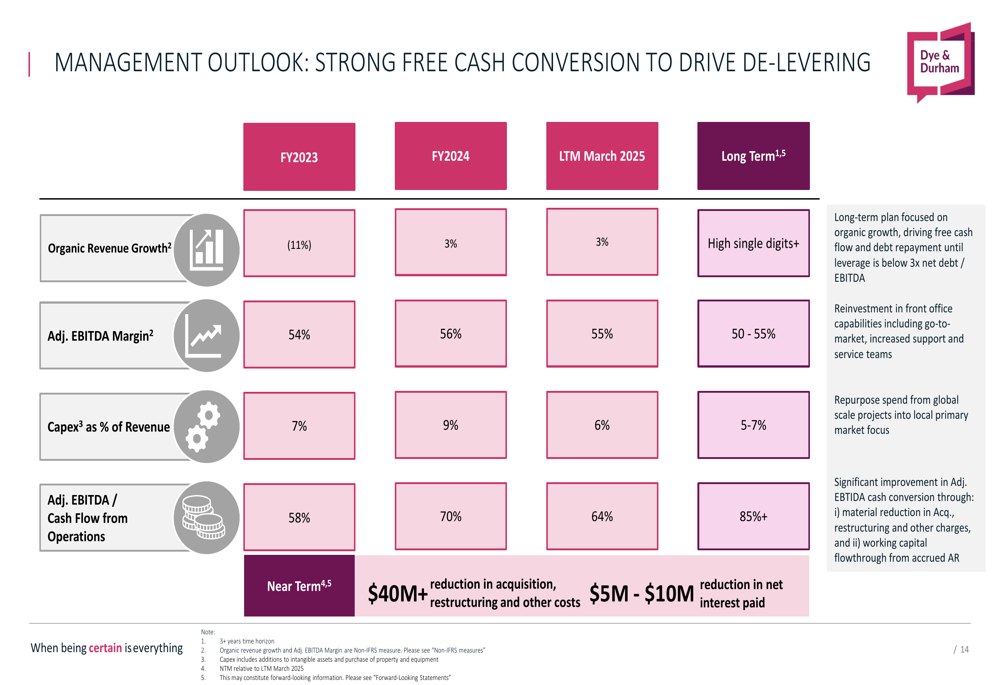

Looking ahead, Dye & Durham’s management has outlined clear targets for future performance, with a strong emphasis on free cash flow conversion to drive debt reduction. The company aims to achieve high single-digit organic revenue growth in the long term while maintaining adjusted EBITDA margins of 50-55%.

The detailed outlook provides specific metrics across different time horizons:

In the near term, management expects to reduce acquisition, restructuring, and other costs by more than C$40 million, along with a C$5-10 million reduction in net interest paid. These initiatives align with the company’s focus on improving financial flexibility and strengthening its balance sheet.

CFO Frank Deliso reinforced this outlook during the earnings call, stating, "We are targeting organic growth in the high single digit plus range," underscoring the company’s growth ambitions despite current challenges.

The company faces several ongoing risks, including macroeconomic uncertainty affecting real estate activity, potential impacts of interest rate fluctuations on refinancing, and an ongoing Competition Bureau investigation. With net debt of C$1.35 billion, the focus on de-levering and improving cash flow conversion remains critical to the company’s financial strategy.

As Dye & Durham continues to implement its strategic initiatives, investors will be watching closely for signs of improved organic growth and progress on debt reduction, while the company works to maintain its strong EBITDA margins and expand its contracted revenue base.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.