Gold prices steady ahead of Fed decision; weekly weakness noted

Dynatrace Inc (NYSE:DT) released its Q4 and fiscal year 2025 results on May 14, 2025, showcasing solid financial performance with robust profitability metrics despite signs of moderating growth. The company’s stock rose 2.43% in premarket trading to $51.77, indicating positive investor reception to the results.

Quarterly Performance Highlights

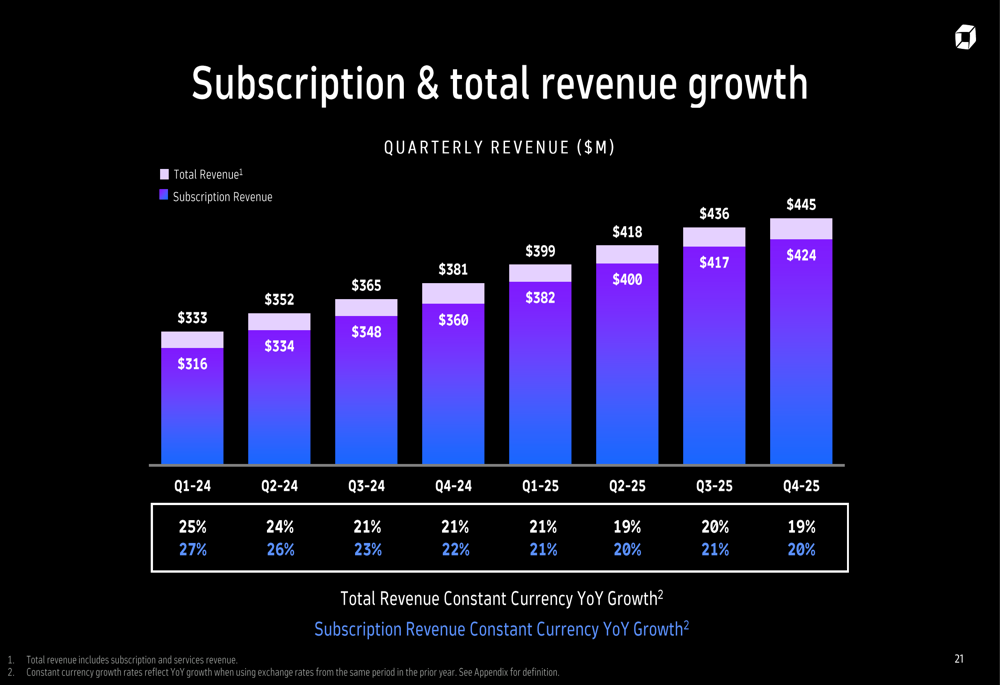

Dynatrace reported Q4 2025 total revenue of $445 million, representing 19% year-over-year growth in constant currency. Subscription revenue, which constitutes 95% of the company’s revenue mix, reached $424 million, growing 20% year-over-year in constant currency.

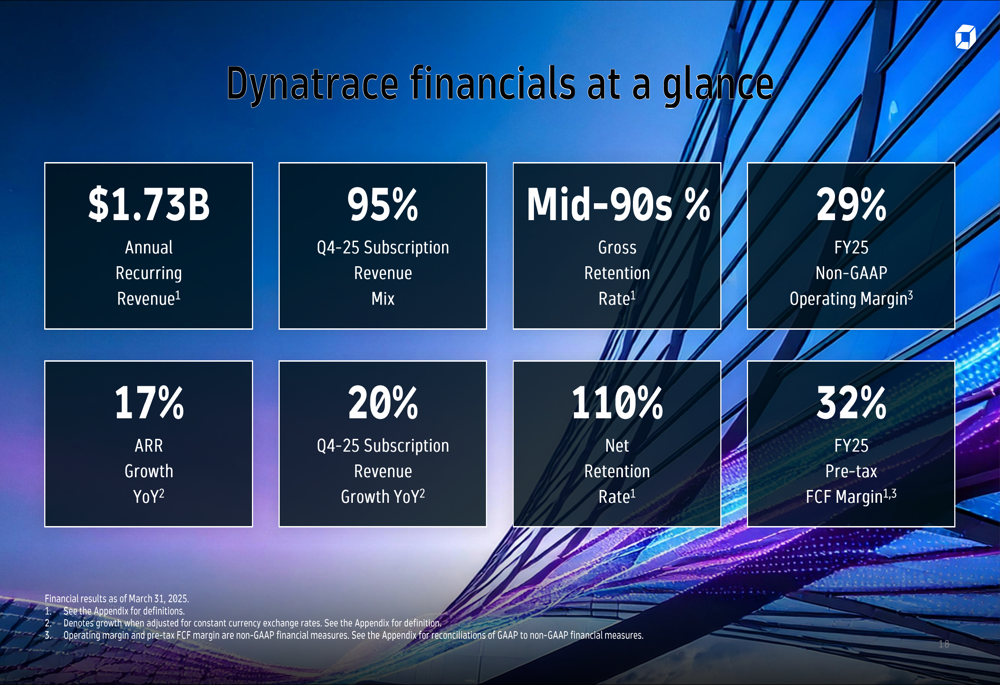

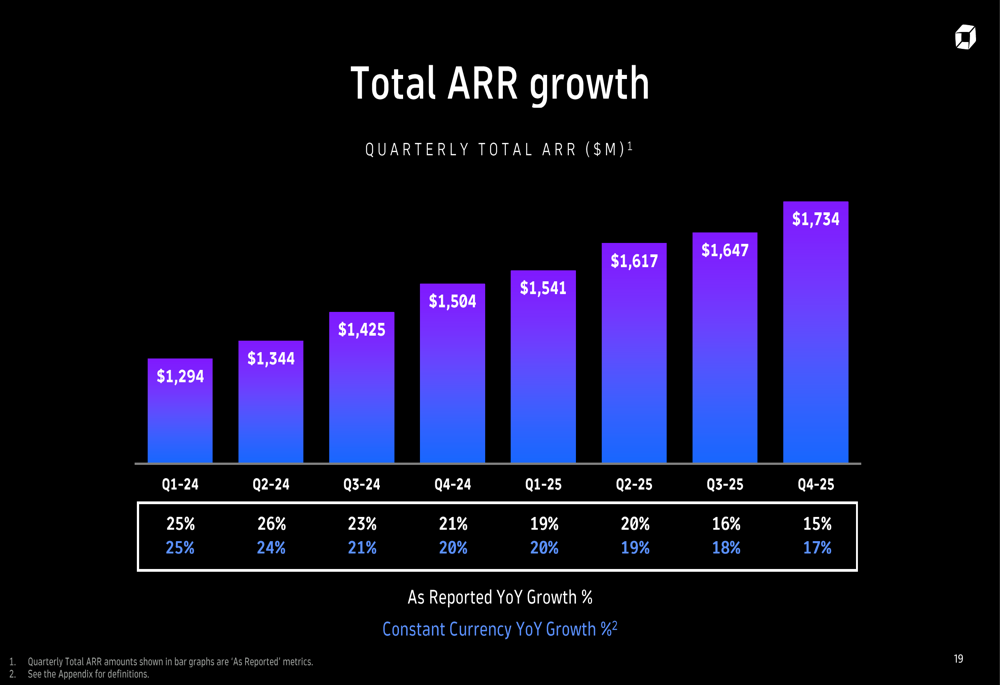

Annual Recurring Revenue (ARR) reached $1.73 billion, growing 17% year-over-year in constant currency. The company maintained strong customer retention metrics with a net retention rate of 110% and gross retention rate in the mid-90s percentage range.

As shown in the following financial overview, Dynatrace continues to demonstrate a balanced approach to growth and profitability:

While ARR growth has been gradually moderating over recent quarters, the company has maintained consistent revenue expansion:

Subscription revenue continues to be the primary growth driver for Dynatrace, highlighting the company’s successful transition to a subscription-based business model:

Strategic Initiatives

Dynatrace positions itself as "the leading AI-powered observability platform," focusing on helping enterprises transform complexity into business assets. The company’s core value proposition centers on enabling organizations to understand their business operations better through comprehensive observability.

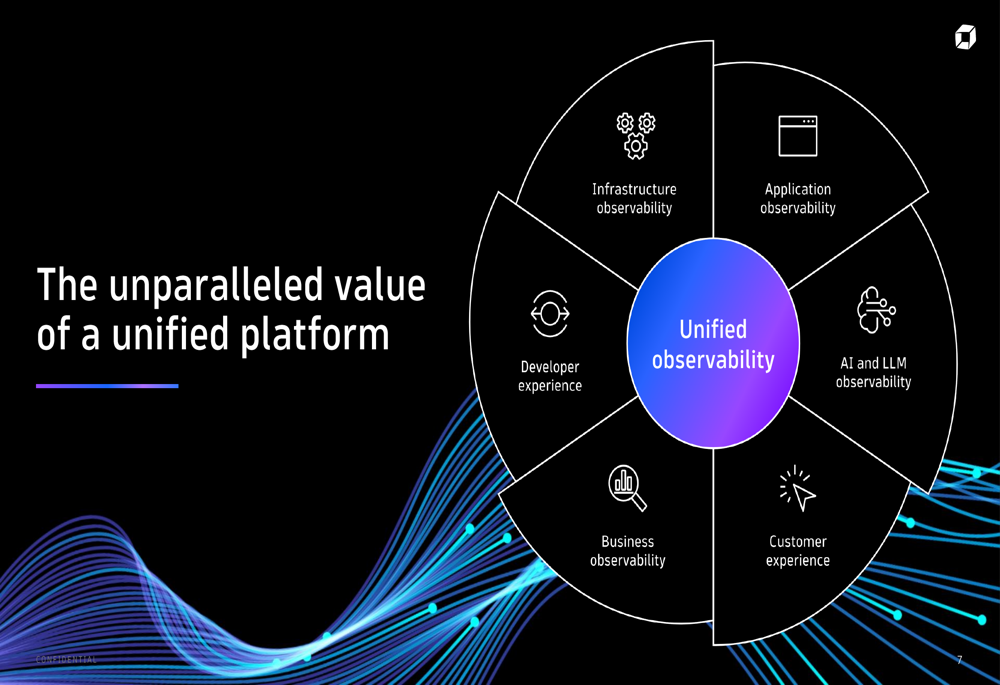

The company’s unified platform approach integrates various observability domains, providing a comprehensive solution for enterprise customers:

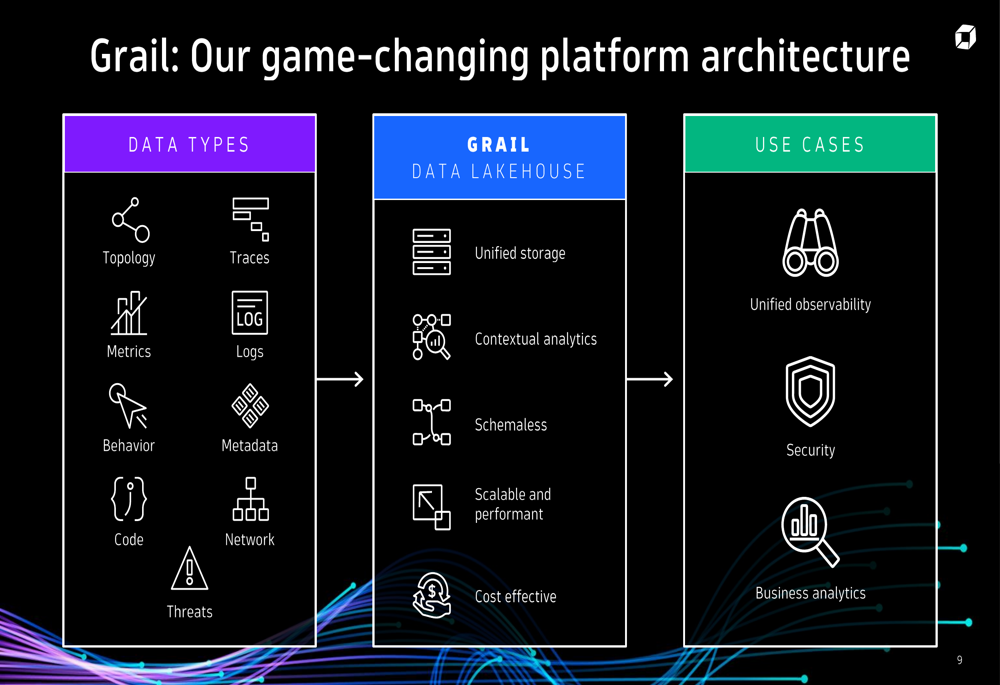

A key technical differentiator for Dynatrace is its Grail data lakehouse architecture, which provides unified storage and contextual analytics capabilities:

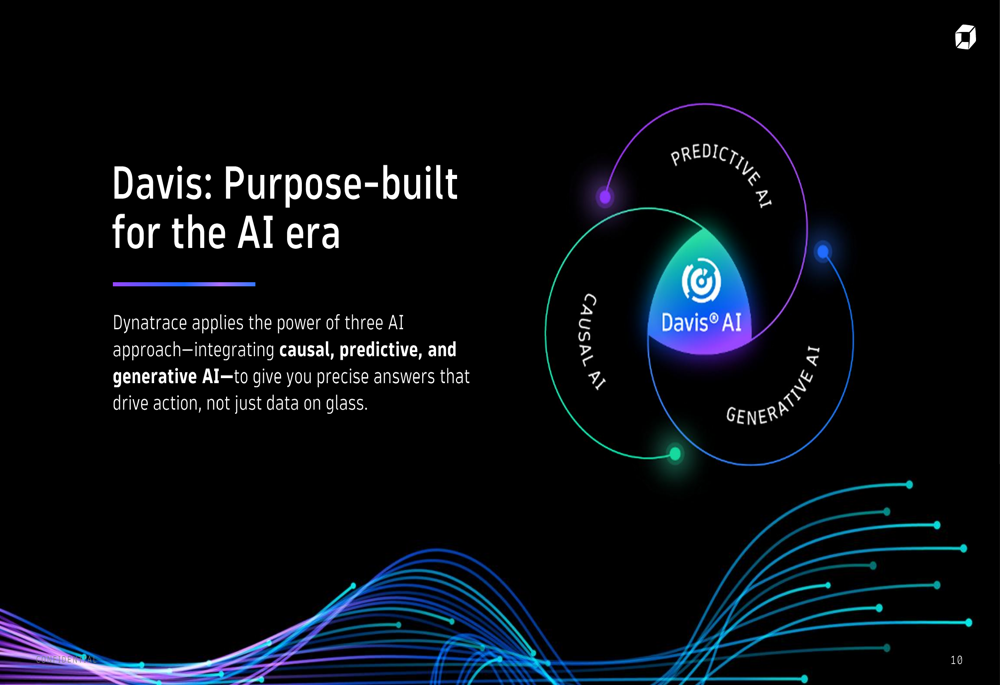

Complementing this infrastructure is Davis AI, Dynatrace’s artificial intelligence engine that integrates causal, predictive, and generative AI capabilities:

Detailed Financial Analysis

Dynatrace demonstrated strong profitability metrics in FY2025, with a non-GAAP operating margin of 29%, up from 28% in FY2024. The company generated $431 million in free cash flow for FY2025, representing a margin of 25%. On a pre-tax basis, free cash flow margin reached an impressive 32%.

The company’s gross margins remain best-in-class, with non-GAAP subscription gross margin at 87% for FY2025. This high margin profile reflects the scalability of Dynatrace’s platform and its efficient operating model.

Operating expenses as a percentage of revenue have been well-managed, with non-GAAP R&D, S&M, and G&A expenses at 16%, 31%, and 8% of revenue respectively for FY2025. This disciplined approach to spending has enabled the company to maintain strong profitability while continuing to invest in innovation.

Competitive Industry Position

Dynatrace operates in a large and growing market, with the total addressable market (TAM) for observability and security estimated at $65 billion, comprising $51 billion for observability and $14 billion for security.

The company has been recognized as a leader in the cloud observability market since 2005, citing analyst recognition from Gartner (NYSE:IT), Forrester, ISG, and GigaOm. Dynatrace claims to be positioned "furthest for Completeness of Vision and highest in Ability (OTC:ABILF) to Execute" in the 2024 Gartner Magic Quadrant for Observability Platforms for the 14th time.

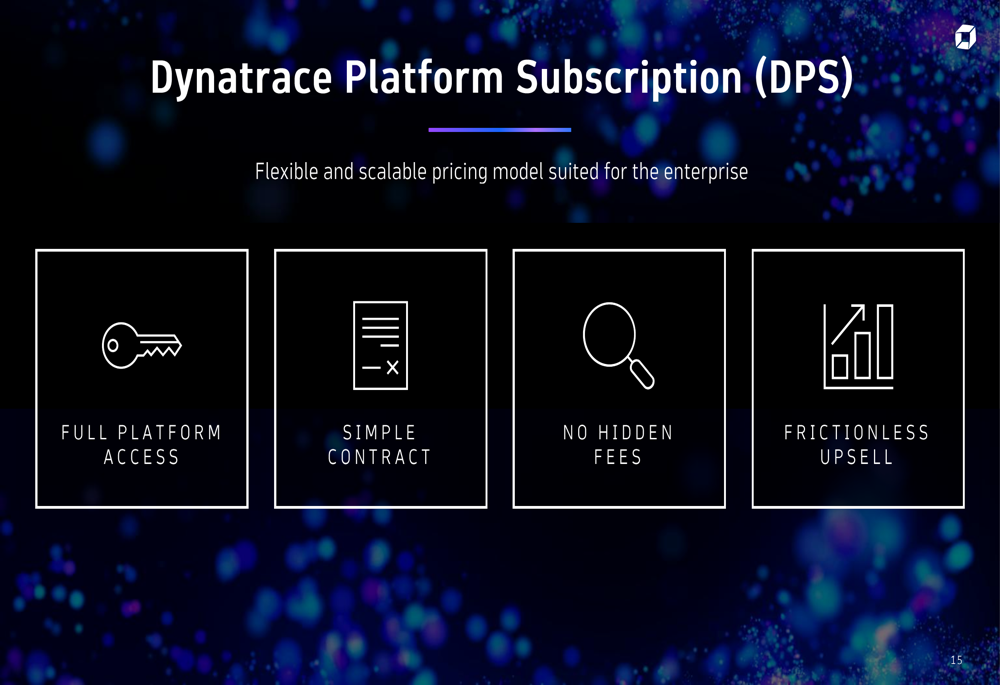

To enhance its competitive position, Dynatrace has introduced the Dynatrace Platform Subscription (DPS) model, which offers customers flexible and scalable pricing with full platform access:

Forward-Looking Statements

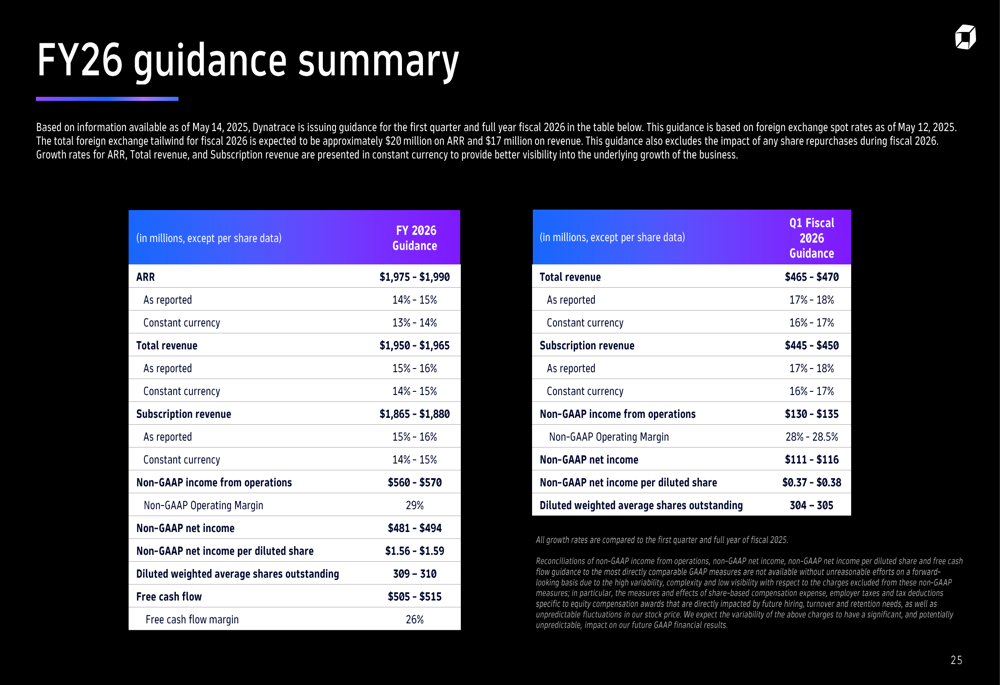

For fiscal year 2026, Dynatrace provided the following guidance:

The FY2026 guidance suggests continued but slightly moderating growth compared to FY2025, with ARR expected to grow 14-15% to reach $1,975-$1,990 million. Total (EPA:TTEF) revenue is projected to increase 15-16% to $1,950-$1,965 million, with subscription revenue growing at a similar rate to $1,865-$1,880 million.

Importantly, Dynatrace expects to maintain its strong profitability profile, with non-GAAP operating margin projected at 29% for FY2026, consistent with FY2025 levels. Free cash flow is anticipated to reach $505-$515 million, representing a margin of 26%.

For Q1 FY2026, the company expects total revenue of $465-$470 million (17-18% growth) and subscription revenue of $445-$450 million (17-18% growth), with a non-GAAP operating margin of 28-28.5%.

Dynatrace’s ability to maintain strong profitability while continuing to grow in a competitive market highlights the strength of its business model and the value proposition of its unified observability platform. However, investors will be watching closely to see if the company can reaccelerate growth in the coming quarters as it continues to expand its platform capabilities and address the growing demand for AI-powered observability solutions.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.