Aspire Biopharma faces potential Nasdaq delisting after compliance shortfall

Introduction & Market Context

Dynavax Technologies Corporation (NASDAQ:DVAX) released its second quarter 2025 earnings presentation on August 7, 2025, highlighting record HEPLISAV-B sales and progress across its vaccine pipeline. The company’s stock closed at $11.06, down 1.16% for the day, reflecting some investor caution despite the positive quarterly results.

The presentation comes after a challenging first quarter where Dynavax reported an EPS miss, posting -$0.77 against an expected $0.04. However, the Q2 results suggest the company is maintaining its revenue growth trajectory while advancing its diversified vaccine portfolio.

Quarterly Performance Highlights

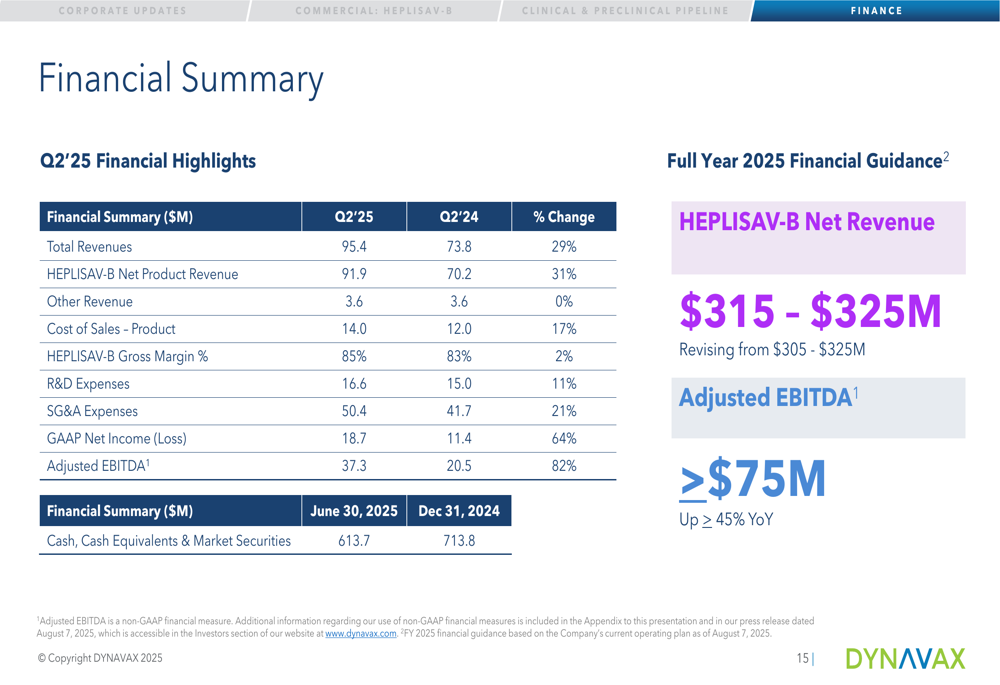

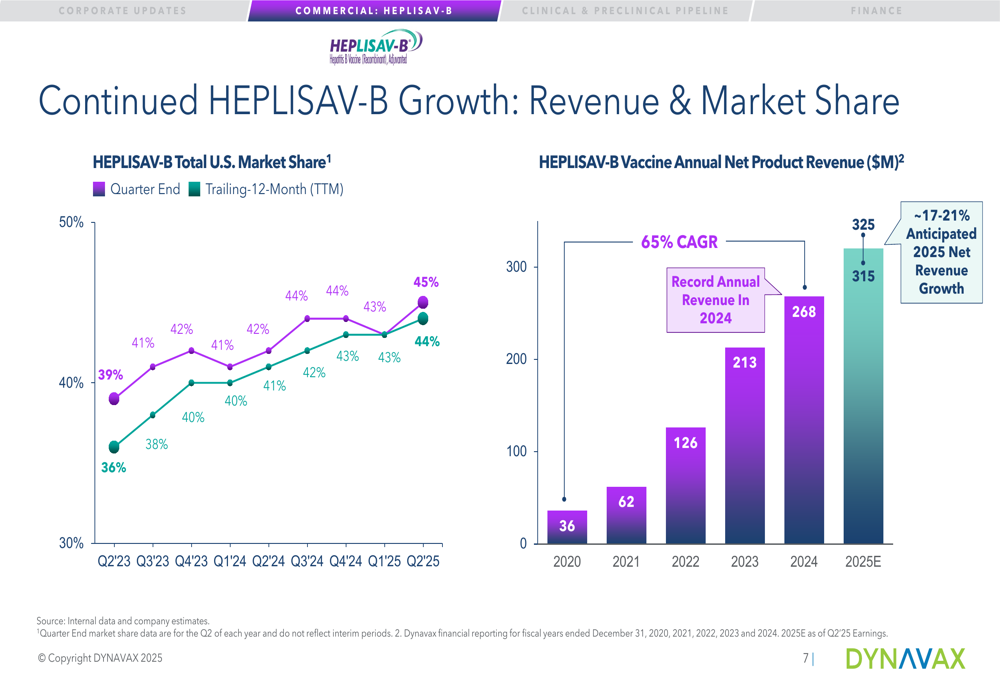

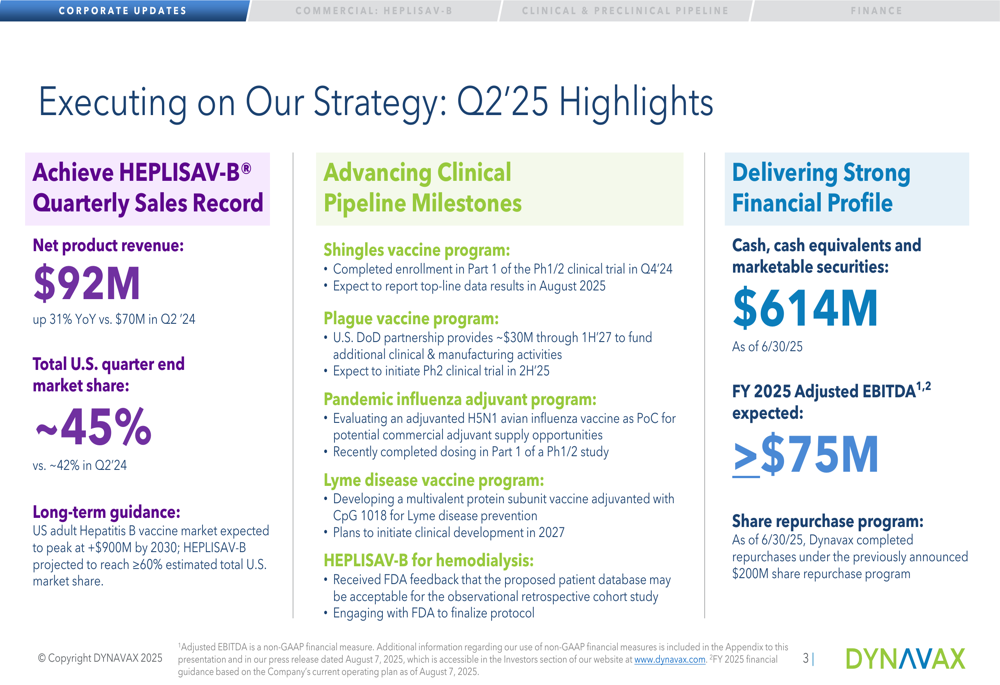

Dynavax reported record HEPLISAV-B net product revenue of $91.9 million in Q2 2025, representing a 31% year-over-year increase. The company’s hepatitis B vaccine continues to gain market share, now capturing approximately 45% of the U.S. adult market.

As shown in the following financial summary from the presentation:

Total (EPA:TTEF) revenues for the quarter reached $95.4 million, with HEPLISAV-B maintaining a strong gross margin of 85%. The company ended the quarter with $613.7 million in cash, cash equivalents, and marketable securities, a slight decrease from the $661 million reported at the end of Q1 2025.

Dynavax also completed its previously announced $200 million share repurchase program, demonstrating confidence in its long-term growth prospects despite recent stock price weakness.

HEPLISAV-B Growth and Market Position

HEPLISAV-B continues to be Dynavax’s primary revenue driver, with impressive growth across multiple market segments. The vaccine has achieved particularly strong penetration in retail pharmacy (59%), integrated delivery networks (51%), and dialysis centers (53%).

The following chart illustrates HEPLISAV-B’s consistent revenue growth trajectory since 2020:

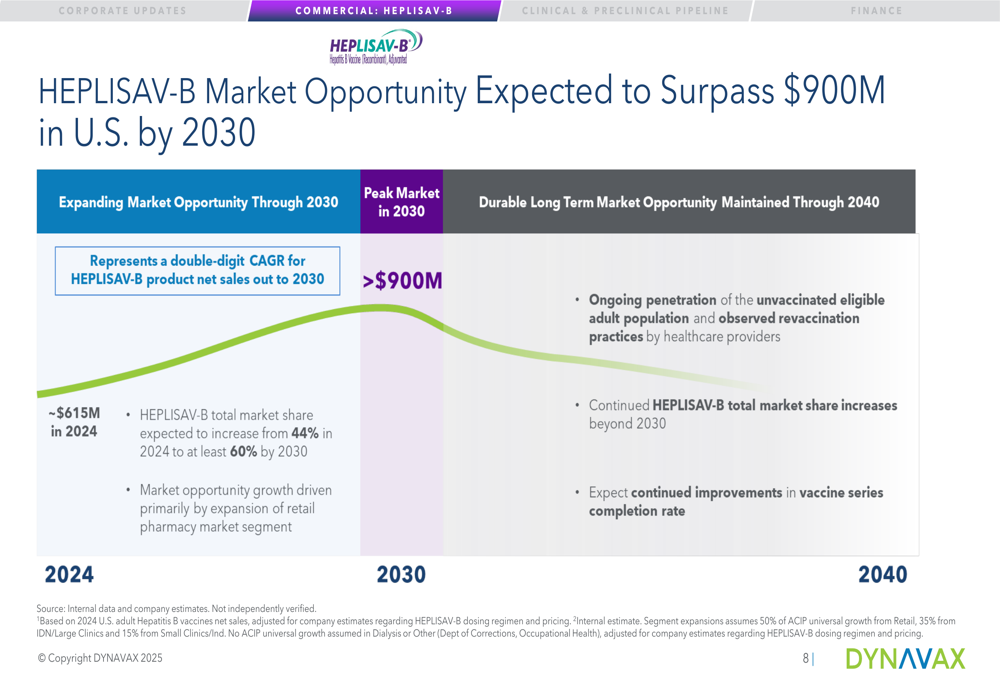

Looking ahead, Dynavax projects the U.S. adult Hepatitis B vaccine market to expand significantly, reaching over $900 million by 2030. The company expects HEPLISAV-B to capture at least 60% of this growing market, as shown in the market opportunity projection:

This growth is expected to be primarily driven by expansion in the retail pharmacy segment, where HEPLISAV-B already holds a dominant position.

Pipeline Development Progress

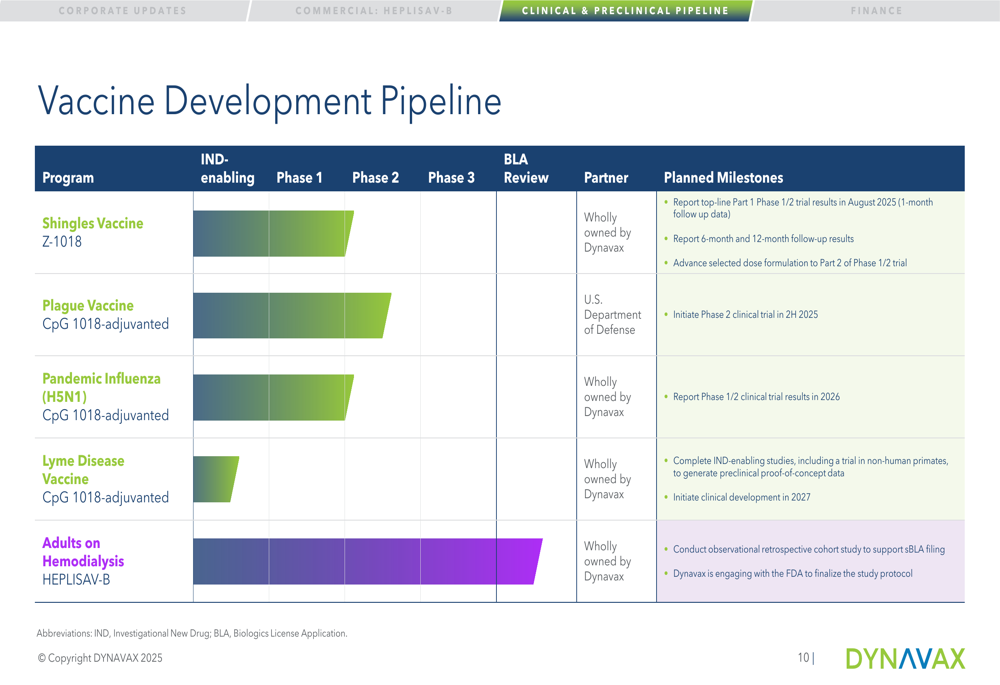

Beyond HEPLISAV-B, Dynavax is advancing a diversified vaccine portfolio leveraging its proprietary CpG 1018 adjuvant technology. The company’s development pipeline includes several promising candidates:

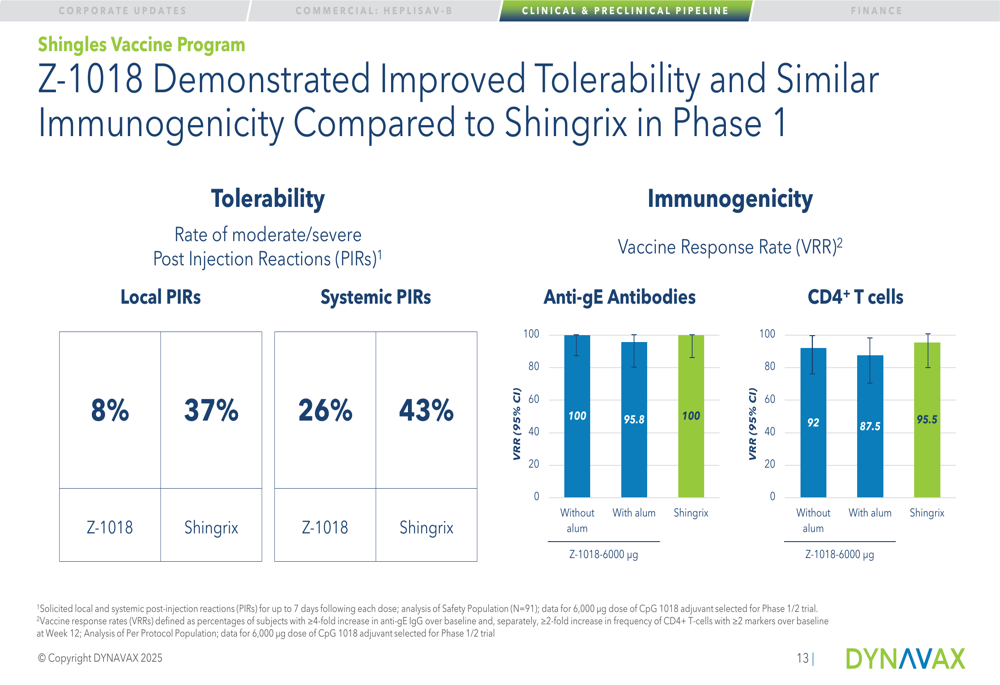

The shingles vaccine program (Z-1018) represents one of Dynavax’s most advanced pipeline opportunities. Early clinical data suggests Z-1018 may offer similar immunogenicity to the market-leading Shingrix vaccine but with significantly improved tolerability. Post-injection reactions were reported in only 8% of Z-1018 recipients compared to 37% for Shingrix.

As illustrated in the following comparative data:

Dynavax expects to report top-line data from Part 1 of its Phase 1/2 shingles vaccine trial in August 2025, a key catalyst for the company. The global shingles vaccine market represents a substantial opportunity, estimated at approximately $4.2 billion in 2024.

Additional pipeline programs include vaccines for plague, pandemic influenza (H5N1), and Lyme disease, with several milestone events expected in the coming quarters.

Financial Performance and Outlook

Dynavax maintained its full-year 2025 guidance, projecting HEPLISAV-B net revenue between $315-$325 million, representing 17-21% growth over 2024. The company also expects adjusted EBITDA to exceed $75 million for the full year.

The Q2 highlights summarize the company’s current financial position and outlook:

While the presentation emphasizes revenue growth and adjusted EBITDA, it notably omits discussion of EPS figures, which were a concern in Q1 when the company reported a significant earnings miss. The decrease in cash position from $661 million in Q1 to $614 million in Q2 suggests continued investment in R&D and commercial activities.

Market Reaction and Analyst Perspectives

Despite the positive revenue growth and pipeline progress, Dynavax’s stock has shown weakness, trading well below its 52-week high of $14.63. The current price of $11.06 represents a modest premium to the 52-week low of $9.22.

This cautious market reaction may reflect ongoing concerns about profitability and the significant investments required to advance the company’s pipeline programs. The Q1 earnings report highlighted increased R&D and SG&A expenses as potential pressure points for short-term profitability.

However, Dynavax’s strong market position in the hepatitis B vaccine segment, combined with its promising pipeline candidates, particularly in the lucrative shingles vaccine market, provides multiple potential growth catalysts. The company’s substantial cash reserves also offer financial flexibility to support continued pipeline development while maintaining its commercial operations.

As Dynavax progresses toward its strategic goal of building a diversified adult vaccine portfolio, investors will be closely watching the upcoming shingles vaccine data readout and the continued execution of the company’s commercial strategy for HEPLISAV-B.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.