Powell’s speech, Nvidia’s chips, Meta deal - what’s moving markets

Introduction & Market Context

Eagle Materials Inc . (NASDAQ:NYSE:EXP) presented its first quarter fiscal 2026 earnings results on July 29, 2025, revealing a mixed performance characterized by record revenue growth but declining earnings per share. The company’s stock responded positively in premarket trading, rising 2.53% to $226.50, suggesting investors were encouraged by the overall trajectory despite some earnings pressure.

The building materials producer continues to benefit from infrastructure spending and residential construction in its key markets, while simultaneously investing heavily in facility modernization and sustainability initiatives. This comes after a challenging previous fiscal year when the company missed earnings expectations in Q1 2025.

Quarterly Performance Highlights

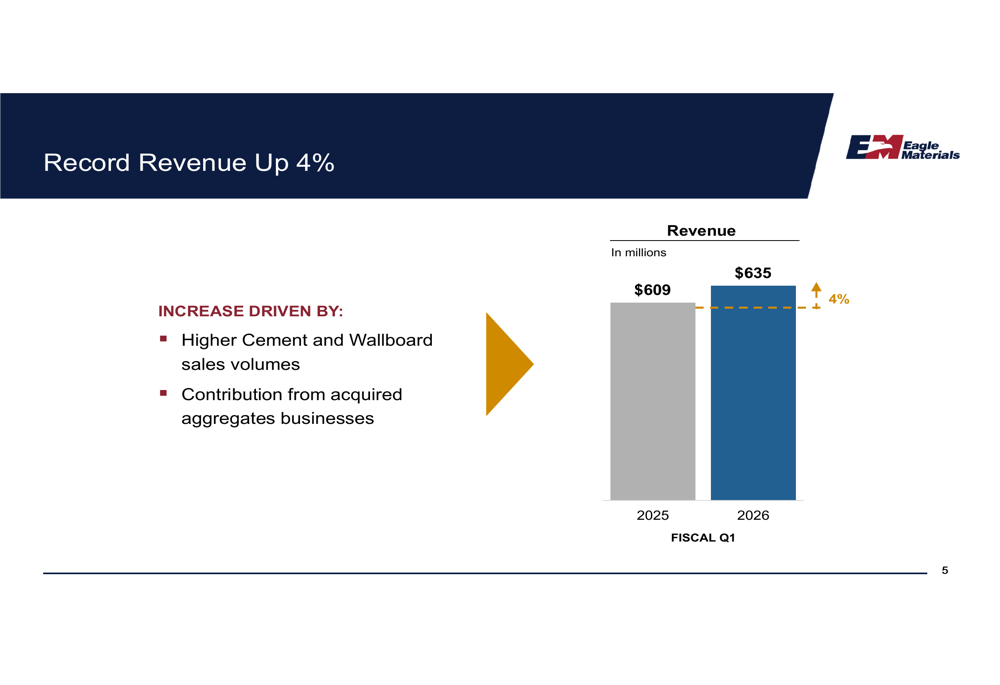

Eagle Materials delivered record first-quarter revenue of $635 million, representing a 4% increase from $609 million in the same period last year. The company attributed this growth to higher cement and wallboard sales volumes, along with contributions from recently acquired aggregates businesses.

As shown in the following revenue comparison chart:

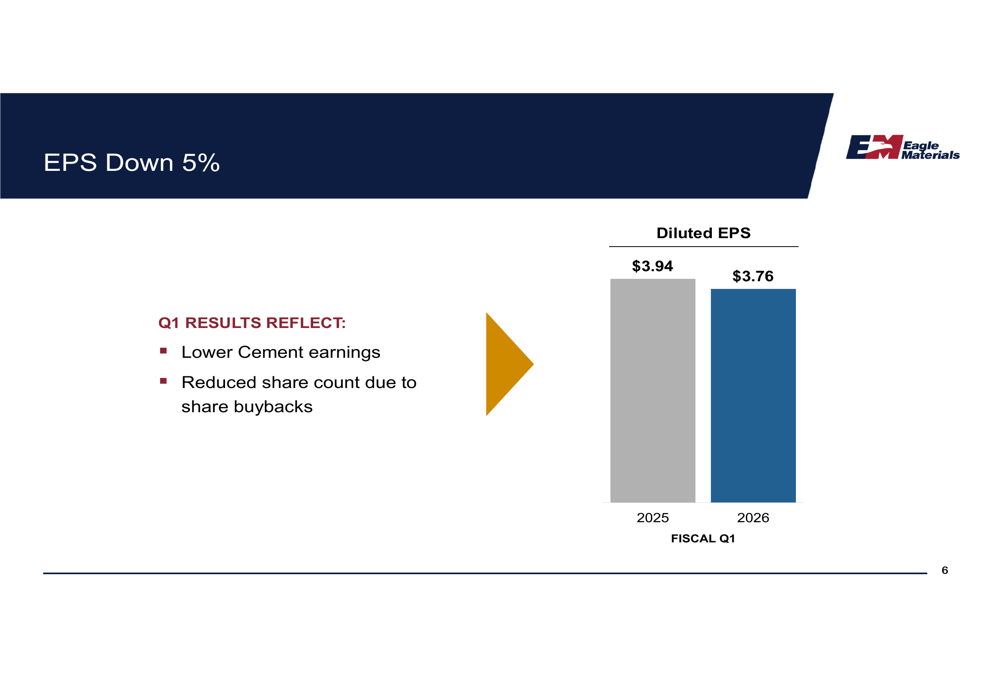

Despite the revenue gains, earnings per share declined 5% year-over-year to $3.76 from $3.94 in Q1 FY2025. The company cited lower cement earnings as the primary factor for the decrease, though this was partially offset by a reduced share count resulting from the company’s ongoing share repurchase program.

The EPS decline is illustrated in this comparison:

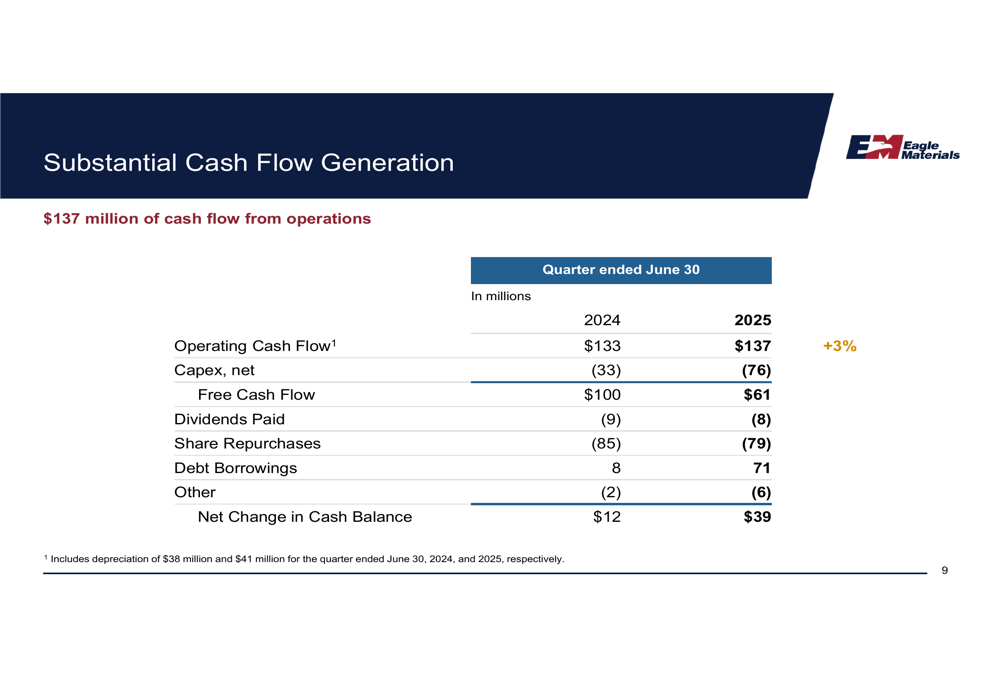

The company maintained a solid gross profit margin of 29.2% while generating $137 million in operating cash flow, a 3% improvement from the previous year. Eagle Materials continued its shareholder return strategy by repurchasing 358,000 shares for $79 million and paying $8 million in quarterly dividends, returning a total of $87 million to shareholders.

Segment Analysis

Eagle Materials’ performance varied across its two main business segments: Heavy Materials and Light Materials.

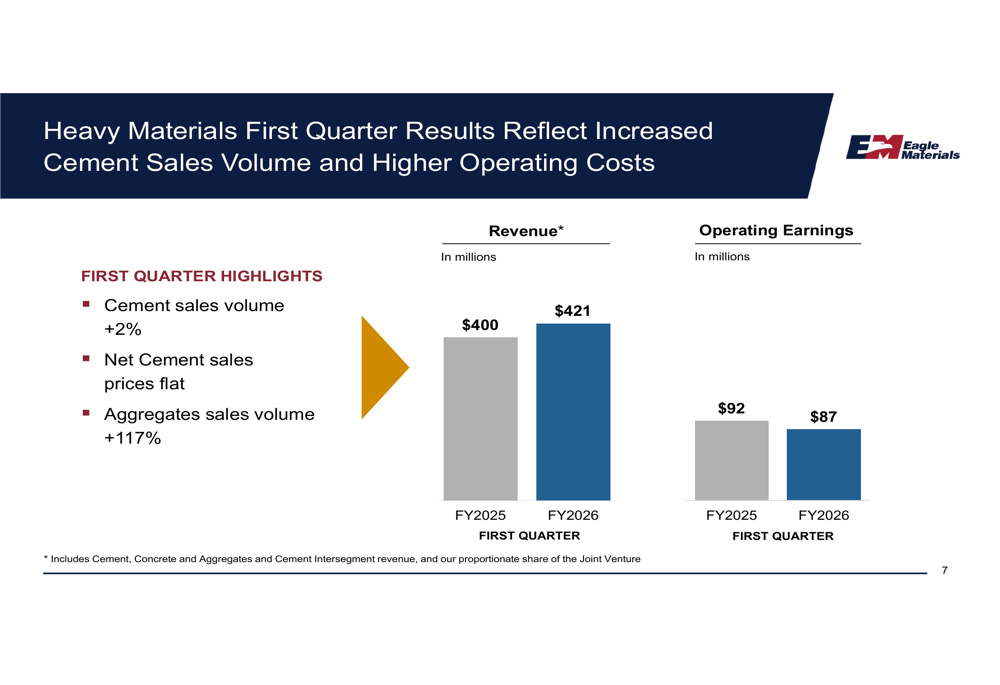

The Heavy Materials segment, which includes cement and concrete products, saw revenue increase from $400 million to $421 million. However, operating earnings declined from $92 million to $87 million. Cement sales volume increased by 2% while pricing remained flat compared to the previous year. The most significant growth came from aggregates, where sales volume surged by 117%, largely due to recent acquisitions.

The segment performance is detailed in the following chart:

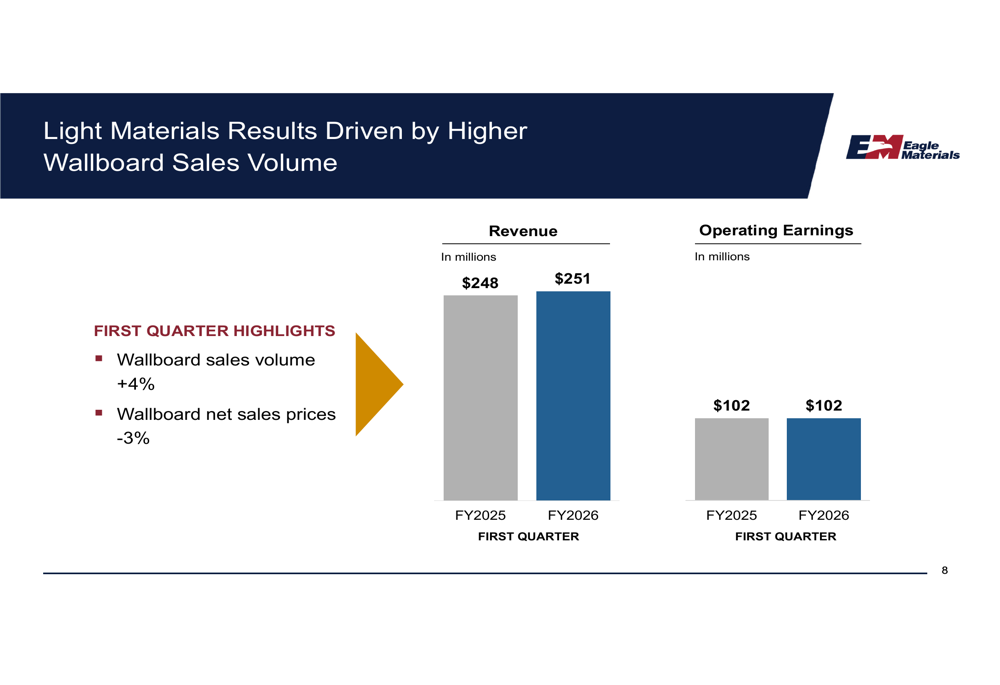

The Light Materials segment, primarily consisting of gypsum wallboard and paperboard, delivered more stable results. Revenue edged up slightly from $248 million to $251 million, while operating earnings remained flat at $102 million. Wallboard sales volume increased by 4%, though this was partially offset by a 3% decline in wallboard prices.

The Light Materials results are illustrated here:

Capital Allocation and Cash Flow

Eagle Materials significantly increased its capital expenditures in Q1 FY2026 to $76 million, more than double the $33 million spent in the same period last year. This substantial increase reflects the company’s ongoing investments in plant modernization, including projects at its Laramie, Wyoming cement plant and Duke, Oklahoma wallboard facility.

The increased capital spending resulted in a reduction in free cash flow to $61 million from $100 million in the prior year, despite the higher operating cash flow. The company’s detailed cash flow statement reveals the following:

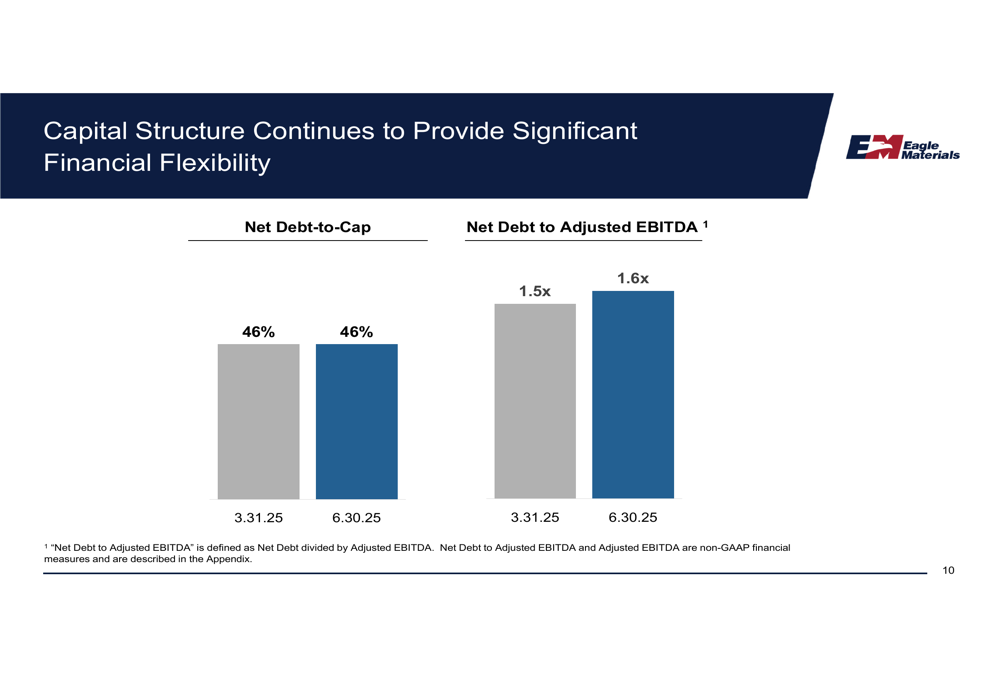

Despite the increased investments and share repurchases, Eagle Materials maintained a conservative financial position. The net debt-to-capital ratio remained steady at 46%, while the net debt to adjusted EBITDA ratio increased slightly from 1.5x to 1.6x, still indicating substantial financial flexibility.

The capital structure metrics are shown here:

Forward Outlook and Strategic Initiatives

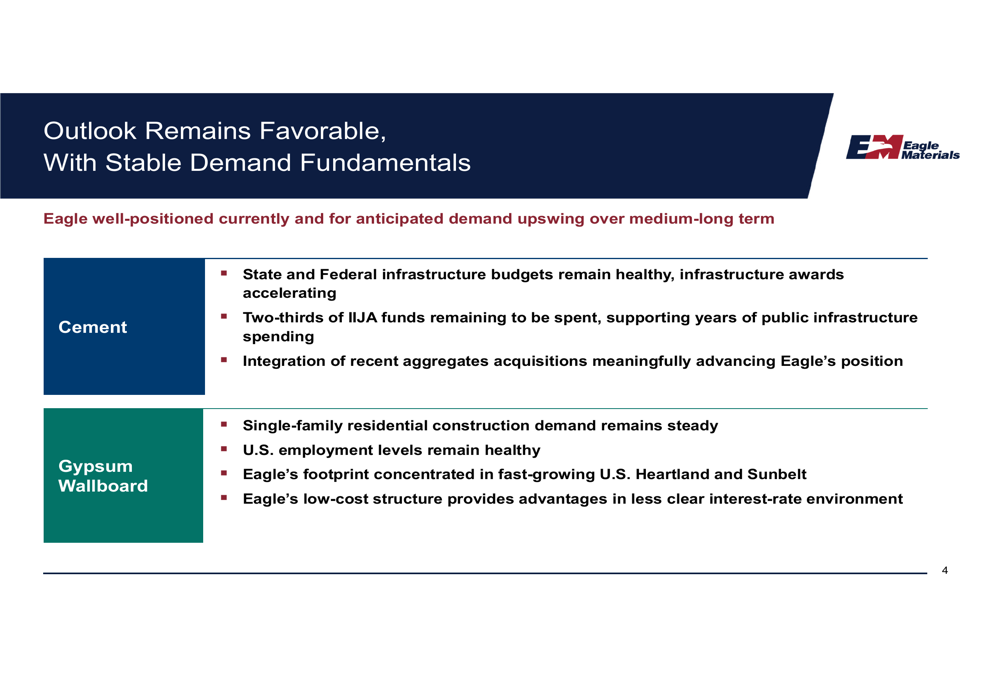

Eagle Materials presented an optimistic outlook based on several favorable market conditions. For its cement business, the company highlighted healthy state and federal infrastructure budgets with accelerating infrastructure awards. Management noted that approximately two-thirds of Infrastructure Investment and Jobs Act (IIJA) funds remain to be spent, providing a substantial pipeline of future projects.

The company’s forward-looking assessment is detailed in this slide:

In the wallboard segment, Eagle Materials expects steady demand from single-family residential construction, supported by healthy U.S. employment levels. The company emphasized its geographic advantage with operations concentrated in the fast-growing U.S. Heartland and Sunbelt regions, areas experiencing above-average population growth and construction activity.

Eagle Materials also highlighted progress on its sustainability initiatives, having achieved its mid-term CO2e intensity target. The company noted its position as a lead equity investor in Terra CO2, suggesting ongoing commitment to reducing its environmental footprint.

The company’s strategic focus remains on maintaining its low-cost producer status while continuing to invest in modernization and selective acquisitions to enhance its competitive position in key markets.

With a net debt to adjusted EBITDA ratio of just 1.6x, Eagle Materials retains significant financial flexibility to pursue both organic growth initiatives and potential acquisition opportunities while continuing to return capital to shareholders through dividends and share repurchases.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.