S&P 500 rides Apple-led tech rally higher

Introduction & Market Context

Eagle Point Credit Company (NYSE:ECC), a closed-end management investment company specializing in collateralized loan obligations (CLOs), presented its Q1 2025 update on May 28, 2025, highlighting portfolio growth and strong cash distributions in an expanding CLO market.

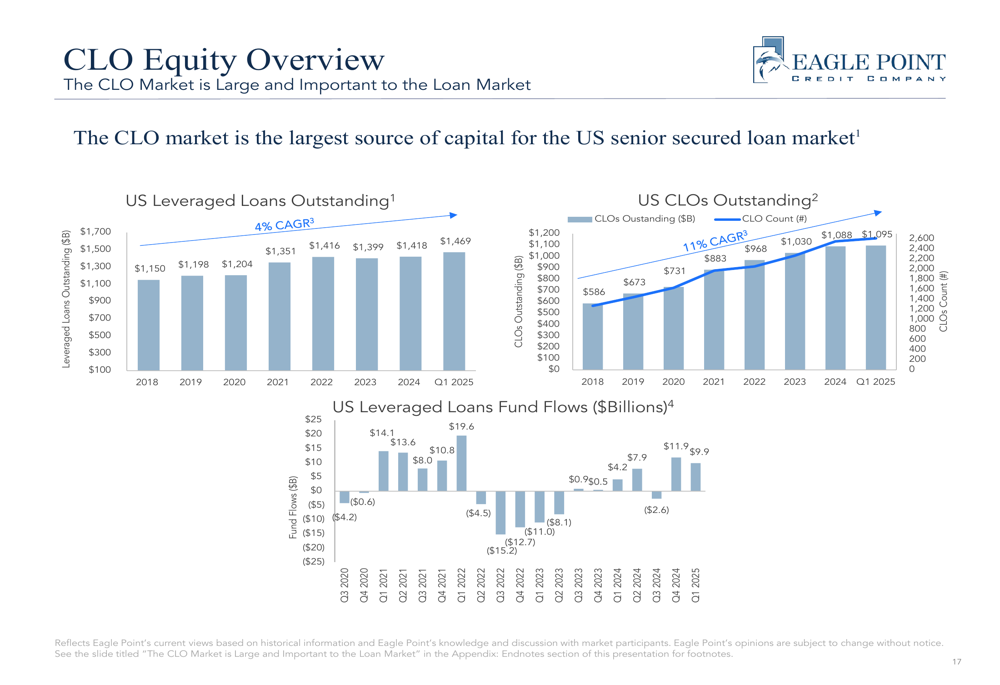

The presentation revealed that ECC continues to capitalize on the growing CLO market, which remains the largest source of capital for the U.S. senior secured loan market. With a total market capitalization of $1.46 billion, ECC maintains its position as a significant player in the CLO investment space.

As shown in the following chart, both the leveraged loan market and CLO market have experienced steady growth, with U.S. CLOs outstanding growing at an 11% CAGR from 2018 to Q1 2025, outpacing the 4% growth in leveraged loans:

This growth trajectory provides ECC with an expanding market for its investment strategy, which focuses primarily on CLO equity tranches. The company emphasized that senior secured loans, the primary assets underlying CLOs, have demonstrated remarkable consistency, with the S&P UBS Leveraged Loan Index generating positive total returns in 30 of the past 33 full calendar years.

Quarterly Performance Highlights

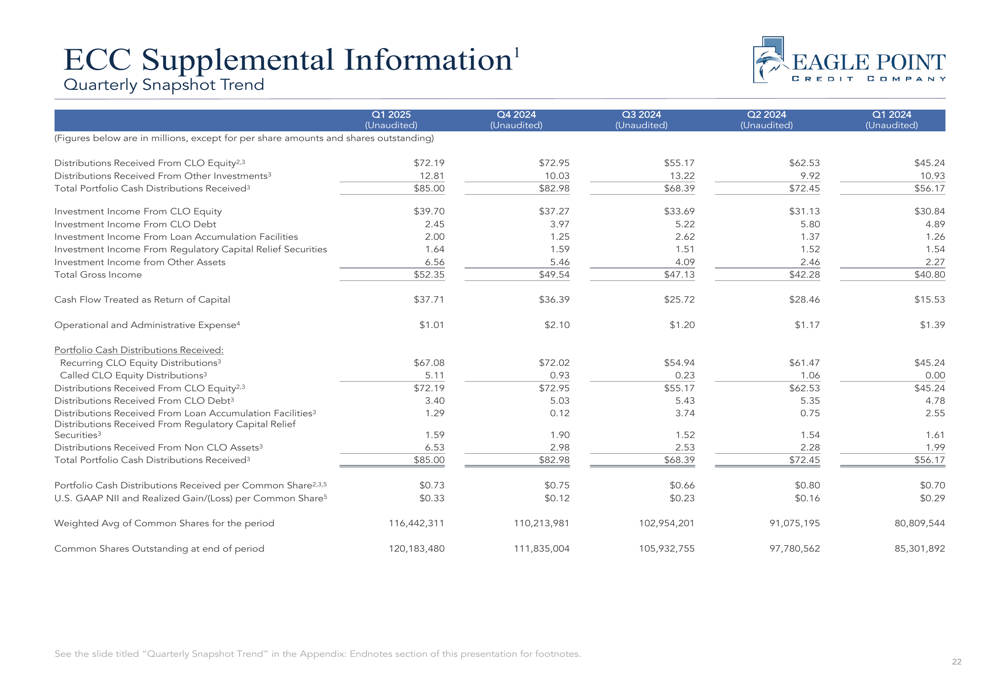

ECC reported strong cash distributions in Q1 2025, with total portfolio cash distributions received reaching $85.00 million, up significantly from $56.17 million in Q1 2024. This represents a 51.3% year-over-year increase in cash distributions.

The company’s quarterly financial snapshot reveals consistent improvement across key metrics:

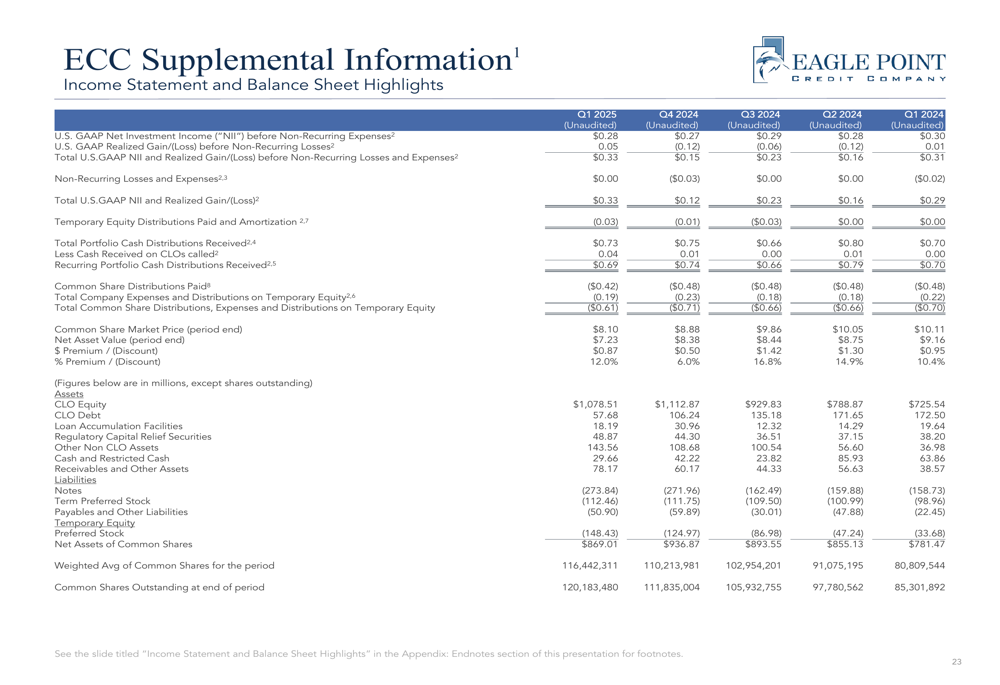

Total (EPA:TTEF) gross income for Q1 2025 reached $52.35 million, compared to $40.80 million in Q1 2024, representing a 28.3% year-over-year increase. U.S. GAAP Net Investment Income (NII) and realized gains per common share stood at $0.33 for Q1 2025, higher than the $0.29 reported in Q1 2024.

The income statement and balance sheet highlights further demonstrate ECC’s financial position:

This performance comes after a mixed Q3 2024, when the company reported a decrease in recurring cash flows to $68.2 million ($0.66 per share) from $71.4 million ($0.79 per share) in the previous quarter, though NAV per share increased from $8.44 to $8.60 during that period.

Portfolio Composition and Strategy

ECC’s investment portfolio remains heavily weighted toward CLO equity, which constitutes 79% of the total portfolio. The company’s diversified approach includes exposure to consumer ABS (6%), regulatory capital relief (4%), and CLO debt (4%), among other investments.

As illustrated in the following portfolio breakdown, ECC maintains a well-diversified approach while focusing on its core CLO equity strategy:

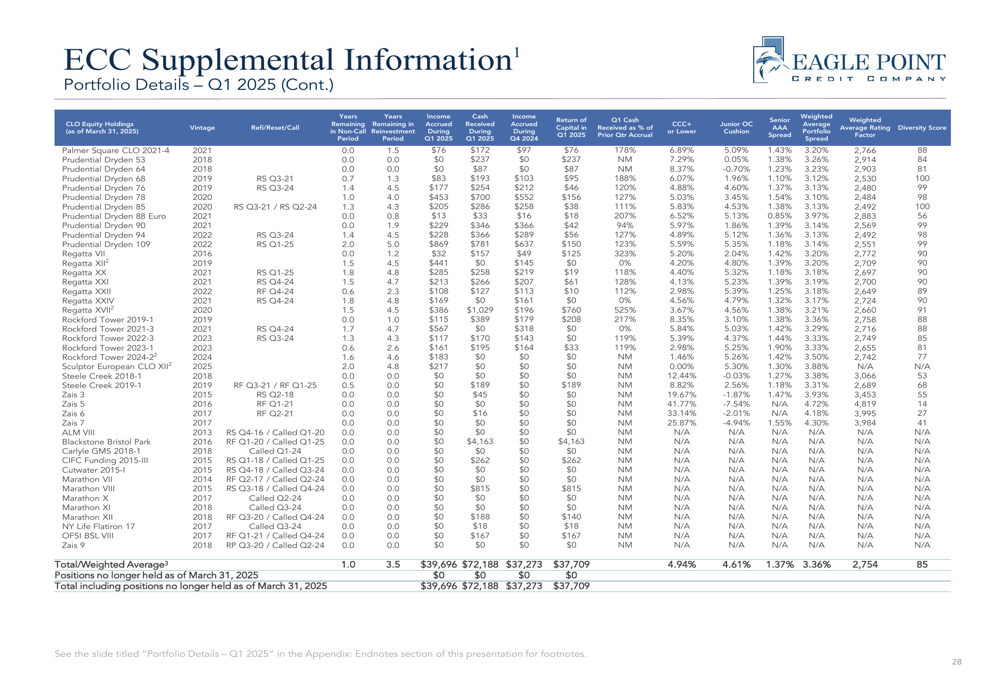

The company’s portfolio includes 215 CLO equity securities managed by 45 different CLO collateral managers, providing significant diversification. With exposure to 1,931 unique underlying loan obligors and a maximum exposure to any individual obligor of just 0.59%, ECC maintains a well-diversified credit risk profile.

ECC’s investment approach is characterized as a "private equity style" strategy applied to fixed income investing, with emphasis on proactive sourcing, rigorous analysis, and involvement at the CLO formation and structuring stage. This approach is managed by a senior investment team with an average of 21 years of CLO experience.

Distribution and Income Analysis

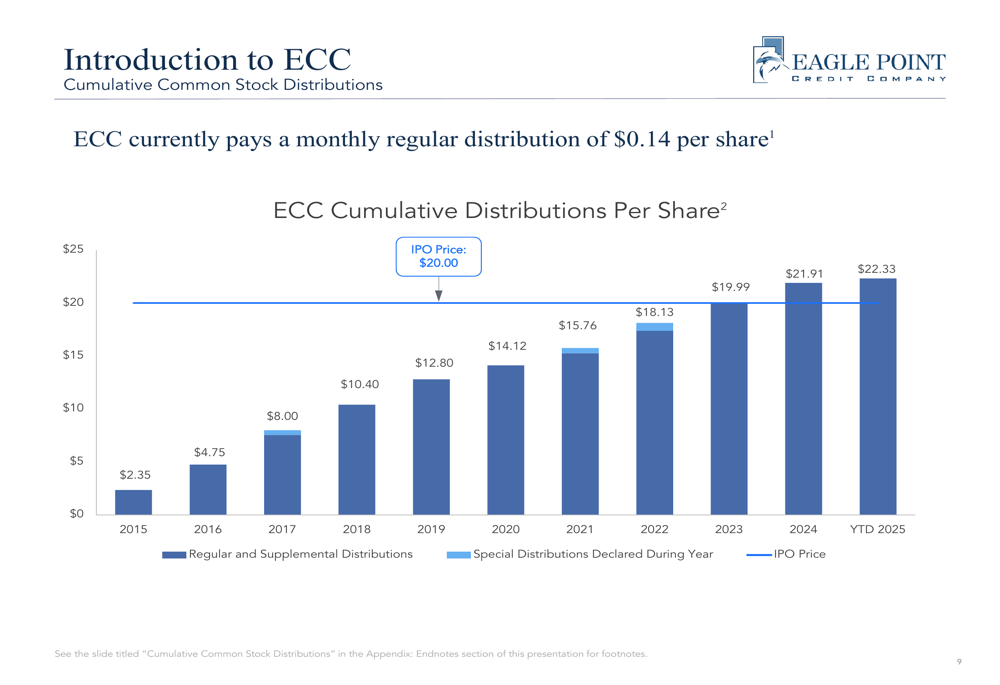

ECC currently pays a monthly distribution of $0.14 per share of common stock, which translates to a distribution rate of 21.6%. Since its IPO in October 2014, the company has paid cumulative common distributions of $22.33 per share, exceeding its initial IPO price of $20.

The following chart illustrates the growth in cumulative distributions over time:

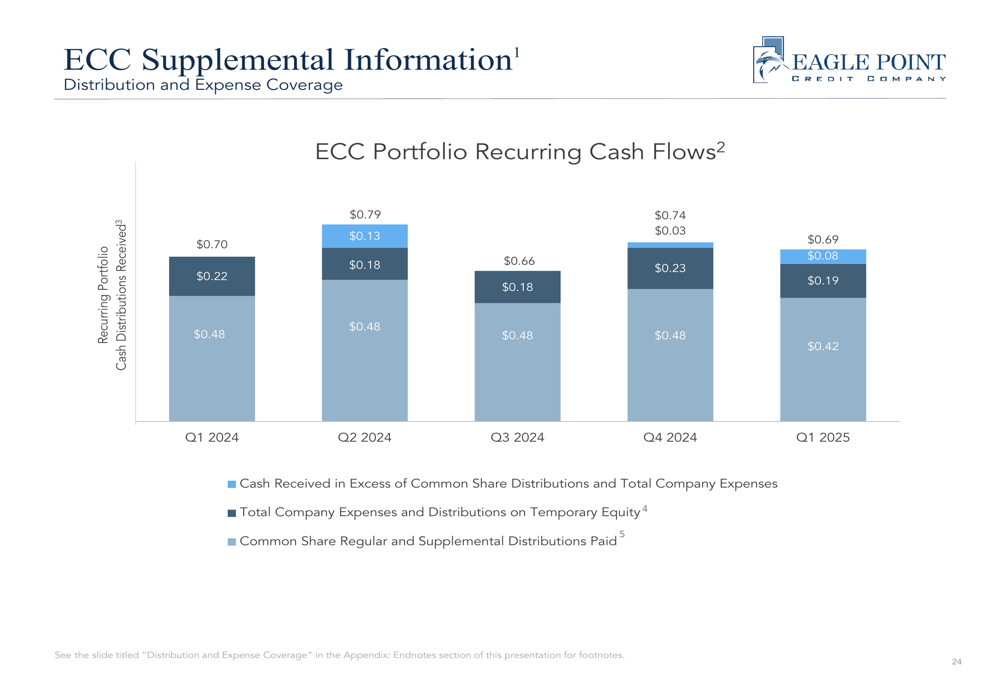

The company’s ability to maintain its distribution is supported by strong portfolio cash flows. As shown in the distribution and expense coverage chart, ECC’s portfolio recurring cash flows have consistently exceeded its distributions and expenses:

For Q1 2025, ECC received $0.69 per share in cash flows, which covered both its expenses ($0.19 per share) and distributions ($0.42 per share) with excess cash remaining. This demonstrates the company’s ability to generate sufficient cash flow to support its high distribution rate.

Forward-Looking Statements

Looking ahead, ECC highlighted several factors that position it favorably in the current market environment. The company’s weighted average reinvestment period stands at 3.5 years, providing a substantial runway for its CLO investments to continue generating returns through various market cycles.

ECC’s management remains focused on maintaining a long reinvestment period as a key risk mitigant, a strategy that was emphasized in their Q3 2024 earnings call. The company has also been proactive in deploying capital, having invested over $171 million into new investments with an average yield of 18.5% on CLO equity purchases during Q3 2024.

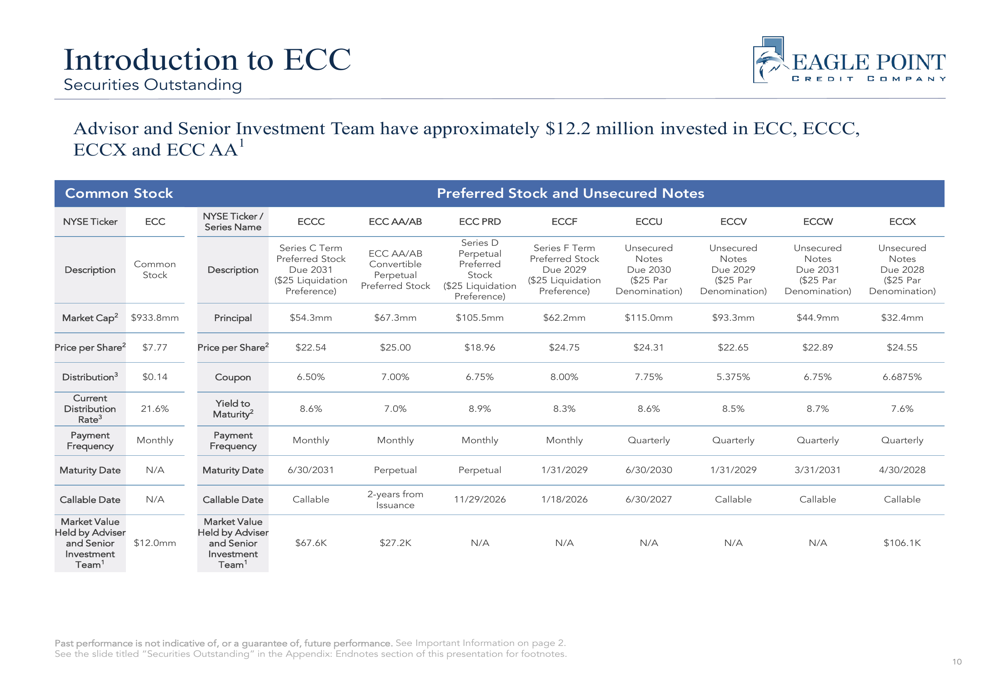

The company’s securities outstanding provide a comprehensive view of its capital structure:

With a common stock market capitalization of $933.8 million and a total market capitalization of $1.46 billion, ECC maintains a diversified capital structure that includes preferred stock and unsecured notes. Notably, the company’s adviser and senior investment team have approximately $12.2 million invested in ECC securities, demonstrating alignment of interests with shareholders.

ECC’s performance relative to the S&P BDC Index shows that while the company has slightly underperformed the index in terms of total return (108.64% versus 119.55% from October 2014 to April 2025), it has traded at an average premium to book value of 10.7% compared to an average discount of -5.0% for the index. This suggests investor confidence in ECC’s strategy and management.

As ECC continues to navigate the CLO market, its focus on maintaining a diversified portfolio with a long reinvestment period positions it to potentially benefit from the ongoing expansion of the CLO market while generating substantial cash distributions for shareholders.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.