Cardiff Oncology shares plunge after Q2 earnings miss

Introduction & Market Context

East West Bancorp (NASDAQ:EWBC) released its first quarter 2025 earnings presentation on April 22, 2025, revealing solid performance with record quarterly revenue and fee income. The bank reported net income available to common equity of $290 million and diluted earnings per share of $2.08. EWBC shares closed at $76.28 on the day of the presentation, rising 3.68% during regular trading hours.

The bank’s performance comes amid a challenging environment for regional banks, with East West demonstrating resilience through its diversified business model and cross-border capabilities. The presentation highlighted the company’s strategic focus on optimizing its deposit mix, maintaining balanced loan growth, and strengthening its fee income streams.

Quarterly Performance Highlights

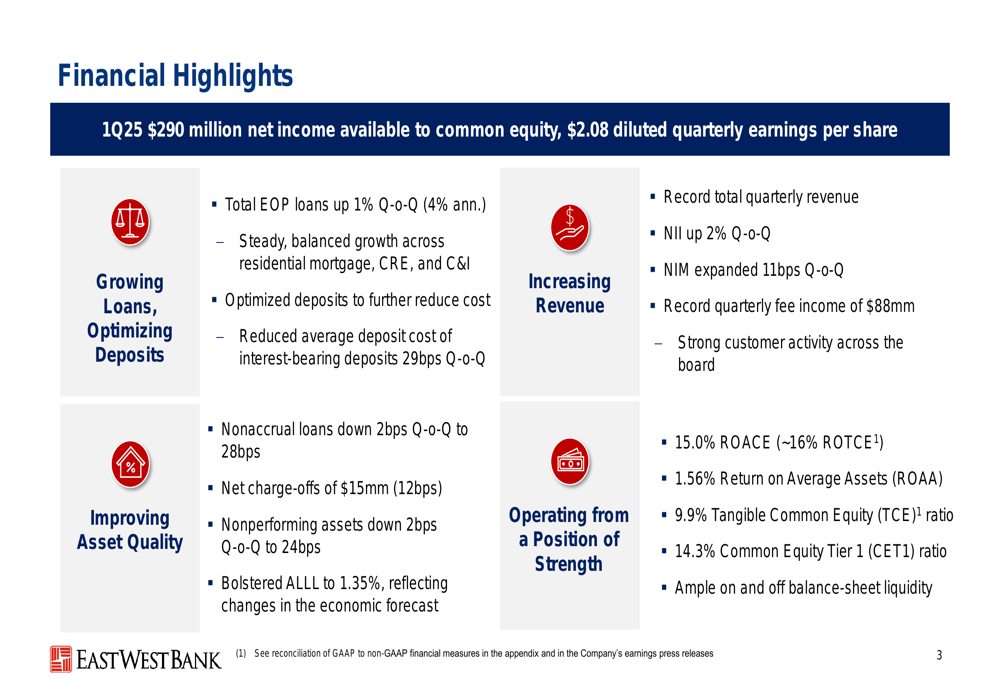

East West Bancorp reported strong financial metrics for Q1 2025, with several key achievements that underscore the bank’s operational strength and strategic execution.

As shown in the following comprehensive overview of the quarter’s financial highlights:

The bank reported net income available to common equity of $290 million and diluted quarterly earnings per share of $2.08. Total (EPA:TTEF) end-of-period loans increased by 1% quarter-over-quarter (4% annualized), reflecting steady balanced growth. The bank also optimized its deposit mix to reduce costs, with the average cost of interest-bearing deposits decreasing by 29 basis points quarter-over-quarter.

Revenue performance was particularly strong, with record total quarterly revenue driven by a 2% quarter-over-quarter increase in net interest income (NII) and an 11 basis point expansion in net interest margin (NIM). The bank also achieved record quarterly fee income of $88 million.

Asset quality metrics improved across the board, with nonaccrual loans decreasing by 2 basis points quarter-over-quarter to 28 basis points and nonperforming assets declining by 2 basis points to 24 basis points. The bank reported net charge-offs of $15 million (12 basis points) and bolstered its allowance for loan losses (ALLL) to 1.35%.

Detailed Financial Analysis

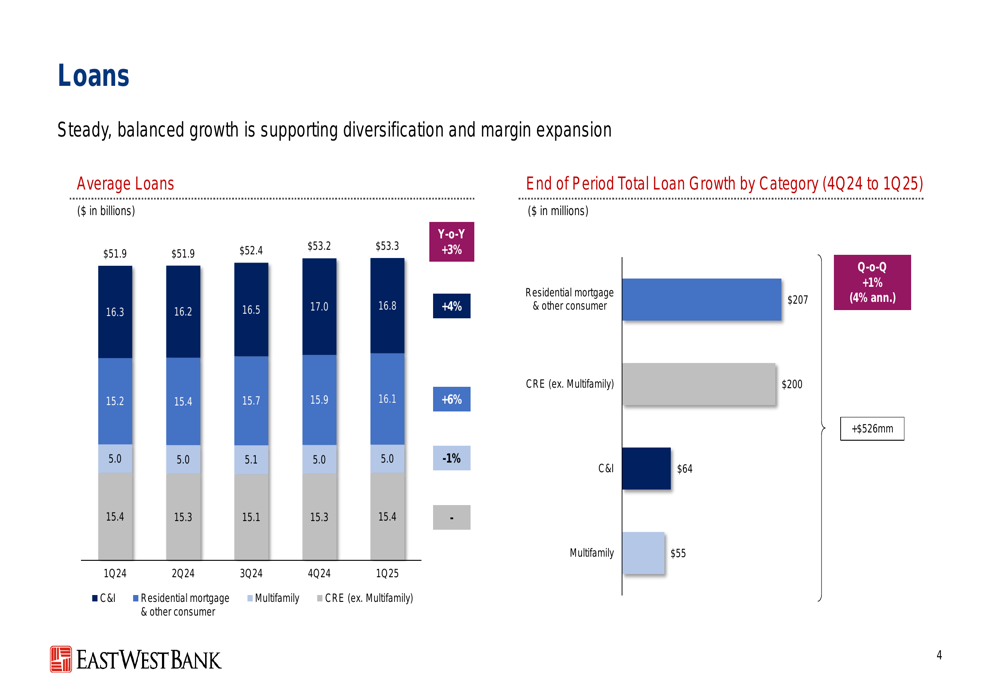

East West Bancorp’s loan portfolio showed continued diversification and growth in Q1 2025, with balanced increases across multiple categories.

The following chart illustrates the composition and growth of the bank’s loan portfolio:

Average loans increased across most categories year-over-year, with C&I loans growing by 3% to $53.3 billion, residential mortgage and other consumer loans increasing by 4% to $16.8 billion, and CRE (excluding multifamily) rising by 6% to $16.1 billion. Multifamily loans remained relatively flat at $5.0 billion. Total loan growth from Q4 2024 to Q1 2025 was $526 million, with residential mortgage and other consumer contributing $207 million, CRE (excluding multifamily) adding $200 million, C&I growing by $64 million, and multifamily increasing by $55 million.

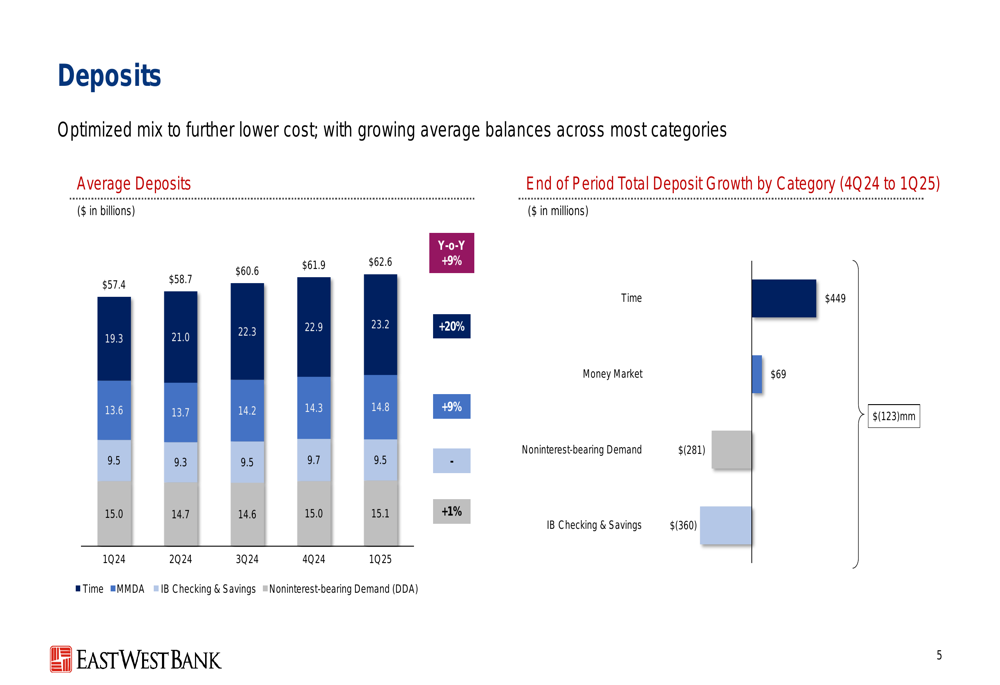

On the deposit front, East West Bancorp focused on optimizing its mix to reduce costs while maintaining adequate funding:

Average deposits showed year-over-year growth across all categories, with time deposits increasing by 9% to $62.6 billion, money market deposit accounts (MMDA) growing by 20% to $23.2 billion, and interest-bearing checking and savings rising by 9% to $14.8 billion. Noninterest-bearing demand deposits remained relatively stable at $15.1 billion, up 1% year-over-year. End-of-period total deposits decreased slightly by $123 million from Q4 2024 to Q1 2025, with increases in time deposits ($449 million) and money market accounts ($69 million) offset by decreases in noninterest-bearing demand ($281 million) and interest-bearing checking and savings ($360 million).

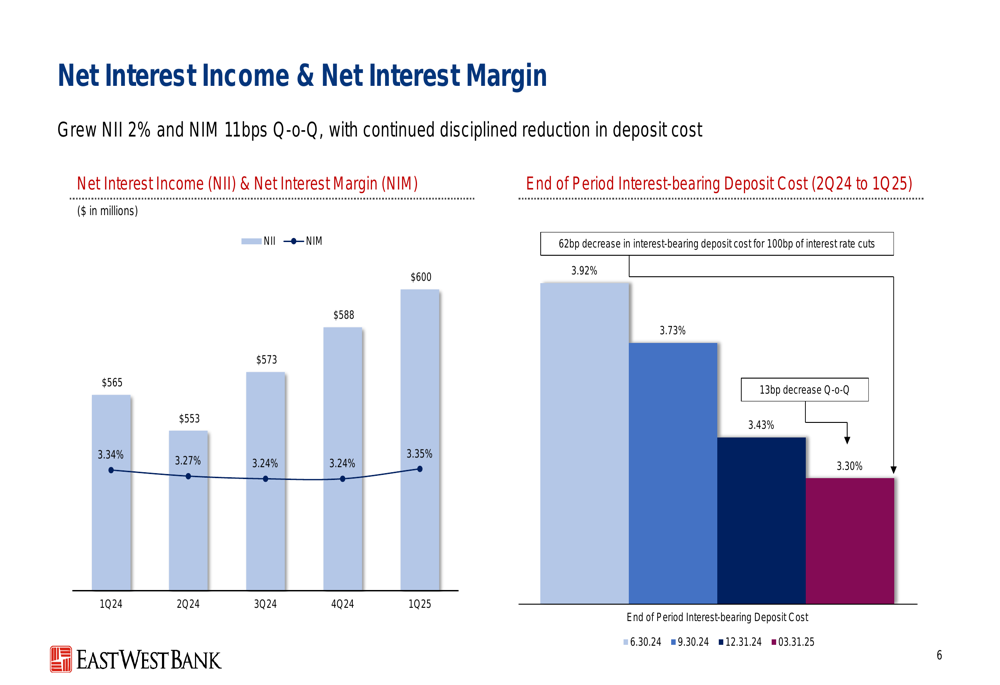

The bank’s net interest income and margin showed improvement in Q1 2025:

Net interest income increased from $565 million in Q1 2024 to $600 million in Q1 2025, while net interest margin expanded from 3.24% in Q4 2024 to 3.35% in Q1 2025, an 11 basis point improvement. The end-of-period interest-bearing deposit cost decreased from 3.92% on June 30, 2024, to 3.30% on March 31, 2025, representing a 62 basis point decrease for 100 basis points of interest rate cuts and a 13 basis point decrease quarter-over-quarter.

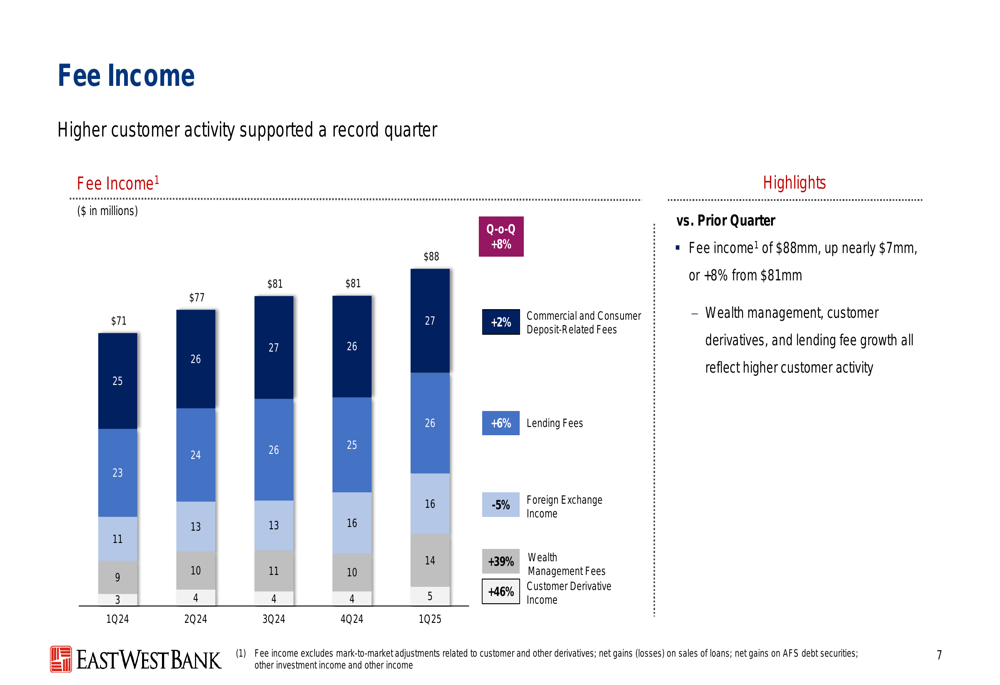

Fee income reached a record level in Q1 2025, reflecting the bank’s success in diversifying its revenue streams:

Fee income for Q1 2025 was $88 million, up from $81 million in Q4 2024, representing an 8% increase. The growth was driven by increased customer activity across wealth management, customer derivatives, and lending fees.

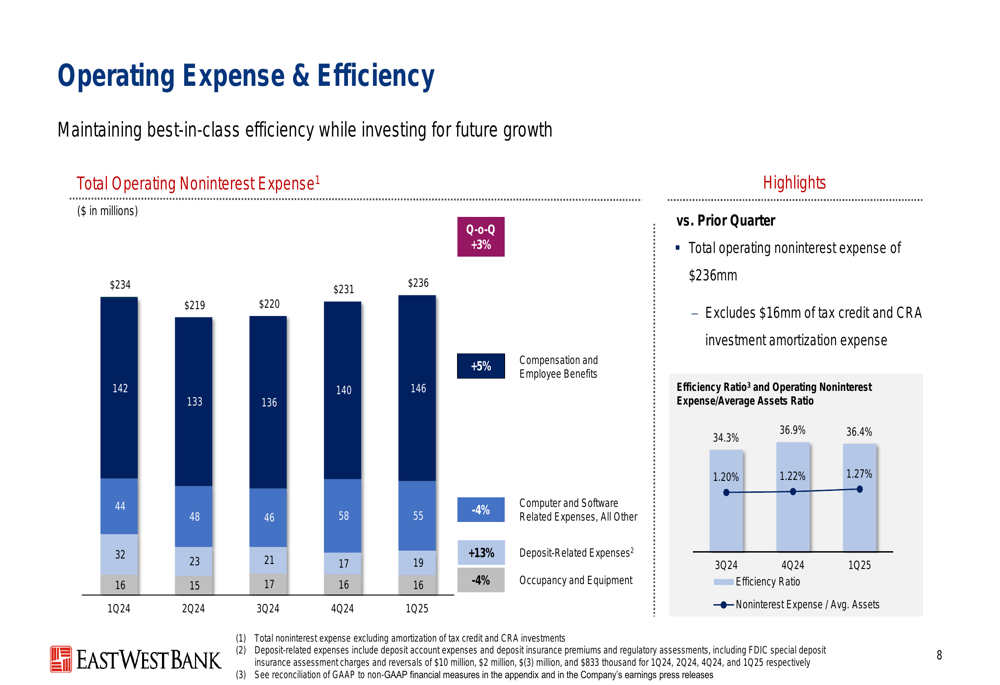

Operating expenses remained well-controlled, contributing to the bank’s strong efficiency ratio:

Total operating noninterest expense for Q1 2025 was $236 million, excluding $16 million of tax credit and CRA investment amortization expense. The efficiency ratio improved to 36.4% from Q4 2024, and the operating noninterest expense to average assets ratio decreased to 1.27%.

Asset Quality & Capital Position

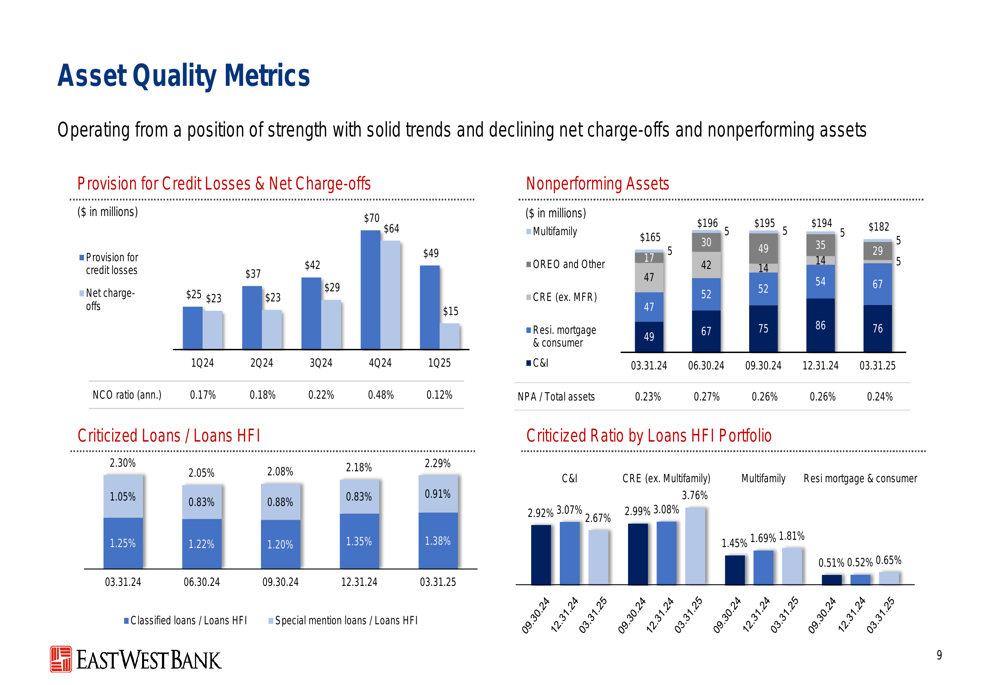

East West Bancorp maintained strong asset quality metrics in Q1 2025, with improvements in several key indicators:

Provision for credit losses was $70 million in Q1 2025, while net charge-offs were lower at $15 million. Nonperforming assets totaled $182 million as of March 31, 2025, representing 0.24% of total assets, a decrease from the previous quarter. The net charge-off ratio (annualized) was 0.12% in Q1 2025, and criticized loans to loans held for investment stood at 2.29%.

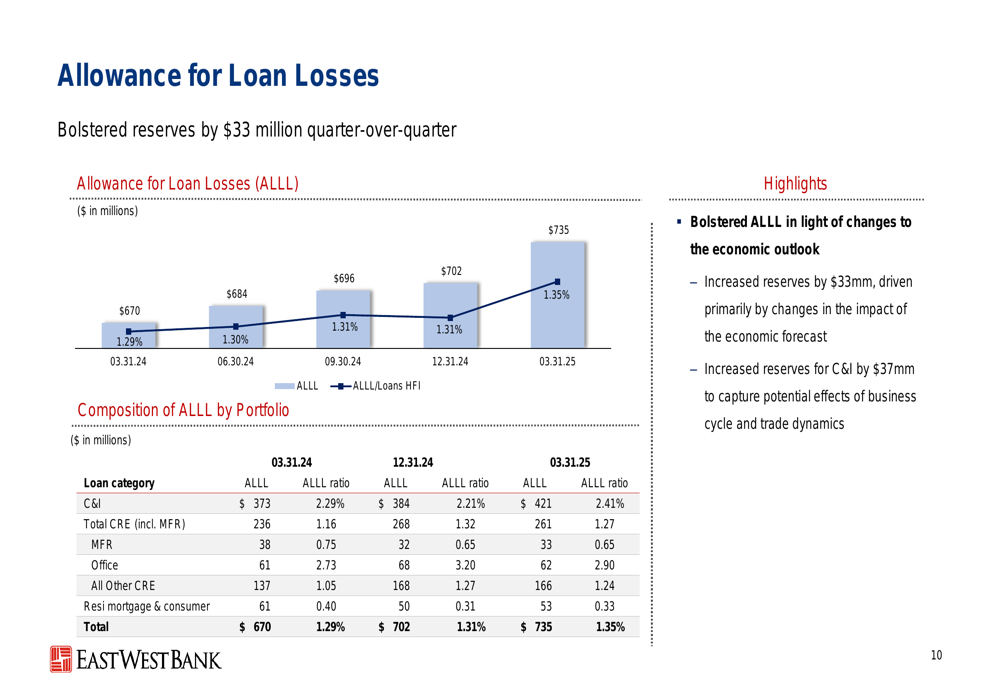

The bank bolstered its allowance for loan losses in light of changes to the economic outlook:

The allowance for loan losses increased to $735 million as of March 31, 2025, with reserves increasing by $33 million, driven primarily by changes in the impact of the economic forecast. The bank increased reserves for C&I loans by $37 million to capture potential effects of the business cycle and trade dynamics.

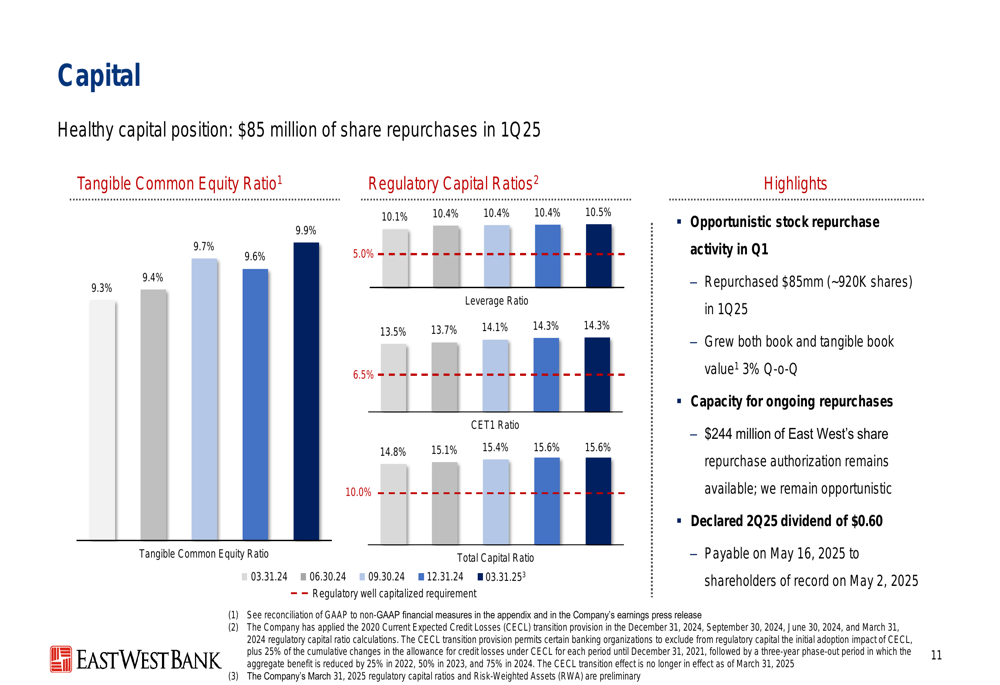

East West Bancorp maintained a healthy capital position, enabling continued shareholder returns:

The bank repurchased $85 million of shares (approximately 920,000 shares) in Q1 2025 and grew both book and tangible book value by 3% quarter-over-quarter. The tangible common equity ratio increased to 9.6% as of March 31, 2025, and regulatory capital ratios showed an upward trend. The bank declared a Q2 2025 dividend of $0.60 per share, payable on May 16, 2025, to shareholders of record on May 2, 2025.

Forward-Looking Statements

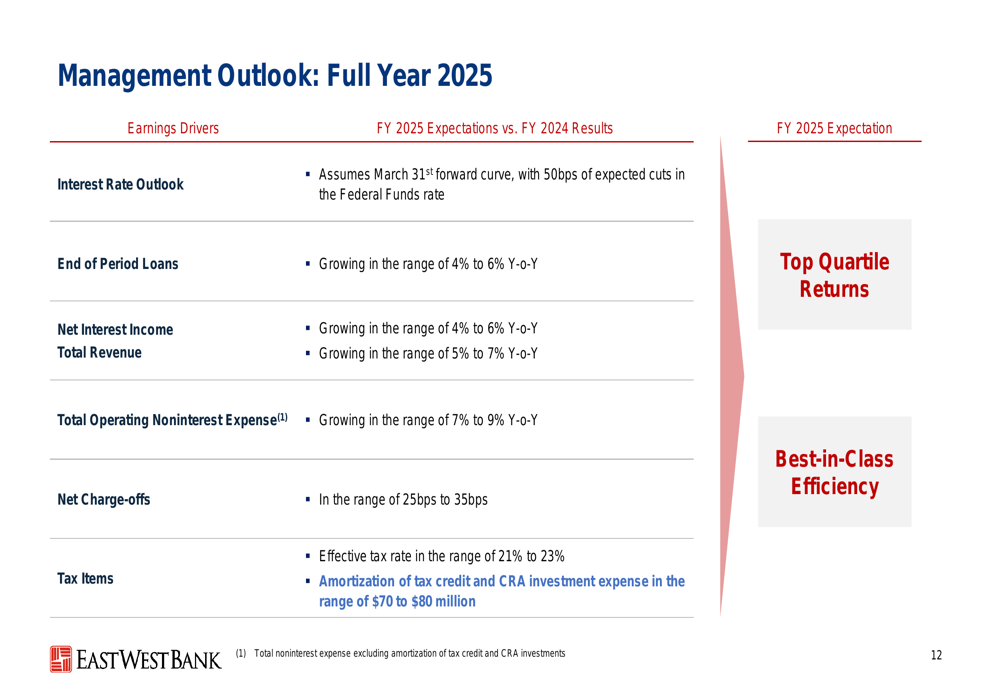

East West Bancorp’s management provided an optimistic outlook for the full year 2025, projecting growth across key metrics:

The bank’s interest rate outlook assumes the March 31st forward curve, with 50 basis points of expected cuts in the Federal Funds rate. Management expects end-of-period loans to grow in the range of 4% to 6% year-over-year, net interest income to increase by 4% to 6%, and total revenue to grow by 5% to 7%. Total operating noninterest expense is projected to rise by 7% to 9%, while net charge-offs are expected to be in the range of 25 to 35 basis points.

The bank’s effective tax rate is anticipated to be in the range of 21% to 23%, with amortization of tax credit and CRA investment expense in the range of $70 to $80 million. Management’s ultimate goal is to achieve top quartile returns and best-in-class efficiency.

This outlook represents an improvement from the previous quarter’s expectations, reflecting the bank’s confidence in its ability to navigate the current economic environment and capitalize on growth opportunities. The projected loan growth of 4-6% for FY 2025 is higher than the 2-4% growth expected in the previous quarter, indicating increased optimism about lending activity.

East West Bancorp’s strong Q1 2025 performance, combined with its healthy capital position and optimistic outlook, positions the bank well for continued success in the evolving banking landscape.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.