Oil prices push higher amid worries over Russian supply disruptions

Introduction & Market Context

EchoStar Corporation (NASDAQ:SATS) released its Q2 2025 earnings presentation on August 1, 2025, revealing mixed results across its business segments. The satellite and telecommunications company reported an overall revenue decline of 5.8% year-over-year, with its stock plummeting 16.23% to $27.30 in response to the disappointing financial performance, despite some positive metrics in its wireless business.

The sharp decline in the company’s share price indicates investors were unimpressed with EchoStar’s quarterly performance, particularly the significant 36.8% drop in Operating Income Before Depreciation and Amortization (OIBDA) and deteriorating free cash flow. This reaction came despite management’s continued commitment to achieving positive operating free cash flow for the full year 2025.

Quarterly Performance Highlights

EchoStar’s Q2 2025 presentation highlighted several key metrics across its business segments, with its wireless division emerging as the primary bright spot amid broader company challenges.

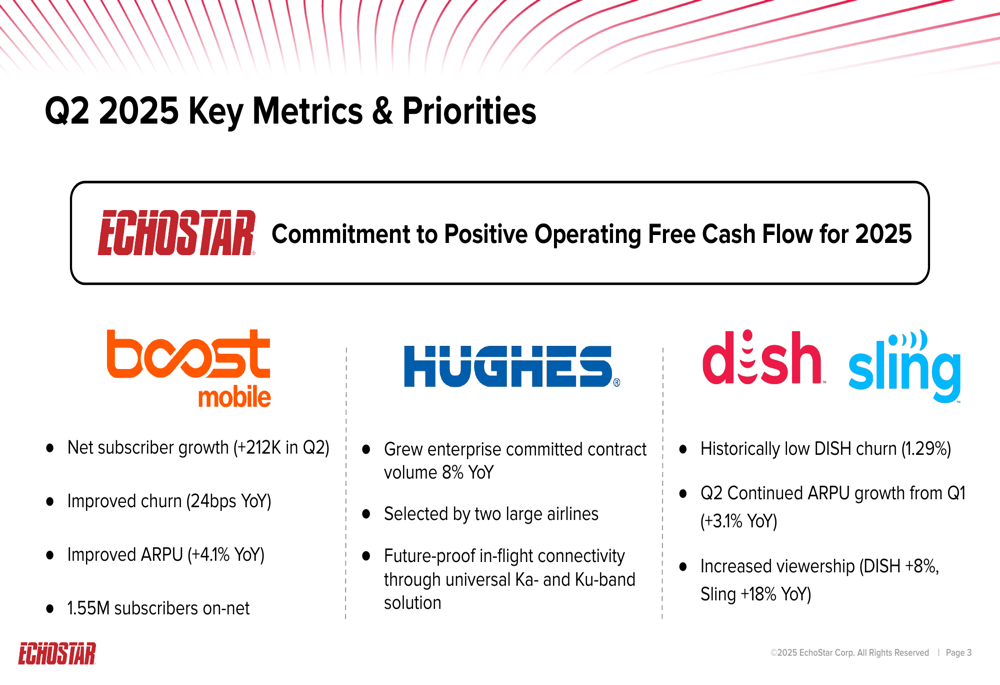

As shown in the following key metrics summary, Boost Mobile achieved substantial subscriber growth while Hughes secured important enterprise contracts:

In the wireless segment, Boost Mobile added 212,000 net subscribers during Q2, a significant improvement from the 16,000 net subscriber loss in the same period last year. The company also reported improved wireless churn (down 24 basis points year-over-year) and ARPU growth of 4.1% compared to Q2 2024.

The Hughes satellite business secured contracts with two large airlines and grew its enterprise committed contract volume by 8% year-over-year to $1.6 billion. Meanwhile, the Dish & Sling TV segment achieved historically low DISH churn of 1.29% and increased viewership metrics, with DISH up 8% and Sling up 18% year-over-year.

Detailed Financial Analysis

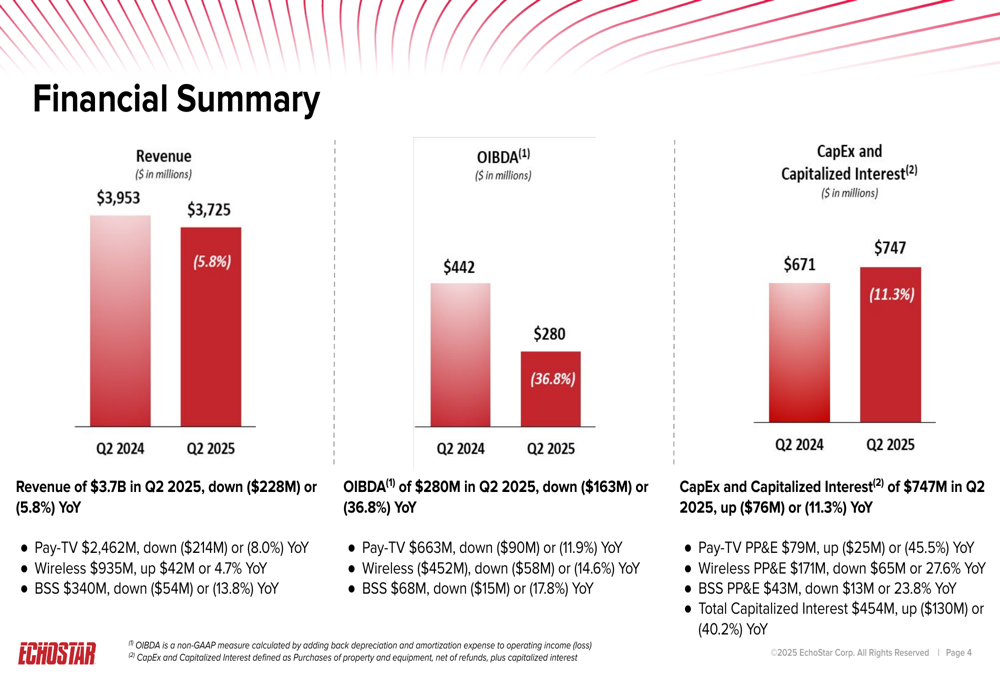

Despite these operational improvements in specific areas, EchoStar’s overall financial performance showed significant deterioration compared to the previous year. The following chart illustrates the company’s revenue, OIBDA, and capital expenditure trends:

Total (EPA:TTEF) revenue for Q2 2025 was $3.73 billion, down 5.8% from $3.95 billion in Q2 2024. This decline was primarily driven by the Pay-TV segment, which saw an 8.0% revenue drop to $2.46 billion, and the Broadband & Satellite Services (BSS) segment, which declined 13.8% to $340 million. The Wireless segment was the only bright spot, with revenue increasing 4.7% to $935 million.

OIBDA fell dramatically by 36.8% to $280 million, compared to $442 million in the prior year period. All segments contributed to this decline, with Pay-TV OIBDA down 11.9%, Wireless OIBDA down 14.6%, and BSS OIBDA down 17.8%.

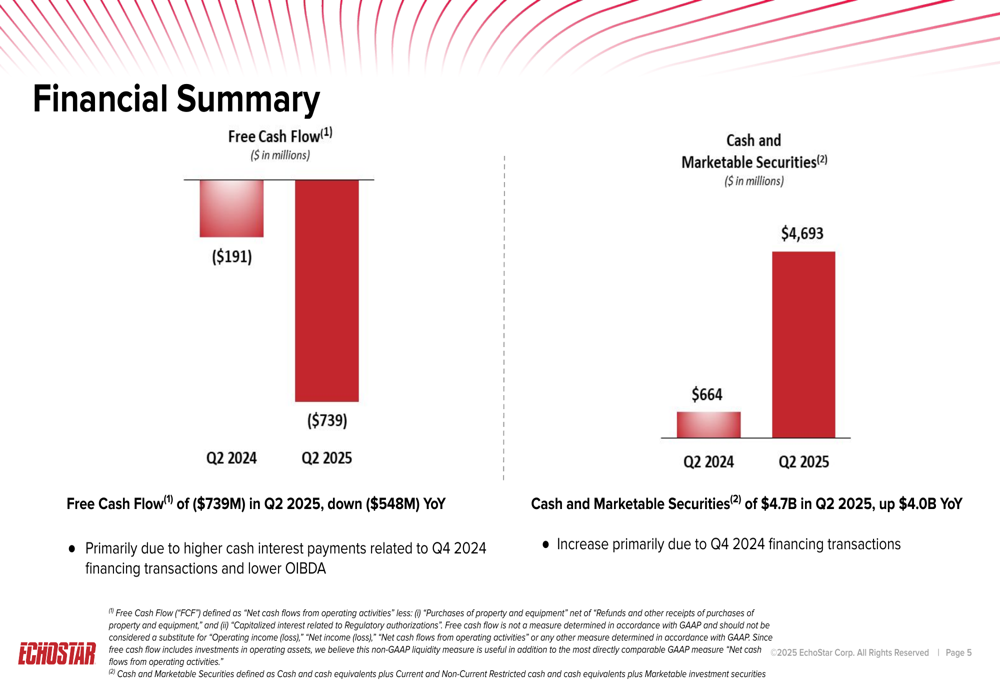

The company’s free cash flow and cash position metrics reveal a concerning trend in cash generation but a strengthened balance sheet:

Free cash flow deteriorated significantly to negative $739 million in Q2 2025, a $548 million decline from the negative $191 million reported in Q2 2024. The company attributed this primarily to higher cash interest payments related to Q4 2024 financing transactions and lower OIBDA.

On a more positive note, EchoStar’s cash and marketable securities position strengthened considerably to $4.69 billion, up $4.0 billion year-over-year, primarily due to the aforementioned financing transactions completed in late 2024.

Segment Performance Analysis

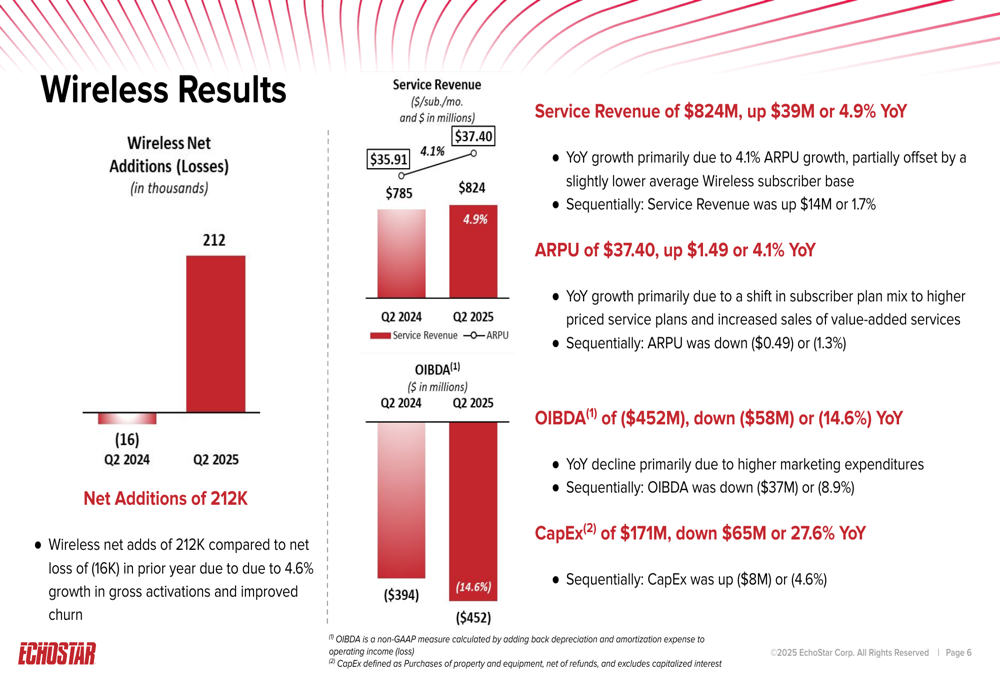

The Wireless segment showed encouraging operational metrics despite OIBDA challenges, as illustrated in the following chart:

Wireless service revenue grew 4.9% year-over-year to $824 million, driven primarily by 4.1% ARPU growth to $37.40. The segment’s net additions of 212,000 subscribers represented a substantial improvement from the 16,000 net subscriber loss in Q2 2024. However, OIBDA declined 14.6% to negative $452 million, which the company attributed to higher marketing expenditures.

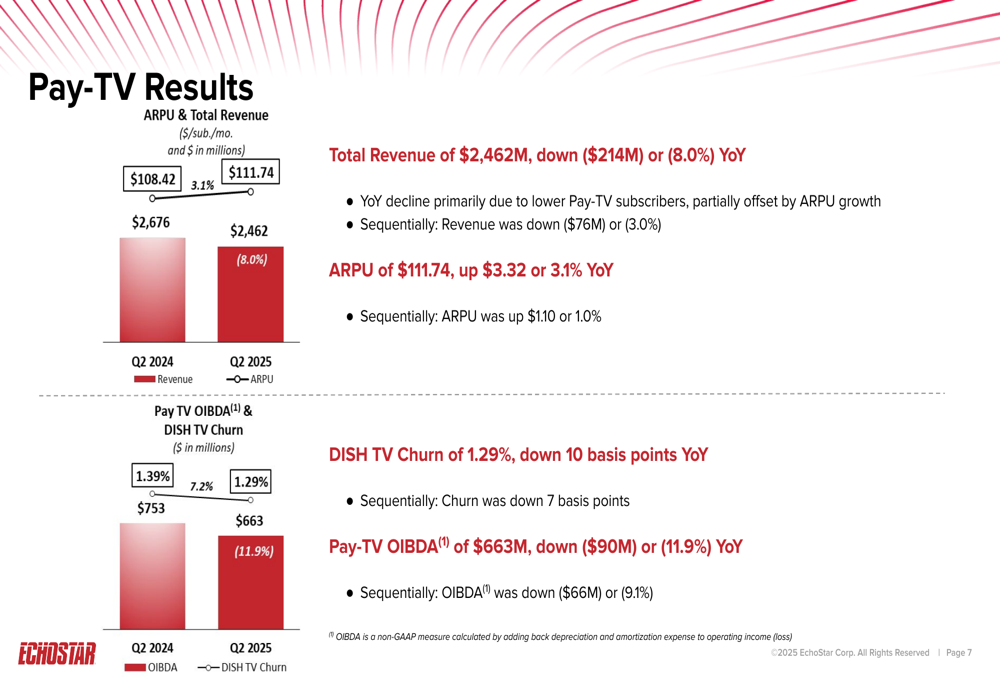

The Pay-TV segment continued its revenue decline but showed improvements in profitability metrics:

Pay-TV revenue fell 8.0% year-over-year to $2.46 billion, primarily due to lower subscriber numbers. However, ARPU increased 3.1% to $111.74, and DISH TV churn improved by 10 basis points to a historically low 1.29%. OIBDA declined 11.9% to $663 million.

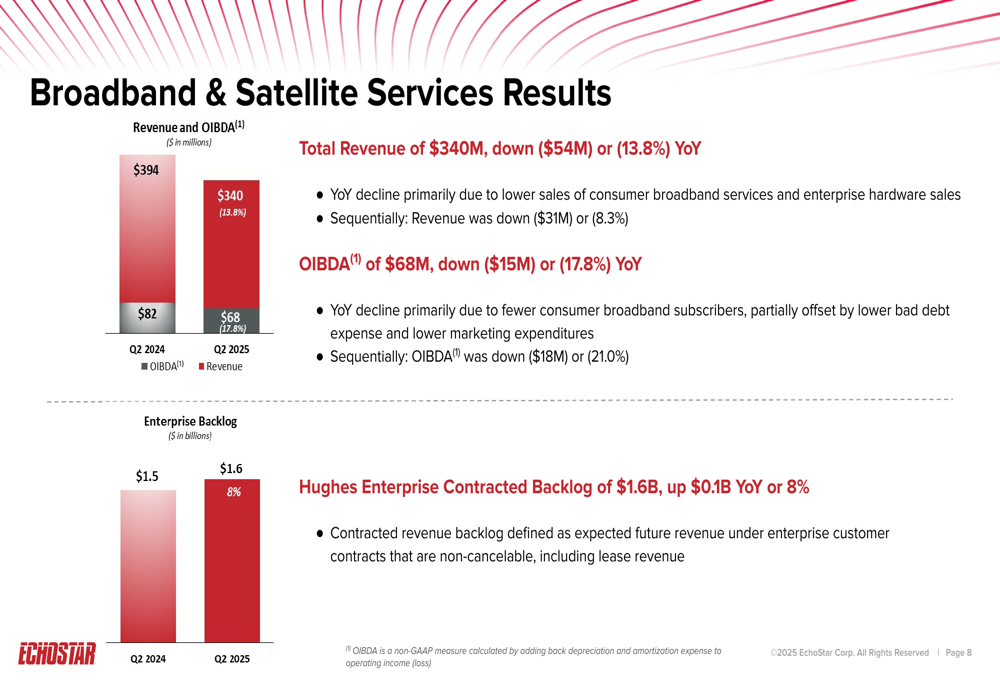

The Broadband & Satellite Services segment faced challenges but showed promise in enterprise contracts:

BSS revenue declined 13.8% to $340 million, with OIBDA falling 17.8% to $68 million. The company attributed these declines primarily to lower sales of consumer broadband services and enterprise hardware. However, the Hughes Enterprise Contracted Backlog grew 8% year-over-year to $1.6 billion, providing some optimism for future revenue stability.

Strategic Initiatives

EchoStar’s presentation emphasized several strategic priorities aimed at improving financial performance and positioning the company for future growth. The company remains committed to achieving positive operating free cash flow for the full year 2025, despite the negative free cash flow reported in Q2.

In the Wireless segment, the company continues to focus on subscriber growth and retention, with 1.55 million subscribers now on its own network. The improved churn metrics suggest these efforts are yielding results, though the higher marketing expenditures impacting OIBDA indicate significant investment is required to maintain this growth.

For the Hughes satellite business, EchoStar is emphasizing enterprise growth, particularly in the aviation sector with its "future-proof in-flight connectivity through universal Ka- and Ku-band solution." The 8% growth in enterprise contracted backlog provides evidence that this strategy is gaining traction.

In the Pay-TV segment, which continues to face secular decline, the company is focusing on maximizing profitability through ARPU growth and churn management rather than subscriber growth. The historically low churn rate of 1.29% and 3.1% ARPU growth suggest this approach is working, though it cannot fully offset the revenue impact of subscriber losses.

Forward-Looking Statements

Looking ahead, EchoStar faces significant challenges in reversing its overall revenue and OIBDA declines while improving free cash flow. The company’s commitment to positive operating free cash flow for 2025 will require substantial improvement from the negative $739 million reported in Q2.

The sharp stock price decline following the earnings release suggests investors remain skeptical about EchoStar’s ability to navigate these challenges successfully. However, the growth in wireless subscribers, improvements in Pay-TV metrics, and expansion of the Hughes enterprise backlog provide potential pathways to improved performance in future quarters.

The substantial cash position of $4.69 billion gives the company financial flexibility to invest in growth initiatives or weather continued challenges, though the higher interest payments resulting from recent financing transactions will continue to pressure free cash flow.

In its Q1 2025 earnings call, CEO Hamid Akavan had emphasized EchoStar’s unique market positioning, stating, "We are the only company that can do it all in house." The Q2 results suggest that while this integrated approach may offer long-term advantages, it has not yet translated into improved financial performance across all segments.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.