60%+ returns in 2025: Here’s how AI-powered stock investing has changed the game

Introduction & Market Context

Ecovyst Inc. (NYSE:ECVT) presented its third quarter 2025 results on November 4, revealing a strategic transformation plan centered around the divestiture of its Advanced Materials & Catalysts segment. Despite reporting strong year-over-year revenue growth of 33.1%, the company's stock declined 6.59% to close at $8.27, reflecting investor concerns over a revenue miss compared to analyst expectations and margin compression.

The company's presentation highlighted its strategic pivot to focus on its core Ecoservices business, which includes regeneration services and virgin sulfuric acid production, while exiting the Advanced Materials & Catalysts segment through a sale expected to generate approximately $530 million in net proceeds.

Strategic Initiatives

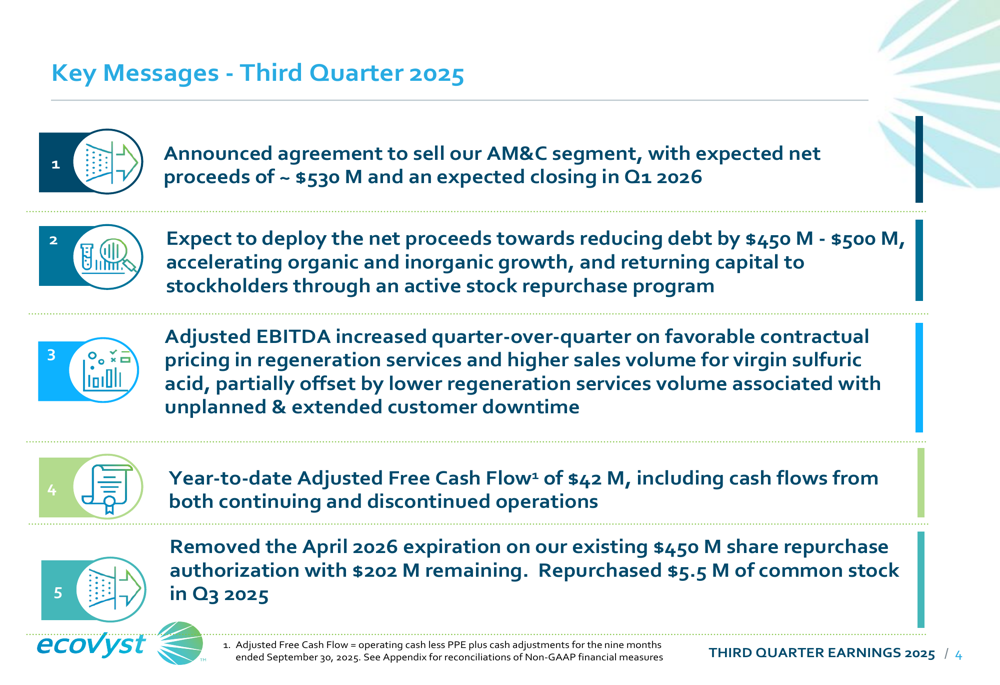

Ecovyst's most significant strategic announcement was the agreement to sell its Advanced Materials & Catalysts segment, with the transaction expected to close in Q1 2026. Management plans to deploy the proceeds primarily toward debt reduction, with $450-500 million allocated to paying down the company's term loan.

As shown in the following key messages from the presentation:

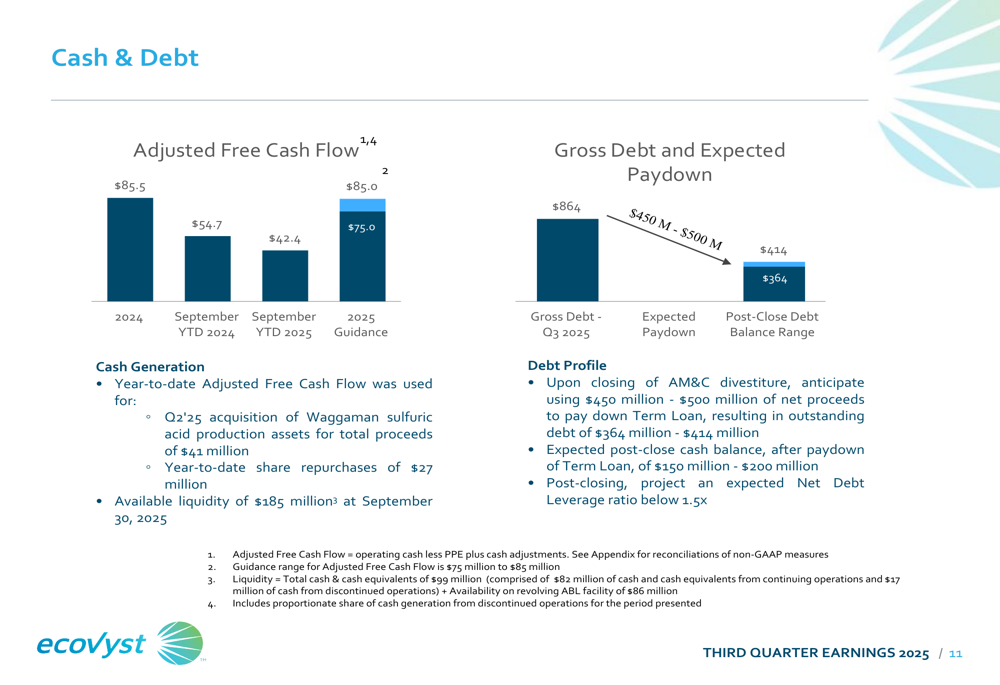

This strategic divestiture is expected to transform Ecovyst's capital structure, reducing gross debt from the current $864 million to between $364-414 million post-closing. The company projects its net debt leverage ratio will fall below 1.5x, providing significant financial flexibility.

Beyond debt reduction, management intends to accelerate organic and inorganic growth initiatives while continuing to return capital to shareholders through an active stock repurchase program. The company has $202 million remaining on its share repurchase authorization and repurchased $5.5 million of common stock in Q3 2025.

The following slide illustrates the planned debt reduction and expected post-closing financial position:

Quarterly Performance Highlights

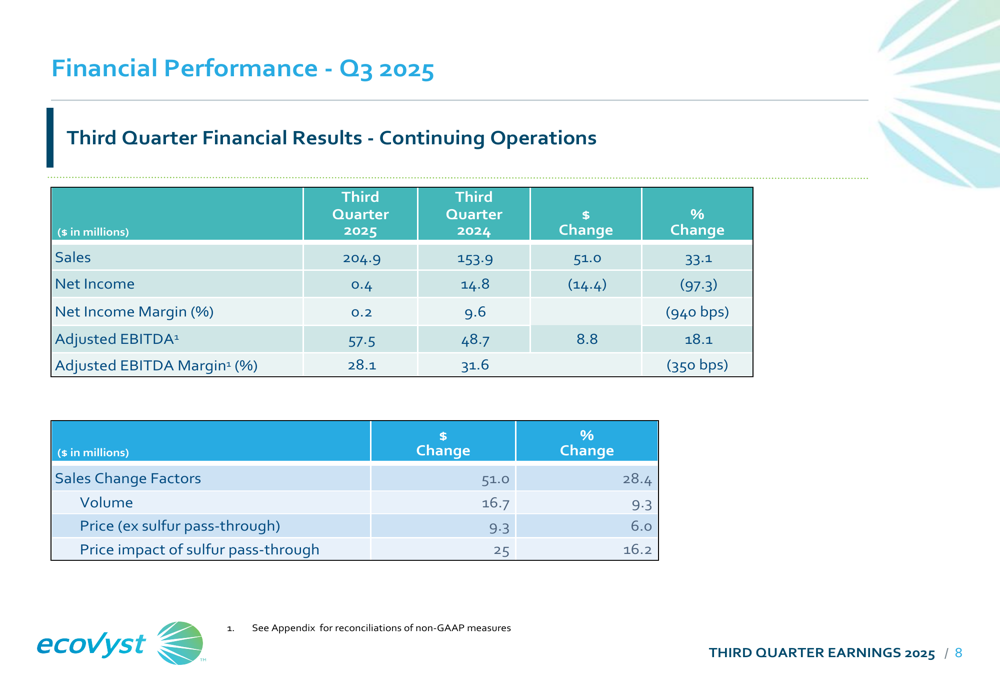

Ecovyst reported Q3 2025 sales of $204.9 million, representing a 33.1% increase from the prior year period. This growth was driven by a combination of volume growth (9.3%), price increases excluding sulfur pass-through (6.0%), and the impact of sulfur pass-through (16.2%).

The company's key financial metrics for the quarter are summarized below:

Adjusted EBITDA for the quarter reached $57.5 million, an 18.1% increase year-over-year, though the adjusted EBITDA margin contracted to 28.1% from 31.6% in Q3 2024. This margin compression was primarily attributed to the mechanical effect of higher sulfur costs passed through to customers, which increases revenue without a corresponding increase in EBITDA.

The detailed financial comparison with the prior year quarter shows the magnitude of growth across key metrics:

Detailed Financial Analysis

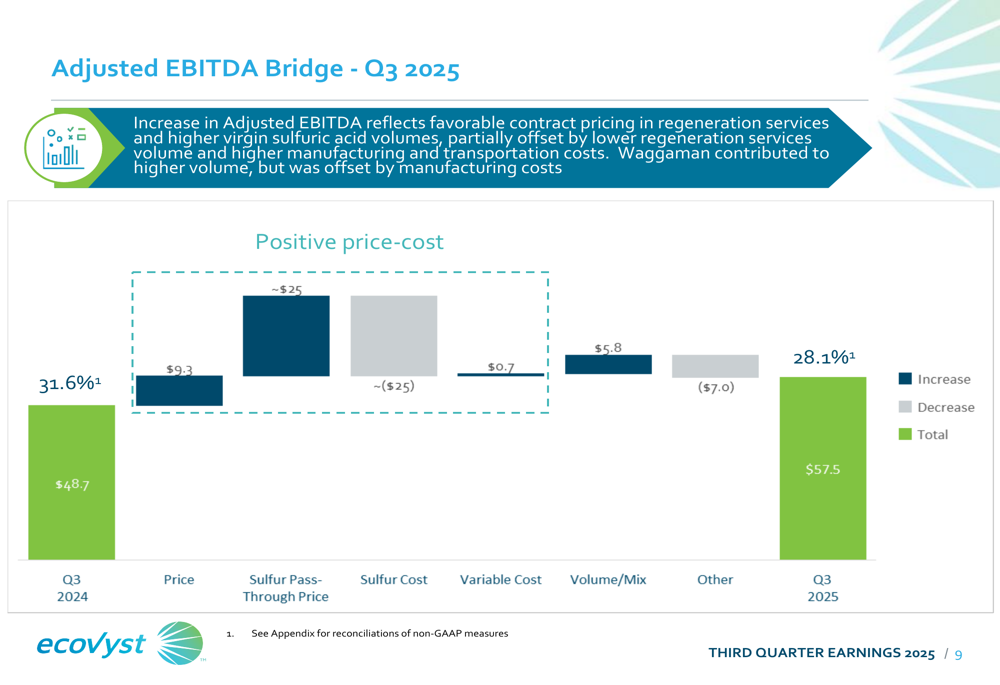

The drivers behind Ecovyst's adjusted EBITDA performance are clearly illustrated in the bridge analysis below, which shows how various factors contributed to the year-over-year change:

Price increases contributed $9.3 million to adjusted EBITDA growth, while volume and mix improvements added another $5.8 million. The sulfur pass-through mechanism had a neutral impact on EBITDA (approximately +$25 million in price offset by -$25 million in cost), while "Other" factors, including higher manufacturing and transportation costs, reduced EBITDA by $7.0 million.

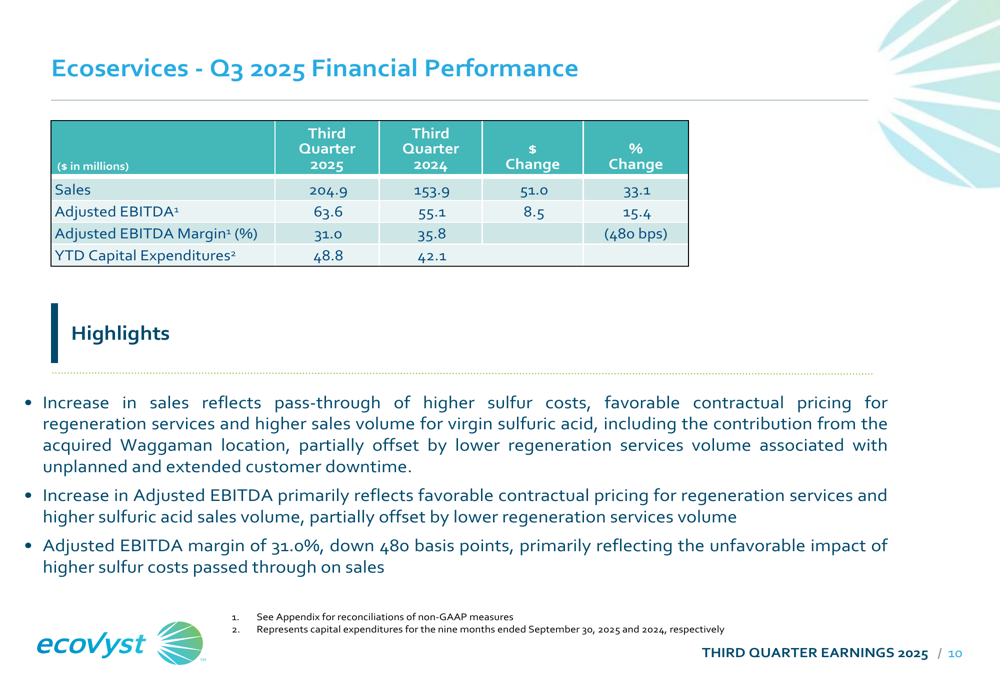

The Ecoservices segment, which represents Ecovyst's continuing operations following the planned AM&C divestiture, delivered sales of $204.9 million and adjusted EBITDA of $63.6 million, with a 31.0% margin. This represents a 480 basis point margin decline from Q3 2024, primarily due to the impact of higher sulfur costs passed through on sales.

The segment's performance was detailed as follows:

Management noted that while regeneration services volume was negatively impacted by unplanned and extended customer downtime, this was partially offset by favorable contractual pricing and higher virgin sulfuric acid volumes, including the contribution from the recently acquired Waggaman location.

Forward-Looking Statements

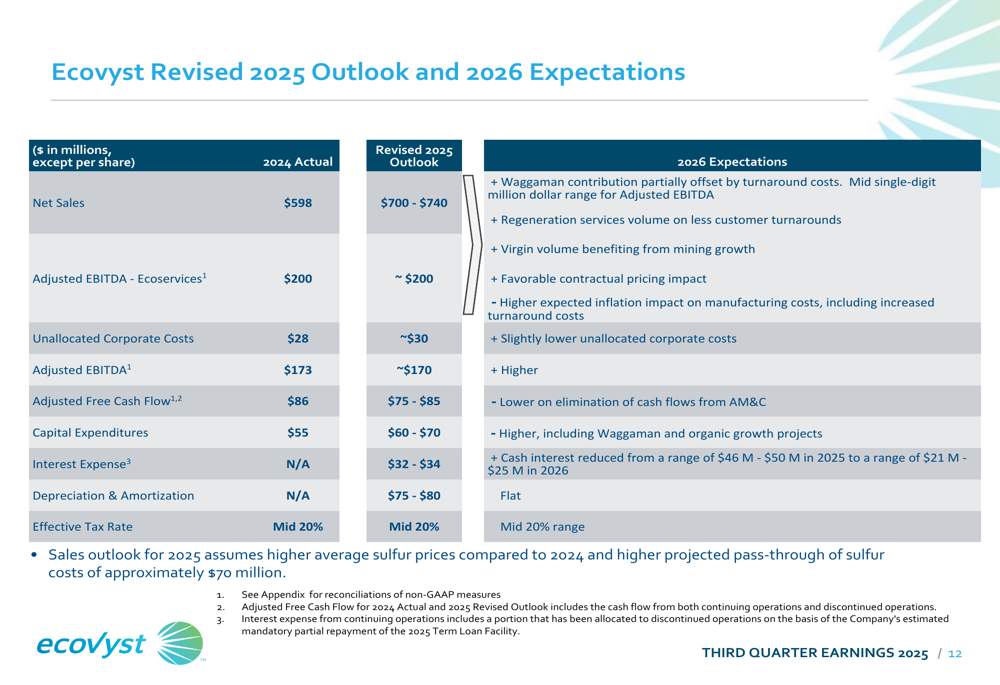

Ecovyst provided an updated outlook for 2025 and preliminary expectations for 2026, reflecting both the continuing operations and the impact of the planned AM&C divestiture:

For 2025, the company expects:

- Sales of $700-740 million

- Adjusted EBITDA of approximately $170 million

- Adjusted free cash flow of $75-85 million

- Capital expenditures of $60-70 million

Looking ahead to 2026, Ecovyst anticipates higher adjusted EBITDA driven by the Waggaman contribution, regeneration services volume recovery, virgin volume growth from mining applications, and favorable contractual pricing. However, adjusted free cash flow is expected to decline due to the elimination of cash flows from the divested AM&C segment.

Interest expense is projected to decrease significantly in 2026, from $32-34 million in 2025 to $21-25 million, reflecting the substantial debt reduction following the AM&C divestiture.

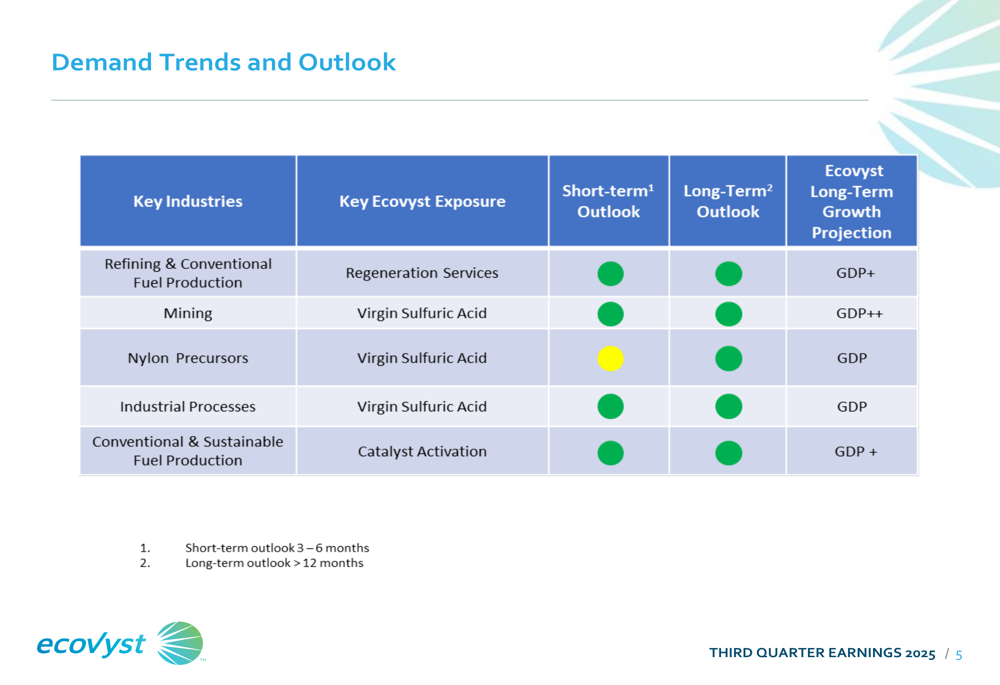

The company's demand outlook remains positive across its key industries, with particularly strong prospects in mining applications:

Summary and Outlook

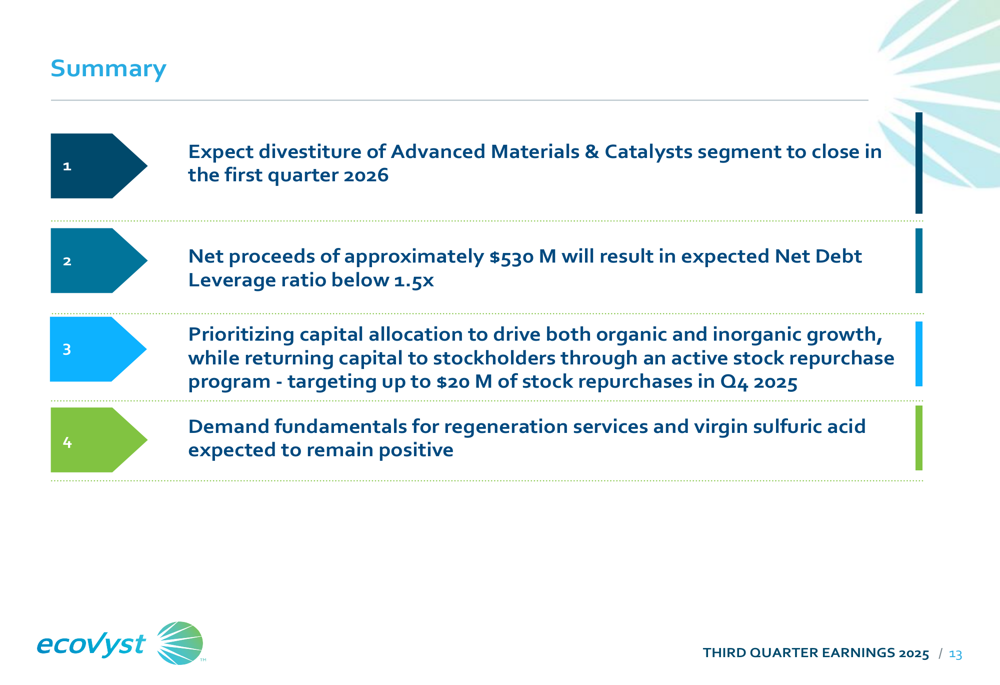

Ecovyst's third quarter presentation emphasized four key takeaways that summarize the company's current position and strategic direction:

Despite the positive long-term outlook and strategic transformation, investors appeared to focus on the near-term challenges, including the revenue miss versus analyst expectations and margin compression. The stock's 6.59% decline on the day of the presentation suggests the market is taking a cautious approach to the company's transformation.

Management remains confident in the fundamentals of its core businesses, highlighting strong demand for regeneration services and virgin sulfuric acid, particularly in mining applications where the company expects growth to exceed GDP. With the planned debt reduction and streamlined focus on Ecoservices, Ecovyst is positioning itself for potentially improved financial performance in 2026 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.