Microsoft’s data-center shortages to persist longer than expected - Bloomberg

Introduction & Market Context

EDP Energias de Portugal (OL:EDP) presented its first-quarter 2025 results on May 9, showing strong financial performance driven primarily by its flexible generation assets in Iberia. The company benefited from favorable hydro conditions and high European gas prices during the quarter, positioning it well to achieve its full-year targets.

The Portuguese utility continues to execute its strategic focus on renewable energy expansion while maintaining disciplined cost management. The company’s performance comes amid an energy landscape increasingly characterized by the need for flexible generation assets to balance growing solar penetration in the Iberian market.

Quarterly Performance Highlights

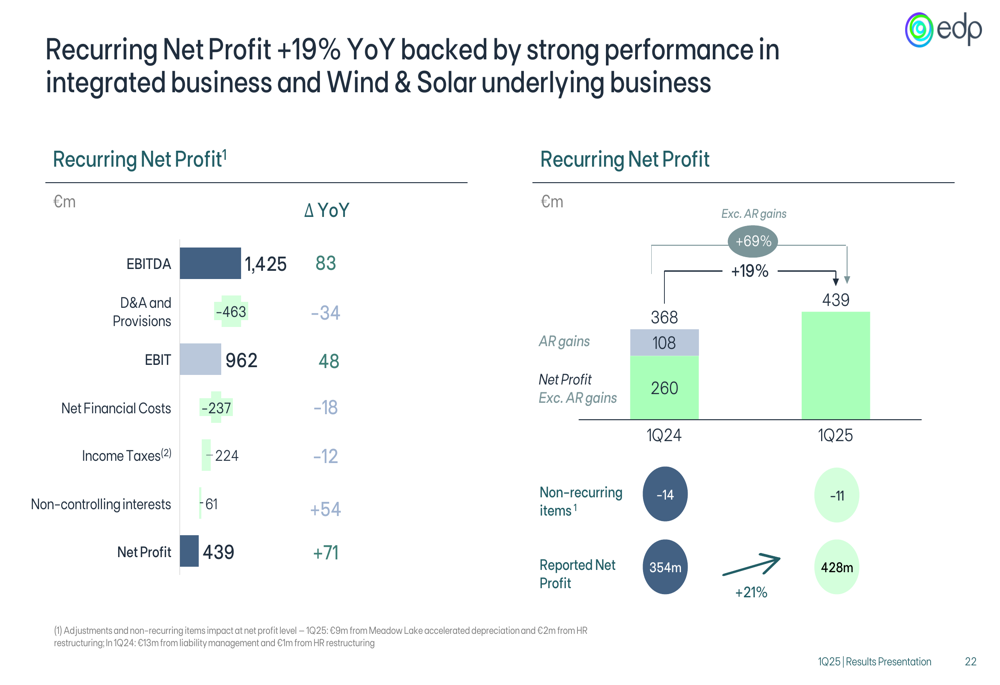

EDP reported a 19% year-over-year increase in recurring net profit, reaching €0.4 billion for Q1 2025. This growth was primarily driven by strong performance in the company’s flexible generation assets in Iberia, despite the absence of asset rotation gains compared to the same period last year.

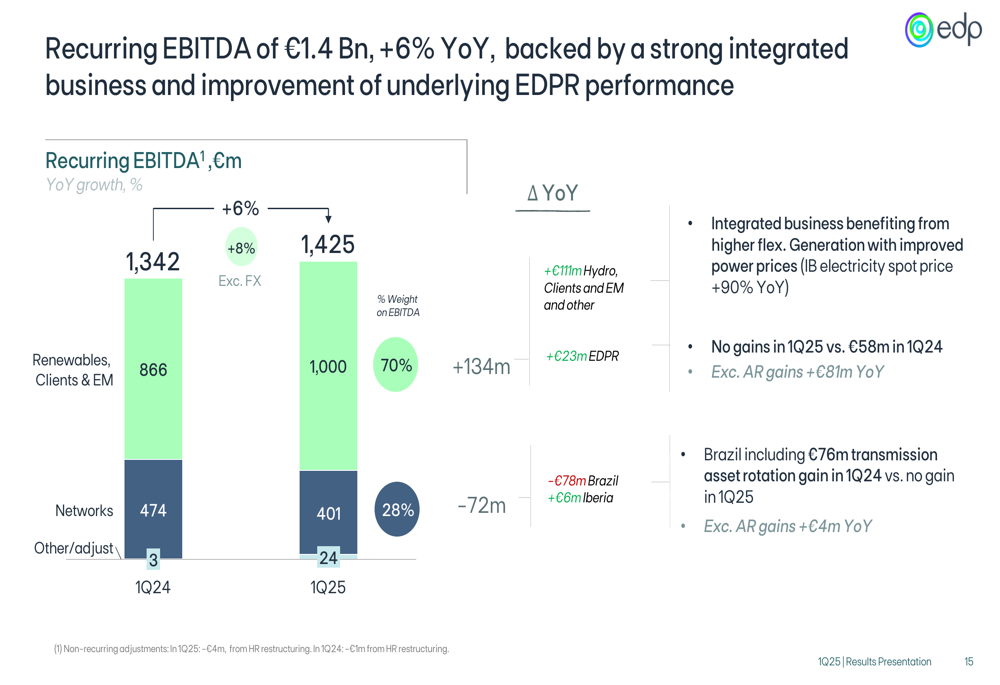

Recurring EBITDA grew 6% year-over-year to €1.4 billion, with the Renewables, Clients & Energy Management segment contributing 70% of the total. The company’s Wind & Solar division saw a 20% EBITDA increase excluding asset rotation gains, supported by new capacity added in Q4 2024.

As shown in the following chart detailing EDP’s recurring EBITDA breakdown:

The Networks segment, which accounted for 28% of EBITDA, showed resilient underlying performance with 7% growth excluding gains and foreign exchange impacts. However, reported Networks EBITDA declined from €474 million in Q1 2024 to €401 million in Q1 2025, primarily due to the absence of asset rotation gains from transmission assets in Brazil that were present in the previous year.

Detailed Financial Analysis

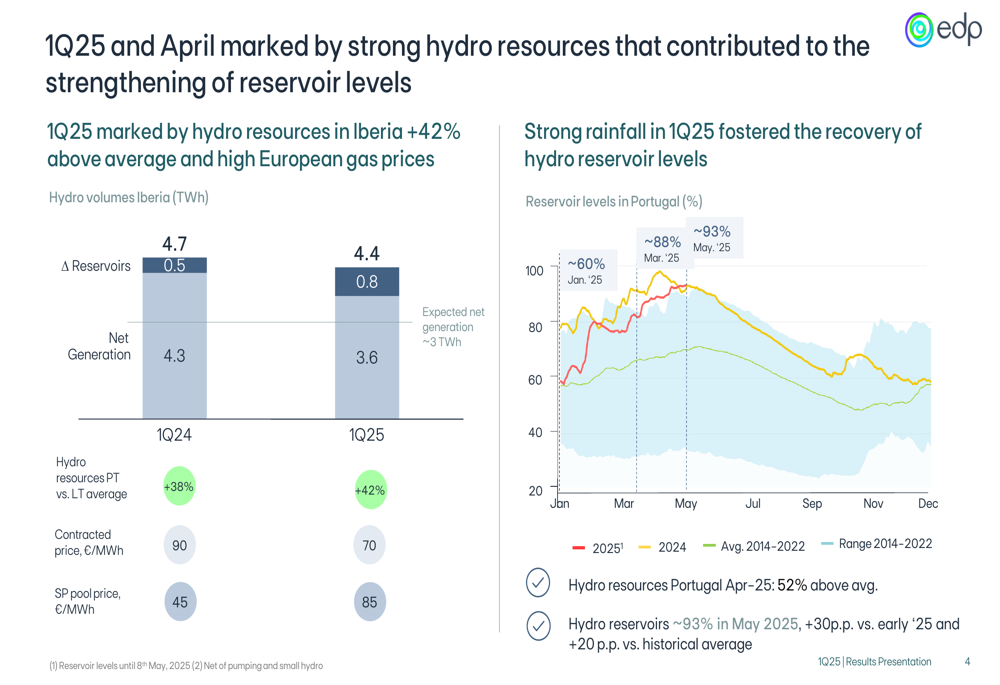

The company’s strong Q1 performance was significantly influenced by favorable hydro conditions in Iberia, with resources 42% above the long-term average. This contributed to high reservoir levels, reaching approximately 93% in May 2025, which is 30 percentage points higher than at the beginning of the year and 20 percentage points above the historical average.

The following chart illustrates the hydro resources and reservoir levels:

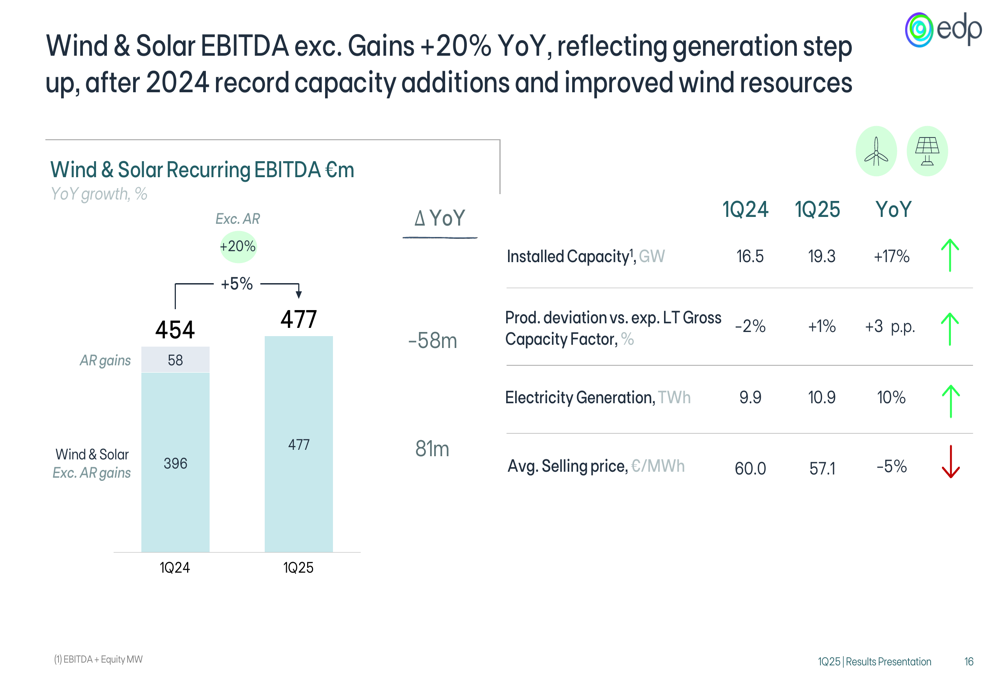

EDP’s Wind & Solar division continued its growth trajectory, with installed capacity increasing 17% year-over-year to 19.3 GW in Q1 2025. Electricity generation from these assets rose 10% to 10.9 TWh, though average selling prices decreased 5% to €57.1/MWh.

The detailed performance of the Wind & Solar segment is shown below:

The Generation & Supply business in Iberia showed particularly strong results, with EBITDA increasing 27% year-over-year to €523 million. This performance was driven by the company’s flexible generation assets, which benefited from a 90% increase in electricity spot prices in the Iberian market (OMIE), rising from €45/MWh in Q1 2024 to €85/MWh in Q1 2025.

EDP has maintained strong cost discipline, with recurring operating expenses decreasing from €0.48 billion in Q1 2023 to €0.46 billion in Q1 2025, despite a 10% increase in installed capacity. The company has also reduced its workforce from 13,300 employees in Q1 2023 to 12,400 in Q1 2025, demonstrating its focus on operational efficiency.

Strategic Initiatives

EDP continues to execute its strategic focus on expanding its renewable energy portfolio while investing in electricity networks. The company confirmed it is on track to add 2 GW of new renewable capacity in 2025, with limited execution risk related to supply chain issues or US import tariffs.

In the networks business, EDP has proposed a 50% increase in high-voltage and medium-voltage investments in Portugal for the 2026-2030 period, rising from €1.0 billion to €1.5 billion. The company noted that the Portuguese regulator ERSE has calculated this would have a limited impact of +0.7% on end-user electricity prices by 2030.

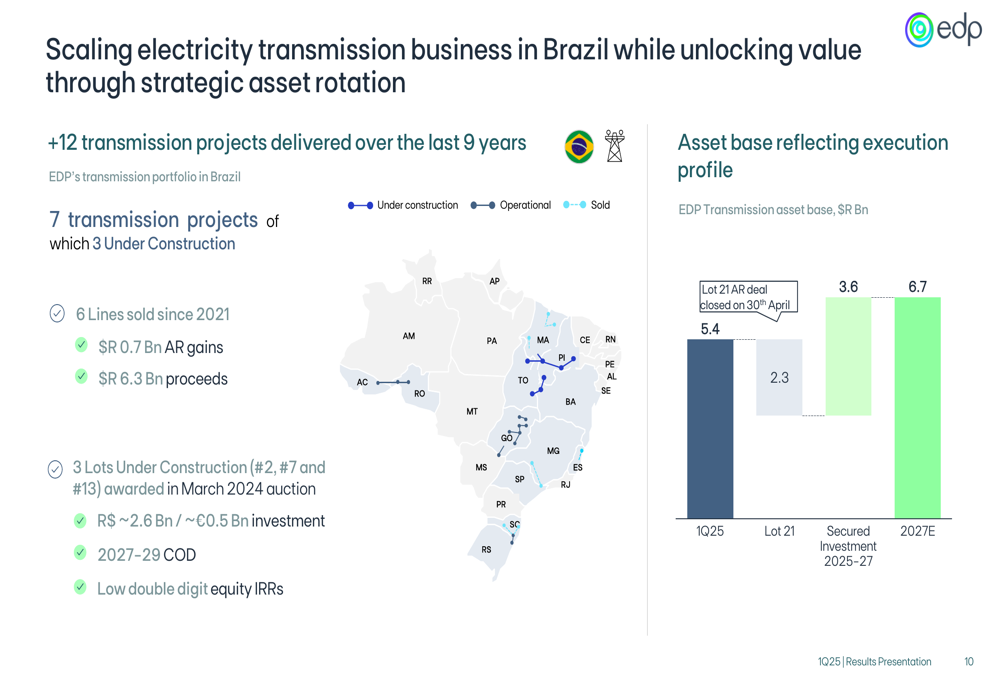

In Brazil, EDP is scaling its electricity transmission business while unlocking value through strategic asset rotation. The company has delivered 12 transmission projects over the last nine years and expects its transmission asset base to grow from R$5.4 billion in Q1 2025 to R$6.7 billion by 2027.

The company’s strategy for its transmission business in Brazil is illustrated below:

Forward-Looking Statements

For the full year 2025, EDP has maintained its guidance of approximately €4.8 billion in recurring EBITDA, €1.2 billion in recurring net profit, and €16 billion in net debt. This outlook is supported by structural improvements in flexible generation activities, above-average hydro generation in Q1 and April, high reservoir levels, and increased contribution from new renewable capacity.

The company expects lower asset rotation gains compared to 2024 and anticipates a weaker USD and BRL against the EUR. The net debt guidance assumes approximately €2 billion in asset rotation proceeds and €1 billion in tax equity proceeds.

EDP’s recurring net profit performance and outlook are summarized in the following chart:

EDP also announced it will hold a Capital Markets Day in November 2025 to provide a strategic update for the period beyond 2026, signaling the company’s continued focus on long-term planning and transparent communication with investors.

In closing remarks, management emphasized the sound Q1 2025 results supported by strong underlying performance, positive outlook for the integrated business in Iberia, resilient electricity networks with significant investment opportunities, good visibility on 2025 renewable capacity additions, and solid visibility supporting the 2025 outlook.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.