Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

EDP Renewables (EDPR) presented its first half 2025 results on July 30, 2025, highlighting operational growth that helped offset pricing pressures in key markets. The company’s stock has shown resilience, with shares trading at €10.10, up 1% following the presentation, according to available market data.

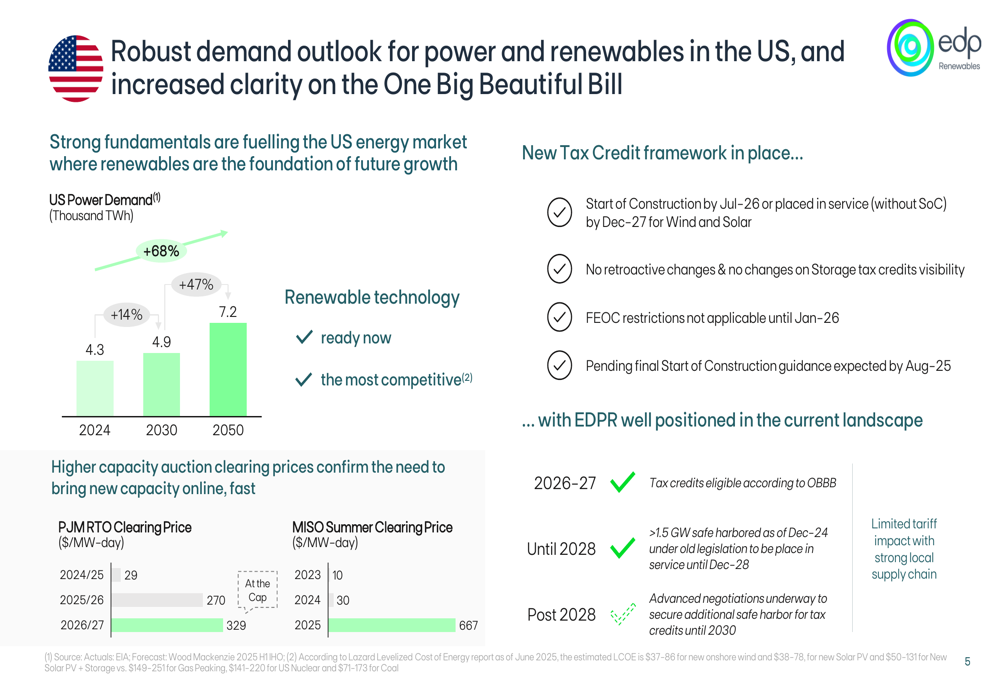

The renewable energy provider operates in a market characterized by robust demand growth, particularly in the United States, where power demand is projected to increase 68% by 2050, reaching 7.2 thousand TWh from 4.3 thousand TWh in 2024. This favorable long-term outlook provides a supportive backdrop for EDPR’s expansion strategy.

As shown in the following chart detailing the US market outlook and tax credit framework:

In Europe, the company highlighted the European Commission’s efforts to advance grid reforms and enhance industrial resilience through initiatives like the European Grids Package and the Net-Zero Industry Act, creating additional opportunities for renewable energy providers.

Operational Performance Highlights

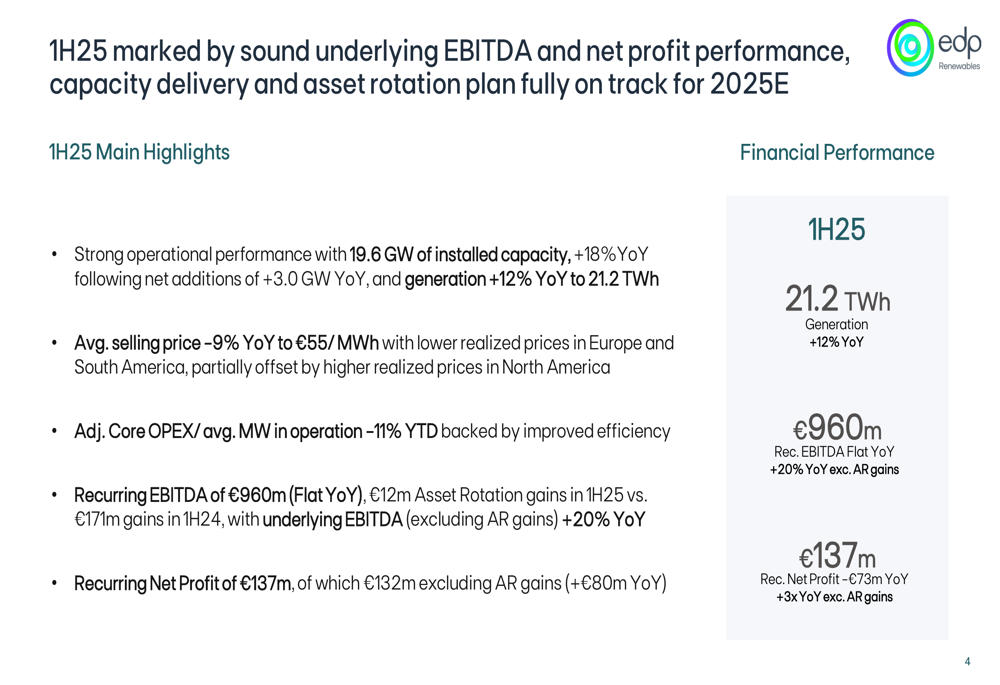

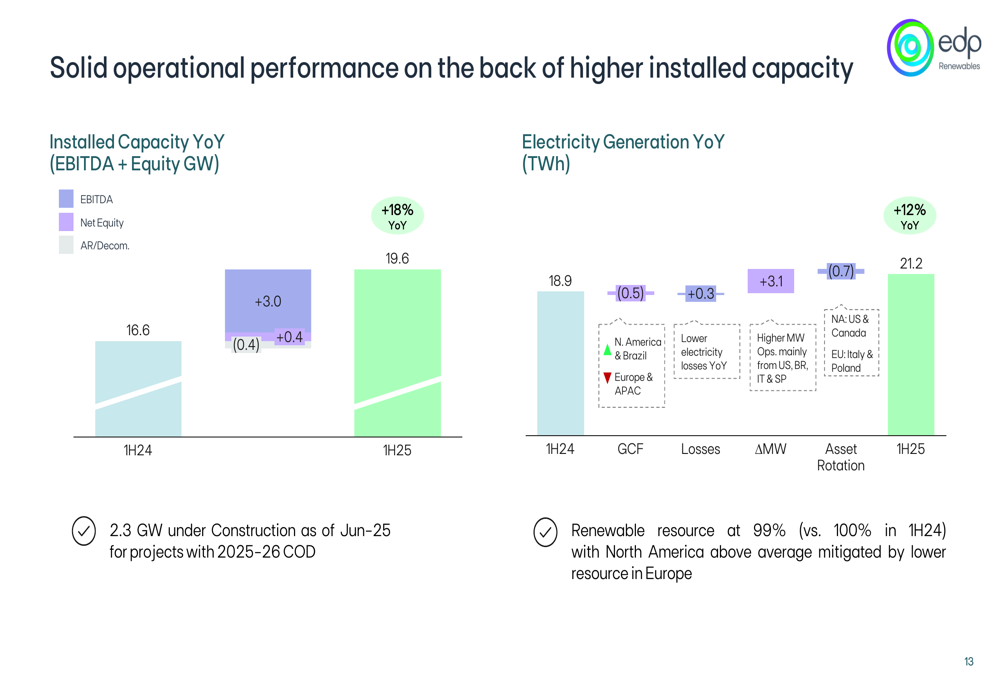

EDPR reported solid operational metrics for the first half of 2025, with installed capacity reaching 19.6 GW, an 18% increase year-over-year. Electricity generation grew by 12% to 21.2 TWh, demonstrating the company’s expanding operational footprint.

The following slide summarizes EDPR’s key performance indicators for 1H25:

Despite the growth in generation, EDPR faced headwinds from lower average selling prices, which declined 9% year-over-year to €55/MWh. This pricing pressure was partially offset by operational efficiency improvements, with adjusted core OPEX per average MW decreasing by 11% year-to-date.

The company’s operational performance is illustrated in the following chart showing the growth in installed capacity and generation:

Financial Results Analysis

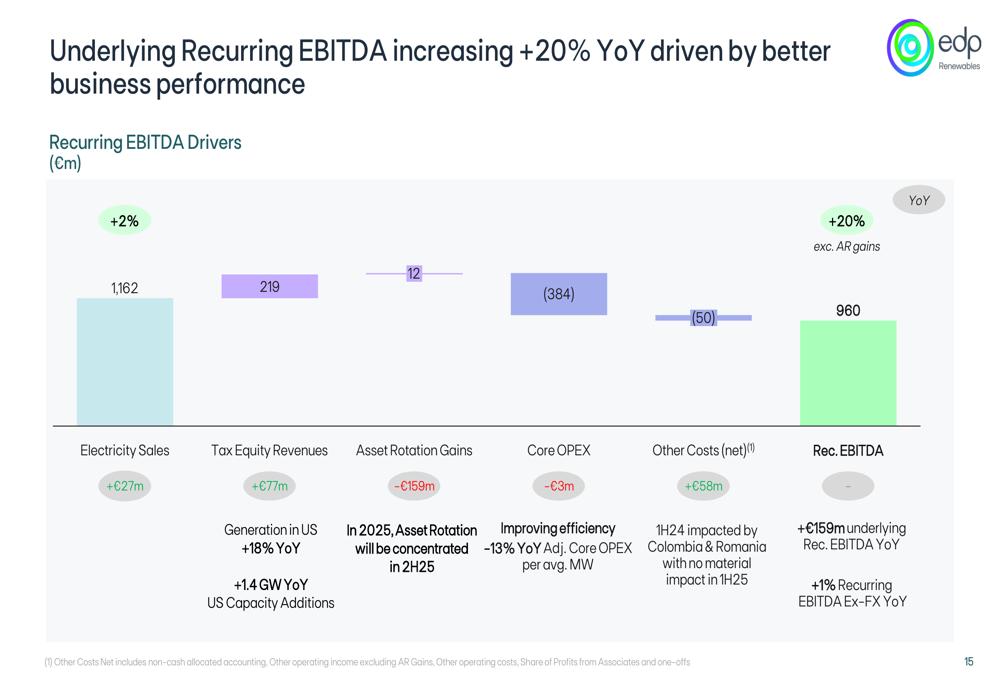

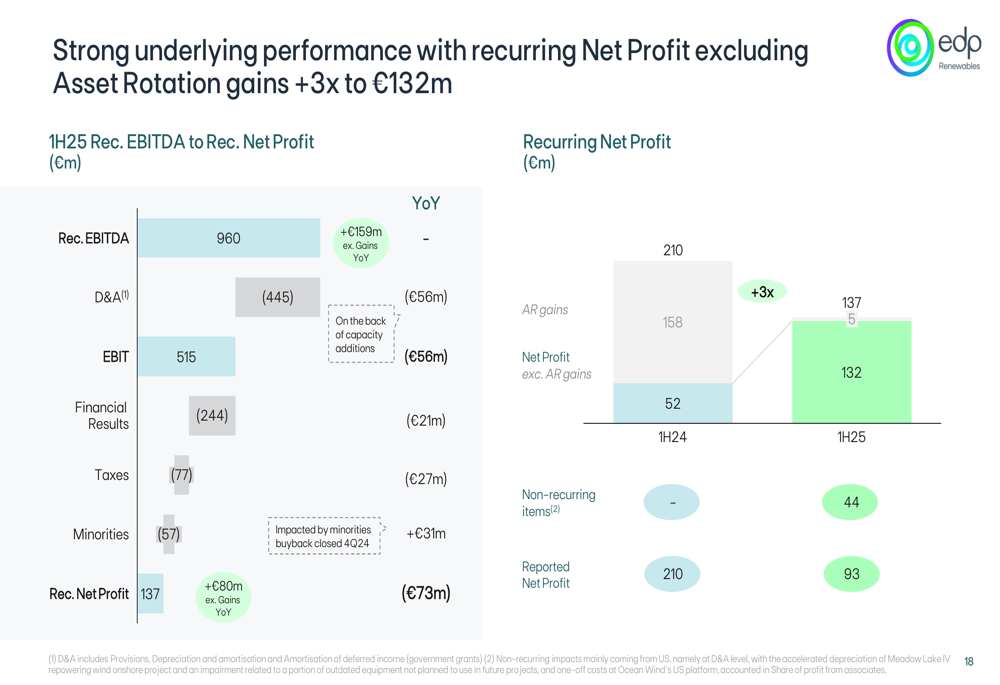

EDPR reported recurring EBITDA of €960 million for 1H25, which remained flat year-over-year. However, when excluding asset rotation gains, recurring EBITDA increased by 20% year-over-year, demonstrating strong underlying business performance.

The drivers behind EDPR’s recurring EBITDA performance are detailed in this bridge analysis:

More impressively, recurring net profit excluding asset rotation gains increased threefold to €132 million, highlighting the company’s improved profitability despite challenging market conditions. The comprehensive bridge from EBITDA to net profit shows the various components affecting the bottom line:

Total electricity sales increased by 2% year-over-year to €1,162 million, with the 12% growth in generation partially offset by the 9% decrease in average selling price. The company’s financial results also benefited from a €21 million year-over-year improvement in financial results, despite a €1.7 billion increase in nominal financial debt.

Strategic Initiatives & Asset Rotation

EDPR continues to execute its asset rotation strategy, with approximately €0.7 billion already closed or signed and an additional €1.3 billion under binding bids for 2025. The company emphasized strong demand for these assets, with attractive sales multiples averaging €1.5 million EV/MW.

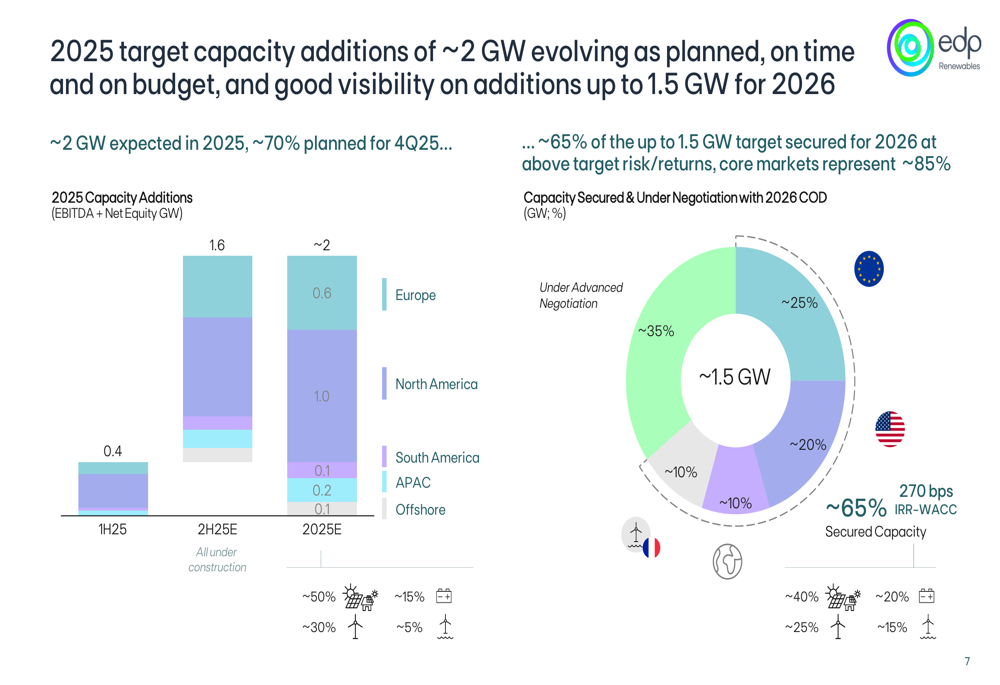

The company’s 2025 target for capacity additions remains at approximately 2 GW, which management reports is progressing on time and on budget. Additionally, EDPR has good visibility on additions of up to 1.5 GW for 2026, with approximately 65% of this target already secured at above-target risk/return profiles.

The following slide details EDPR’s progress on its 2025 capacity addition targets:

Total investments for 1H25 decreased by 25% to €1.1 billion compared to €1.5 billion in 1H24, reflecting a more focused capital allocation approach. The company continues to improve efficiency, with adjusted annualized core OPEX per average MW in operation decreasing from €46.4 in FY24 to €41.3 in 1H25, while also reducing its workforce from 2,935 to 2,883 employees.

Forward-Looking Statements

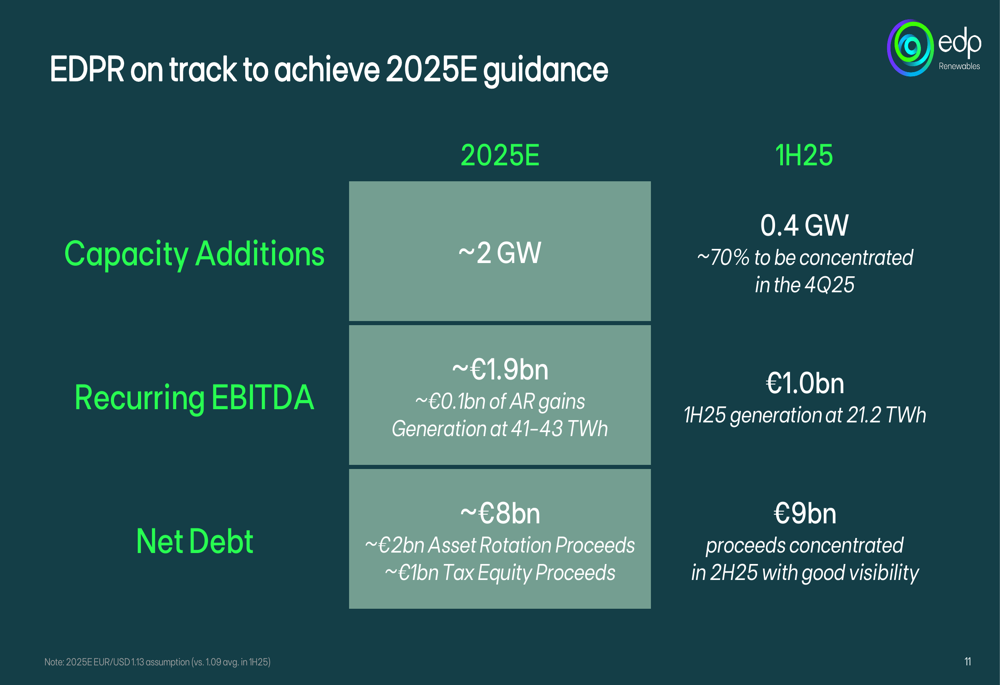

EDPR maintained its 2025 guidance, targeting recurring EBITDA of approximately €1.9 billion (including €0.1 billion of asset rotation gains), generation of 41-43 TWh, and net debt of approximately €8 billion. The company expects to achieve these targets through continued operational growth, efficiency improvements, and proceeds from asset rotation (€2 billion) and tax equity (€1 billion).

The following slide compares EDPR’s 2025 targets with its 1H25 results:

Management expressed confidence in meeting these targets, noting that while only 0.4 GW of capacity additions were completed in 1H25, approximately 70% of the planned 2 GW additions for 2025 are expected to be concentrated in the fourth quarter. Similarly, asset rotation proceeds are expected to be concentrated in the second half of 2025, which should help reduce net debt from the current €9 billion level.

In summary, EDPR’s 1H25 results demonstrate operational resilience in a challenging price environment, with strong underlying performance when excluding asset rotation gains. The company remains on track to achieve its 2025 targets, supported by continued efficiency improvements and strategic asset rotation initiatives.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.