JFrog stock rises as Cantor Fitzgerald maintains Overweight rating after strong Q2

Introduction & Market Context

eHealth , Inc. (NASDAQ:EHTH) released its Q1 2025 financial results on May 7, 2025, showcasing significant improvement across key metrics and a return to profitability. The company’s stock, which closed at $4.68 on May 6, saw a substantial 11.75% jump to $5.23 in premarket trading, indicating positive investor reaction to the results.

The online health insurance marketplace reported strong performance amid favorable industry conditions, including positive announcements on 2026 Medicare Advantage reimbursement rates and final Medicare rules that the company views as beneficial for the industry.

Q1 2025 Financial Highlights

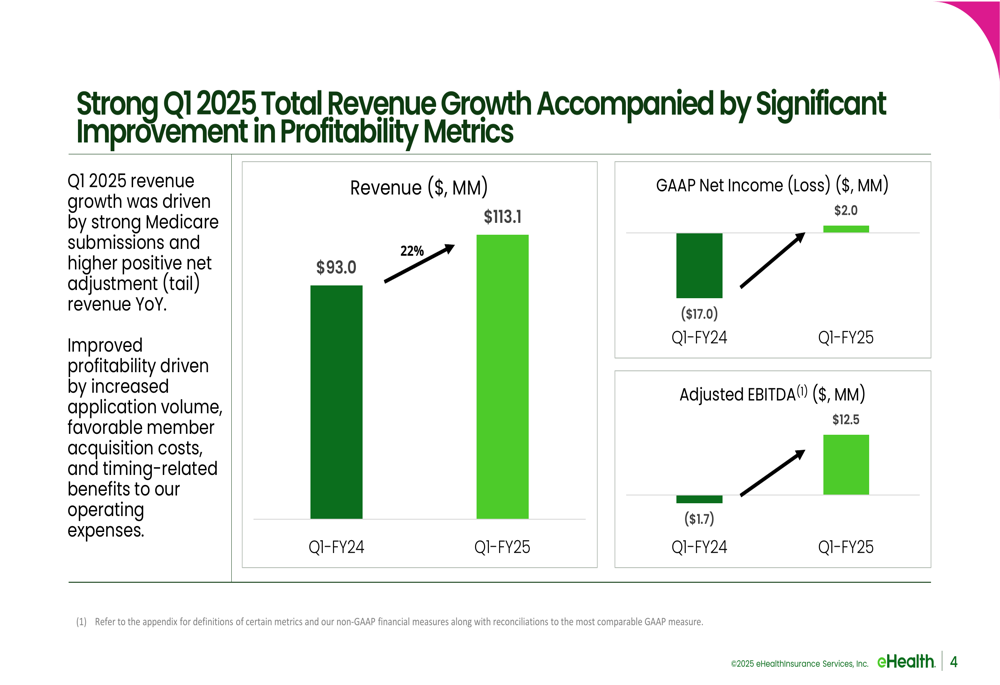

eHealth delivered impressive financial results in the first quarter, with total revenue increasing 22% year-over-year to $113.1 million, compared to $93.0 million in Q1 2024. The company achieved a GAAP net income of $2.0 million, a substantial improvement from a net loss of $17.0 million in the same period last year.

As shown in the following chart detailing revenue and profitability growth:

Adjusted EBITDA reached $12.5 million, compared to a negative $1.7 million in Q1 2024. The company also reported strong cash flow performance, with operating cash flow improving 9% to $77.1 million.

The quarterly performance continues the positive momentum seen in Q4 2024, when the company reported revenue of $315.2 million and record GAAP net income of $97.5 million, as noted in previous earnings reports.

Medicare Segment Performance

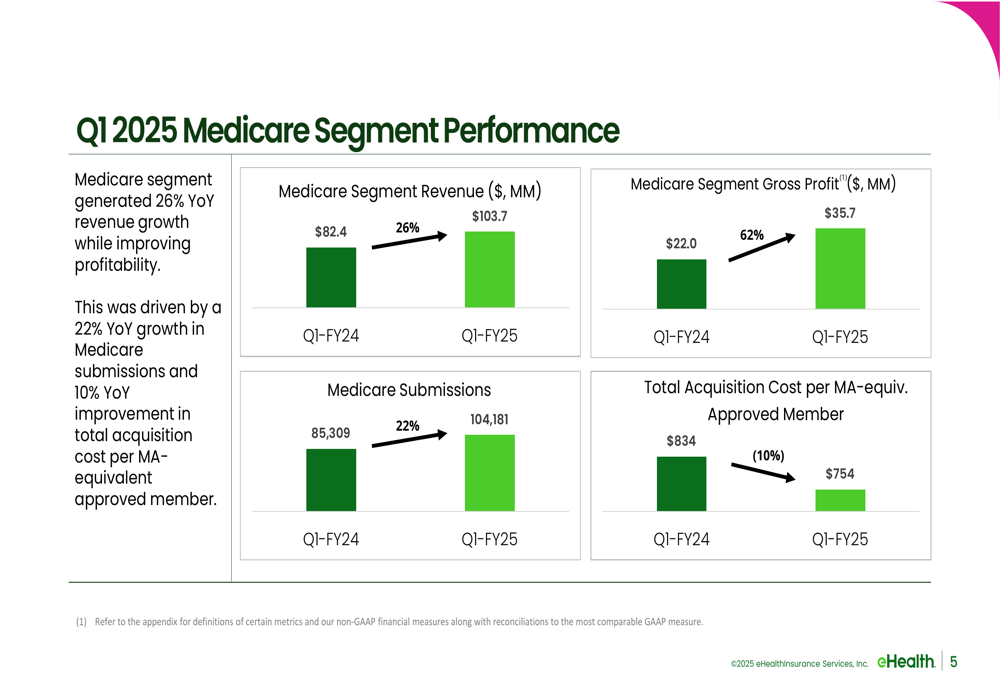

The Medicare segment, which represents eHealth’s core business, showed particularly strong results in Q1 2025. Medicare segment revenue increased 26% year-over-year to $103.7 million, while gross profit surged 62% to $35.7 million.

Total (EPA:TTEF) Medicare submissions grew 22% to 104,181, while the company managed to reduce its total acquisition cost per Medicare Advantage-equivalent approved member by 10% to $754.

The following chart illustrates the Medicare segment’s performance metrics:

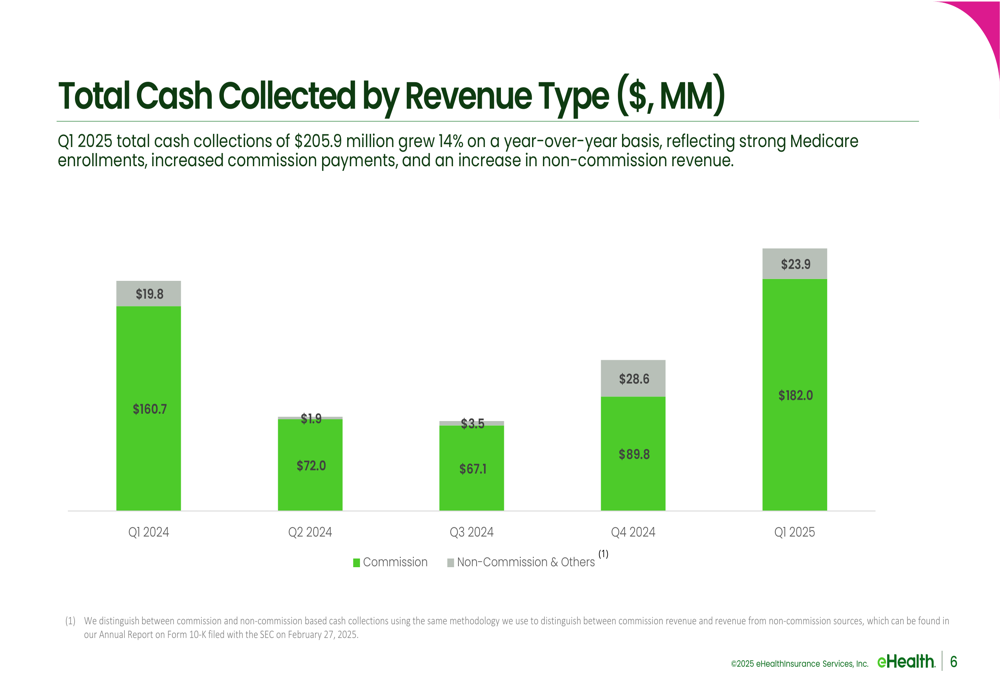

The company’s cash collection also showed healthy growth, with Q1 2025 total cash collections reaching $205.9 million, a 14% increase year-over-year. Commission revenue represented the majority of collections at $182.0 million, with non-commission revenue accounting for $23.9 million.

Digital Transformation Progress

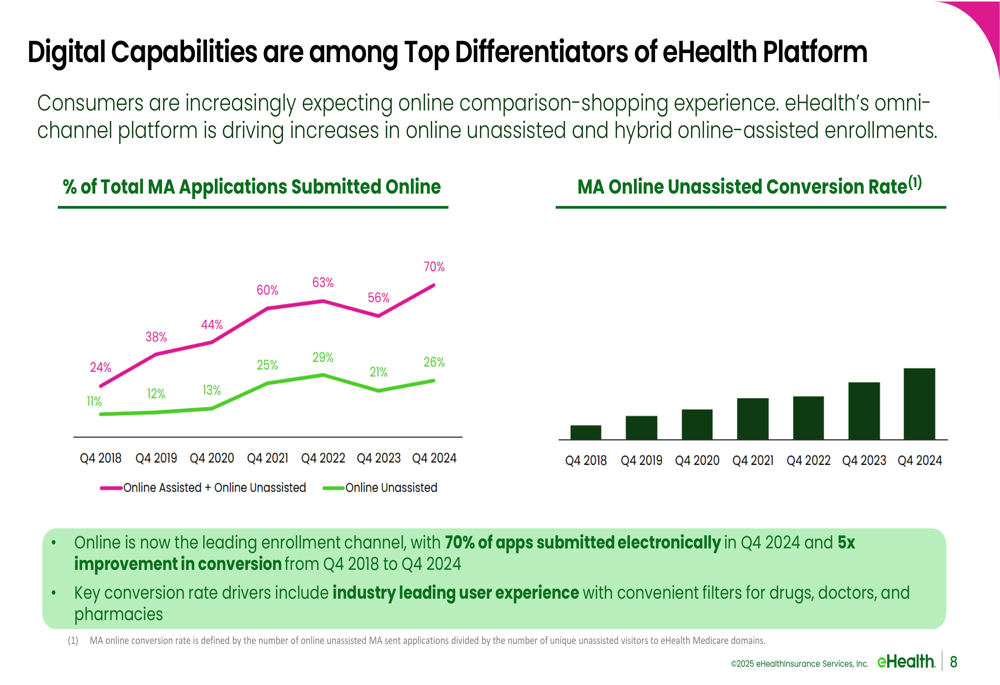

A key driver of eHealth’s improved performance has been its successful digital transformation. The company reported that online has become its leading enrollment channel, with 70% of applications submitted electronically in Q4 2024, representing significant progress in its digital strategy.

The company has achieved a five-fold improvement in online conversion rates since Q4 2018, driven by what it describes as an industry-leading user experience with convenient filters for drugs, doctors, and pharmacies.

The following chart demonstrates the company’s digital capabilities and online conversion progress:

Strategic Initiatives and AI Investments

eHealth is actively investing in technology leadership, with a particular focus on artificial intelligence to enhance customer experience and operational efficiency. In April, the company launched a pilot using AI to help streamline and improve how consumers comparison shop for health plans.

The company has implemented AI-based voice agents to handle incoming calls, gather information, communicate disclosures, and determine eligibility before transferring calls to human licensed advisors who complete sales. This represents a significant advancement in eHealth’s digital-enabled enrollment platform.

For fiscal year 2025, eHealth outlined six strategic objectives, including continuing to grow its consumer brand, optimizing consumer-centric retention efforts, optimizing its telesales organization, advancing AI and digital technology leadership, strengthening carrier relationships, and pursuing targeted diversification beyond Medicare Advantage.

FY25 Guidance and Outlook

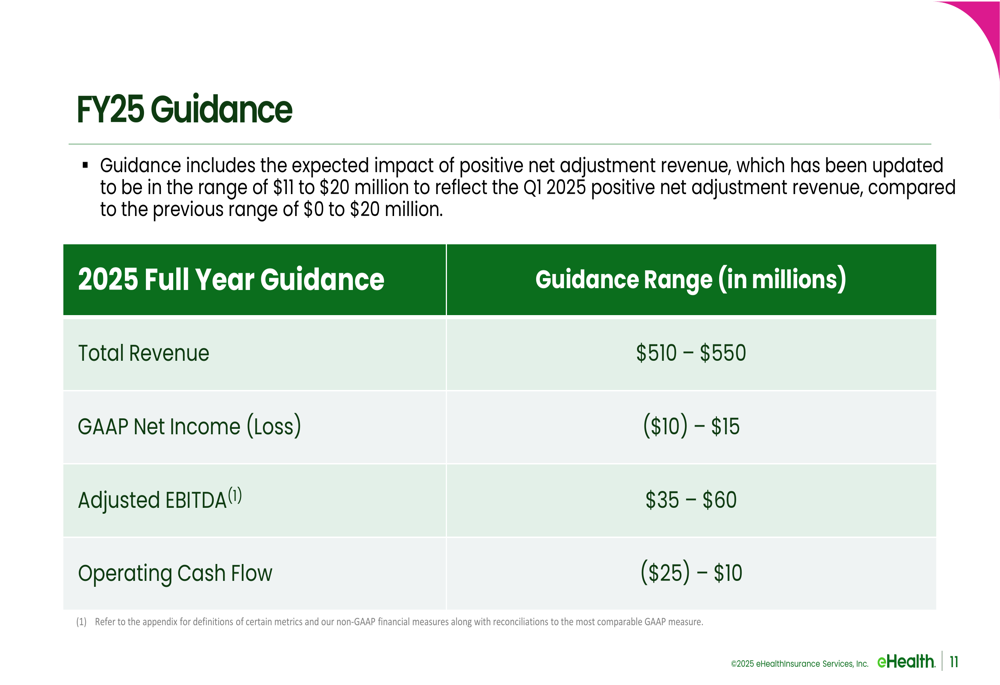

eHealth provided financial guidance for the full year 2025, projecting total revenue between $510 million and $550 million, and GAAP net income ranging from a loss of $10 million to a profit of $15 million. Adjusted EBITDA is expected to be between $35 million and $60 million, while operating cash flow is projected between a negative $25 million and a positive $10 million.

The guidance includes the expected impact of positive net adjustment revenue, which has been updated to a range of $11 million to $20 million, reflecting the Q1 2025 positive net adjustment revenue. This is an improvement from the previous range of $0 to $20 million.

The company’s outlook aligns with its three-year compound annual growth rates, underscoring its commitment to long-term strategic goals. The favorable announcements on 2026 Medicare Advantage reimbursement rates and final Medicare rules are viewed as positive developments for eHealth and the broader industry.

Despite the positive Q1 results and outlook, investors should note that eHealth’s stock has shown significant volatility, with the share price currently trading well below its 52-week high of $11.36, though substantially above its 52-week low of $3.58.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.