Tonix Pharmaceuticals stock halted ahead of FDA approval news

eHealth , Inc. (NASDAQ:EHTH) released its second quarter 2025 financial results on August 6, showing a revenue decline but improved profitability metrics compared to the same period last year. Despite posting a quarterly loss, the company raised its full-year guidance, signaling confidence in a strong second-half performance. The stock responded positively, trading up 10.09% in premarket activity at $3.60 per share.

Quarterly Performance Highlights

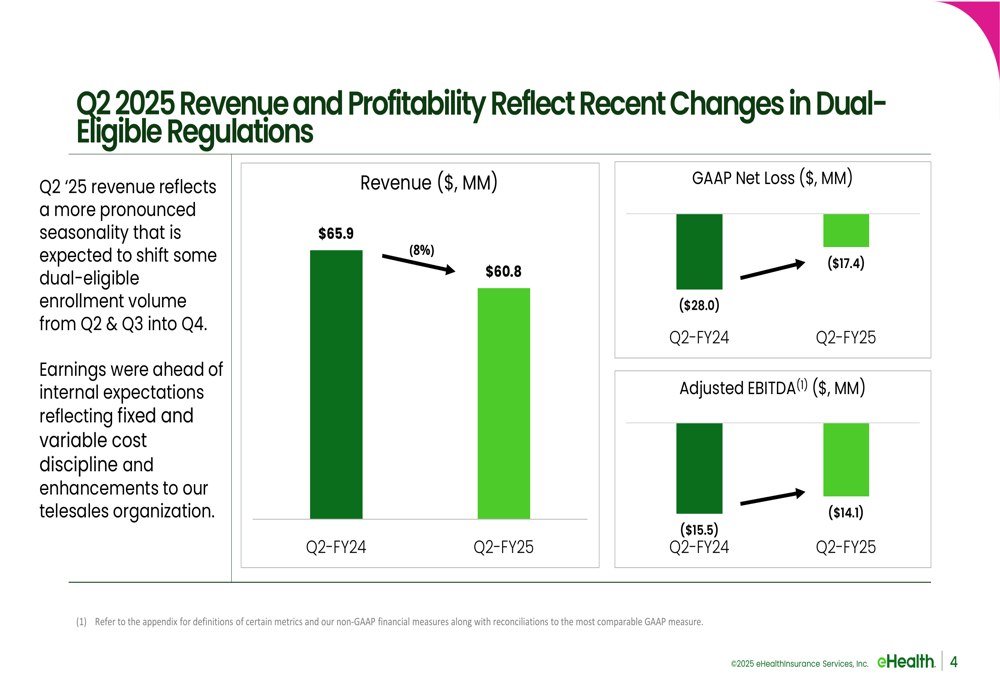

eHealth reported Q2 2025 total revenue of $60.8 million, representing an 8% decrease year-over-year from $65.9 million in Q2 2024. Despite the decline, the company noted that results exceeded internal expectations. The GAAP net loss improved significantly to $17.4 million, compared to a $28.0 million loss in the same quarter last year. Adjusted EBITDA also showed improvement at $(14.1) million versus $(15.5) million in Q2 2024.

As shown in the following chart of quarterly revenue and profitability metrics:

The company attributed the revenue decline to a more pronounced seasonality effect that is expected to shift some dual-eligible enrollment volume from Q2 and Q3 into Q4. Operating costs and expenses decreased 11% to $83.8 million compared to $93.8 million in Q2 2024, reflecting the company’s focus on cost discipline.

"We delivered a strong quarter that exceeded internal expectations and began the critical preparation process for the Medicare Annual Enrollment Period," the company stated in its presentation.

Detailed Financial Analysis

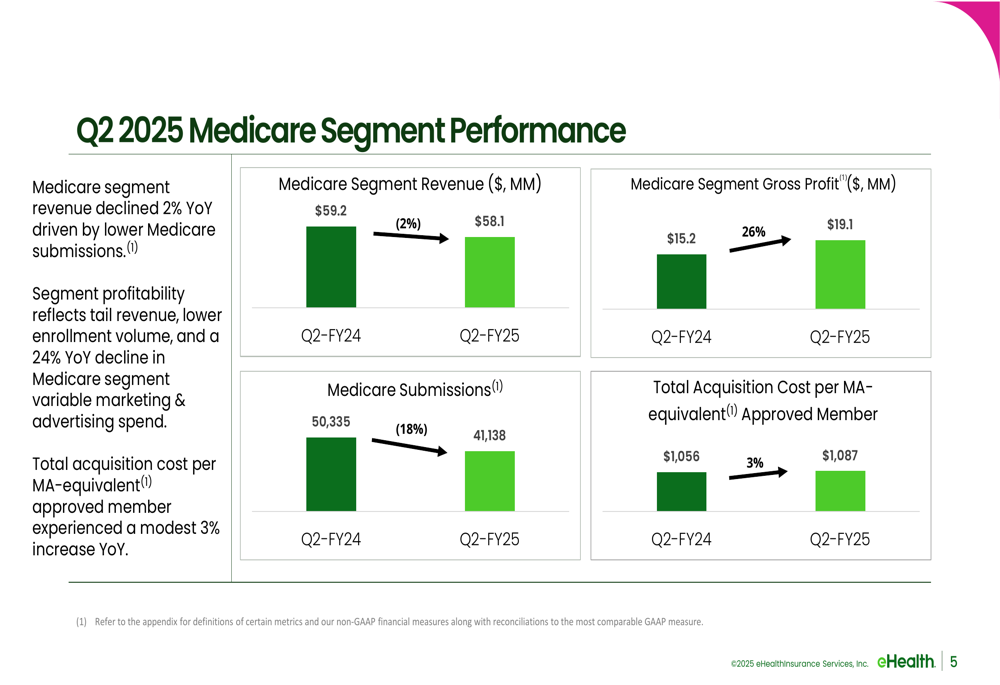

The Medicare segment, which represents eHealth’s core business, saw revenue decrease by 2% to $58.1 million compared to $59.2 million in Q2 2024. Medicare submissions declined 18% to 41,138, reflecting the seasonality shift mentioned earlier. Despite lower submission volume, Medicare segment gross profit increased 26% to $19.1 million.

The following chart illustrates the Medicare segment performance:

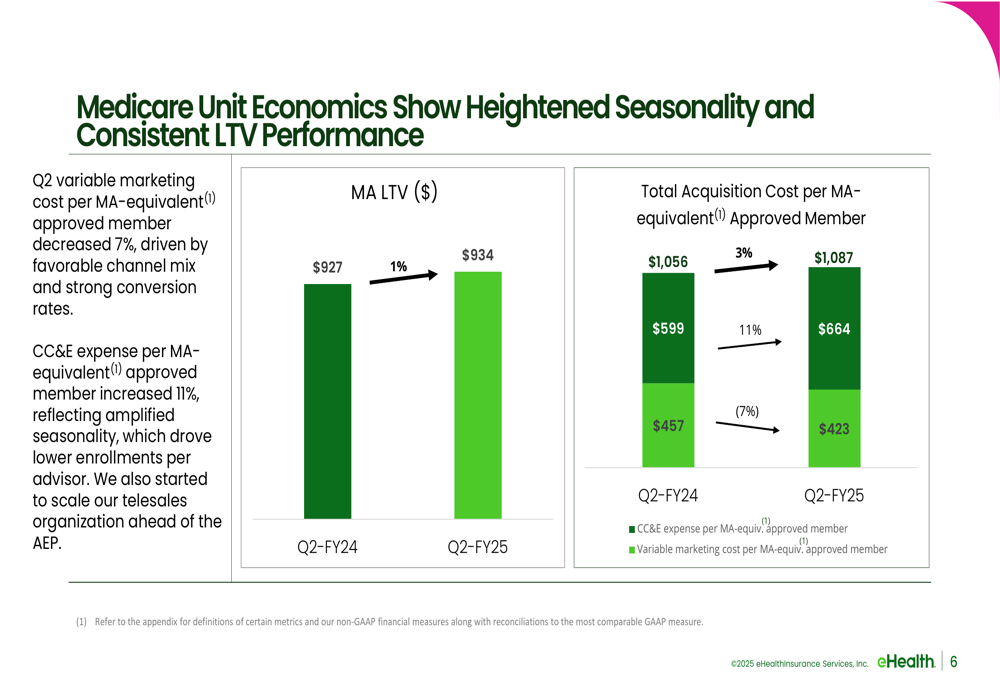

Medicare unit economics showed mixed results. The Medicare Advantage Lifetime Value (MA LTV) increased slightly by 1% to $934, while total acquisition cost per MA-equivalent approved member rose 3% to $1,087. This increase was driven by an 11% rise in customer care and enrollment (CC&E) expense per approved member, partially offset by a 7% decrease in variable marketing cost per approved member.

The company’s Medicare unit economics are detailed in this chart:

Cash, cash equivalents, and marketable securities stood at $105.2 million as of June 30, 2025, which the company described as reflecting "strong cash collections from new Medicare enrollments." This represents a decrease from the $155.6 million reported at the end of Q1 2025.

Strategic Initiatives

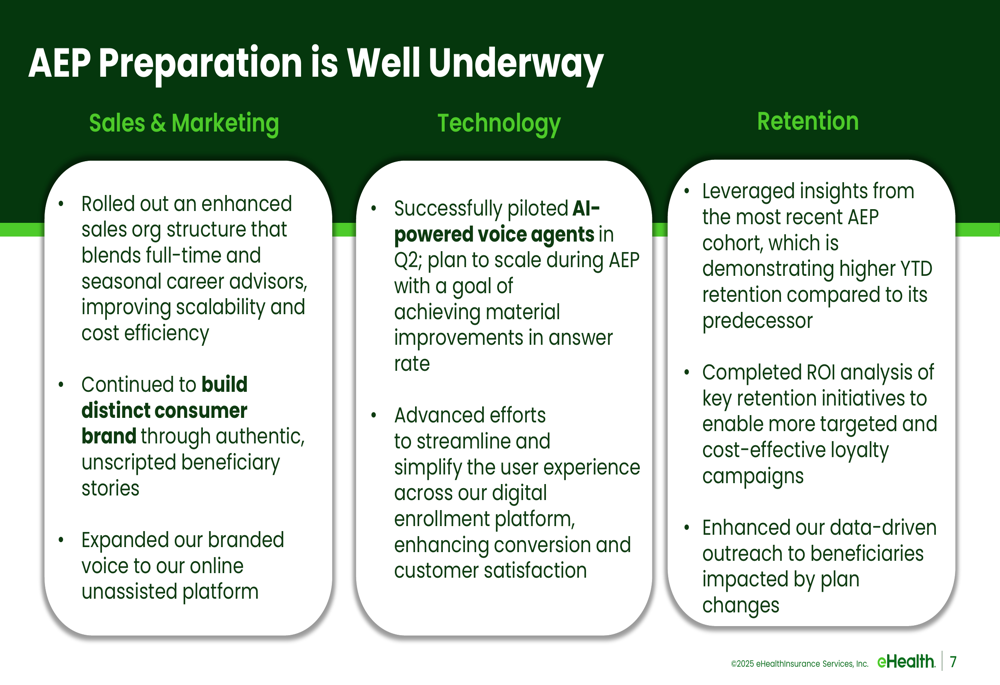

eHealth outlined its preparation efforts for the upcoming Annual Enrollment Period (AEP), focusing on three key areas: Sales & Marketing, Technology, and Retention. The company has rolled out an enhanced sales organization structure and continued to build its consumer brand. On the technology front, eHealth successfully piloted AI-powered voice agents and advanced efforts to streamline operations.

The company’s AEP preparation strategy is outlined here:

For fiscal year 2025, eHealth is pursuing six strategic objectives that include growing its consumer brand, optimizing retention efforts, optimizing its telesales organization, advancing AI and digital technology leadership, strengthening carrier relationships, and pursuing targeted diversification beyond Medicare Advantage.

"We are focusing on evolving and optimizing our consumer-centric retention efforts while continuing to advance our AI and digital technology leadership," the company noted in its strategic objectives.

Forward-Looking Statements

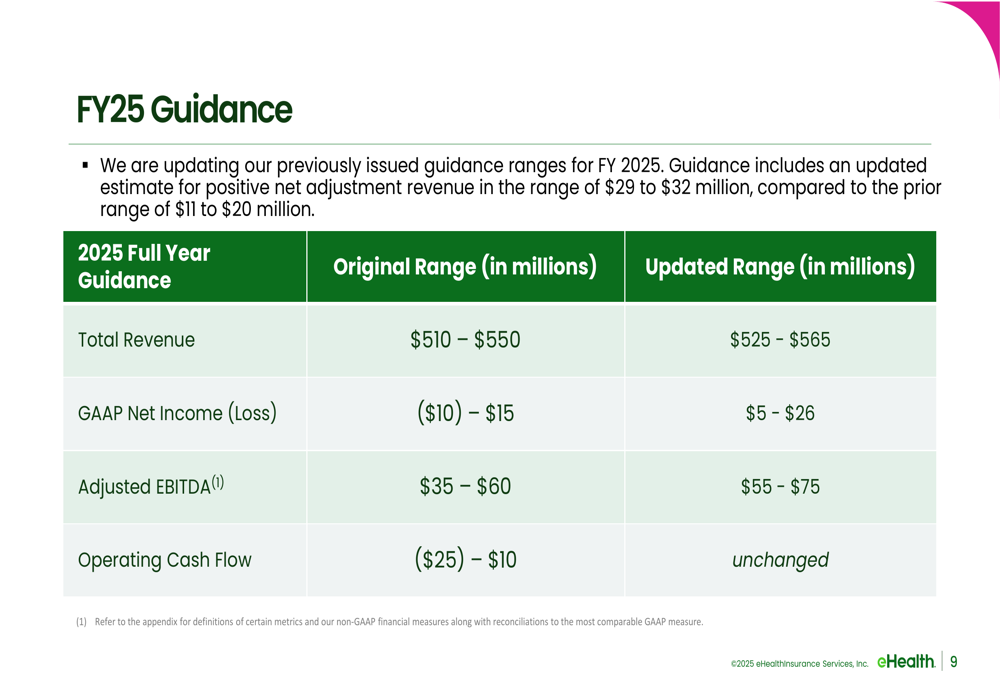

In a significant vote of confidence for future performance, eHealth raised its full-year 2025 guidance across multiple metrics. The company now expects total revenue between $525-$565 million, up from the previous range of $510-$550 million. GAAP net income is projected at $5-$26 million, a substantial improvement from the prior guidance of a $10 million loss to $15 million income. Adjusted EBITDA guidance was also raised to $55-$75 million from $35-$60 million.

The updated guidance includes a positive net adjustment revenue estimate in the range of $29 to $32 million, compared to the prior range of $11 to $20 million.

As shown in the following guidance comparison chart:

This improved outlook comes despite the Q2 loss and suggests that eHealth expects significant improvement in the second half of the year, particularly during the Annual Enrollment Period in Q4. The company’s Q1 2025 performance, which showed a net income of $2 million compared to a net loss of $17 million in Q1 2024, provides some historical basis for this optimism.

The guidance upgrade represents a notable shift from the company’s Q1 earnings call, where it had maintained its previous guidance despite exceeding expectations. The revised outlook suggests that management has gained additional confidence in its operational improvements and strategic positioning for the remainder of the fiscal year.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.