Asahi shares mark weekly slide after cyberattack halts production

Introduction & Market Context

Eidesvik Offshore ASA (OB:EIOF) released its Q2 2025 presentation on August 27, showcasing continued operational strength amid favorable market conditions in both traditional offshore and renewable energy sectors. The Norwegian offshore vessel operator reported almost full fleet utilization and improved financial metrics, maintaining its position as a leading provider of specialized offshore vessels.

The company highlighted steady oil demand with strong backlog and tender activity for EPC firms, while noting that the global PSV fleet remains flat. An uptick in offshore drilling rigs is expected to secure increased activity in 2026 and 2027, with subsea and renewables activity projected to remain high.

Quarterly Performance Highlights

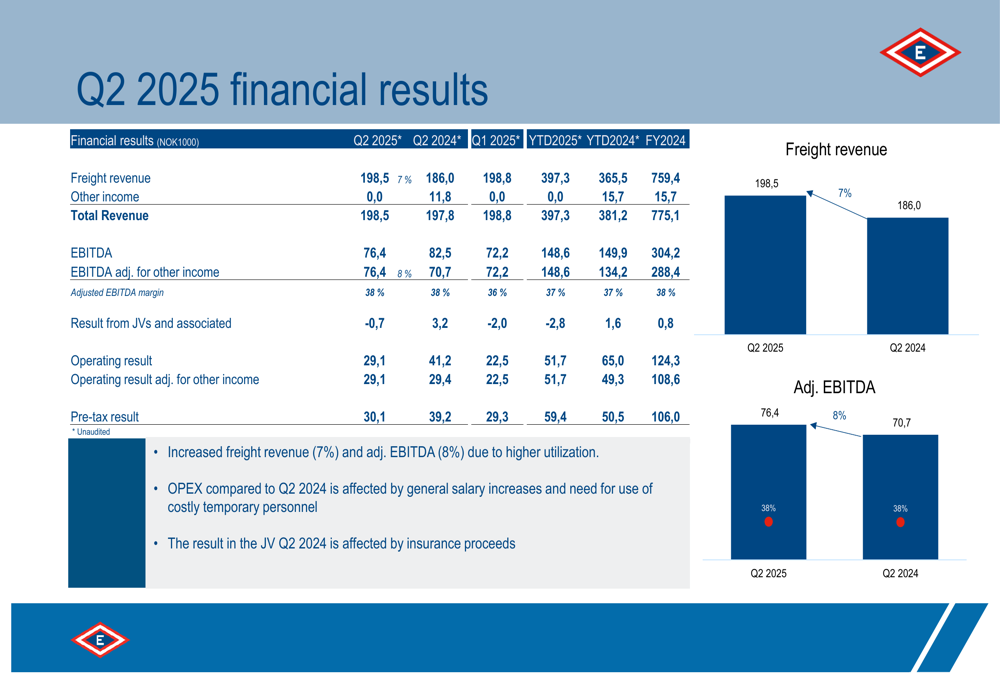

Eidesvik reported freight revenue of NOK 198.5 million in Q2 2025, representing a 7% increase from NOK 186 million in the same period last year. Adjusted EBITDA rose 8% to NOK 76.4 million, maintaining a stable margin of 38%.

As shown in the following comprehensive financial results comparison:

The improved performance was primarily driven by higher fleet utilization, which reached 98% during the quarter. This represents a continuation of the strong momentum seen in Q1 2025, when the company reported an 11% year-over-year revenue increase.

"Continued excellent operational performance" was highlighted as a key achievement in the presentation, with no Lost Time Incidents (LTIs) recorded during the quarter. The company’s current stock price stands at NOK 13.40, trading between its 52-week range of NOK 10.05 to NOK 16.58.

Segment Analysis

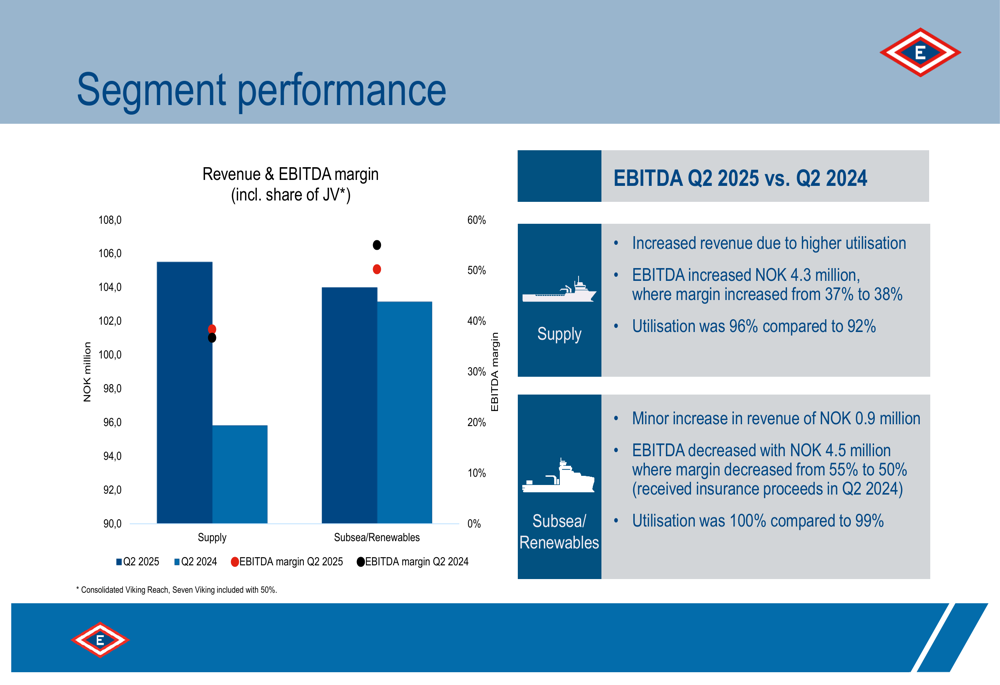

Eidesvik’s business is divided into two main segments: Supply and Subsea/Renewables. The Supply segment showed improved performance with increased utilization of 96% compared to 92% in Q2 2024, resulting in higher revenue and an improved EBITDA margin of 38% (up from 37%).

The Subsea/Renewables segment maintained near-perfect utilization at 100% (compared to 99% in Q2 2024) but experienced a decrease in EBITDA margin from 55% to 50%. This segment breakdown is illustrated in the following chart:

The company’s strategic focus on green offshore vessels is evident in its fleet composition, with vessels featuring LNG Dual Fuel, Battery Hybrid, and Methanol Dual Fuel technologies. This aligns with Eidesvik’s stated mission to be "the market leader within green offshore vessels."

Contract Backlog and Future Outlook

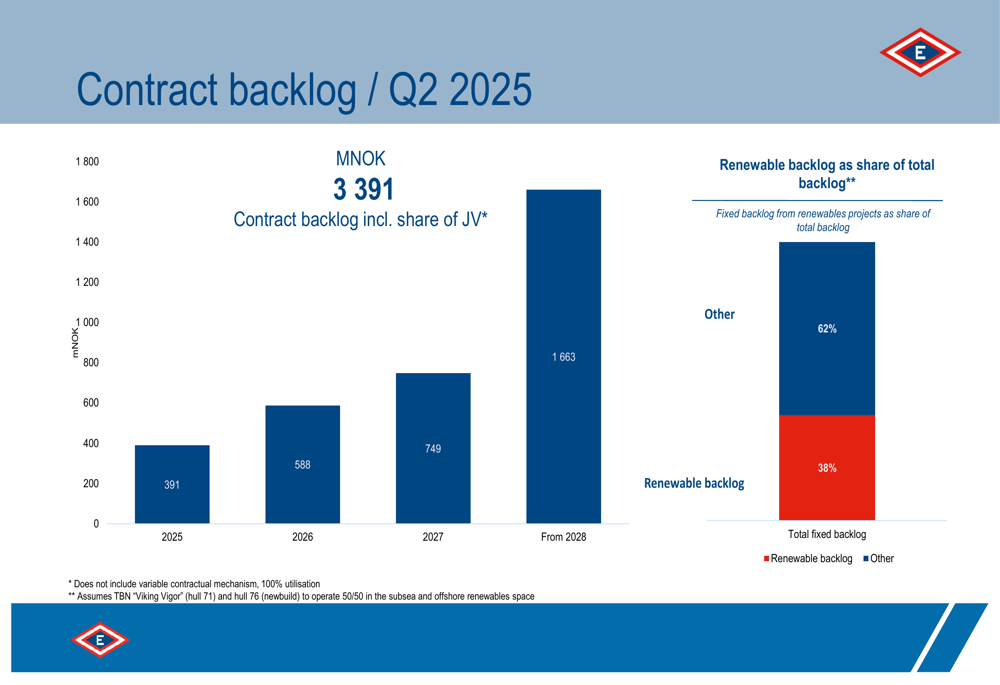

One of the most significant highlights from the presentation was the strong contract backlog, which totaled NOK 3,391 million including joint ventures. This represents an increase from NOK 2,882 million previously reported. The backlog extends well into the future, with NOK 1,663 million scheduled for 2028 and beyond.

The following chart illustrates the distribution of the contract backlog by year:

Notably, 38% of the total fixed backlog comes from renewable energy projects, demonstrating Eidesvik’s successful diversification strategy. The company also announced that Subsea7 has extended the contract for the subsea vessel Seven Viking, declaring the remaining option for 2026 and adding 2027 as a firm year, plus an option for 2028, with improved market terms for the 2027-2028 period.

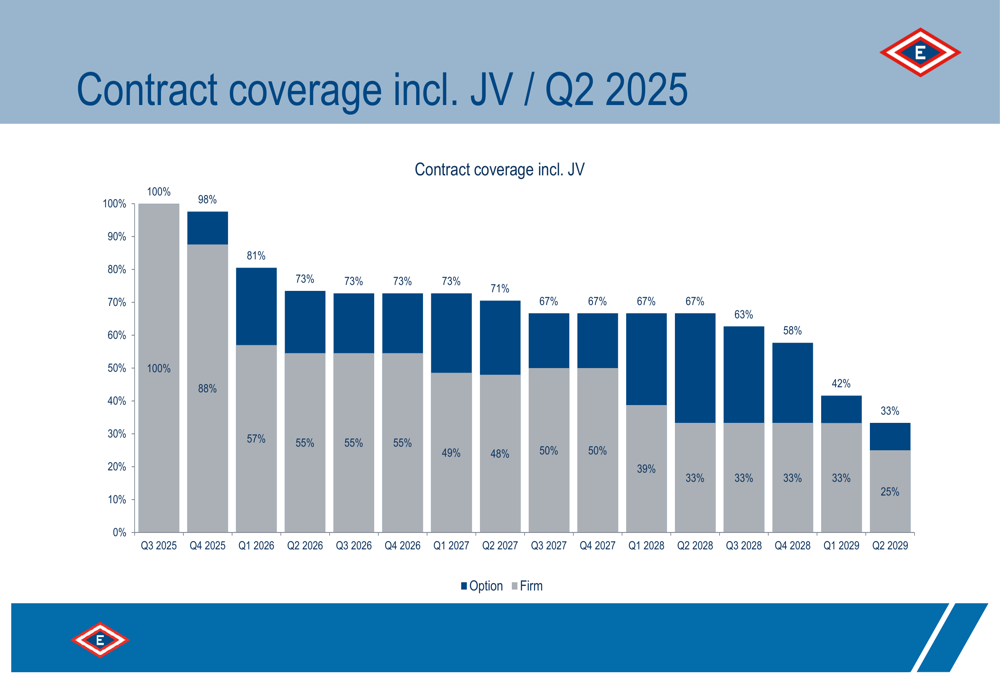

The contract coverage visualization below shows the percentage of fleet secured with contracts through Q2 2029:

Looking ahead, Eidesvik noted that PSV legacy contracts will roll off in late 2025, which could impact revenue if not replaced. However, the company expressed a positive long-term outlook for both segments and reaffirmed its growth strategy while maintaining dividend payments to shareholders. The Board of Directors has approved a dividend payment of NOK 0.30 per share, with an ex-date of August 28, 2025.

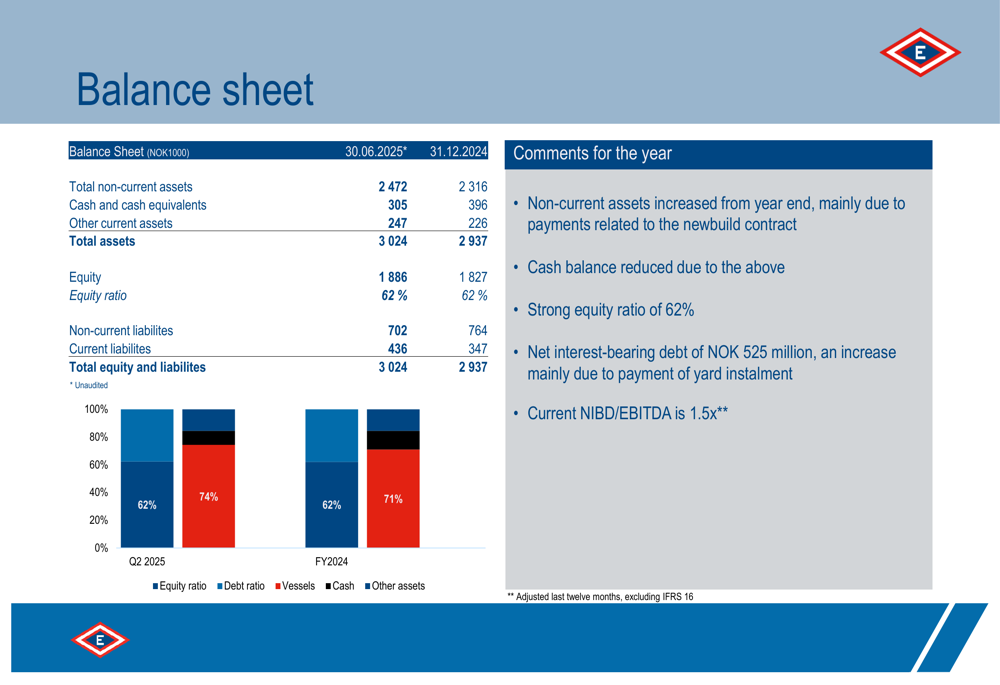

Balance Sheet and Financial Position

Eidesvik maintained a strong balance sheet with an equity ratio of 62% as of June 30, 2025, unchanged from the end of 2024. Total assets increased to NOK 3,024 million from NOK 2,937 million at year-end 2024.

The company’s financial position is detailed in the following balance sheet overview:

Cash and cash equivalents decreased to NOK 305 million from NOK 396 million, primarily due to payments related to newbuild contracts. Net interest-bearing debt increased to NOK 525 million, resulting in a NIBD/EBITDA ratio of 1.5x, which the company describes as "among the industry’s healthiest."

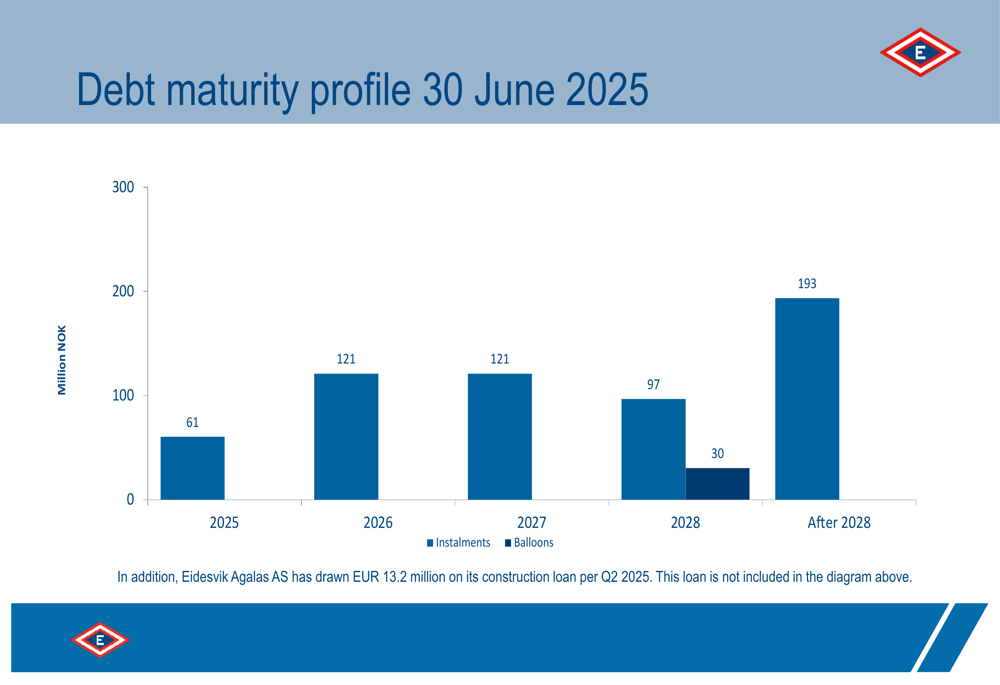

The debt maturity profile shows a manageable distribution of obligations, with the largest portions due after 2028:

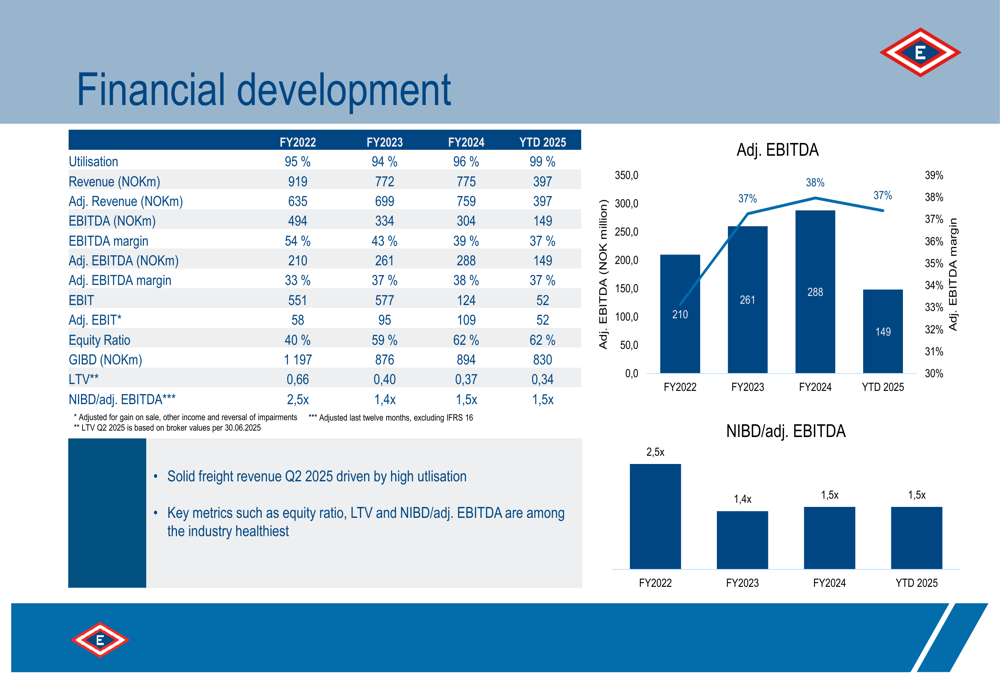

Eidesvik’s financial development over recent years demonstrates consistent improvement, with adjusted EBITDA growing from NOK 210 million in FY2022 to NOK 288 million in FY2024, while maintaining stable leverage ratios:

With its strong operational performance, growing renewable energy exposure, and solid financial position, Eidesvik appears well-positioned to navigate market challenges while pursuing its growth strategy in both traditional offshore and renewable energy markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.