Gold prices edge higher; Fed indepedence fears spur safe haven buying

Introduction & Market Context

Elektroimportøren AS (OB:ELIMP) presented its Q1 2025 financial results on May 15, 2025, revealing strong performance across its operations in Norway and Sweden. The electrical equipment retailer’s stock closed at NOK 13.25 on May 14, up 5.16% ahead of the earnings release, reflecting positive market sentiment. The company’s shares have been trading near their 52-week high of NOK 14.70, having recovered substantially from their 52-week low of NOK 8.76.

Despite lingering market uncertainty and low consumer confidence measures at the end of Q1, Elektroimportøren delivered solid growth across all business segments, continuing the positive momentum reported in its Q4 2024 results.

Quarterly Performance Highlights

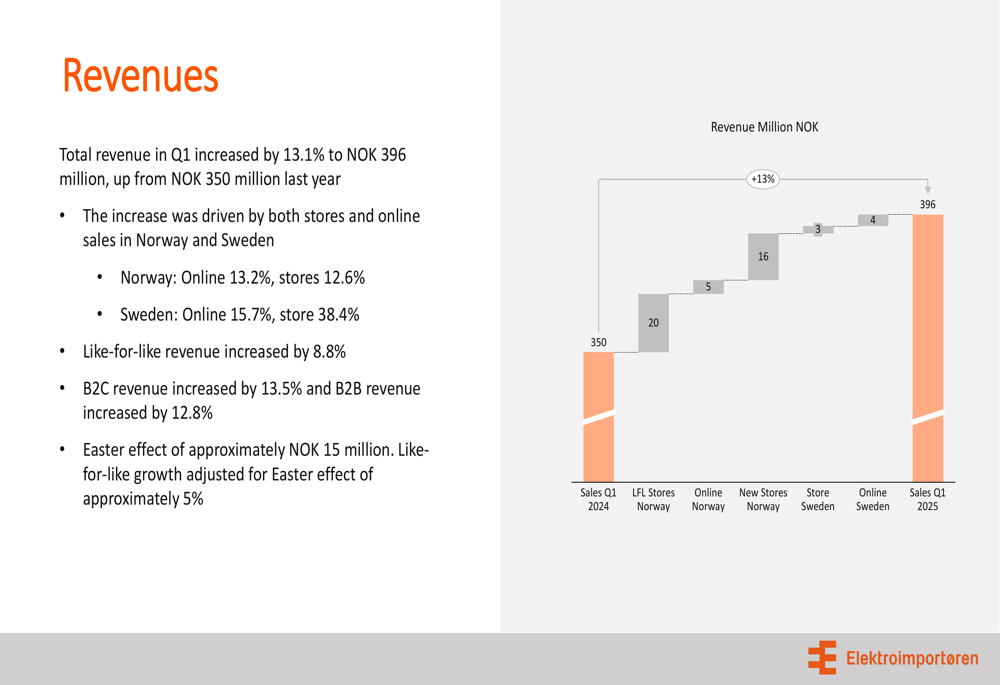

Elektroimportøren reported group revenue of NOK 396 million for Q1 2025, representing a 13.1% increase from NOK 350 million in the same period last year. Like-for-like revenue grew by 8.8%, though the company noted an Easter effect of approximately NOK 15 million, adjusting the like-for-like growth to approximately 5% when factoring out this seasonal impact.

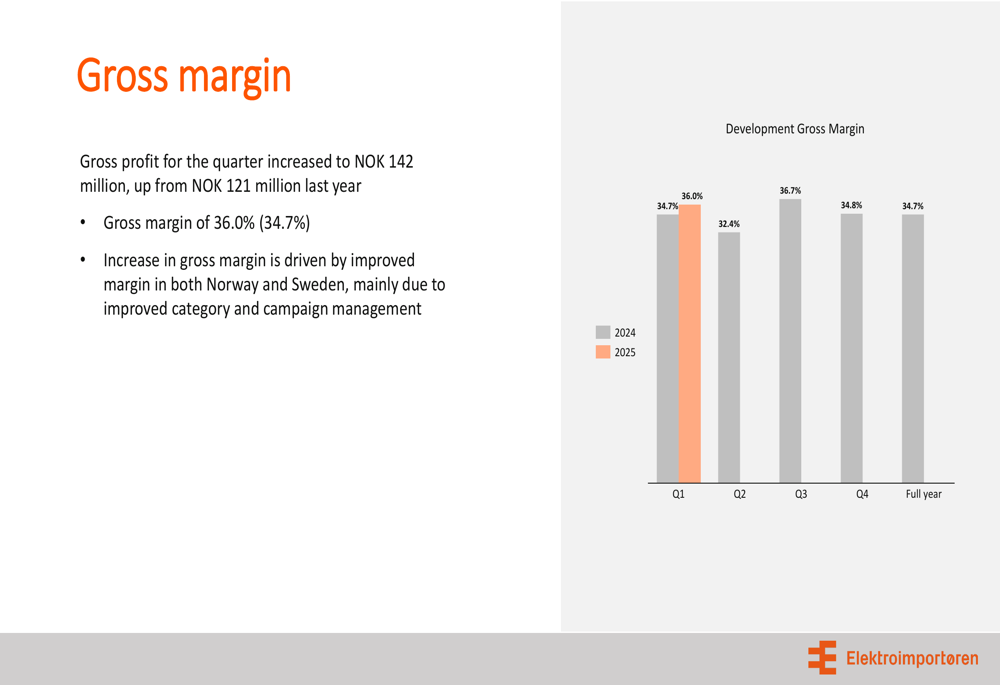

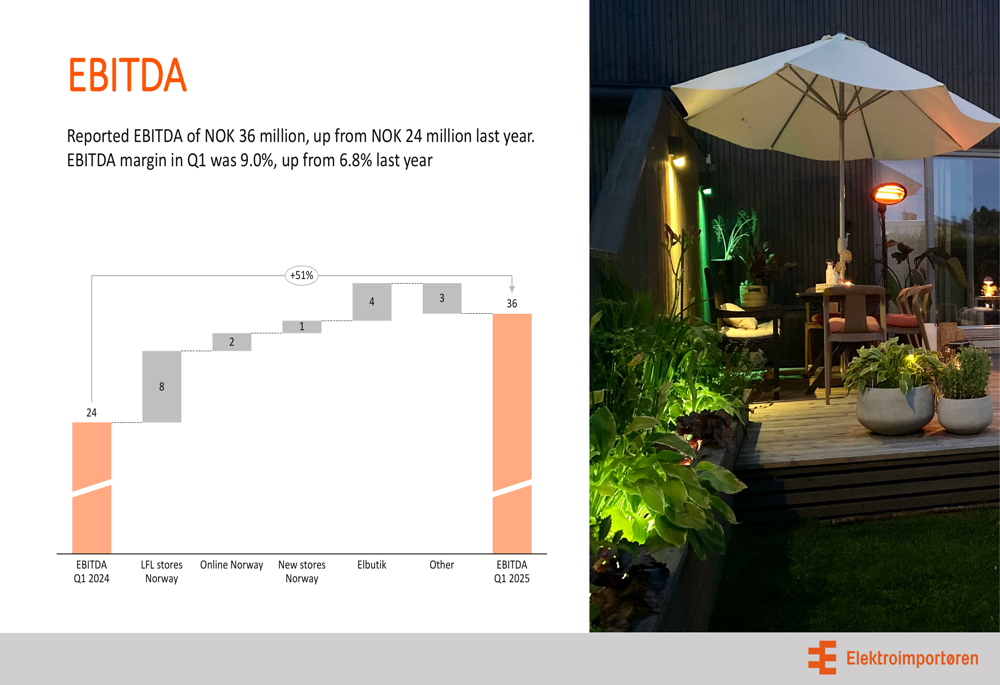

The company’s gross margin improved to 36.0%, up from 34.7% in Q1 2024, driven by improved category and campaign management in both Norway and Sweden. This margin improvement, coupled with better operational efficiency, led to a significant EBITDA increase to NOK 36 million, up from NOK 24 million in the previous year.

As shown in the following revenue breakdown chart:

The revenue growth was balanced across channels and markets, with Norway’s online sales increasing by 13.2% and store sales by 12.6%. Sweden showed even stronger performance with online sales up 15.7% and store sales surging by 38.4%. Both B2C and B2B segments contributed to this growth, with increases of 13.5% and 12.8% respectively.

Detailed Financial Analysis

Elektroimportøren’s gross profit for Q1 2025 reached NOK 142 million, up from NOK 121 million in Q1 2024. The gross margin improvement to 36.0% represents a continuation of the company’s focus on margin enhancement, as illustrated in this quarterly trend:

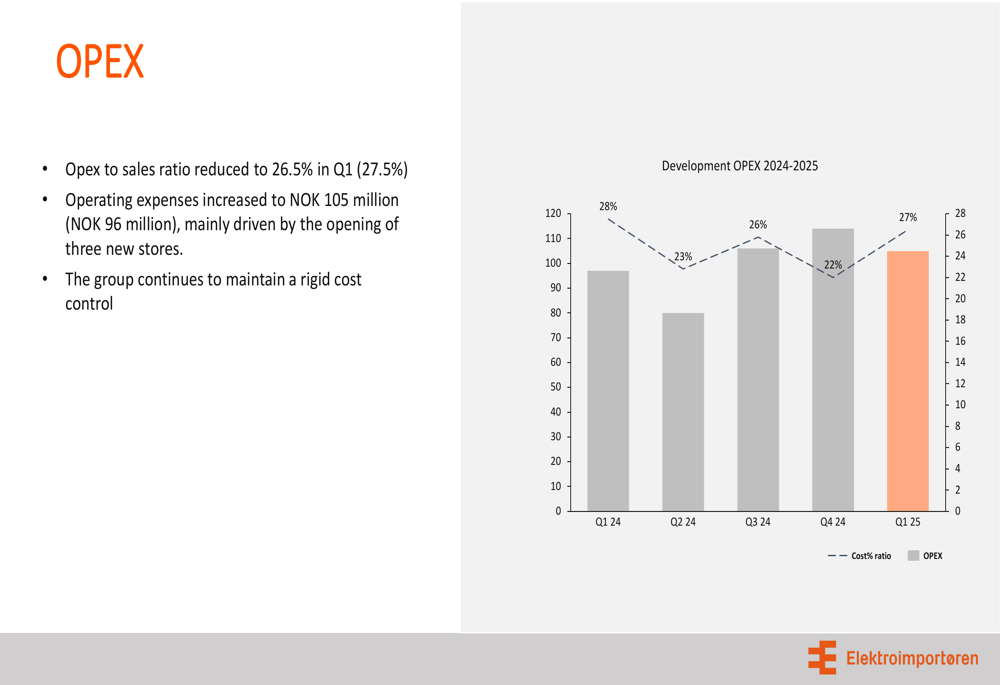

Operating expenses increased to NOK 105 million from NOK 96 million in the previous year, primarily due to the opening of three new stores. However, the OPEX to sales ratio improved to 26.5% from 27.5%, demonstrating the company’s commitment to cost control while expanding operations.

The EBITDA bridge below illustrates how different business segments contributed to the overall EBITDA improvement:

Despite the positive operational performance, the company still reported a net loss of NOK 8 million for the quarter, though this represents an improvement from the NOK 11 million loss in Q1 2024.

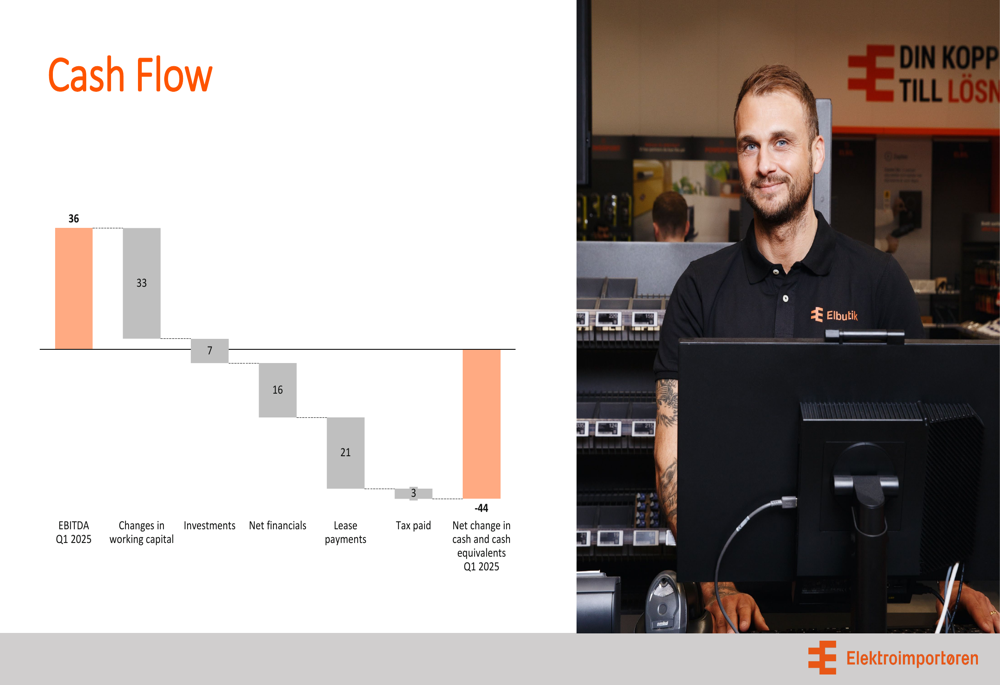

The cash flow analysis shows that while the company generated positive EBITDA, investments and changes in working capital resulted in a net cash reduction of NOK 44 million during the quarter:

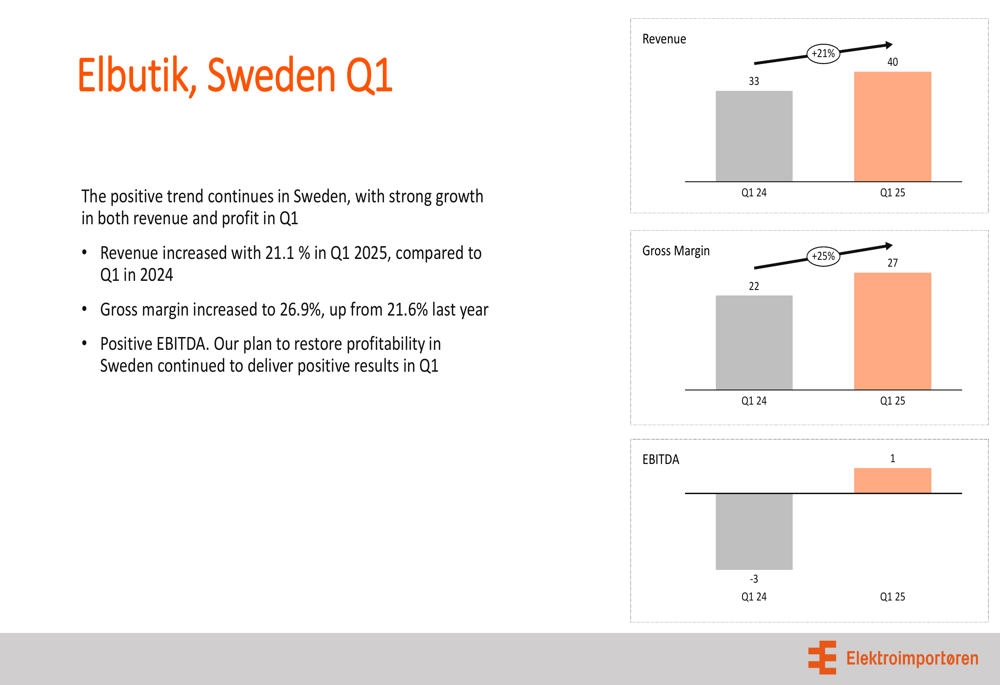

Swedish Operations Turnaround

A particularly noteworthy development was the performance of Elbutik in Sweden, which achieved a 21.1% revenue increase to NOK 40 million and, more importantly, delivered a positive EBITDA of NOK 1 million, compared to a NOK 3 million loss in the same period last year.

The following chart illustrates the impressive turnaround in the Swedish operations:

This performance aligns with the company’s projections from Q4 2024, when it anticipated double-digit growth in Sweden for Q1 2025. The visitor count in Swedish stores increased by 29.8%, contributing significantly to the revenue growth.

Strategic Initiatives

Elektroimportøren continues to execute its strategy focused on four key areas: becoming a total provider of electrical equipment, strengthening its specialist position, developing own brands, and capitalizing on market opportunities.

The company opened its 30th store in Lillehammer in March and is exploring three new locations for signing in Norway during 2025. The integration of SpotOn as Elektroimportøren’s service engine is progressing as planned, with cost savings expected in the second half of 2025.

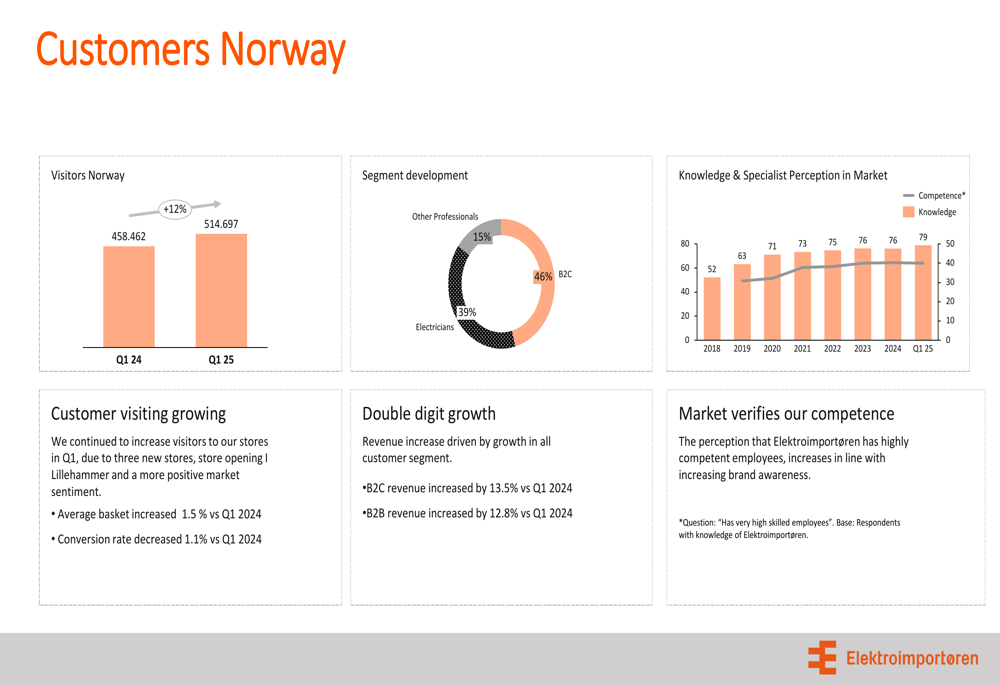

The company’s specialist positioning is reinforced by customer perception data showing that 72% of customers perceive Elektroimportøren as having "very highly skilled employees," with 7 out of 10 sales staff being educated electricians.

Customer statistics for Norway show positive trends, with visitor numbers increasing by 12% year-over-year:

The share of own brand products (Namron) increased to 35% in Norway (from 33.6%) and 10.2% in Sweden (from 8.4%), contributing to margin improvements.

Forward-Looking Statements

Looking ahead, Elektroimportøren maintains a cautiously optimistic outlook while monitoring macroeconomic developments. The company reported that the positive sales trend continued into April, with January-April sales reaching NOK 515 million, representing 8.3% growth compared to the same period last year.

The integration of SpotOn is expected to generate cost savings in the second half of 2025, and Elektroimportøren is also buying back the 8% of SpotOn shares previously held by employees.

While the market remains characterized by uncertainty with low consumer confidence measures at the end of Q1, the company’s performance in both Norway and Sweden suggests it is well-positioned to navigate the challenging environment and continue its growth trajectory.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.