Gold prices edge higher; Fed indepedence fears spur safe haven buying

Introduction & Market Context

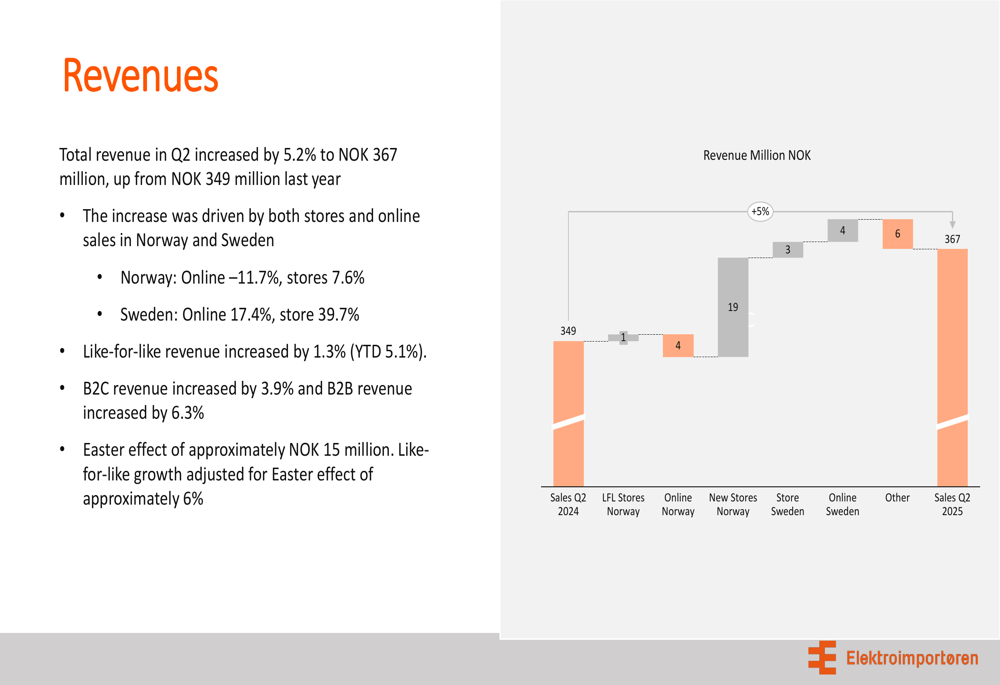

Elektroimportøren AS (OB:ELIMP) presented its Q2 2025 results on August 21, 2025, showing continued revenue growth across both its Norwegian and Swedish operations. The electrical equipment retailer reported a 5.2% increase in revenue compared to the same period last year, reaching NOK 367 million, while significantly improving its gross margin and EBITDA performance.

The company’s stock closed at NOK 15.85 on August 20, down 3.35% ahead of the earnings presentation, reflecting some investor caution. This follows a more robust Q1 2025 performance when the company reported 13.1% year-over-year revenue growth, indicating a moderation in growth momentum during the second quarter.

Quarterly Performance Highlights

Elektroimportøren reported growth across both its B2B and B2C customer segments despite what it described as a "negative Easter effect" during the quarter. The company achieved like-for-like revenue growth of 1.3%, with B2C revenue increasing by 3.9% and B2B revenue growing by 6.3%.

As shown in the following operational summary from the presentation:

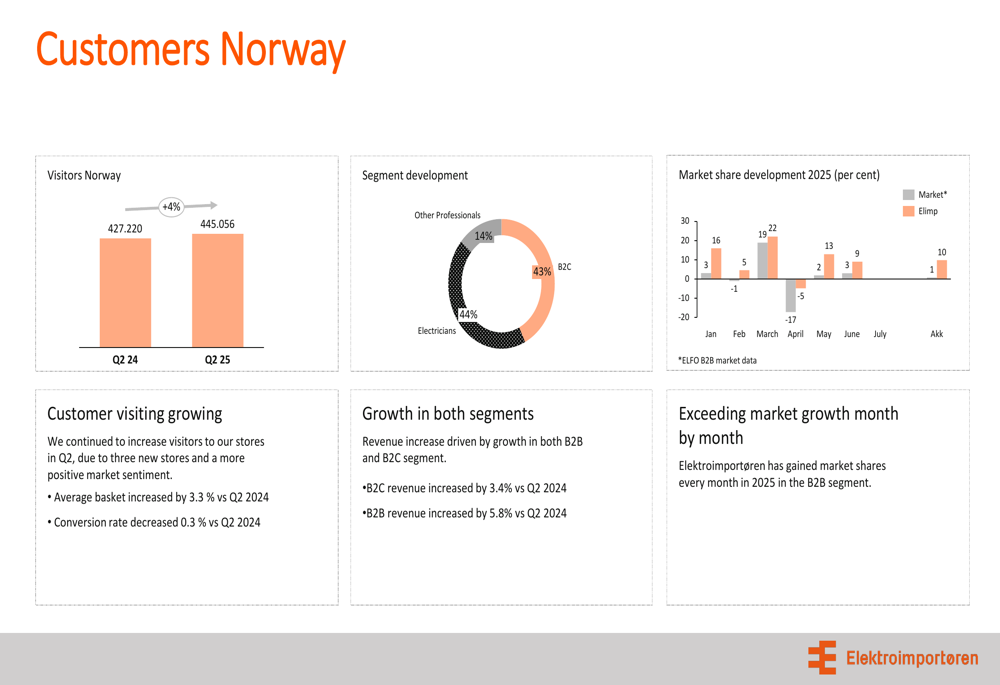

Physical stores emerged as a key growth driver, with increasing visitor numbers and higher average basket values. In Norway, visitor numbers reached 445,056 in Q2 2025, representing a 4% increase from 427,220 in Q2 2024. The average basket value increased by 3.3% compared to the same period last year, though conversion rates decreased slightly by 0.3%.

The following chart illustrates customer metrics in Norway, including segment distribution:

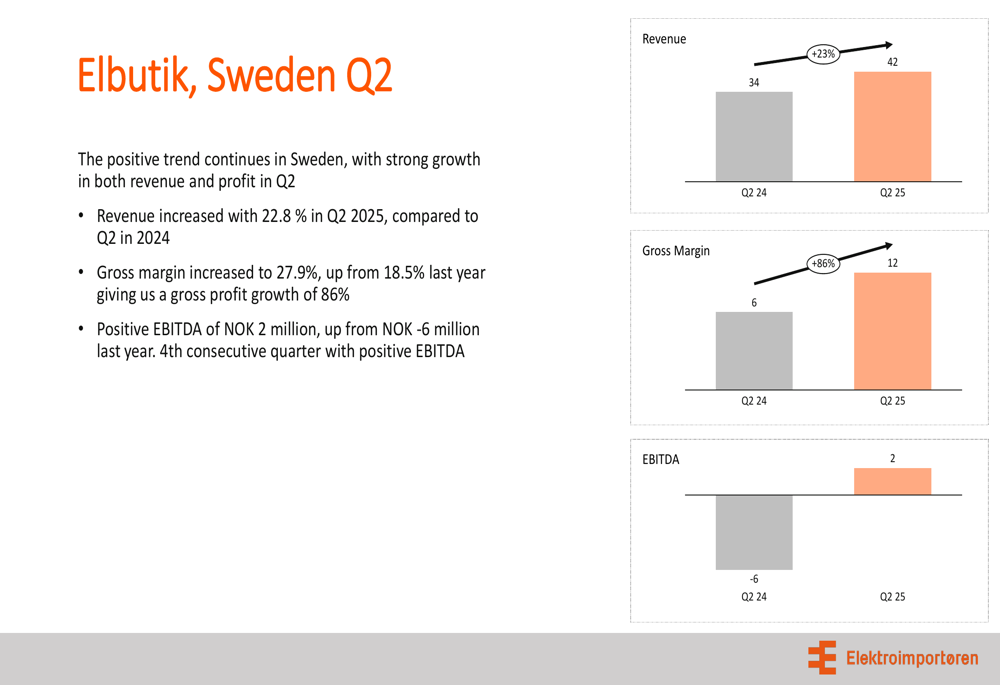

The Swedish operations under the Elbutik brand showed particularly strong performance, with revenue increasing by 22.8% to NOK 42 million from NOK 34 million in Q2 2024. This marks the fourth consecutive quarter of positive EBITDA for the Swedish business.

The following chart details the financial performance of Elbutik in Sweden:

Detailed Financial Analysis

Elektroimportøren’s gross margin improved significantly to 34.9% in Q2 2025, up from 32.4% in the same period last year. This improvement was attributed to better category and campaign management across both Norwegian and Swedish operations.

The revenue breakdown by segment and channel is illustrated in the following chart:

Operating expenses increased to NOK 87 million from NOK 80 million in Q2 2024, primarily driven by the opening of three new stores. As a percentage of sales, operating expenses rose to 23.8% from 22.8% in the prior year.

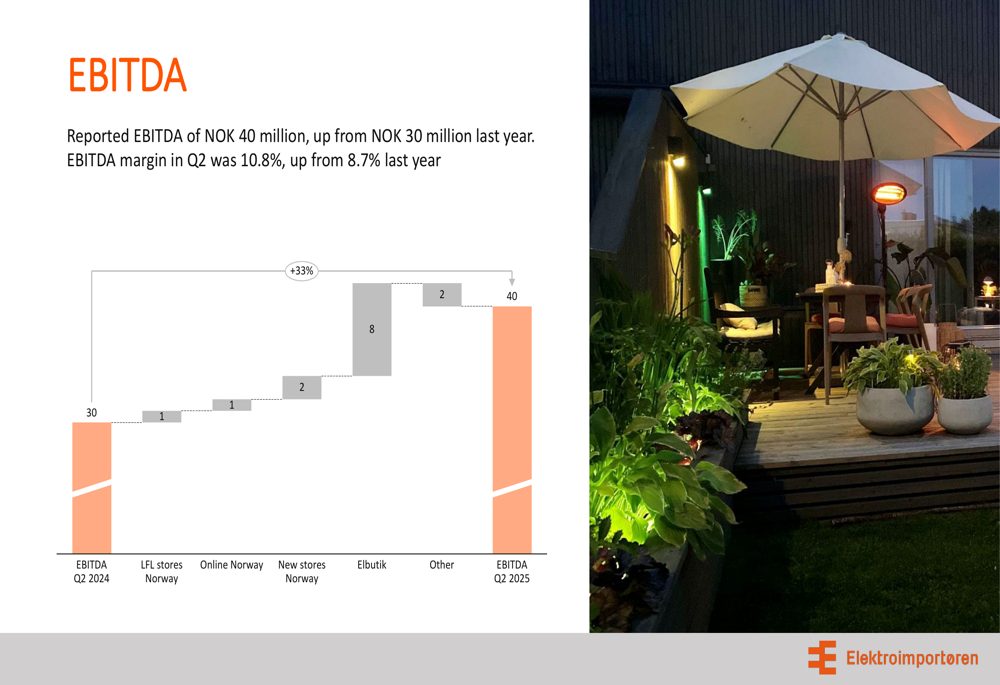

EBITDA showed substantial improvement, increasing to NOK 40 million from NOK 30 million in Q2 2024, representing a 33% increase. The EBITDA margin expanded to 10.8% from 8.7% in the prior year period. Adjusted EBITDA reached NOK 41 million, up from NOK 33 million.

The following chart shows the EBITDA development:

Net profit for the quarter was NOK 0, a significant improvement from the NOK -5 million loss reported in Q2 2024. This achievement of breakeven represents progress from the NOK -8 million loss reported in Q1 2025.

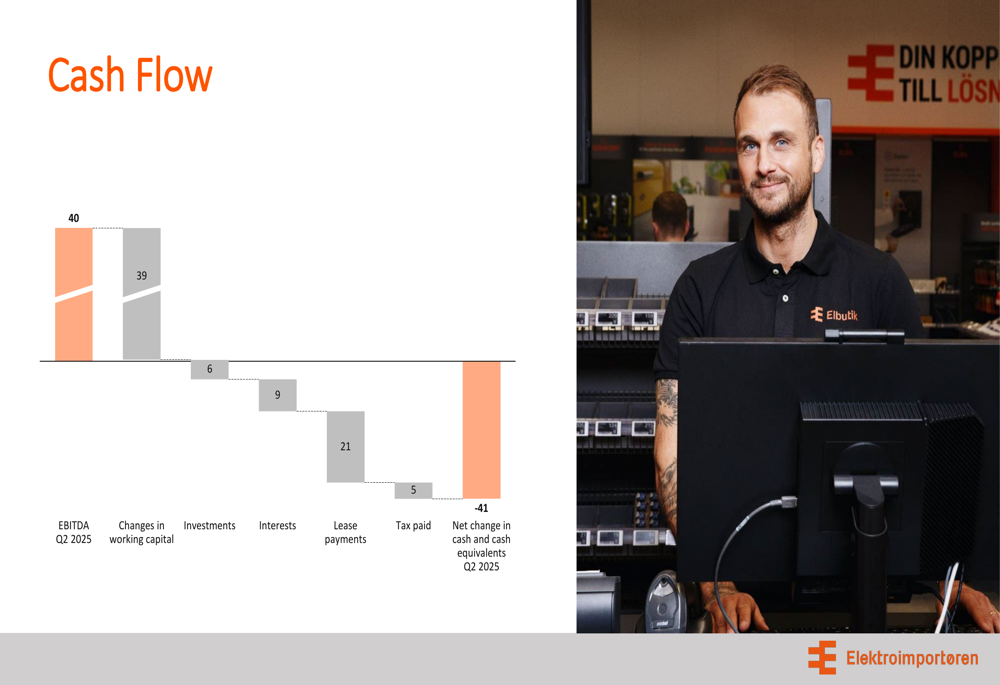

The company’s cash flow for the quarter was negative NOK 41 million, as illustrated in this waterfall chart:

Strategic Initiatives

Elektroimportøren outlined four key strategic areas that form the foundation of its business approach: positioning as a " Total (EPA:TTEF) Provider" of electrical equipment, maintaining a specialist position serving three distinct customer segments, developing high-quality own brands, and pursuing growth opportunities through new stores, Swedish expansion, and focus on Smart Home and energy-efficient solutions.

The following slide details these strategic priorities:

Store expansion remains a central element of the company’s growth strategy. During Q2, Elektroimportøren signed a contract for a new store in Bergen, which is scheduled to open in October 2025. This will be the company’s third location in Bergen, reflecting its commitment to physical retail as a growth driver.

The company also highlighted that 72% of customers perceive Elektroimportøren as having "very highly skilled employees," underscoring its specialist positioning in the market.

Forward-Looking Statements

Following the close of Q2, Elektroimportøren completed the integration of SpotOn in July, incurring minor restructuring costs. The company reported that July sales showed growth compared to the previous year in both B2B and B2C segments, despite very warm weather conditions. July revenue increased by 5.8% compared to the same month last year.

The Swedish operations continue to show positive sales trends, with the Veddesta Store delivering like-for-like growth of +30% year-to-date. The company is considering new store locations in Sweden within the next 24 months, indicating confidence in its expansion strategy despite the moderation in overall growth rate.

With available credit facilities of NOK 120 million out of a total NOK 340 million facility, Elektroimportøren appears well-positioned to fund its continued expansion plans. The company’s loan has a maturity of three years from March 18, 2024, providing financial stability for the medium term.

While Q2 showed a slower growth rate compared to the 13.1% reported in Q1 2025, the significant improvements in gross margin and EBITDA suggest that Elektroimportøren’s focus on profitability is yielding results as it continues its strategic expansion across Norway and Sweden.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.