Street Calls of the Week

Introduction & Market Context

Element Solutions Inc (NYSE:ESI) released its second quarter 2025 earnings presentation on July 31, 2025, reporting 6% organic net sales growth and raising its full-year guidance. The specialty chemicals company, which closed at $23.72 on July 30, saw its stock decline 2.4% ahead of the earnings release.

The results build on momentum from the first quarter, when the company reported 5% organic growth and saw its stock surge over 7%. Element Solutions continues to benefit from strength in high-performance computing, telecom infrastructure, and advanced packaging materials, while navigating softer conditions in European industrial markets.

Quarterly Performance Highlights

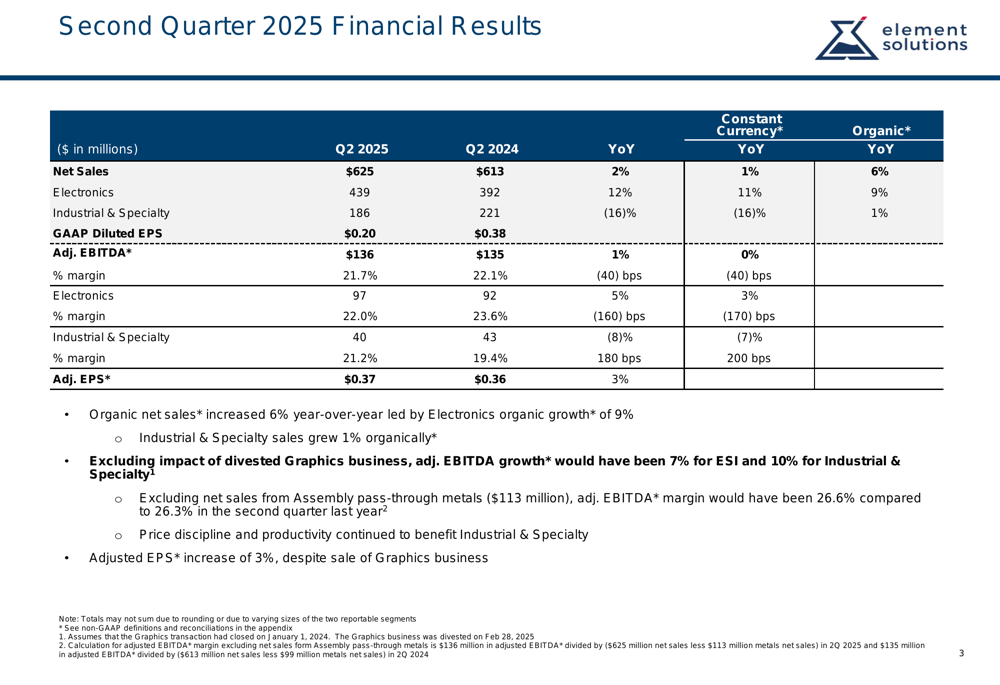

Element Solutions reported net sales of $625 million for Q2 2025, representing a 2% increase from $613 million in the same period last year. On an organic basis, which excludes the impact of currency, pass-through metals pricing, and divestitures, net sales grew by 6%.

Adjusted EBITDA reached $136 million, a 1% increase from Q2 2024, while adjusted earnings per share rose 3% to $0.37 from $0.36 in the prior-year period. The company’s GAAP diluted EPS was $0.20, down from $0.38 in Q2 2024.

As shown in the following financial results summary:

Notably, the company’s adjusted EBITDA margin was 21.7%, slightly down from 22.1% in Q2 2024. However, excluding net sales from Assembly pass-through metals ($113 million), the adjusted EBITDA margin would have been 26.6%, highlighting the underlying profitability of the business.

Segment Analysis

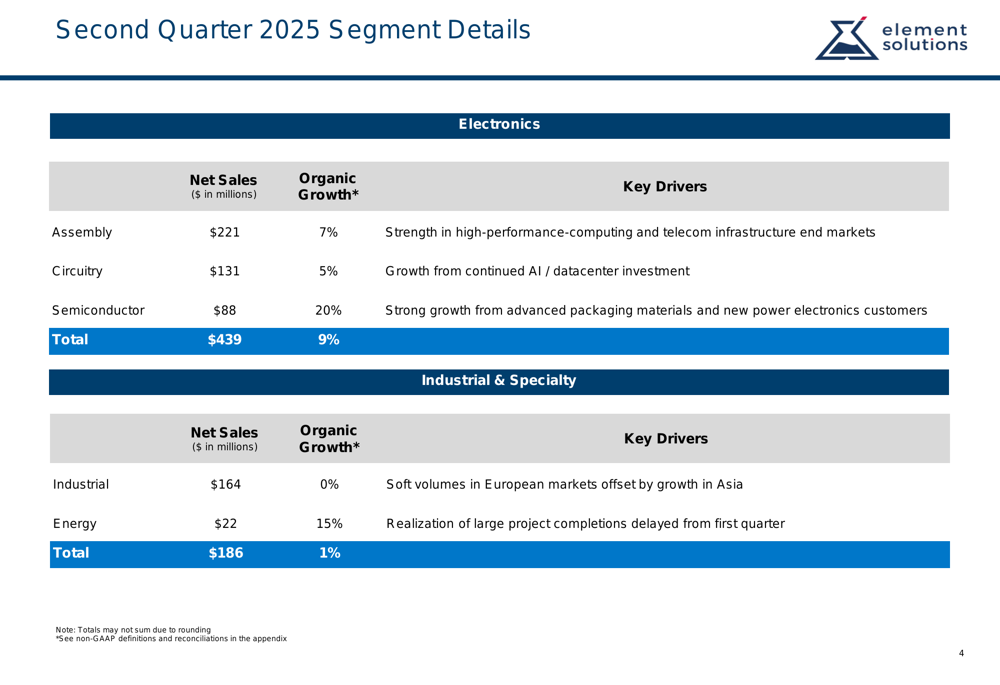

Element Solutions’ performance was driven primarily by its Electronics segment, which posted net sales of $439 million, up 12% year-over-year and 9% on an organic basis. Within Electronics, the Semiconductor business was particularly strong, with 20% organic growth driven by advanced packaging materials and new power electronics customers.

The Industrial & Specialty segment reported net sales of $186 million, down 16% year-over-year but up 1% organically. The decline in reported sales was largely due to the divestiture of the Graphics business. Excluding this impact, the segment’s adjusted EBITDA would have grown by 10%.

The detailed segment breakdown reveals varied performance across business lines:

The Energy business within the Industrial & Specialty segment showed particularly strong organic growth of 15%, driven by the completion of large projects that had been delayed from the first quarter. Meanwhile, the Industrial business reported flat organic growth, with weakness in European markets offset by growth in Asia.

Financial Position and Cash Flow

Element Solutions generated adjusted free cash flow of $59 million in Q2 2025, up from $52 million in the same period last year. The company maintained a solid balance sheet with a net debt to adjusted EBITDA ratio of 2.1x as of June 30, 2025.

During the quarter, Element Solutions repurchased approximately $20 million of shares at an average price of $20.45 per share, with $562 million remaining under its current share repurchase authorization. The company’s capital structure is fully fixed-rate through 2028, providing stability in the current interest rate environment.

The following slide details the company’s balance sheet and cash flow considerations:

Working capital investment increased by $35 million, primarily driven by accounts receivable growth from sales acceleration. However, inventory days continued to improve, indicating better operational efficiency. Capital expenditures totaled $18 million in the quarter, focused on growth investments.

Guidance and Outlook

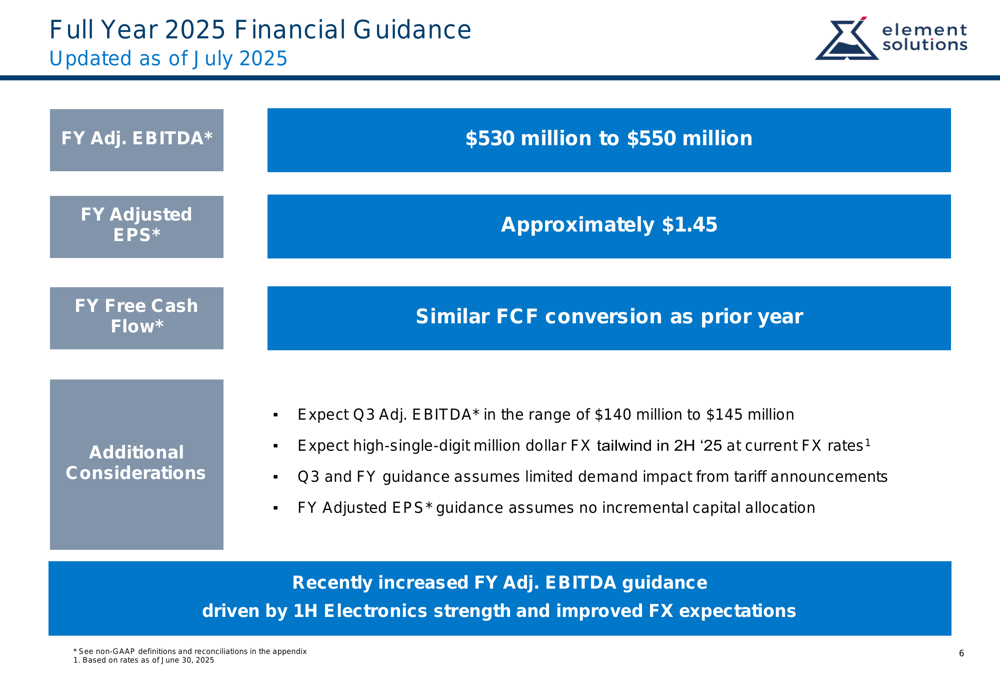

Element Solutions raised its full-year 2025 guidance, now expecting adjusted EBITDA of $530 million to $550 million, up from the previous range of $520 million to $540 million provided after Q1 results. The company also projects adjusted EPS of approximately $1.45 for the full year.

For the third quarter of 2025, management expects adjusted EBITDA in the range of $140 million to $145 million. The guidance assumes a high-single-digit million dollar foreign exchange tailwind in the second half of 2025 at current rates and limited demand impact from recent tariff announcements.

The updated outlook is presented in the following guidance slide:

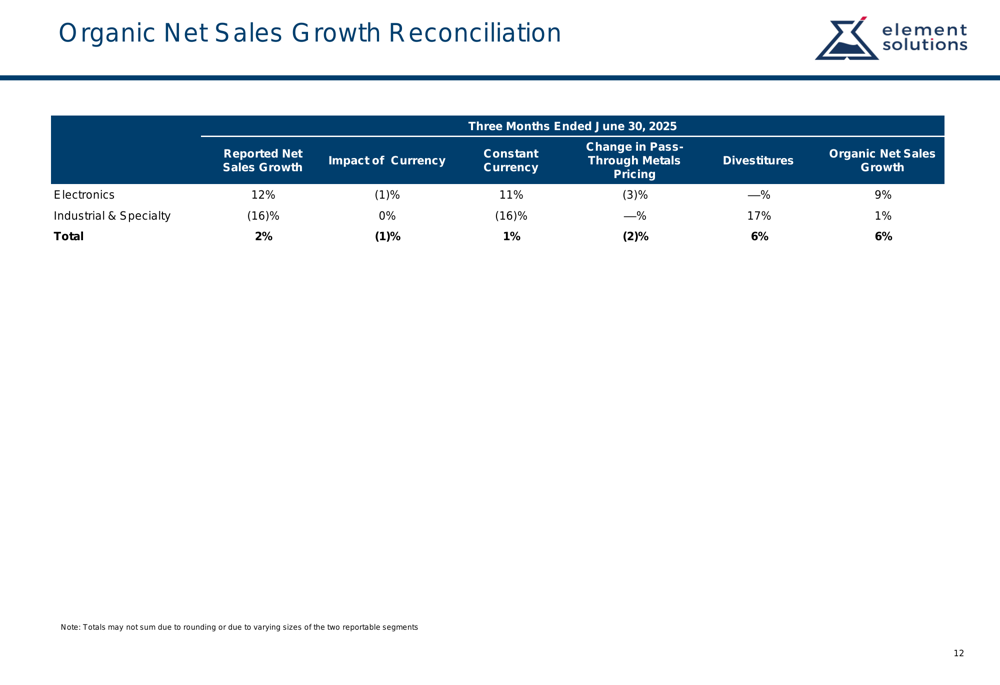

The company’s organic net sales growth calculation, which provides insight into underlying business performance by excluding currency effects, pass-through metals pricing changes, and divestitures, is detailed below:

Element Solutions’ improved guidance reflects continued strength in the Electronics segment and better foreign exchange expectations. This positive outlook builds on the momentum seen in the first quarter, when CEO Ben Glicklage emphasized the company’s strategic focus despite macroeconomic uncertainties.

With a diversified global manufacturing footprint and strong customer engagement in emerging technology areas, Element Solutions appears well-positioned to navigate market challenges while capitalizing on growth opportunities in high-performance computing, AI data centers, and advanced packaging materials through the remainder of 2025.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.