Street Calls of the Week

Eli Lilly and Company (NYSE:LLY) reported explosive revenue growth in its Q1 2025 earnings presentation on May 1, driven by continued strong performance of its GLP-1 receptor agonists for diabetes and obesity. Despite impressive financial results, the stock traded lower in premarket as the company reduced its full-year earnings guidance due to acquired IPR&D charges.

Executive Summary

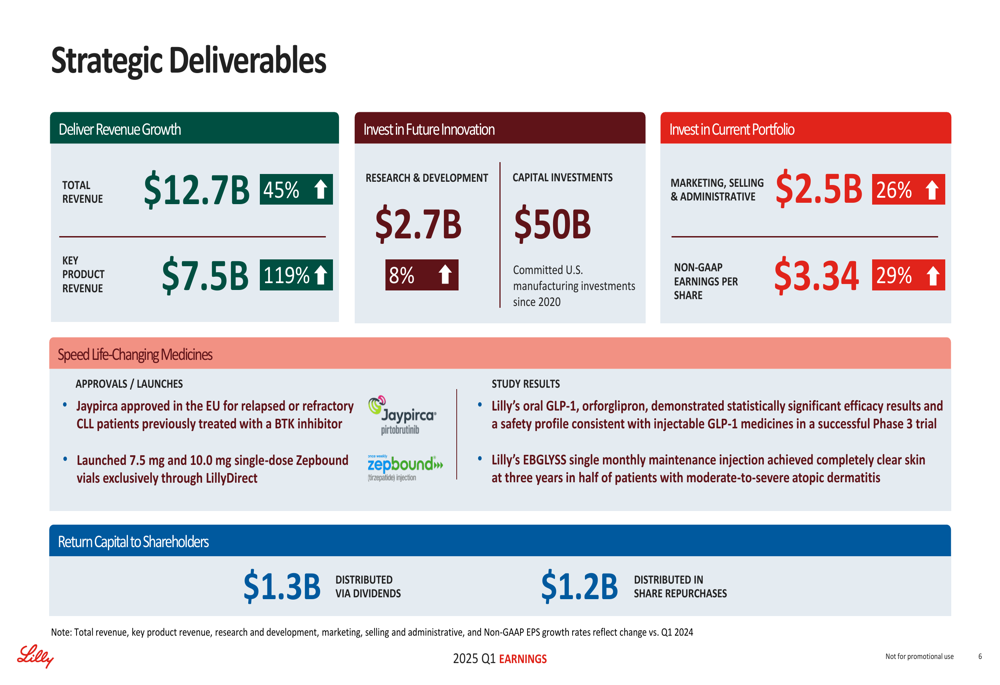

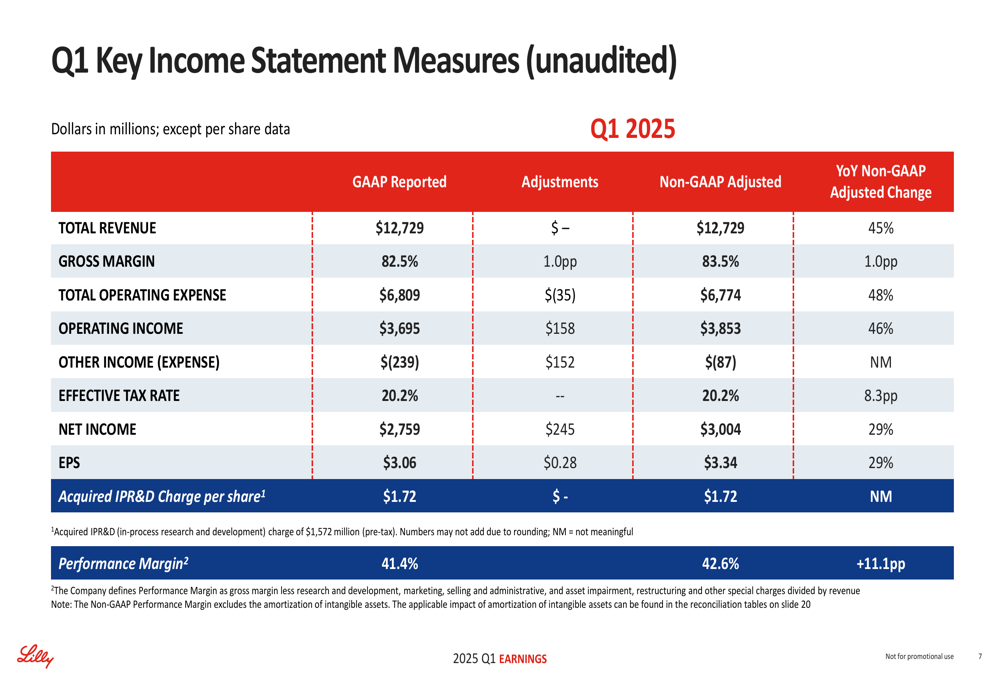

Eli Lilly reported Q1 2025 revenue of $12.7 billion, representing a 45% increase year-over-year, significantly outpacing the 42% growth reported in Q3 2024. The company’s key products, including Mounjaro, Zepbound, and Verzenio, generated $7.5 billion in revenue, a remarkable 119% increase compared to the same period last year.

Non-GAAP earnings per share reached $3.34, up 29% from Q1 2024, while GAAP EPS was $3.06, a 23% increase. The company maintained its 2025 revenue guidance of $58.0 billion to $61.0 billion but reduced its EPS guidance primarily due to a $1.72 per share acquired IPR&D charge in the first quarter.

As shown in the following comprehensive overview of Lilly’s strategic deliverables for the quarter:

Quarterly Performance Highlights

Eli Lilly’s remarkable revenue growth was primarily volume-driven, with volume contributing 53 percentage points to the overall 45% revenue increase, partially offset by a 6% price decrease. The company’s gross margin improved to 82.5%, up 1.6 percentage points year-over-year.

The company’s income statement revealed strong operational performance across key metrics:

Geographically, Lilly experienced robust growth across all regions, with Europe leading at 66% growth (71% at constant exchange rates). The U.S. market, which accounts for approximately two-thirds of total revenue, grew 49% year-over-year.

Product Performance

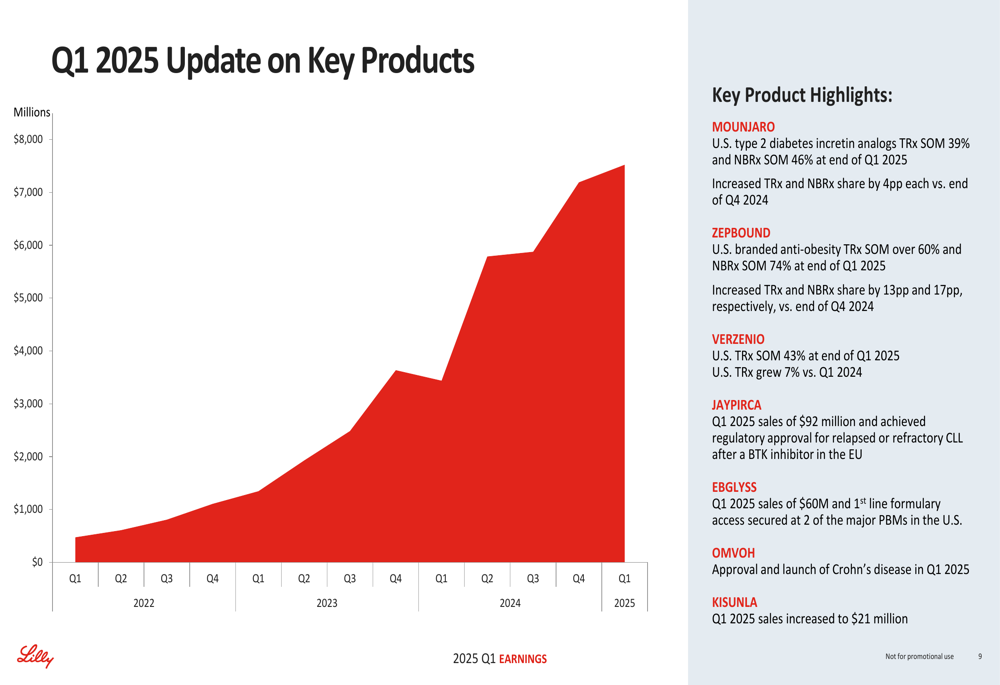

Lilly’s GLP-1 receptor agonists continued their remarkable growth trajectory. Mounjaro (tirzepatide for type 2 diabetes) generated $3.9 billion in global sales, with $2.7 billion coming from the U.S. market. Meanwhile, Zepbound (tirzepatide for obesity) contributed $2.3 billion, almost entirely from the U.S. market.

The following chart illustrates the performance of Lilly’s key products in Q1 2025:

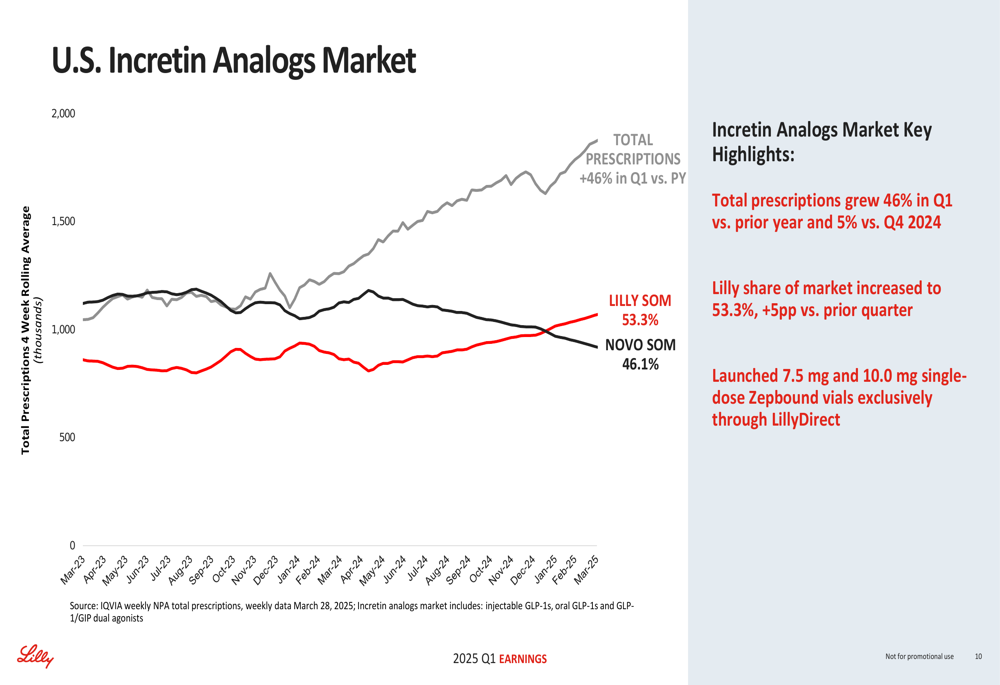

Notably, Lilly has achieved market leadership in the highly competitive U.S. incretin analogs market, with a 53.3% share compared to Novo Nordisk (NYSE:NVO)’s 46.1%. In the branded anti-obesity market, Zepbound has captured over 60% of total prescriptions and 74% of new prescriptions.

As shown in the following chart depicting Lilly’s market share gains in the incretin analogs market:

Strategic Initiatives

Eli Lilly announced plans to double its U.S. manufacturing investments to a total of $50 billion committed since 2020, highlighting the company’s confidence in sustained demand for its products, particularly its GLP-1 drugs. This investment aims to address the supply constraints that have limited the full commercial potential of Mounjaro and Zepbound.

The company also completed the acquisition of Scorpion Therapeutics’ mutant selective PI3Kα inhibitor program, strengthening its oncology pipeline. This acquisition contributed to the $1.72 per share acquired IPR&D charge that impacted the company’s full-year EPS guidance.

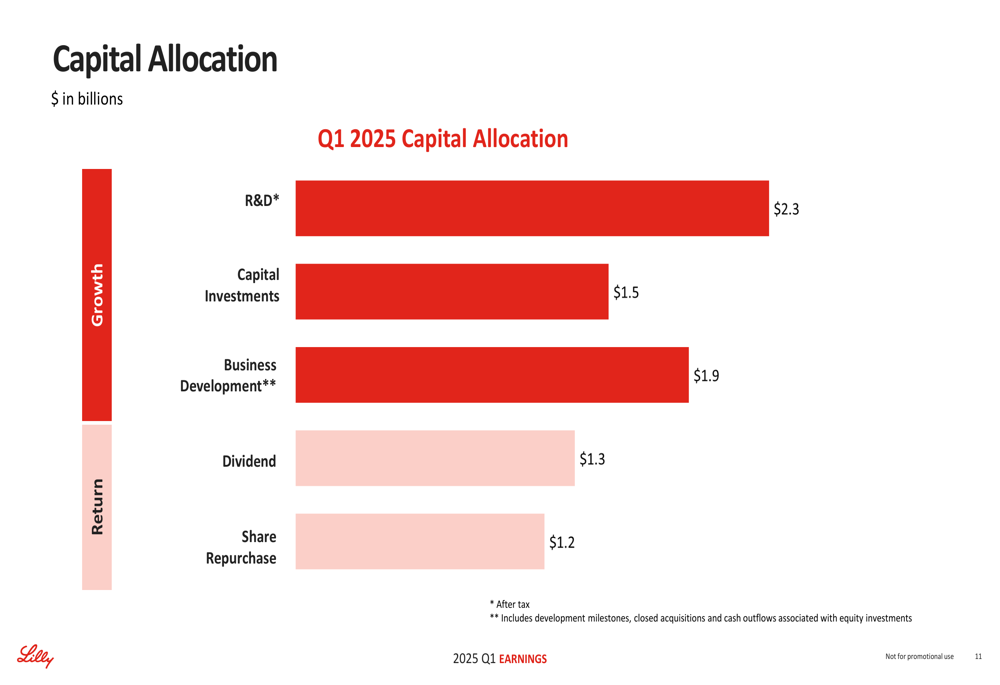

Lilly’s capital allocation strategy for Q1 2025 balanced investments in growth with returns to shareholders:

Pipeline Developments

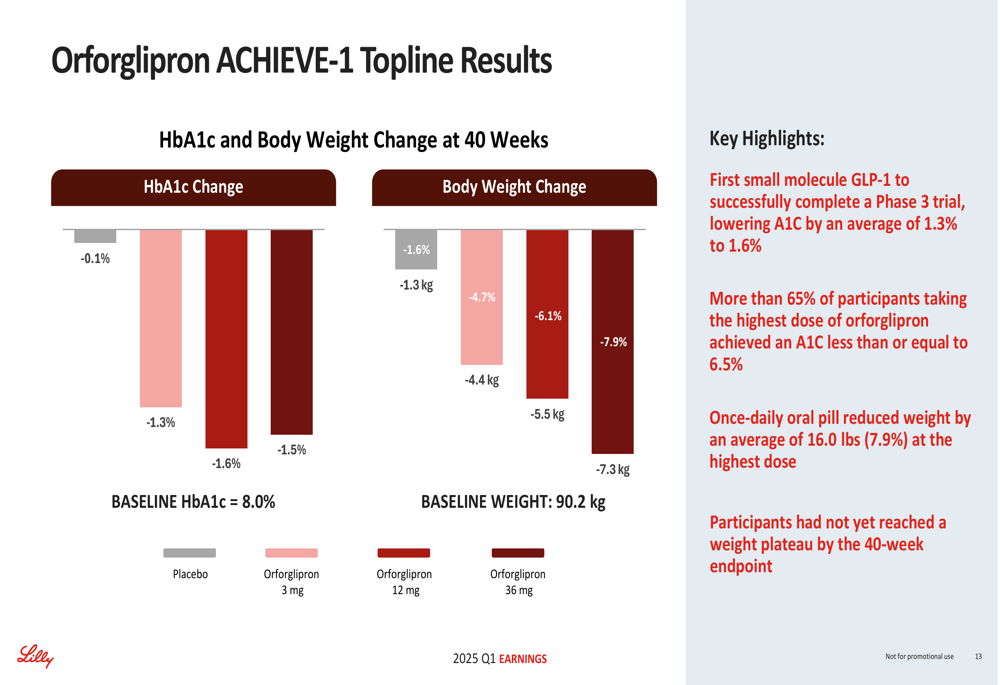

A significant highlight from the presentation was the positive Phase 3 results for orforglipron, Lilly’s oral GLP-1 receptor agonist. The ACHIEVE-1 trial demonstrated statistically significant reductions in HbA1c and body weight compared to placebo, with a safety profile consistent with injectable GLP-1 medicines.

The following chart shows the efficacy results from the ACHIEVE-1 trial:

If approved, orforglipron would be the first small molecule GLP-1 to reach the market, potentially expanding the addressable patient population by offering an oral alternative to injectable GLP-1 drugs. The company plans to submit regulatory applications for obesity in Q4 2025 and for type 2 diabetes in the first half of 2026.

Forward-Looking Statements

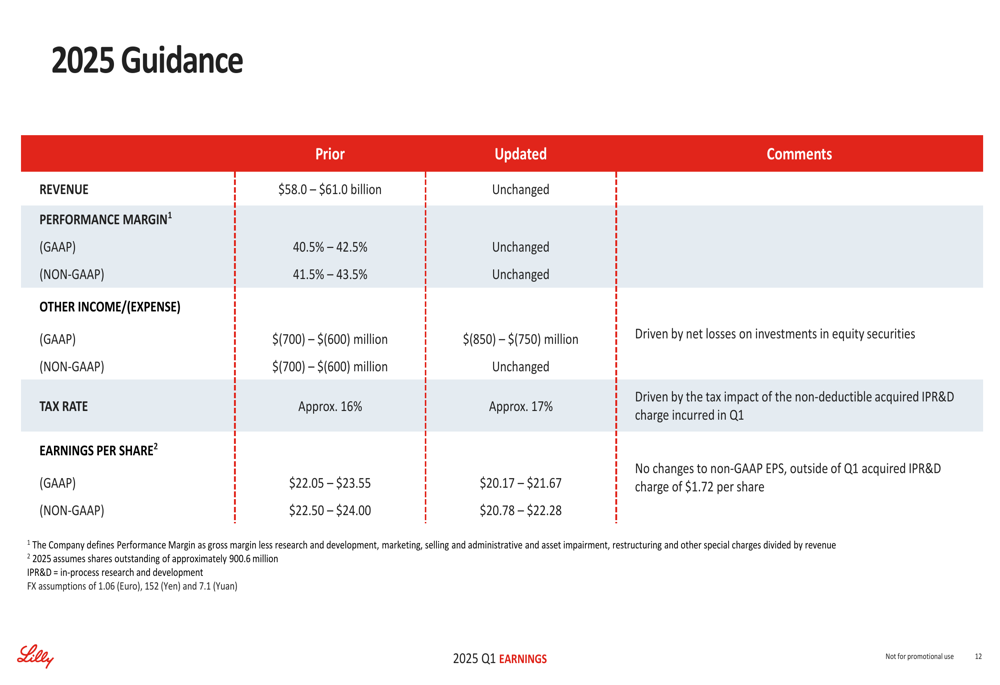

Despite strong Q1 results, Eli Lilly updated its 2025 guidance, maintaining revenue projections but reducing EPS expectations:

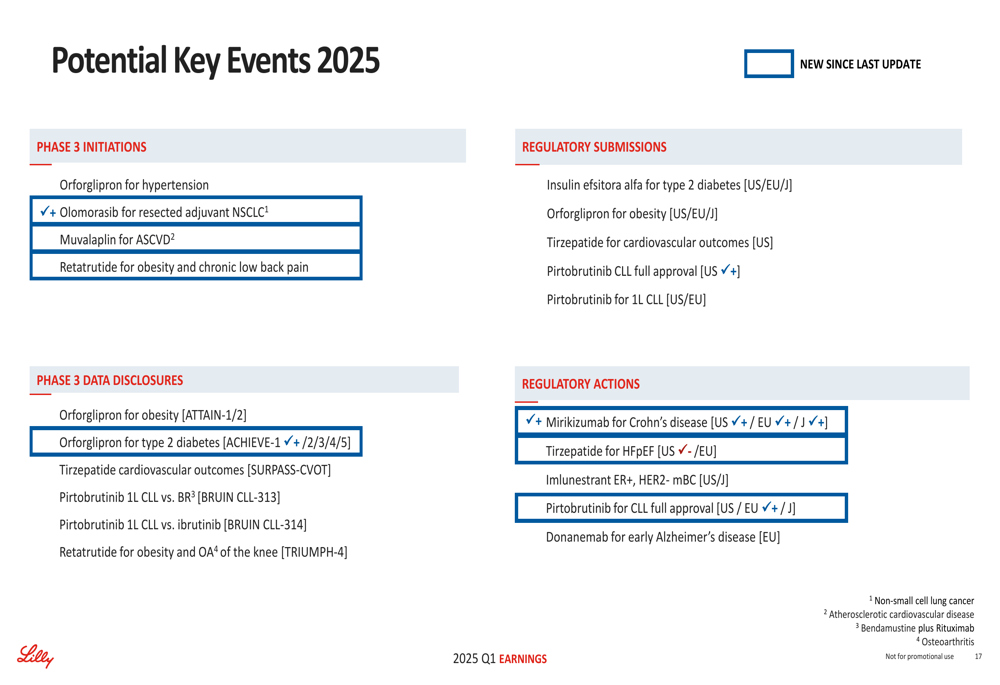

The company highlighted several potential key events for 2025, including multiple regulatory submissions and Phase 3 data disclosures:

Market Context

Despite the strong quarterly performance, Eli Lilly’s stock traded down 6.06% in premarket trading at $844.47, according to the provided fundamentals data. This decline likely reflects investor reaction to the reduced EPS guidance, despite the company maintaining its revenue outlook.

The stock had closed at $898.95 on April 30, 2025, representing a 1.55% gain in the previous session. Prior to this report, Lilly’s stock had been trading near its 52-week high of $972.53, reflecting investor optimism about the company’s growth trajectory.

Eli Lilly’s Q1 2025 results demonstrate the company’s continued dominance in the GLP-1 market, with its incretin analogs driving exceptional revenue growth. The positive Phase 3 results for orforglipron represent a potential game-changer in the GLP-1 space, as an oral option could significantly expand the addressable market.

While the reduced EPS guidance has temporarily dampened investor enthusiasm, the company’s strong revenue growth, market leadership position, and promising pipeline developments suggest Lilly remains well-positioned for continued success in the highly competitive diabetes and obesity treatment markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.