TPI Composites files for Chapter 11 bankruptcy, plans delisting from Nasdaq

Introduction & Market Context

Ellington Financial Inc. (NYSE:EFC) presented its first quarter 2025 earnings results on May 8, 2025, reporting net income of $0.35 per share and maintaining its attractive monthly dividend in a quarter marked by continued strategic portfolio rebalancing. The mortgage REIT, with a market capitalization of approximately $1.3 billion, continues to demonstrate resilience through its diversified investment approach despite fluctuating interest rate conditions.

The company’s shares closed at $12.78 on May 7, 2025, and showed minimal movement in after-hours trading, up just 0.27% to $12.81. This represents a significant decline from the $14.36 level seen after the Q4 2024 earnings release, suggesting investors may be digesting the quarter’s mixed results.

Quarterly Performance Highlights

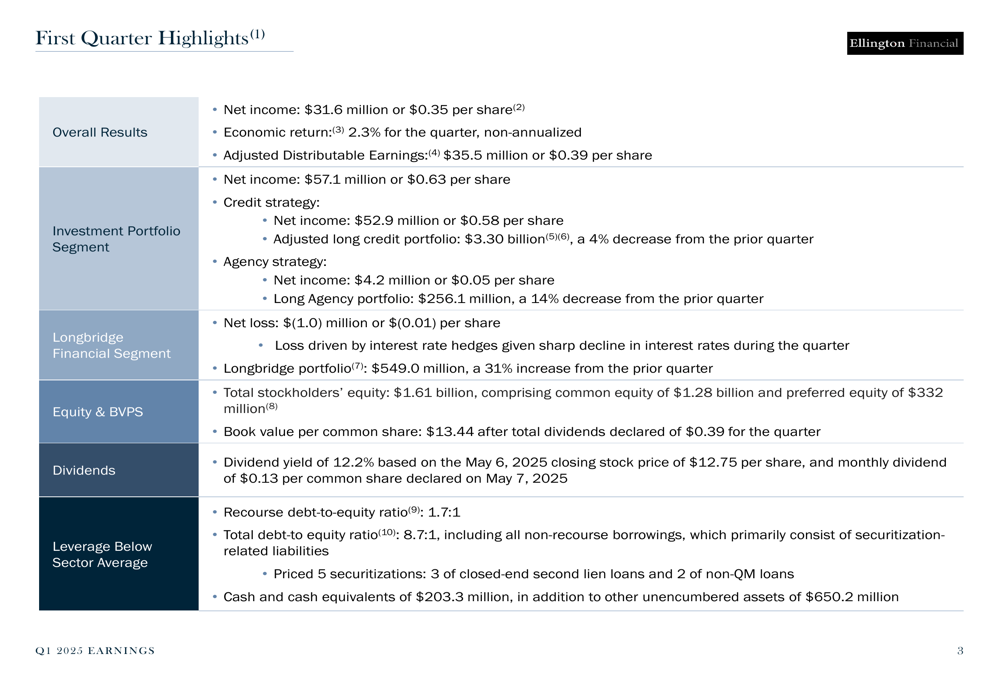

Ellington Financial reported net income of $31.6 million or $0.35 per share for Q1 2025, down from the $0.45 per share reported in Q4 2024. The company’s economic return for the quarter was 2.3% (non-annualized), while adjusted distributable earnings came in at $35.5 million or $0.39 per share.

As shown in the following comprehensive financial overview, the company’s performance varied significantly across its three main segments, with strong credit performance offset by weakness in the Longbridge segment:

The credit strategy was the standout performer, generating net income of $52.9 million or $0.58 per share, while the agency strategy contributed $4.2 million or $0.05 per share. However, the Longbridge Financial segment posted a net loss of $1.0 million or $0.01 per share, a significant reversal from the $0.30 per share contribution in Q4 2024, with the company attributing this primarily to interest rate hedges.

Total (EPA:TTEF) stockholders’ equity stood at $1.61 billion as of March 31, 2025, with book value per common share at $13.44 after accounting for total dividends of $0.39 declared during the quarter. The company maintained its monthly dividend of $0.13 per share, representing an annualized yield of 12.2% based on the May 6, 2025 closing price.

Portfolio Strategy and Composition

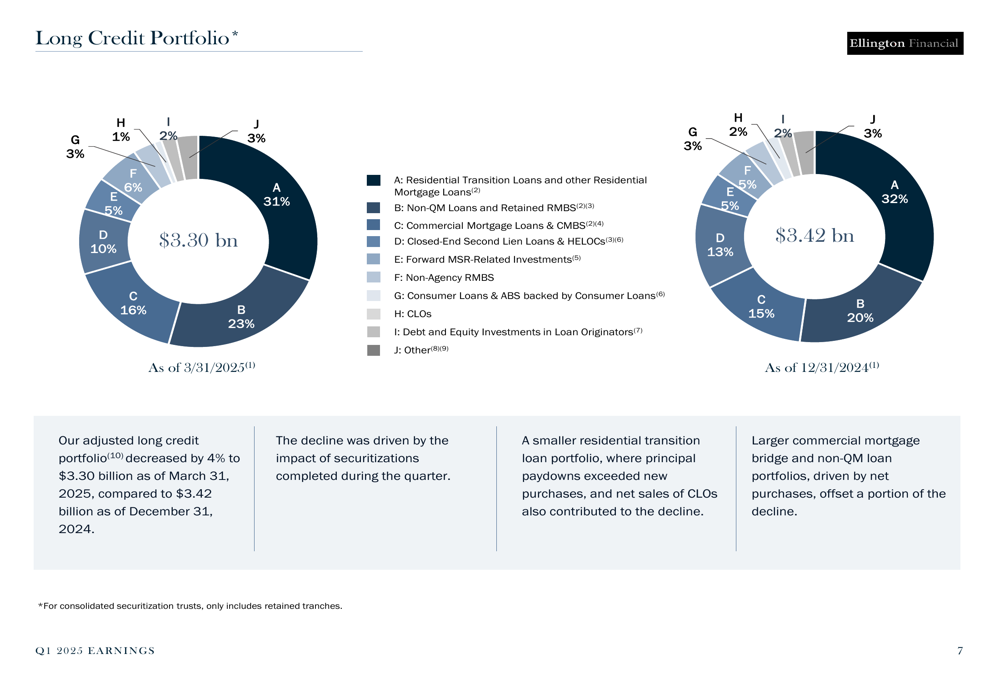

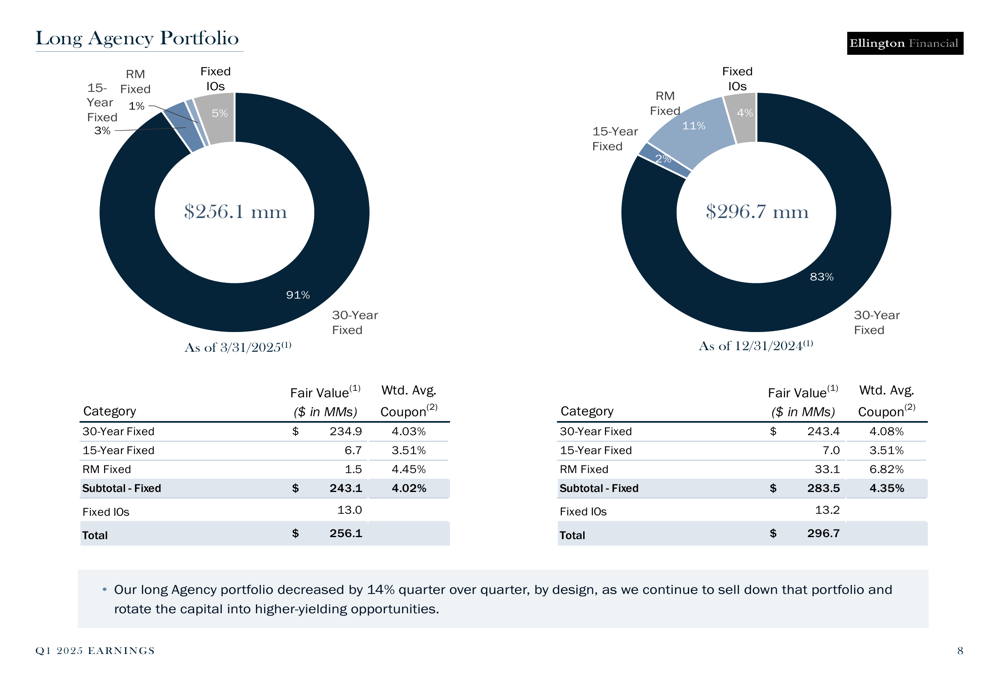

Ellington Financial continues to execute its strategic portfolio rebalancing, reducing exposure to lower-yielding agency mortgage-backed securities while expanding in higher-yielding sectors. The long credit portfolio decreased by 4% quarter-over-quarter to $3.30 billion, while the agency portfolio saw a more significant 14% reduction to $256.1 million.

The credit portfolio remains well-diversified across various asset classes, as illustrated in the following chart:

Residential transition loans and other residential mortgage loans comprise the largest portion at 31%, followed by non-QM loans and retained RMBS at 23%, and commercial mortgage loans and CMBS at 16%. The company noted that the quarter-over-quarter decline was primarily driven by securitizations completed during the quarter and a smaller residential transition loan portfolio.

Similarly, the agency portfolio composition continues to evolve, with a strong preference for 30-year fixed-rate securities:

Management emphasized that the reduction in agency exposure is strategic, noting: "The long Agency portfolio decreased by 14% quarter over quarter, as we continue to sell down that portfolio and rotate the capital into higher-yielding opportunities."

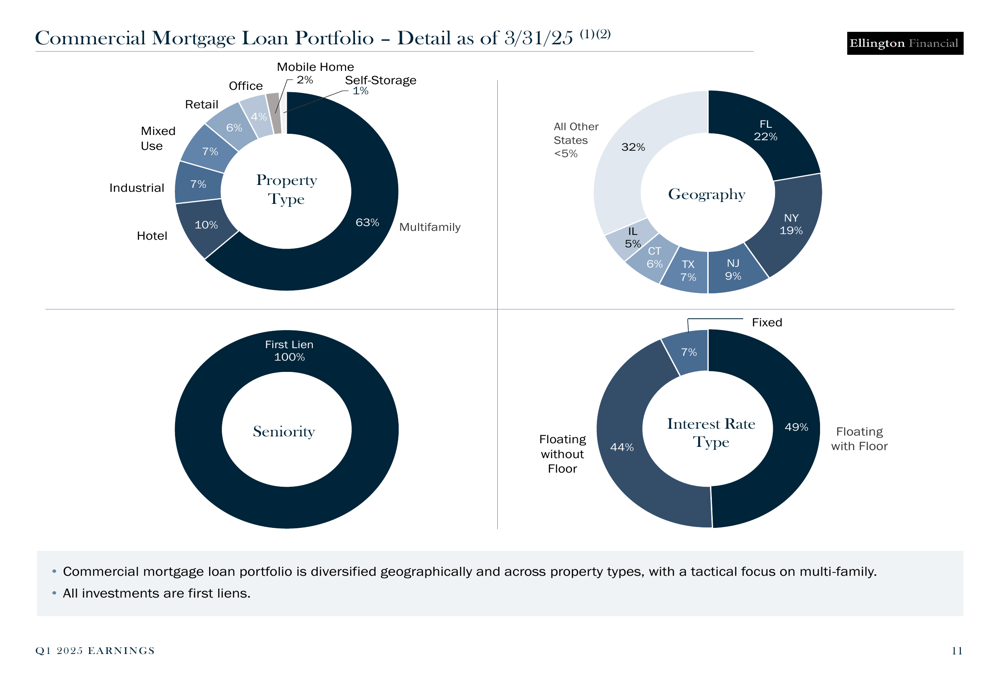

The commercial mortgage loan portfolio remains heavily weighted toward multifamily properties, which account for 63% of the total, with significant geographic diversification:

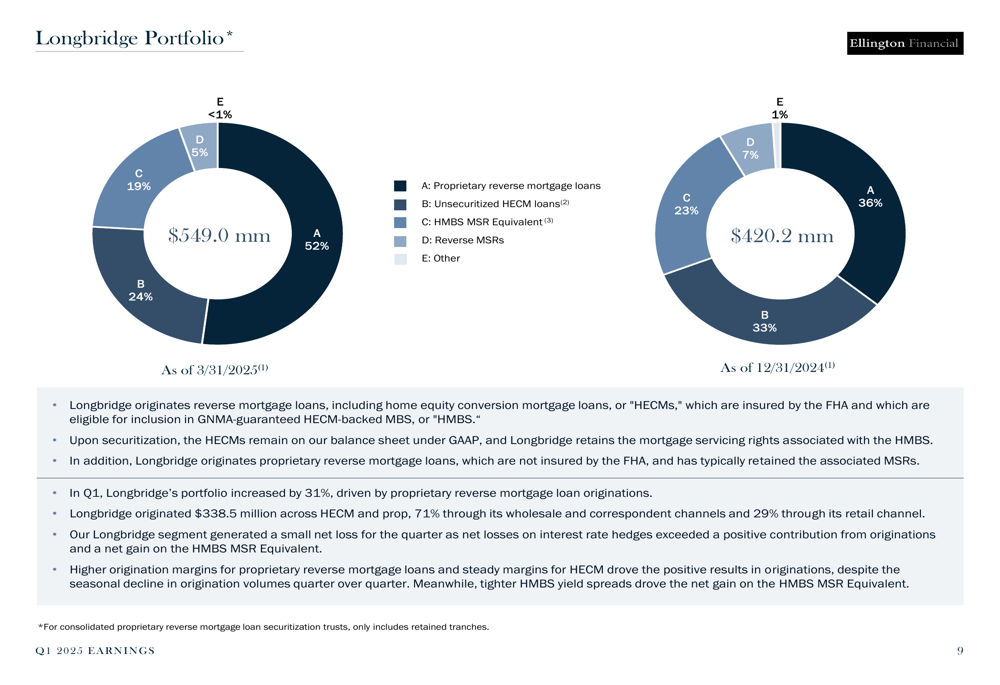

Longbridge Segment Growth

Despite posting a quarterly loss, the Longbridge Financial segment saw significant portfolio growth, increasing 31% quarter-over-quarter to $549.0 million. This growth was primarily driven by proprietary reverse mortgage loan originations.

The following chart illustrates the shifting composition of the Longbridge portfolio:

Proprietary reverse mortgage loans now represent 52% of the portfolio, up from 36% in the previous quarter, while unsecuritized HECM loans declined to 24% from 33%. During the quarter, Longbridge originated $338.5 million across HECM and proprietary loans, demonstrating strong execution in this specialized market segment.

This growth contrasts with the segment’s financial performance, which swung from a $0.30 per share contribution in Q4 2024 to a $0.01 per share loss in Q1 2025, primarily due to interest rate hedging impacts.

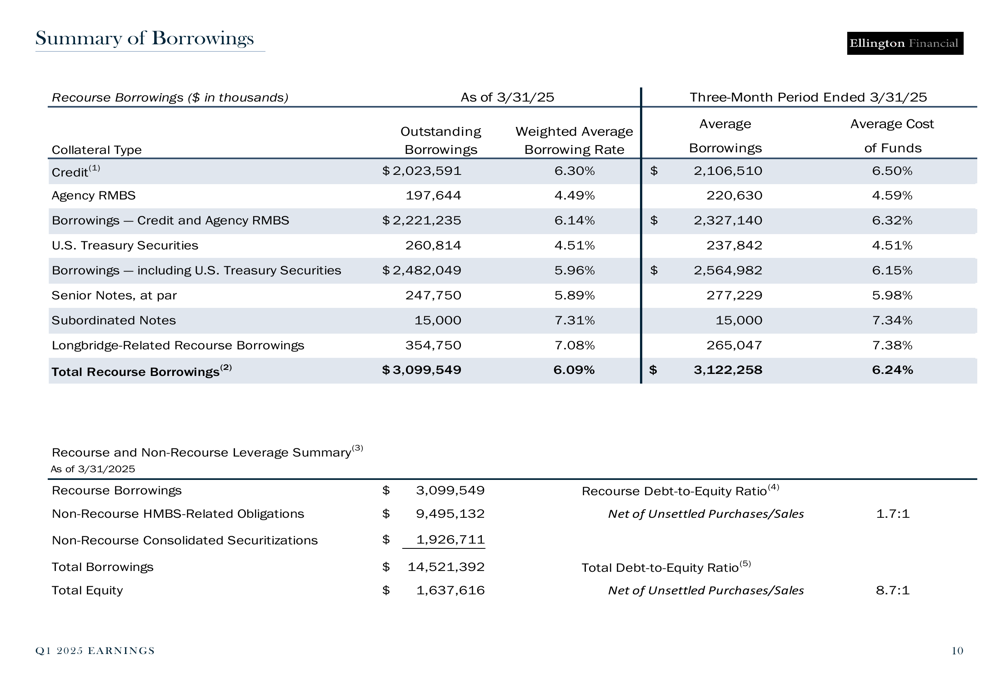

Risk Management and Stability

Ellington Financial maintains a conservative approach to leverage and risk management. The company reported a recourse debt-to-equity ratio of 1.7:1 and a total debt-to-equity ratio of 8.7:1, including all non-recourse borrowings.

The company’s borrowing summary provides a detailed breakdown of its financing structure:

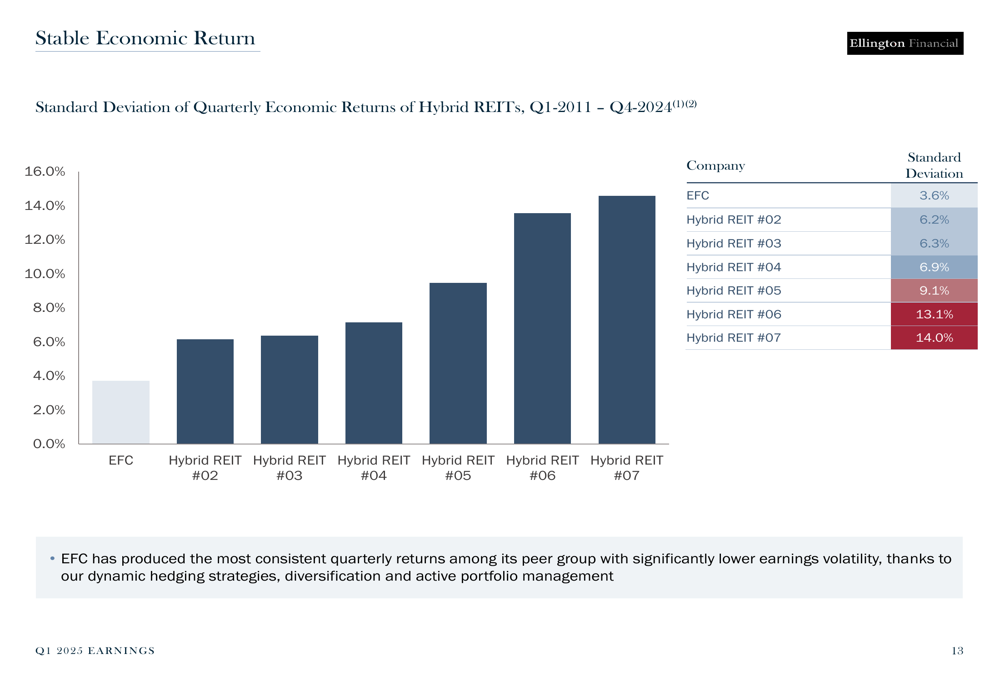

A key competitive advantage highlighted in the presentation is Ellington’s ability to generate stable economic returns with significantly lower volatility than peers:

With a standard deviation of quarterly economic returns of just 3.6%, Ellington Financial demonstrates substantially lower volatility compared to peer hybrid REITs, which range from 6.2% to 14.0%. This stability is attributed to the company’s dynamic interest rate hedging strategy and diversified portfolio approach.

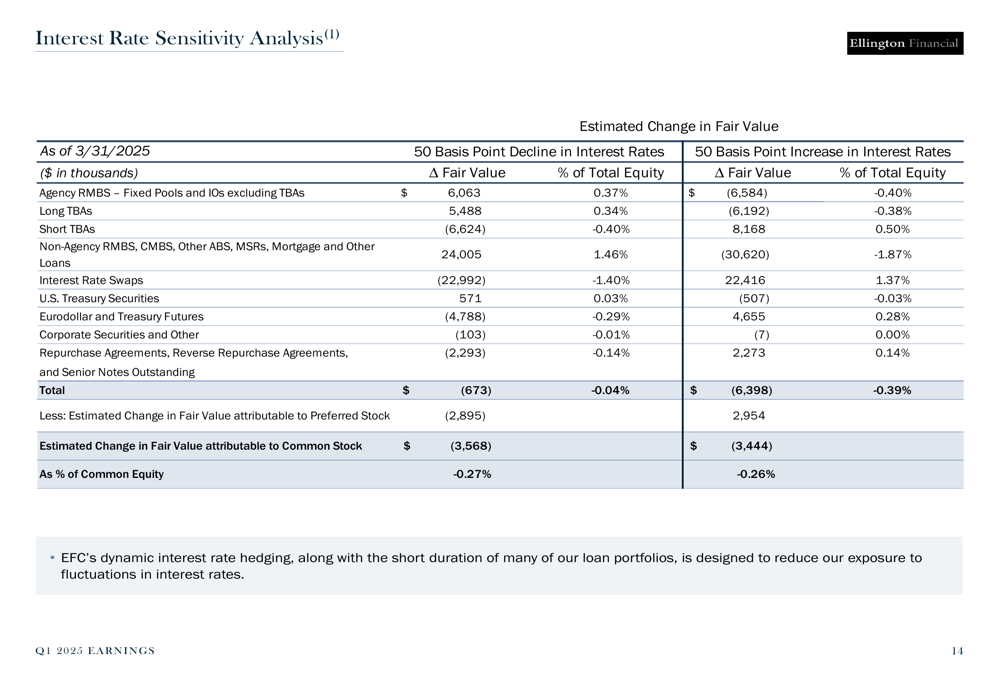

The company’s interest rate sensitivity analysis further illustrates its balanced risk profile:

A 50 basis point decline in interest rates would result in a minimal fair value change of -0.04% of total equity, while a 50 basis point increase would impact fair value by -0.39% of total equity, demonstrating the effectiveness of the company’s hedging strategy.

Strategic Initiatives and Forward Outlook

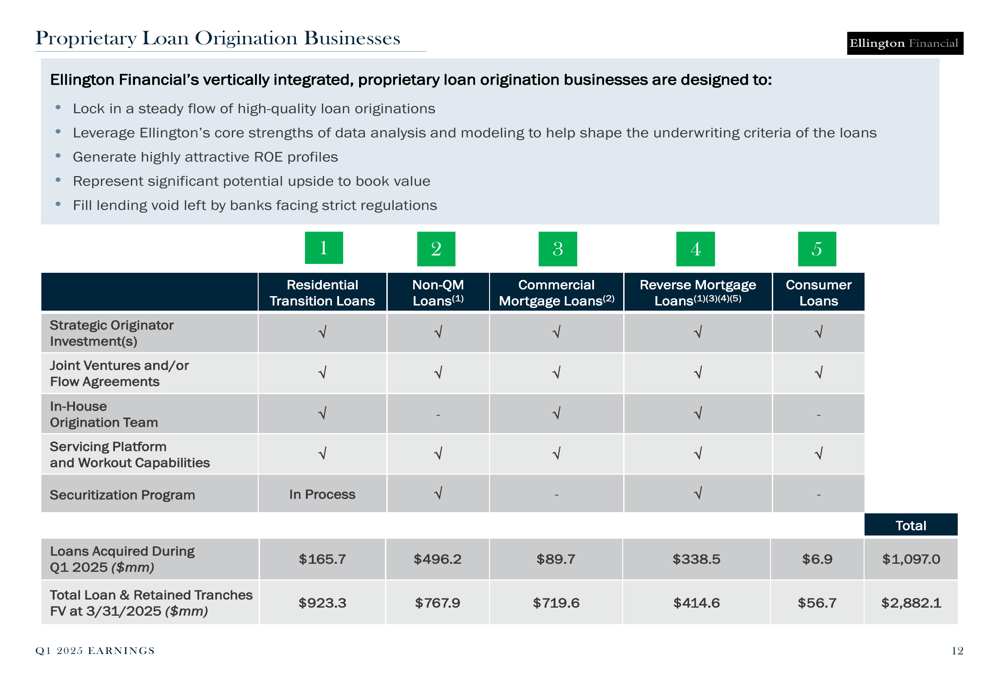

Ellington Financial continues to leverage its proprietary loan origination businesses across multiple sectors, providing a competitive advantage in sourcing attractive investment opportunities:

The matrix above illustrates the company’s involvement across residential transition loans, non-QM loans, commercial mortgage loans, reverse mortgage loans, and consumer loans, with significant volumes acquired during Q1 2025.

Looking forward, management emphasized several key strategic priorities:

1. Continuing to rotate capital from agency securities to higher-yielding credit investments

2. Expanding the Longbridge reverse mortgage business despite near-term hedging challenges

3. Maintaining the attractive dividend yield while focusing on book value stability

4. Leveraging proprietary origination channels to source unique investment opportunities

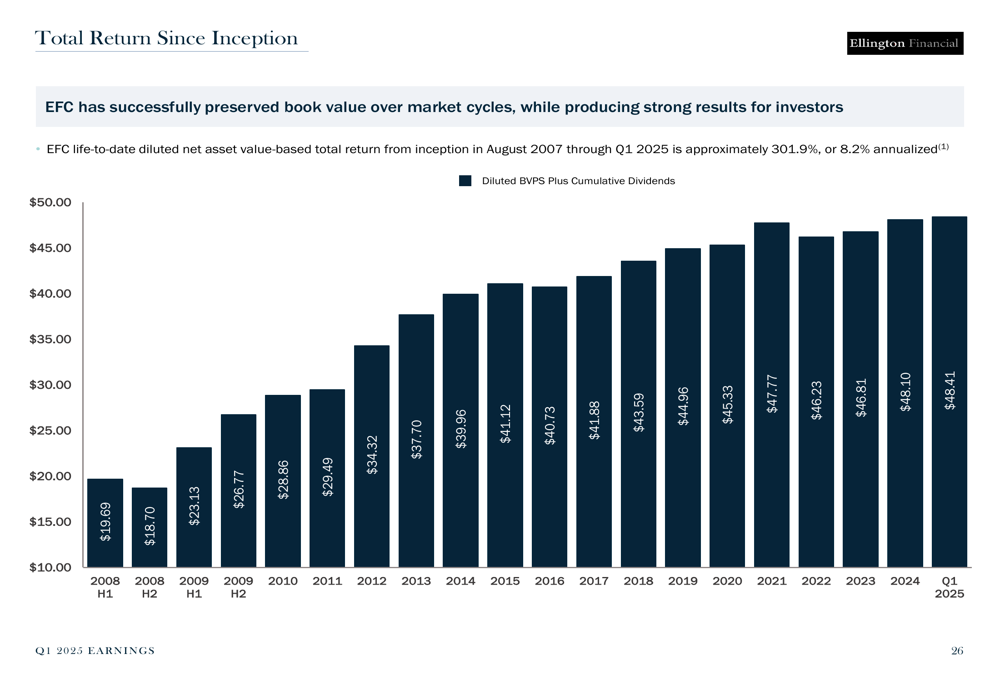

The company’s long-term performance record demonstrates consistent growth in book value plus cumulative dividends:

Since inception, Ellington Financial has delivered a total return of $48.41 per share (as measured by diluted book value per share plus cumulative dividends), reflecting its ability to generate attractive risk-adjusted returns across various market cycles.

While near-term challenges remain, particularly in the Longbridge segment and amid ongoing interest rate uncertainty, Ellington Financial’s diversified approach and conservative risk management position it to continue delivering attractive dividend yields with lower volatility than many of its peers.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.