Dell falls as soft current quarter guide offsets Q2 beat, full-year outlook lift

Introduction & Market Context

Elme Communities (NYSE:ELME) presented its May 2025 investor update highlighting the company’s strategic focus on affordable multifamily properties in the Washington and Atlanta metro areas. The presentation emphasized how Elme’s positioning in the mid-market rental segment provides insulation from new supply and supports stable occupancy and rent growth.

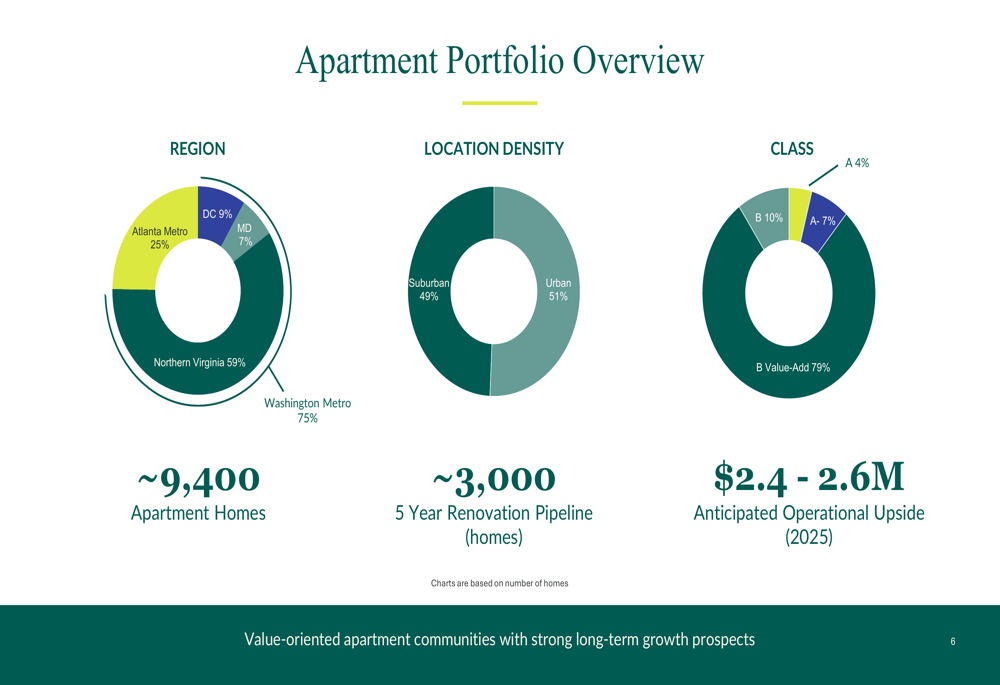

The multifamily REIT, which owns approximately 9,400 apartment homes, reported continued operational improvements and a substantial renovation pipeline aimed at driving NOI growth. With 75% of its portfolio in the Washington Metro area and 25% in Atlanta, Elme is leveraging research-led capital allocation to target submarkets with favorable supply-demand dynamics.

As shown in the following portfolio breakdown, Elme’s properties are strategically diversified across urban and suburban locations, with a strong emphasis on Class B value-add properties:

Quarterly Performance Highlights

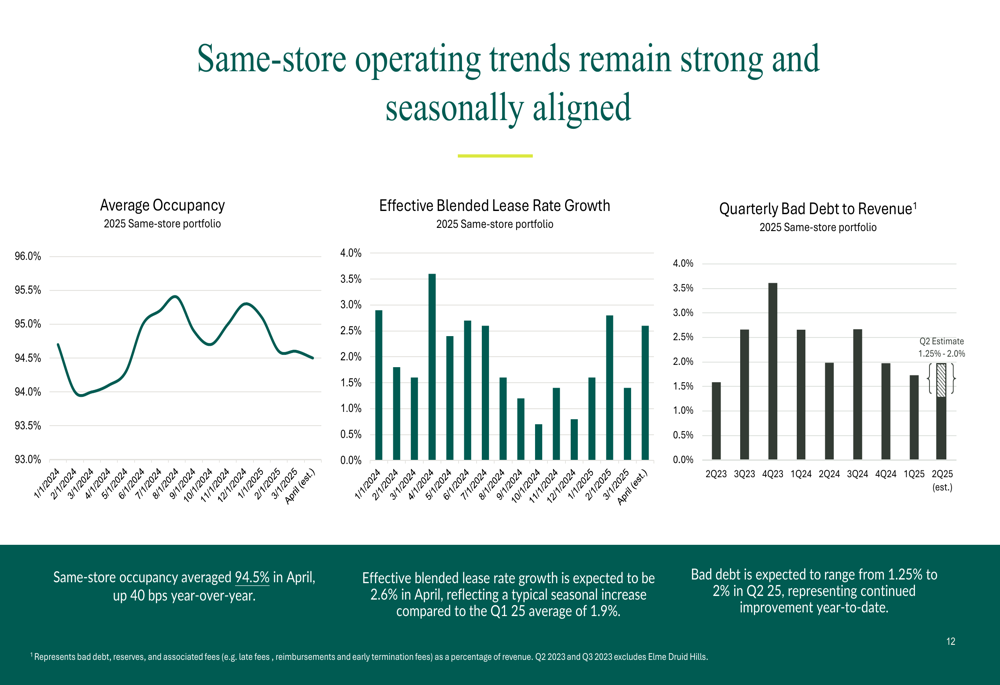

Elme reported solid operating metrics for Q1 2025, with occupancy trending upward and effective rent growth improving. Average occupancy reached 94.5% in April, up 40 basis points year-over-year, while effective blended lease rate growth accelerated to 2.6% in April compared to the Q1 average of 1.9%.

The company also highlighted continued improvement in bad debt, which is expected to range from 1.25% to 2% in Q2 2025, showing progress from previous quarters. These operating trends suggest stabilization and modest growth across Elme’s portfolio.

The following chart illustrates these positive trends in same-store operating metrics:

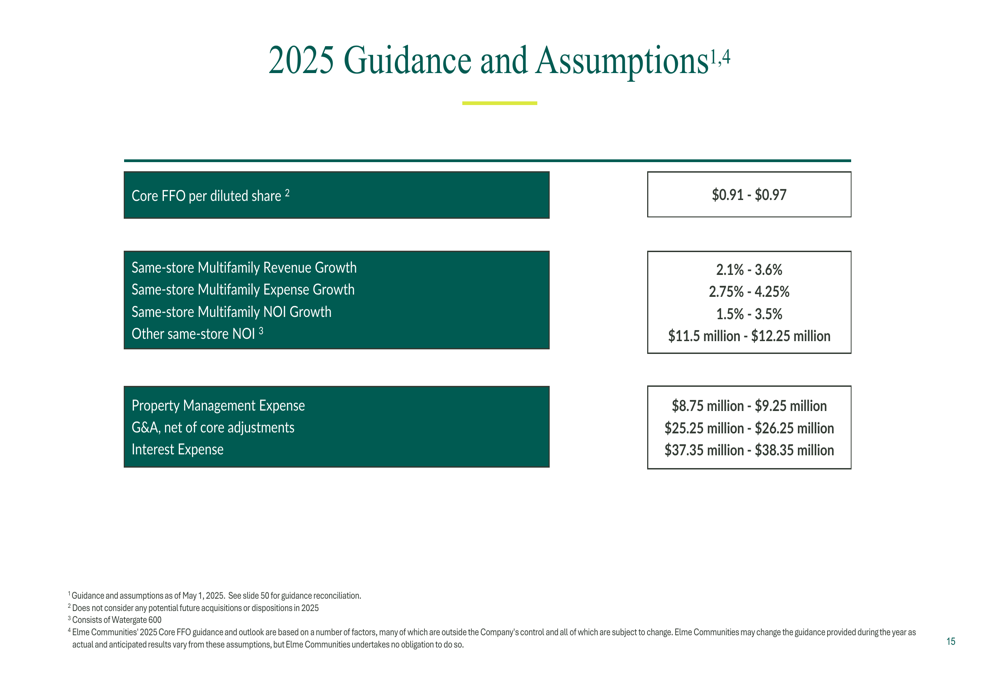

For full-year 2025, Elme provided guidance for core FFO per diluted share of $0.91-$0.97, with same-store multifamily revenue growth of 2.1%-3.6% and NOI growth of 1.5%-3.5%. This outlook reflects management’s confidence in the company’s operational initiatives and market positioning.

The complete 2025 guidance and assumptions are detailed below:

Strategic Initiatives

A key driver of Elme’s growth strategy is its renovation program, which encompasses approximately 3,000 units. The company reported an impressive ~18% ROI on renovations completed in Q1 2025, with costs ranging from $5,000 for partial renovations to $16,000 for full renovations. For 2025, Elme expects to invest approximately $8.6 million in renovation projects.

The renovation program’s impact is illustrated in the following slide, which shows before-and-after examples and the number of completed renovations:

Elme also highlighted operational improvements expected to generate $2.4-$2.6 million in NOI upside in 2025. These initiatives include optimized occupancy through faster unit turns and enhanced marketing, new fee streams from renter insurance and other services, and managed WiFi implementation across multiple communities.

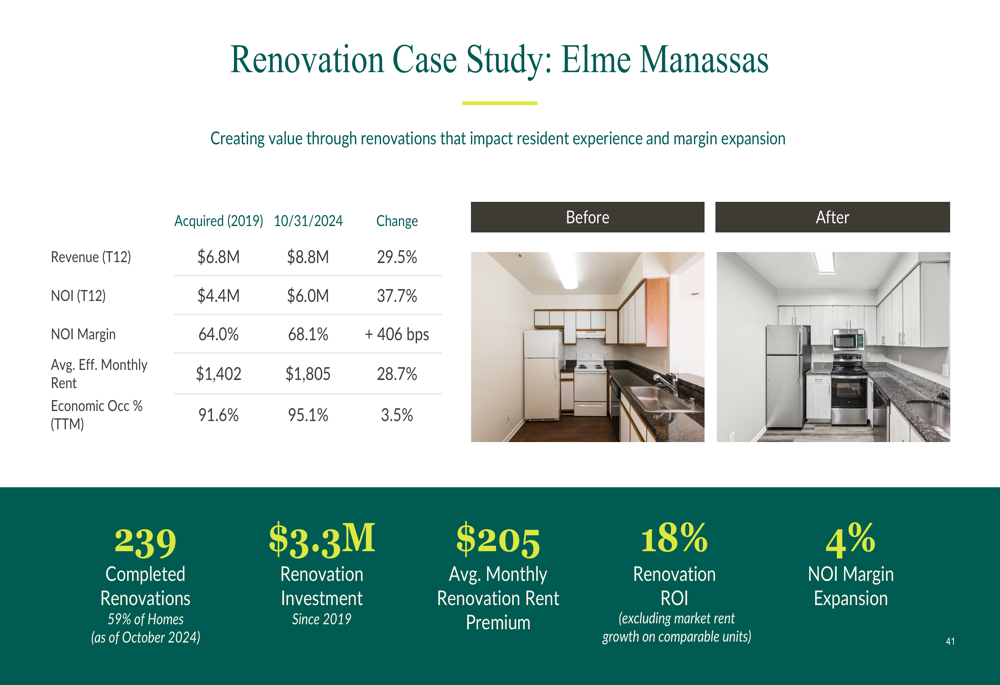

The company provided a compelling case study of its renovation strategy at Elme Manassas, where significant value has been created since acquisition:

Competitive Industry Position

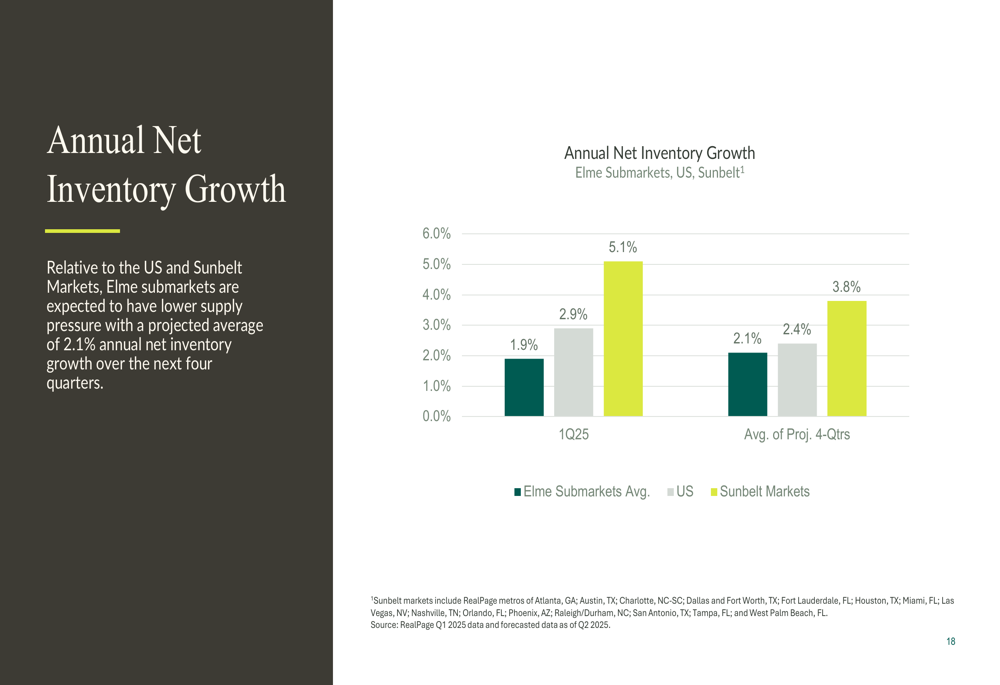

Elme’s investor presentation emphasized the company’s differentiated strategy of targeting affordable, mid-market rentals in submarkets with favorable supply-demand dynamics. Management highlighted that Elme’s submarkets are expected to experience lower supply pressure compared to national and Sunbelt markets, with projected annual net inventory growth of just 2.1% over the next four quarters.

The following chart illustrates this supply advantage:

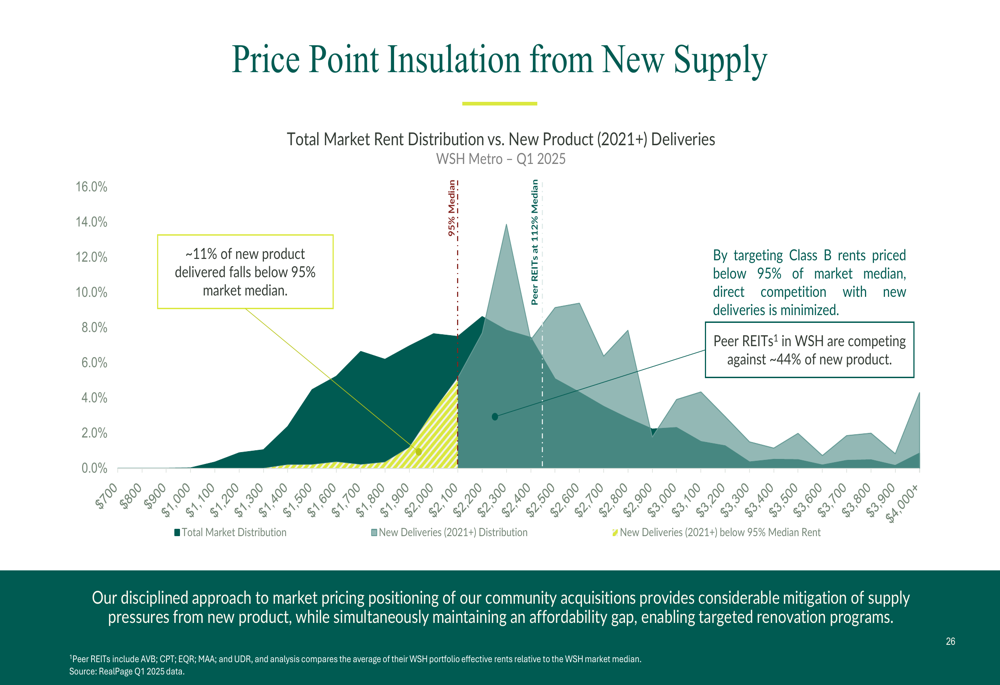

A key competitive advantage for Elme is its focus on properties with rents below 95% of market median, which provides insulation from competition with new deliveries. In the Washington Metro area, only about 11% of new product falls below this threshold, while in Atlanta, the figure is approximately 17%.

This strategic positioning is visualized in the following chart for the Washington Metro market:

Forward-Looking Statements

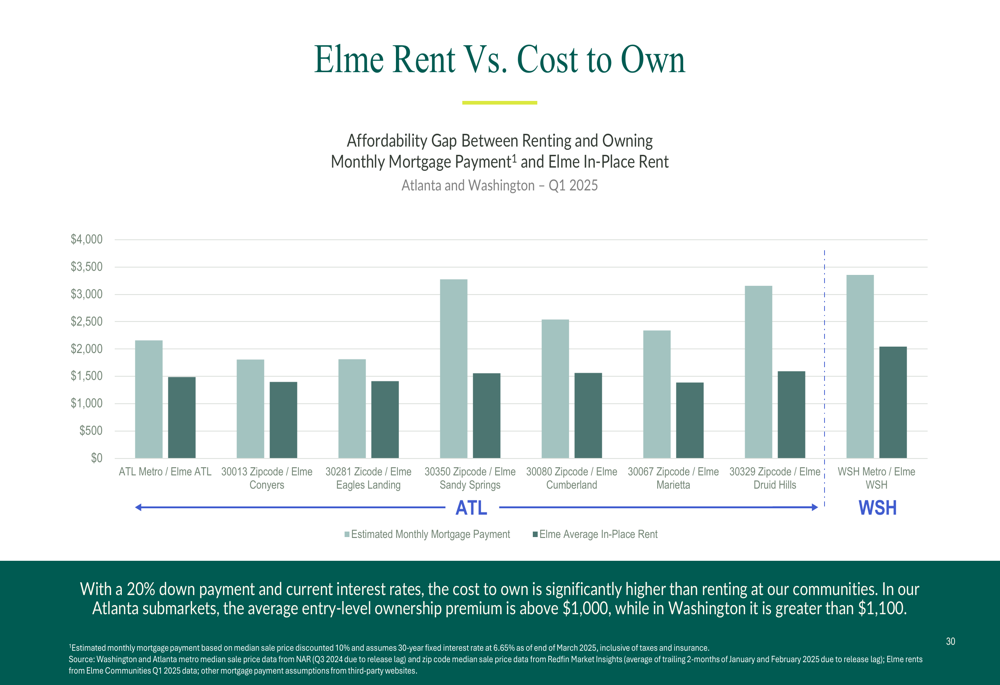

Elme’s presentation highlighted several factors supporting its long-term growth outlook. The company emphasized the significant affordability gap between renting at Elme communities versus homeownership, with the cost to own an entry-level home approximately 1.75 times higher than renting in Washington and 1.66 times higher in Atlanta.

This affordability advantage is illustrated in the following comparison:

The company also noted the declining construction activity in both the Washington (-54% change since peak) and Atlanta (-56% change since peak) metros, suggesting reduced new supply pressure in the coming years. Combined with strong absorption projections exceeding long-term averages, these trends support Elme’s positive outlook for its target markets.

Detailed Financial Analysis

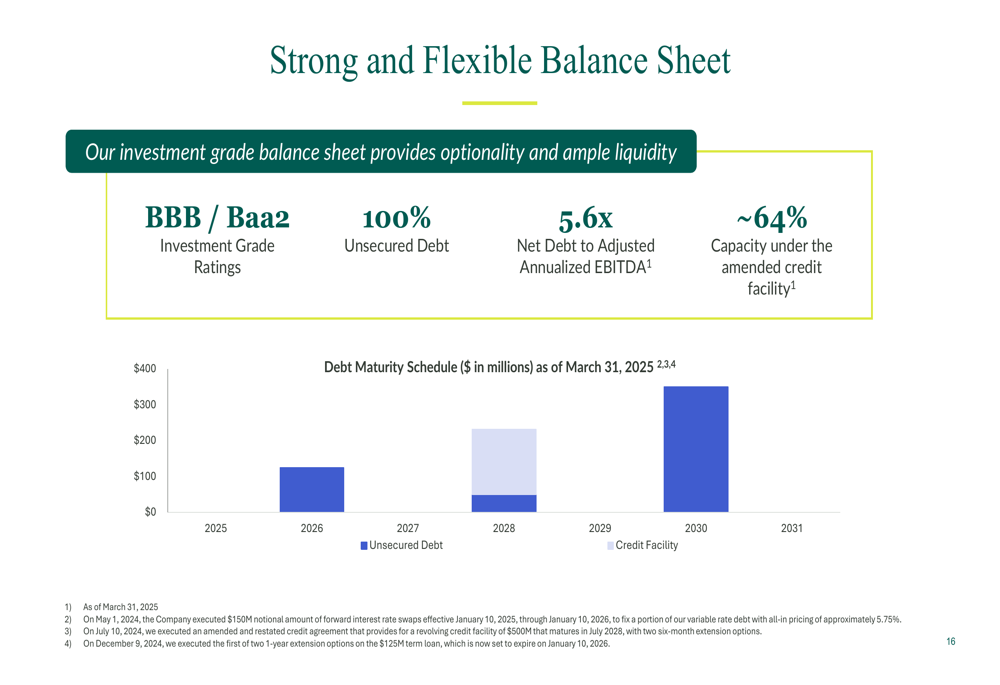

Elme emphasized its strong balance sheet, featuring BBB/Baa2 investment grade ratings and a net debt to adjusted EBITDA ratio of 5.6x. The company maintains 100% unsecured debt with no scheduled maturities until 2026, providing significant financial flexibility.

The debt maturity schedule and key balance sheet metrics are shown below:

The company’s sole remaining commercial asset, Watergate 600, is expected to generate NOI of $11.5-$12.25 million in 2025. This iconic building has a weighted average lease term of approximately 5.1 years and features high-quality institutional tenants.

It’s worth noting that in Elme’s Q3 2024 earnings call from November, the company reported the same 5.6x net debt to adjusted EBITDA ratio, indicating stable leverage levels over the past two quarters. The earnings call also mentioned potential monetization opportunities for assets like Watergate, though no specific updates were provided in the May 2025 presentation.

While the presentation highlighted positive trends across the portfolio, it’s important to note that the Q3 2024 earnings call identified challenges in the Atlanta market, including rent compression due to high inventory levels. The May 2025 presentation acknowledges regional differences but frames the outlook more positively, emphasizing declining construction activity and strong absorption projections in both markets.

Overall, Elme Communities’ May 2025 investor presentation portrays a company with a clear strategic focus on affordable multifamily properties, operational improvements driving NOI growth, and a strong balance sheet positioned for long-term growth in its target markets.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.