EUR/USD likely to find a peak near 1.25: UBS

Introduction & Market Context

Emera Incorporated (TSX:EMA) reported its strongest first quarter in company history on May 8, 2025, with significant growth across key financial metrics. The utility company, which closed at $61.35 on May 7, up 0.29% for the day, delivered exceptional performance amid continued progress on regulatory initiatives and strategic capital deployment.

The record results come as Emera continues to navigate a complex utility landscape, balancing infrastructure investments with customer affordability while managing interest rate and supply chain challenges.

Quarterly Performance Highlights

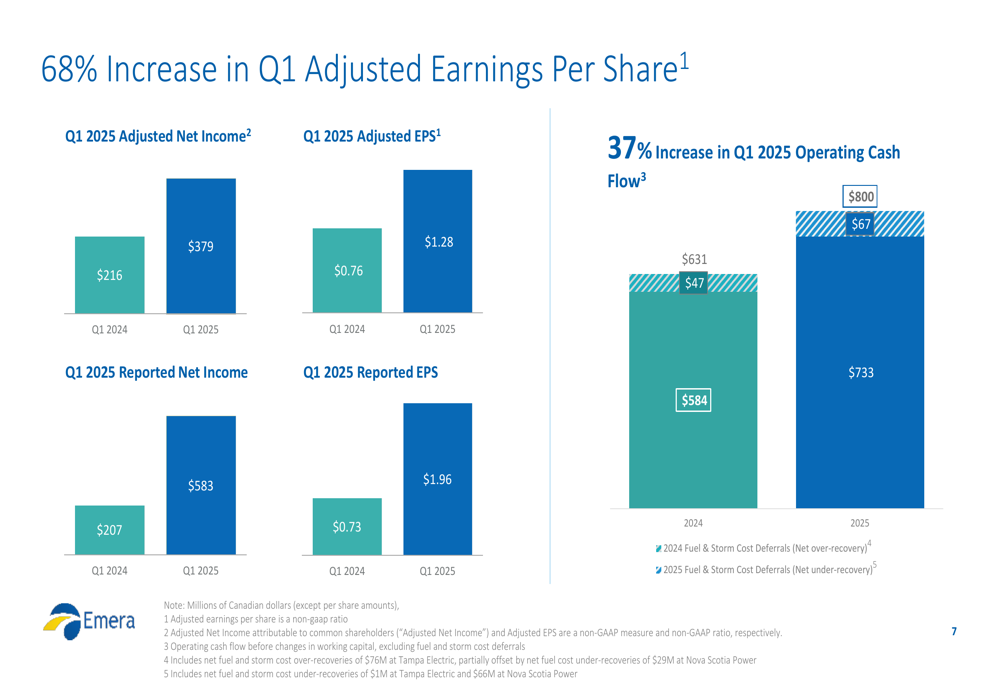

Emera reported a remarkable 68% increase in adjusted earnings per share for Q1 2025, reaching $1.28 compared to $0.76 in the same period last year. Adjusted net income attributable to common shareholders surged to $379 million, up from $216 million in Q1 2024.

As shown in the following earnings breakdown:

Reported net income showed even stronger growth, reaching $583 million ($1.96 per share) versus $207 million ($0.73 per share) in Q1 2024. Operating cash flow before changes in working capital and excluding fuel and storm cost deferrals increased by 37% to $800 million, compared to $631 million in the prior year.

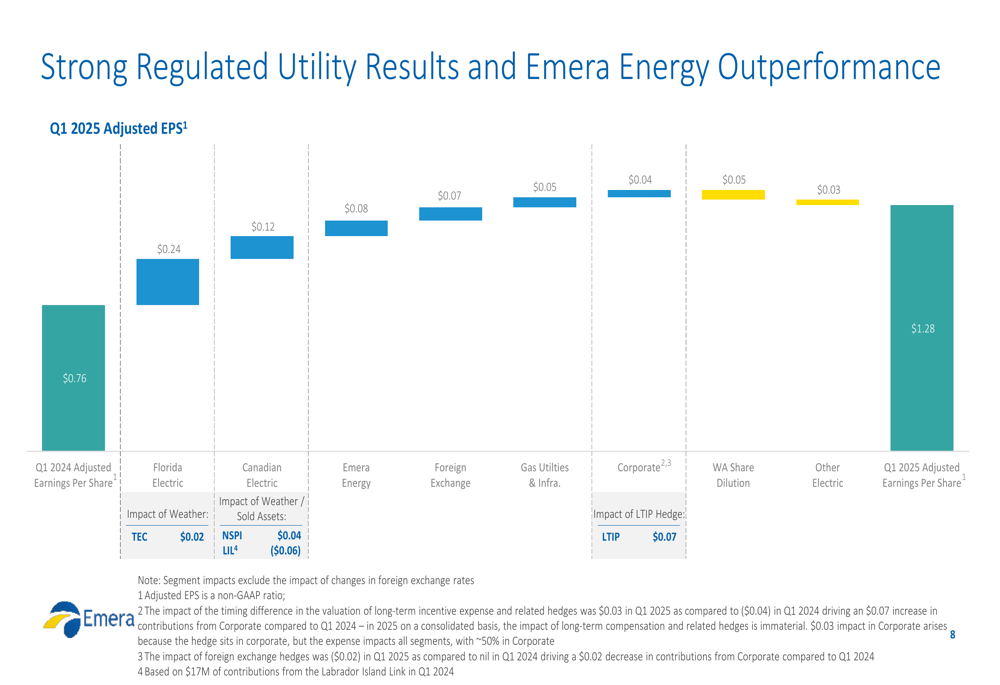

The impressive quarterly performance was driven by contributions across multiple business segments, with Florida Electric operations leading the way with a $0.24 contribution to the adjusted EPS growth. Canadian Electric utilities added $0.12, while Emera Energy contributed $0.08 to the year-over-year improvement.

The following waterfall chart illustrates the contribution of each business segment to the overall adjusted EPS growth:

Strategic Initiatives

Emera reported strong progress on its capital deployment strategy, having invested 22% of its forecasted 2025 capital in the first quarter. The company has successfully de-risked its supply chain for major capital projects and secured solar panels for investments through 2026, with no related tariff risk through 2029.

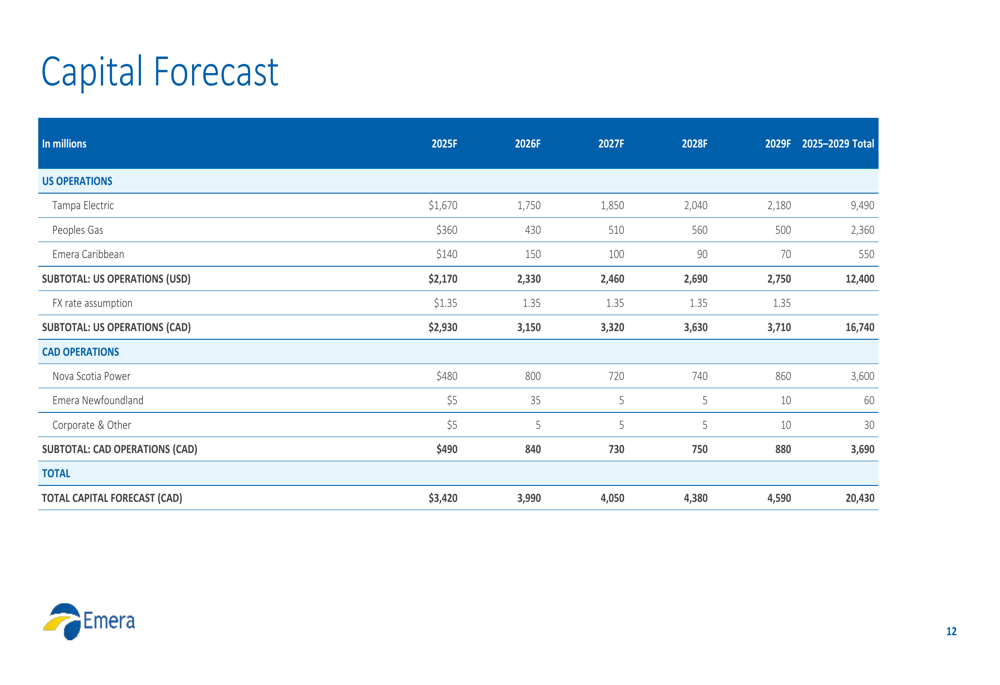

The company’s five-year capital plan of $20 billion is expected to drive 7-8% rate base growth. This investment is strategically allocated across reliability and grid modernization projects ($13.17 billion), renewable energy integration ($3.59 billion), technological innovation ($2.07 billion), and other initiatives ($1.6 billion).

Emera’s capital forecast by operating segment is detailed below:

On the regulatory front, Emera’s subsidiary Peoples Gas filed a general rate application on March 31, 2025, requesting revenue requirements of $104 million USD in 2026 and $27 million USD in 2027. The application includes a requested increase in the return on equity midpoint to 11.1% from the current 10.15%. Hearings are scheduled for September 9-12, 2025, with a final decision expected in Q4 2025 and new rates anticipated to take effect on January 1, 2026.

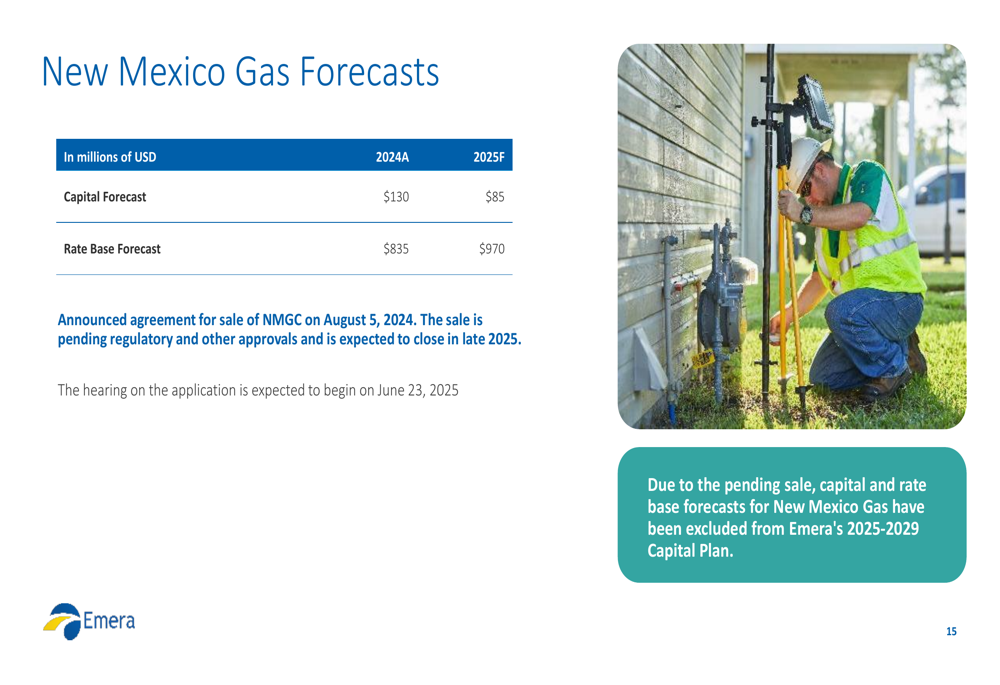

Additionally, Emera continues to progress with the previously announced sale of New Mexico Gas, with a regulatory hearing scheduled to begin on June 23, 2025, and an expected closing date in Q4 2025.

Risk Management

Emera has taken proactive steps to mitigate interest rate and foreign exchange exposures. As of March 31, 2025, the company reported only 11% variable rate debt, with no material maturities remaining in 2025. Management highlighted the balance sheet flexibility to address 2026 hybrid securities.

The company has also implemented a comprehensive foreign exchange hedging strategy, with 65% of USD earnings hedged at a rate of $1.36 for 2025, 27% hedged at $1.38 for 2026, and 13% hedged at $1.38 for 2027. On a hedge-adjusted basis, each $0.01 change in the exchange rate translates to approximately $0.01 impact on adjusted EPS in 2025.

The following chart details Emera’s debt composition and foreign exchange hedging position:

Forward-Looking Statements

Based on the strong Q1 performance, Emera expressed confidence in achieving 5-7% average adjusted EPS growth for the 2025-2027 period. This would translate to adjusted EPS reaching $3.43 at a 5% CAGR or $3.63 at a 7% CAGR by 2027, building on the 2024 adjusted EPS of $2.94.

The company’s rate base is projected to grow at a compound annual growth rate of 7.1% from 2023 to 2029, reaching $38.27 billion by the end of the forecast period. This growth is expected to be driven primarily by US operations, which are forecasted to grow at an 8.6% CAGR, while Canadian operations are projected to grow at a more modest 3.0% CAGR.

The rate base forecast by segment is illustrated in the following table:

Conclusion

Emera’s Q1 2025 results represent a strong start to the year, with record performance across key financial metrics. The company’s strategic focus on regulated utility growth, coupled with prudent risk management and disciplined capital deployment, positions it well to deliver on its long-term growth targets.

With regulatory proceedings progressing as expected and strategic initiatives on track, Emera appears well-positioned to navigate the evolving utility landscape while delivering value to shareholders. Investors will be watching closely to see if the company can maintain this momentum through the remainder of 2025 and beyond.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.