Nvidia among investors in xAI’s $20bn capital raise - Bloomberg News

Emerson Electric Company (NYSE:EMR) reported strong second-quarter 2025 results on May 7, exceeding guidance on key metrics while successfully navigating tariff challenges. The industrial technology giant raised its full-year earnings outlook, citing improving discrete markets and continued strength in its core process and hybrid businesses.

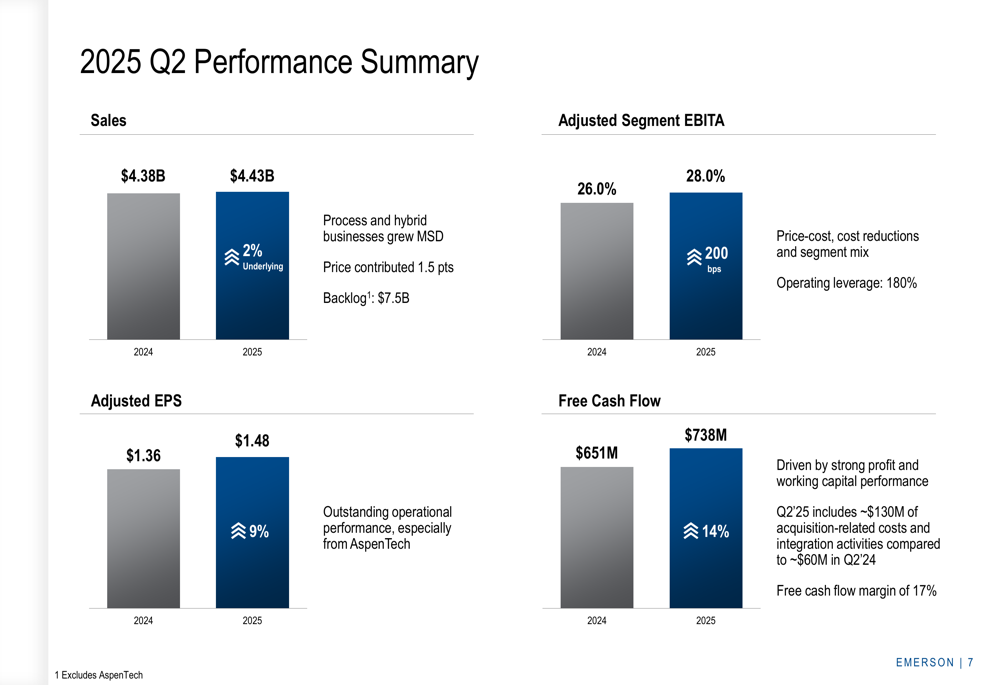

Quarterly Performance Highlights

Emerson delivered exceptional second-quarter results, with underlying orders growth of 4% across all regions. The company reported underlying sales growth of 2%, hitting the top end of its guidance range, while adjusted earnings per share reached $1.48, exceeding the top of guidance by $0.06.

"Our Q2 performance demonstrates solid execution in a fluid environment," said Emerson in its presentation. "We’re seeing sustained momentum in process and hybrid markets with discrete recovery, while demand for industrial software remains strong."

The company achieved an adjusted segment EBITA margin of 28.0%, representing a 200 basis point improvement year-over-year and significantly above the February guidance of approximately 26.5%. Operating leverage was impressive at 180%.

As shown in the following performance summary chart:

Free cash flow grew 14% to $738 million, representing a robust 17% of sales. This improvement was driven by operational excellence and disciplined working capital management.

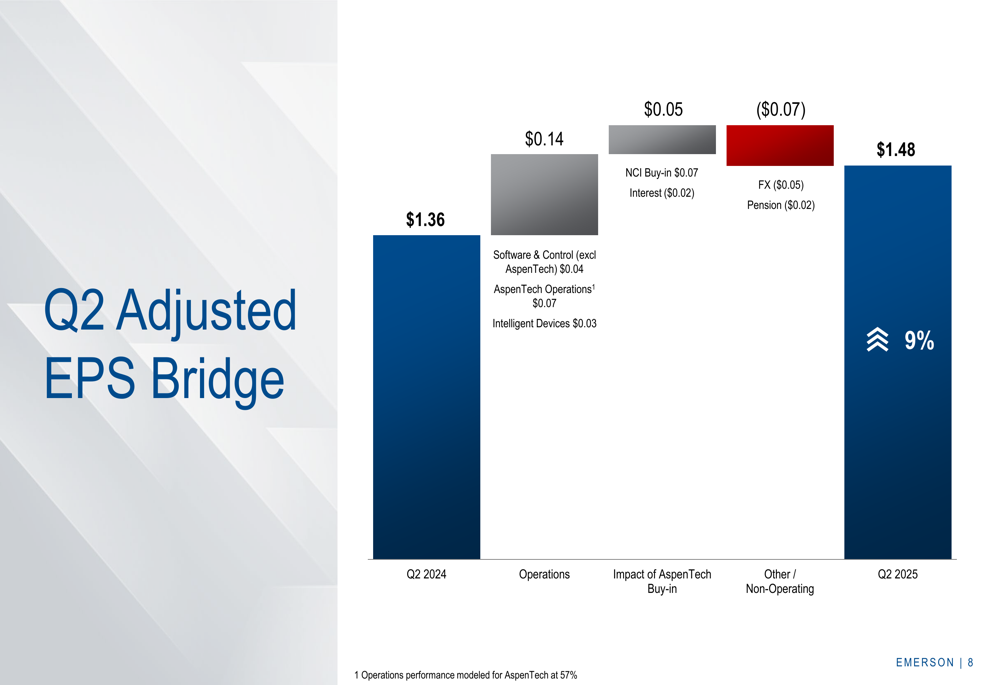

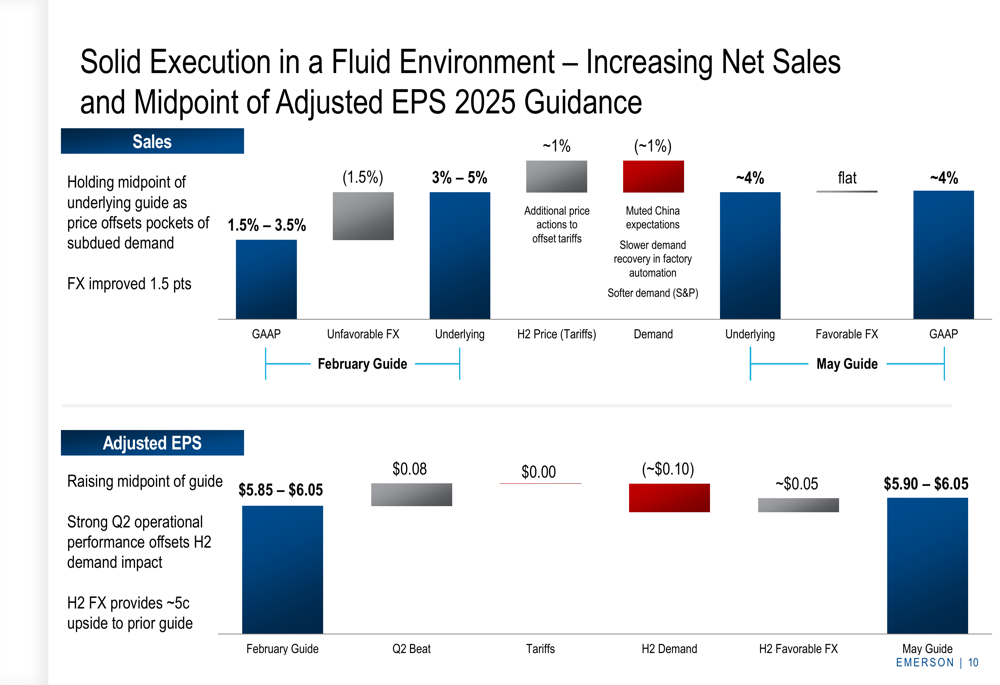

The adjusted EPS bridge below illustrates the key drivers of the 9% year-over-year earnings growth:

Strategic Initiatives and Tariff Mitigation

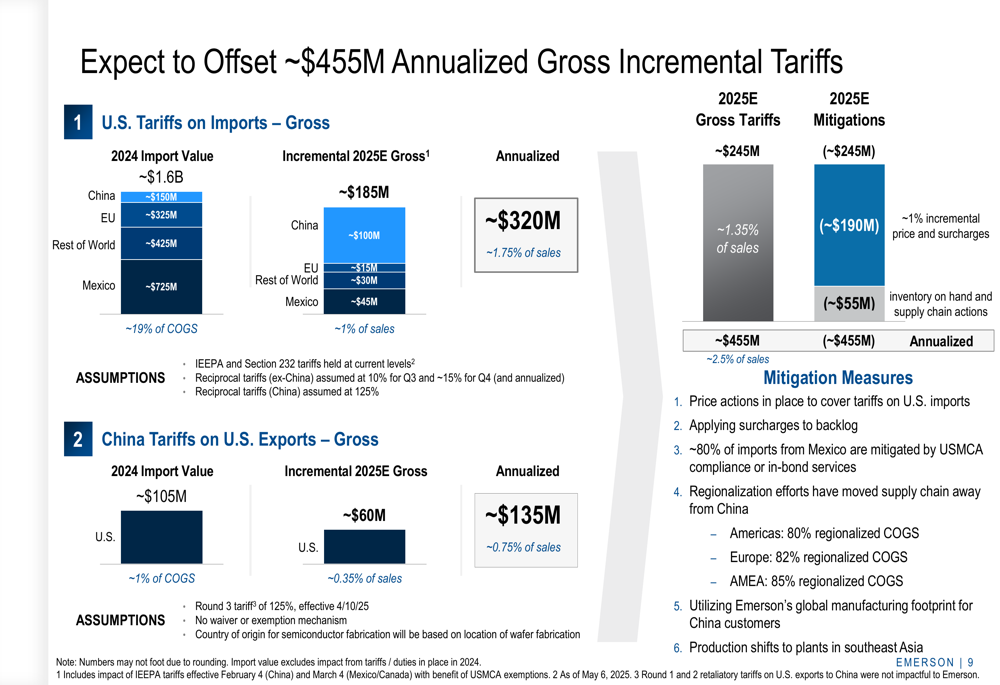

A significant focus of Emerson’s presentation was its comprehensive strategy to offset approximately $455 million in annualized gross incremental tariffs. The company faces tariff pressures from both U.S. tariffs on imports and Chinese tariffs on U.S. exports.

The following chart details Emerson’s tariff exposure and mitigation plans:

For 2025, Emerson expects gross tariff impacts of approximately $245 million but plans to fully mitigate this through a combination of 1% incremental price increases and surcharges ($190 million) along with inventory management and supply chain actions ($55 million).

On the portfolio front, Emerson announced the completion of its transformation with the closing of the AspenTech acquisition, which is expected to be modestly accretive to 2025 adjusted EPS. The company is targeting $100 million in cost synergies by 2028.

"We’ve fully integrated Test & Measurement and completed all actions to achieve a run-rate of $200 million in cost synergies," Emerson noted. The company also determined that retaining its Safety & Productivity business represents the best value for shareholders, concluding a strategic review process.

Market Outlook and Business Trends

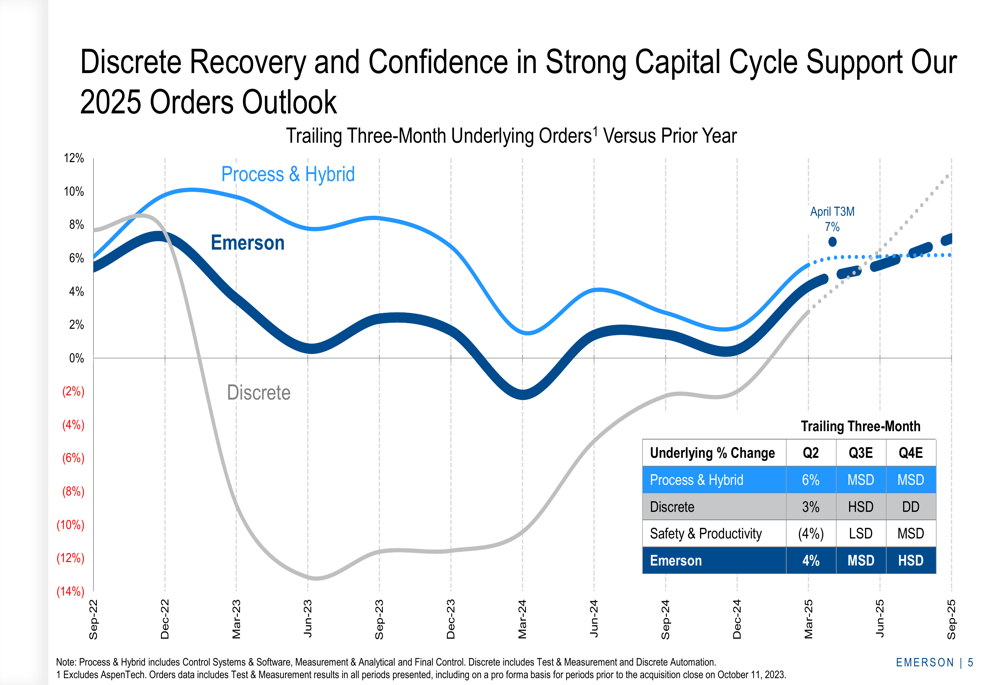

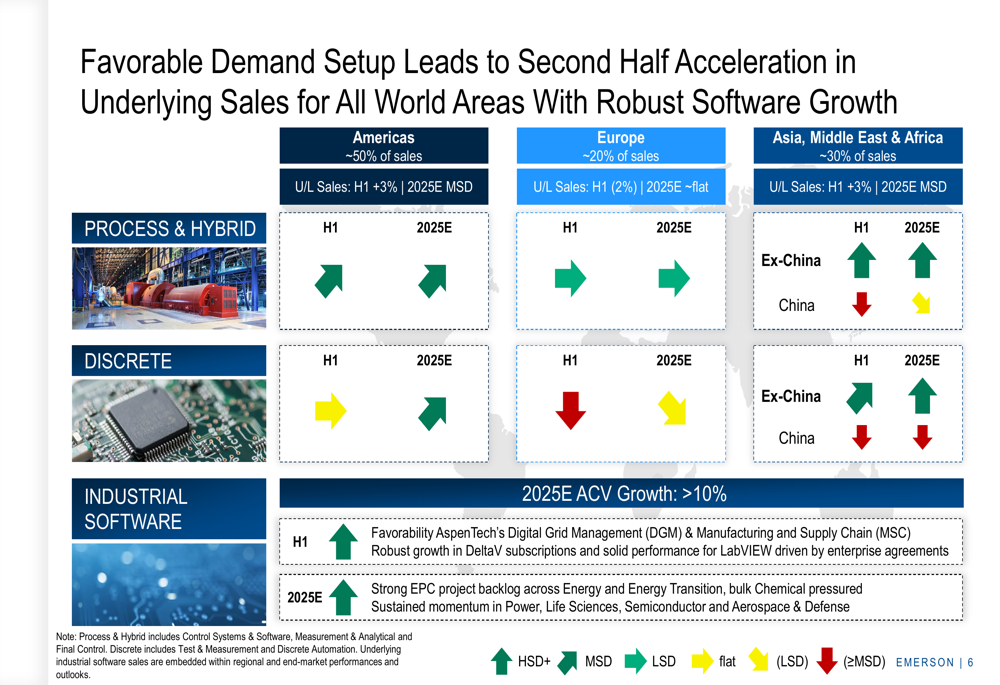

Emerson highlighted a favorable demand environment across its key markets, with particular strength in process and hybrid segments, which grew 6% in the quarter. The discrete business showed encouraging signs of recovery with 3% growth, while Test & Measurement orders turned positive with 8% growth.

The following chart illustrates the discrete recovery trend and confidence in a strong capital cycle:

Regional performance varied, with the Americas showing mid-single-digit growth, Europe remaining flat, and Asia, Middle East & Africa delivering mid-single-digit growth. The company noted particularly favorable conditions in AspenTech’s Digital Grid Management and Manufacturing and Supply Chain segments, robust growth in DeltaV subscriptions, and solid performance for LabVIEW.

The global demand outlook is illustrated in this regional breakdown:

"We’re seeing a strong EPC project backlog across Energy and Energy Transition," Emerson added, highlighting the continued momentum in its core markets despite macroeconomic uncertainties.

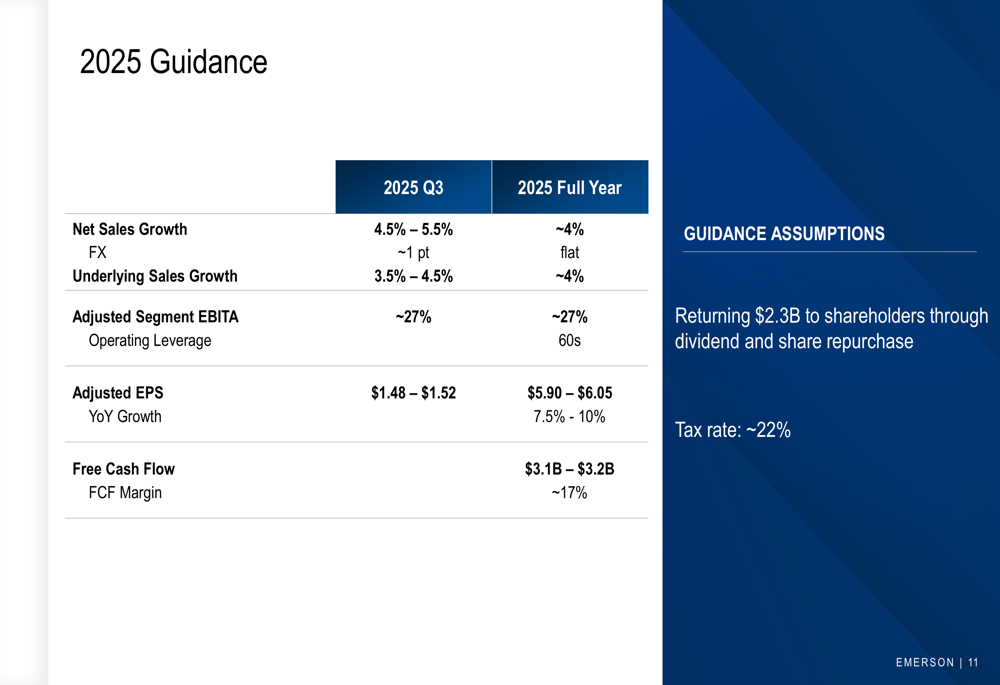

Updated 2025 Guidance

Based on its strong first-half performance and improving market conditions, Emerson raised its full-year guidance. The company now expects:

The updated guidance reflects Emerson’s confidence in its ability to execute in a challenging environment while successfully mitigating tariff impacts. The company is maintaining its commitment to return $2.3 billion to shareholders through dividends and share repurchases in fiscal 2025.

The following chart shows how Emerson adjusted its outlook to account for various factors:

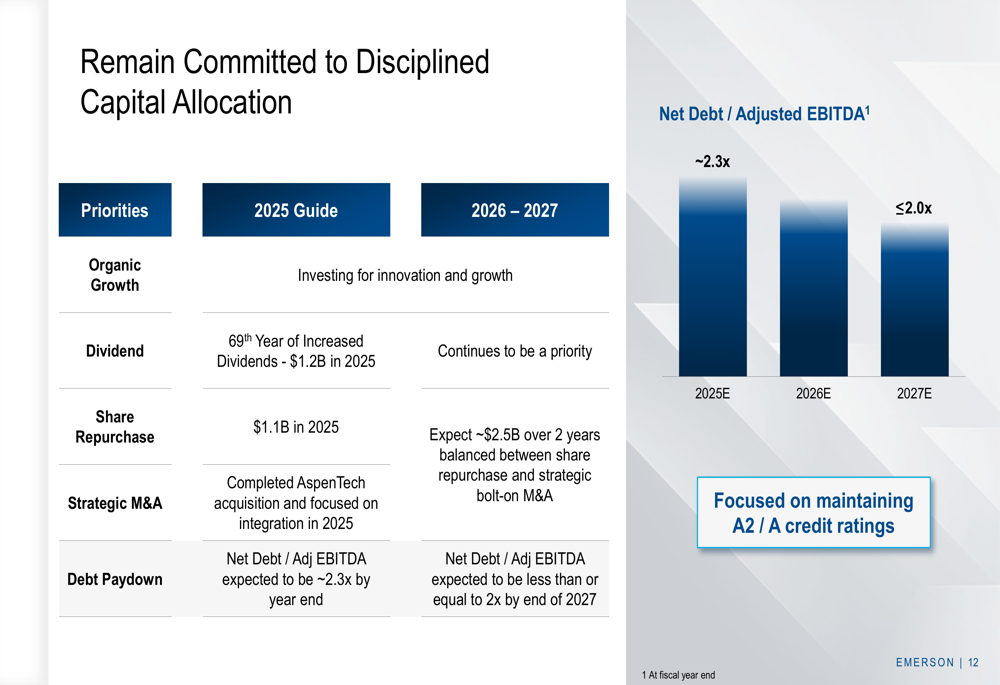

Capital Allocation Strategy

Emerson remains committed to disciplined capital allocation, with a focus on balancing growth investments, shareholder returns, and debt reduction. The company expects to repurchase $1.1 billion in shares during 2025 and approximately $2.5 billion over two years.

"Net Debt to Adjusted EBITDA is expected to be approximately 2.3x by year-end 2025, improving to 2.0x or better by the end of 2027," Emerson stated, underscoring its commitment to maintaining strong investment-grade credit ratings.

The capital allocation priorities are illustrated in this chart:

In premarket trading following the results, Emerson shares were up 3% to $110.49, reflecting positive investor reception to the company’s performance and outlook.

Emerson’s Q2 results demonstrate the company’s ability to navigate a complex global environment while delivering on its strategic objectives. With its portfolio transformation complete, tariff mitigation strategies in place, and discrete markets showing signs of recovery, Emerson appears well-positioned to deliver on its raised full-year targets despite ongoing macroeconomic challenges.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.