Intel shares rise as Elon Musk touts potential Tesla chipmaking deal

Introduction & Market Context

Emerson Electric (NYSE:EMR) released its fourth quarter and full-year 2025 results on November 5, 2025, delivering a mixed performance that met earnings expectations but fell short on revenue. The industrial automation giant reported quarterly adjusted earnings per share of $1.62, matching analyst forecasts, while revenue came in at $4.86 billion, slightly below the expected $4.9 billion.

The market reaction was decidedly negative, with Emerson shares falling 6.57% in pre-market trading to $128.69, reflecting investor disappointment despite the company’s solid earnings performance and optimistic outlook for 2026.

Quarterly Performance Highlights

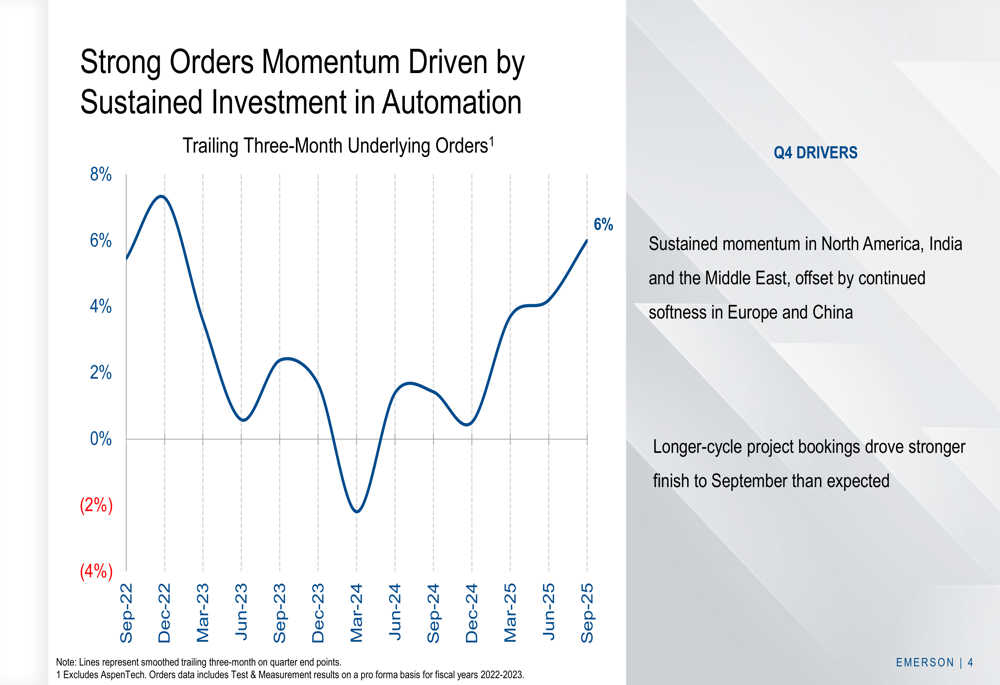

Emerson’s fourth quarter showed continued momentum in orders, with underlying orders growth of 6%, driven by strength in growth verticals, particularly Test & Measurement which surged 27%. The company reported underlying sales growth of 4% for the quarter, with adjusted segment EBITA margin expanding to 27.5%, an improvement of 1.3 percentage points year-over-year.

As shown in the following chart of orders momentum, Emerson has maintained a positive trajectory in recent quarters:

The quarterly performance reflected sustained strength in North America, India, and the Middle East, which helped offset continued softness in Europe and China. Longer-cycle project bookings contributed to a stronger-than-expected finish in September, providing some optimism heading into fiscal 2026.

Detailed Financial Analysis

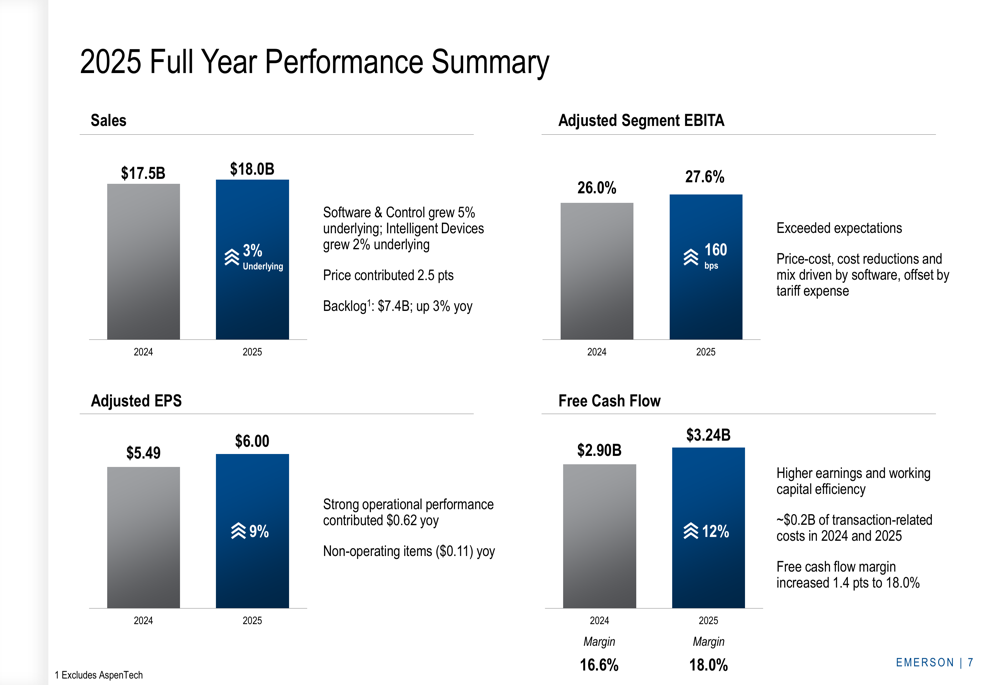

For the full fiscal year 2025, Emerson achieved underlying sales growth of 3%, which was at the lower end of its initial guidance range of 3-5%. The company’s Software & Control segment outperformed with 5% underlying growth, while Intelligent Devices grew at a more modest 2%. Price increases contributed approximately 2.5 percentage points to overall growth.

The following chart illustrates Emerson’s full-year 2025 performance across key metrics:

Emerson’s profitability metrics showed substantial improvement, with adjusted segment EBITA margin reaching 27.6%, up 160 basis points from 2024. This margin expansion was driven by favorable price-cost dynamics, cost reduction initiatives, and improved mix from higher software sales, partially offset by tariff expenses. The company achieved a record gross profit margin of 52.8% for the year.

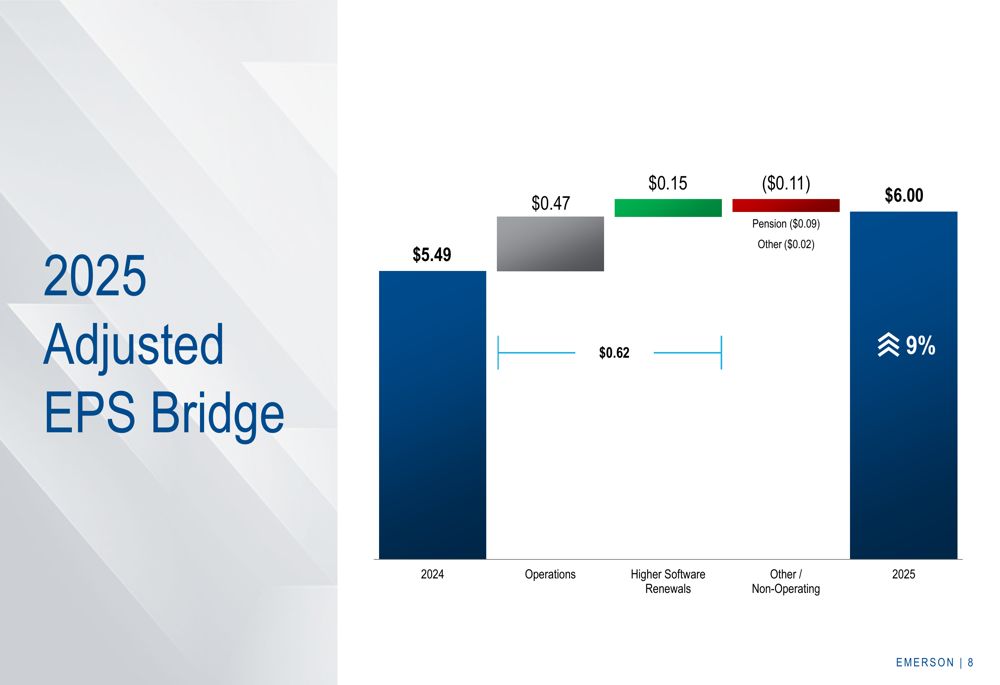

Adjusted earnings per share reached $6.00 for the full year, representing a 9% increase over 2024. As illustrated in the following bridge chart, this growth was primarily driven by operational improvements and higher software renewals:

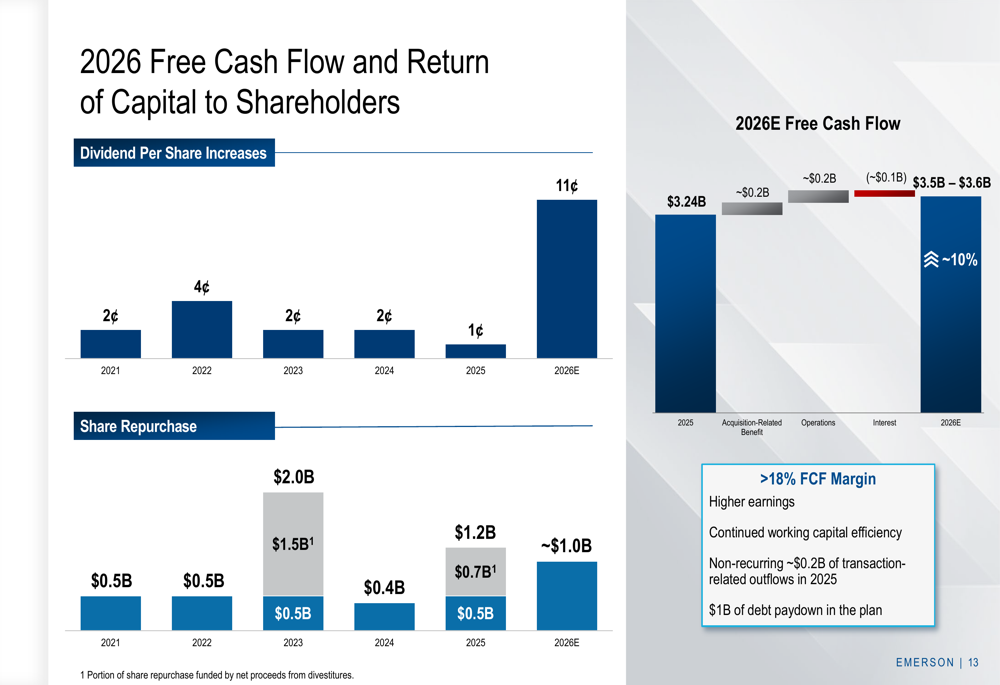

Free cash flow performance was particularly strong at $3.24 billion, up 12% year-over-year, with free cash flow margin improving by 1.4 percentage points to 18.0%. This improvement was attributed to higher earnings and enhanced working capital efficiency, despite approximately $0.2 billion in transaction-related costs.

Strategic Initiatives

Emerson continues to focus on high-growth verticals and accelerating innovation as key pillars of its strategy. The company highlighted its leading technology, domain knowledge, and application expertise in power, LNG, and life sciences sectors, while emphasizing ongoing development of AI-powered tools to enhance productivity and workflow automation.

The company’s strategic focus on growth verticals is illustrated in the following slide:

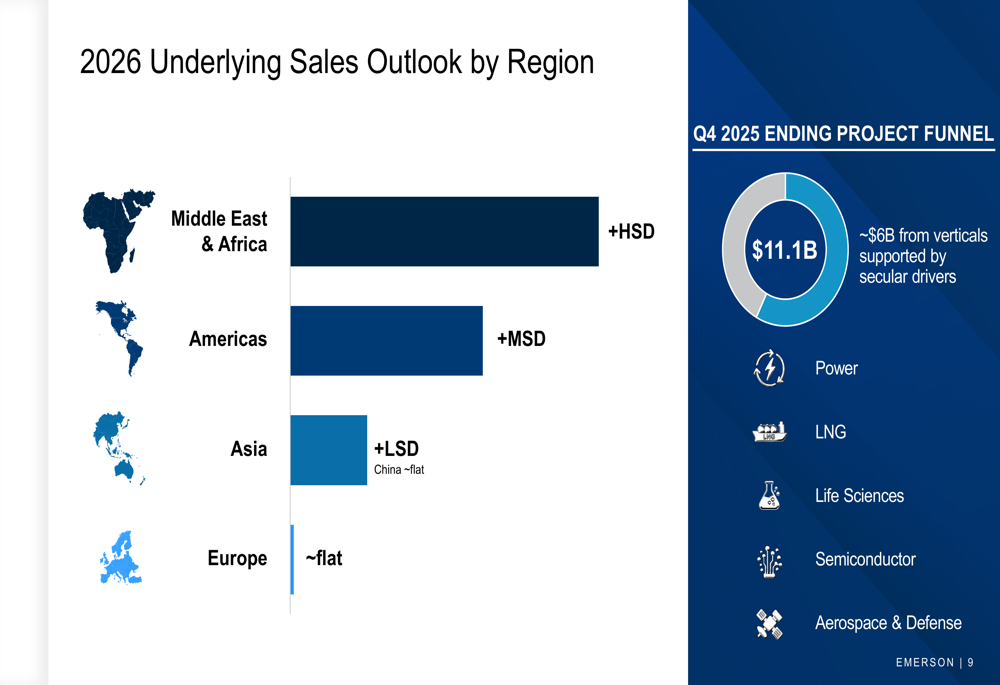

Emerson’s project funnel stood at $11.1 billion at the end of Q4 2025, with approximately $6 billion coming from verticals supported by secular growth drivers, including power, LNG, life sciences, semiconductor, and aerospace & defense sectors.

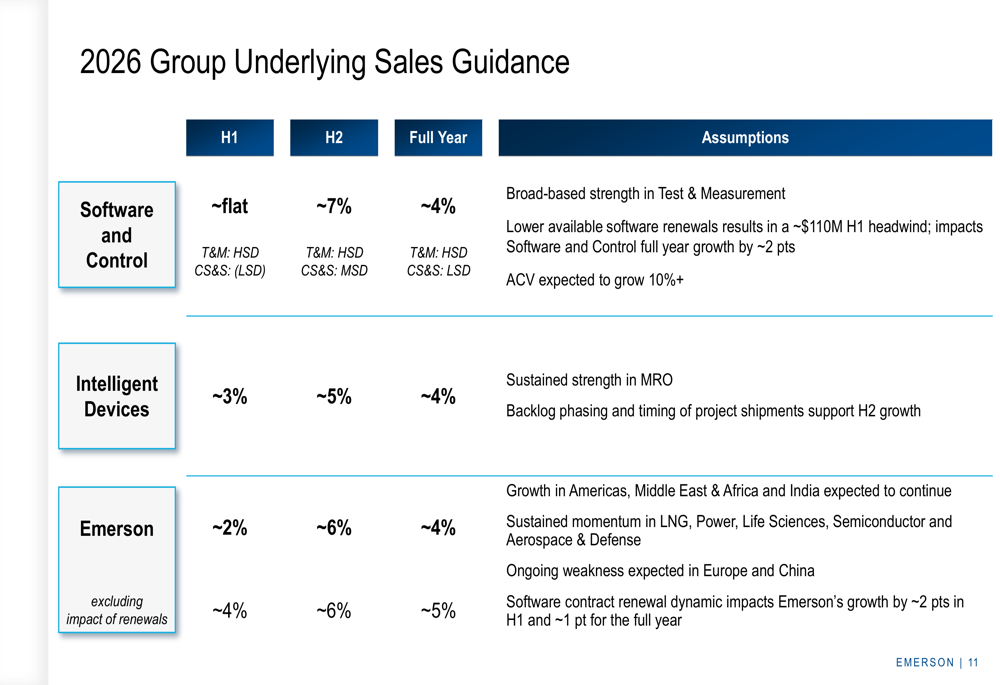

The company’s regional strategy reflects its focus on high-growth markets, with the strongest outlook for the Middle East & Africa (high single-digit growth) and Americas (mid single-digit growth), while Asia (excluding China) is expected to see low single-digit growth. Europe and China are projected to remain flat in 2026.

Forward-Looking Statements

Looking ahead to fiscal 2026, Emerson provided an optimistic outlook with total sales growth projected at approximately 5.5%, including underlying sales growth of around 4%. The company expects adjusted segment EBITA margin to reach approximately 28% and adjusted EPS to range between $6.35 and $6.55.

Emerson plans to return approximately $2.2 billion to shareholders in 2026 through a combination of dividends and share repurchases. This includes a planned 5% increase in dividend per share and approximately $1 billion in share repurchases.

The company’s shareholder return strategy is illustrated in the following chart, showing consistent dividend growth and increasing share repurchase activity:

For the first quarter of fiscal 2026, Emerson expects more modest growth with underlying sales increasing by approximately 2%, adjusted segment EBITA margin of around 27%, and adjusted EPS of approximately $1.40.

The company’s segment-level guidance for 2026 reflects a stronger second half, with both Software and Control and Intelligent Devices segments expected to accelerate growth as the year progresses:

While Emerson’s presentation paints an optimistic picture for 2026, investors appear concerned about the revenue miss in Q4 2025 and the ongoing challenges in Europe and China. The company’s ability to execute on its growth strategy in the face of these regional headwinds will be crucial for regaining investor confidence in the coming quarters.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.