Goldman Sachs chief credit strategist Lotfi Karoui departs after 18 years - Bloomberg

Introduction & Market Context

Italian air navigation service provider ENAV SpA (BIT:ENAV) presented its first half 2025 results on July 31, revealing a mixed financial performance characterized by strong traffic growth and cash generation despite declining revenue and profitability. The company raised its full-year guidance, citing operational excellence and efficiency initiatives as key drivers.

ENAV’s stock has shown resilience despite the mixed results, with shares currently trading at €4.42, up 1.67% in the most recent session. The stock has demonstrated positive momentum over recent months, delivering a 22.3% return over the past six months according to available market data.

Executive Summary

ENAV reported a 7.3% increase in en-route service units for H1 2025, exceeding its plan by 1.1 percentage points. However, total revenue declined to €447 million from €461 million in H1 2024, primarily due to regulatory balance adjustments. Despite this revenue dip, the company nearly doubled its free cash flow to €53.5 million compared to both Q1 2025 and H1 2024.

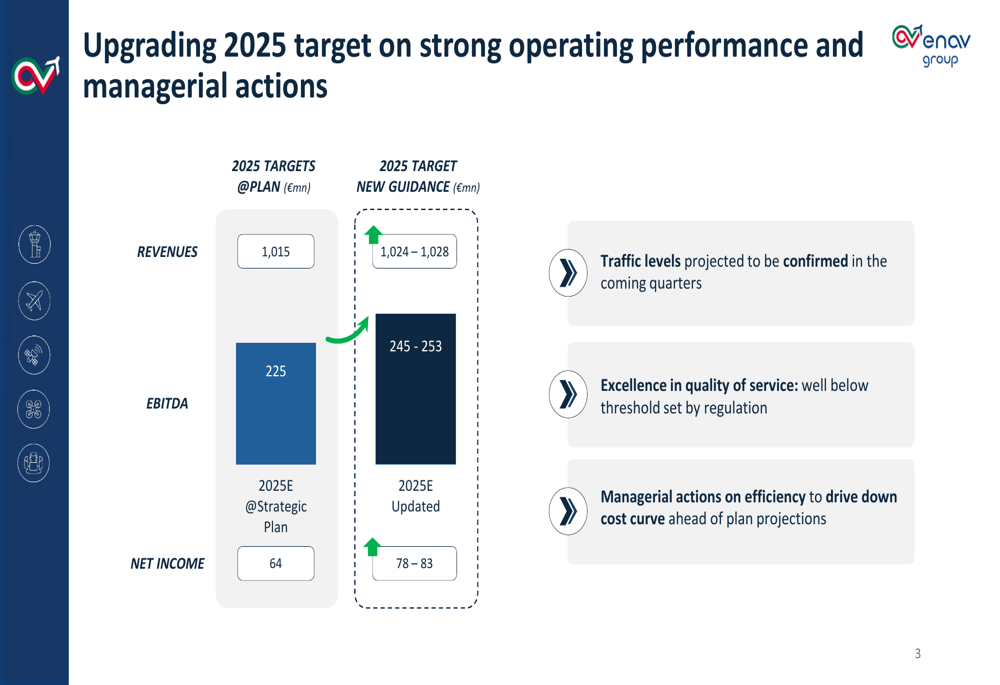

Based on strong operational performance and efficiency initiatives, ENAV upgraded its 2025 guidance, projecting revenues of €1,024-1,028 million (up from €1,015 million), EBITDA of €245-253 million (up from €225 million), and net income of €78-83 million (up from €64 million).

As shown in the following chart of the company’s upgraded 2025 targets:

Quarterly Performance Highlights

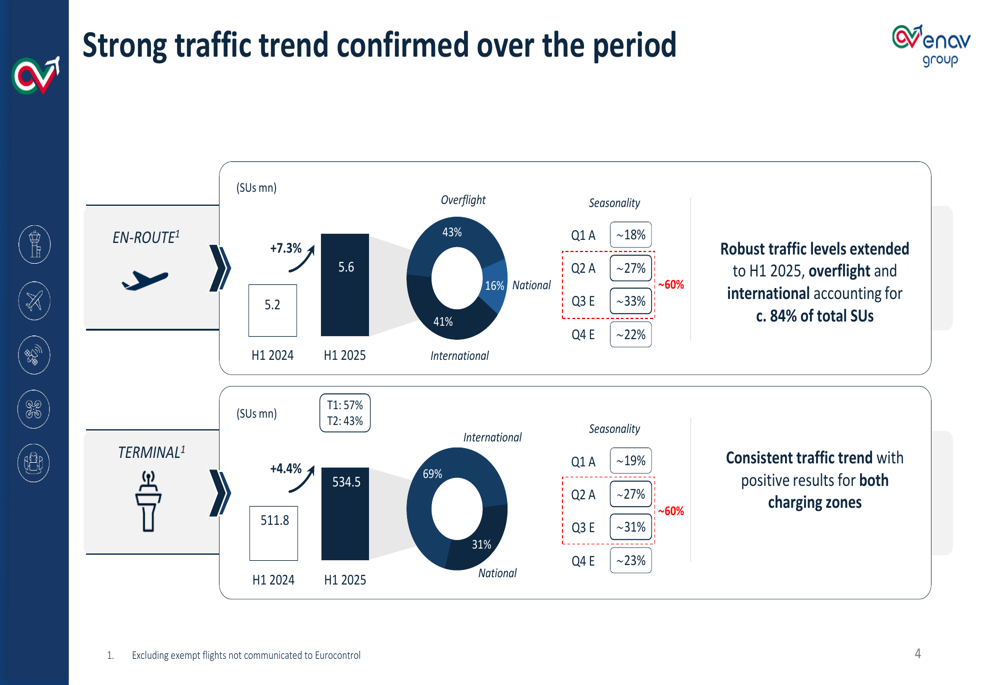

ENAV’s traffic performance remained robust in H1 2025, with en-route service units increasing by 7.3% to 5.6 million and terminal service units growing by 4.4% to 534.5 million compared to H1 2024. The traffic mix shows overflight and international traffic accounting for approximately 84% of total service units, highlighting ENAV’s strategic position in European airspace.

The following chart illustrates the traffic trend confirmation across both en-route and terminal services:

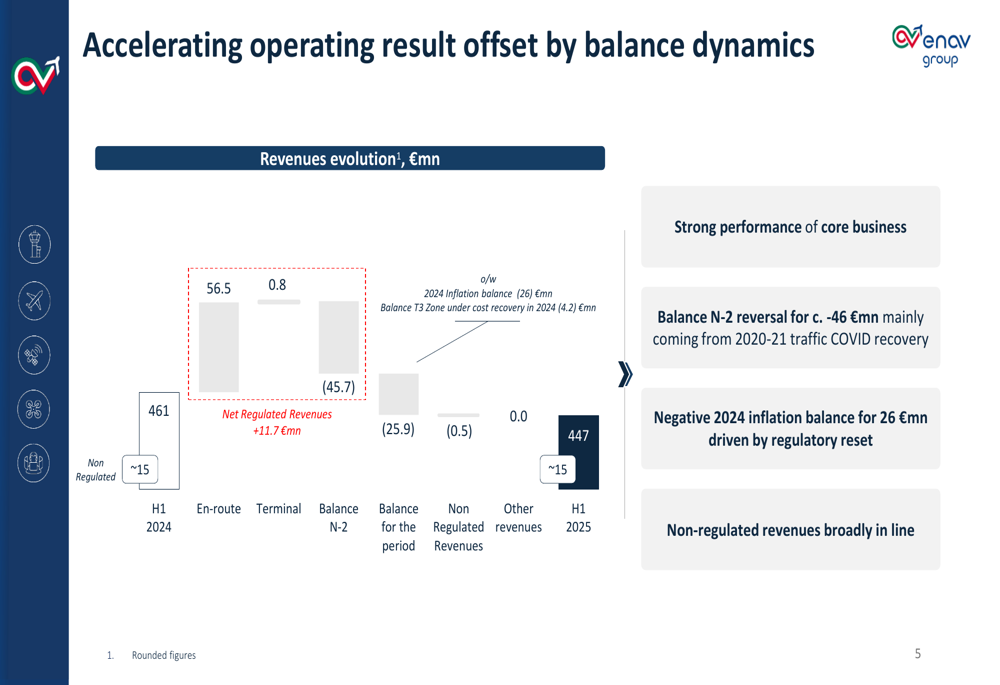

Despite strong traffic growth, ENAV’s revenue declined by €14 million year-over-year to €447 million. This decrease was primarily driven by a €45.7 million negative impact from balance N-2 reversal, mainly related to 2020-21 COVID traffic recovery, as well as a negative 2024 inflation balance of €26 million due to regulatory reset.

The following waterfall chart breaks down the operating result dynamics:

Detailed Financial Analysis

Operating costs increased by 4.5% year-over-year to €377.8 million. Personnel costs, which represent the majority of operating expenses, rose by 4.5% to €309.7 million due to contractual salary inflation adjustments and variable components linked to traffic volume. Other costs increased by 4.9% to €68.1 million, primarily due to higher utility expenses of €1.6 million.

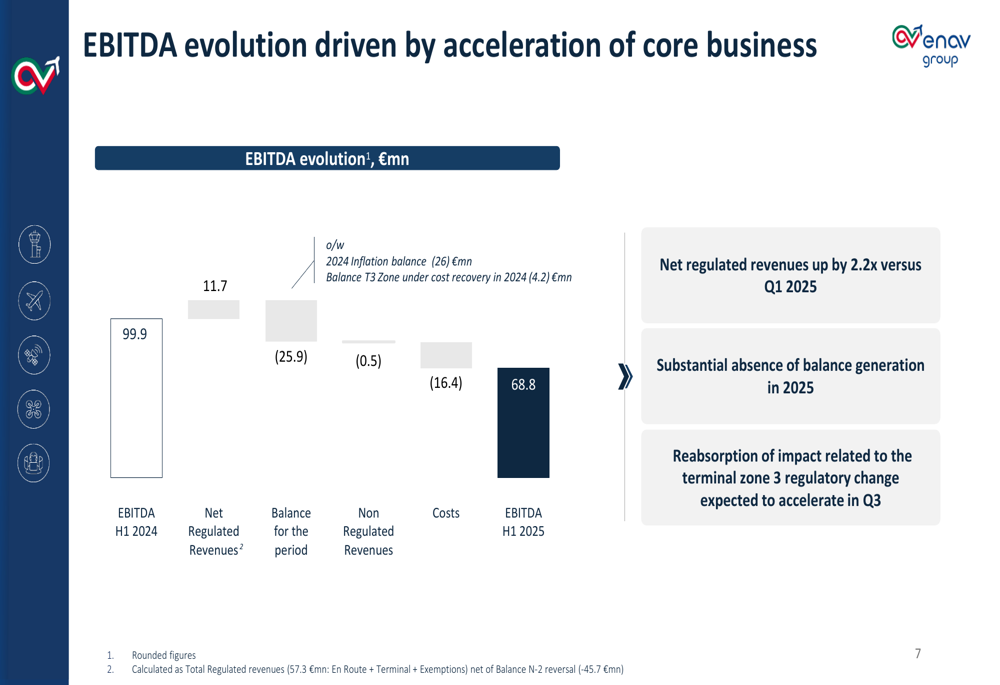

EBITDA decreased from €99.9 million in H1 2024 to €68.8 million in H1 2025, representing a 31.1% decline. This reduction was primarily due to the absence of balance generation in 2025 and the impact of regulatory changes in terminal zone 3, which the company expects to accelerate in Q3.

The following chart illustrates the EBITDA evolution from H1 2024 to H1 2025:

Net income fell by 69.6% to €7.0 million compared to €23.0 million in H1 2024, reflecting the lower EBITDA partially offset by a 9.8% decrease in depreciation, amortization, and provisions. Financial expenses remained stable at €4.5 million.

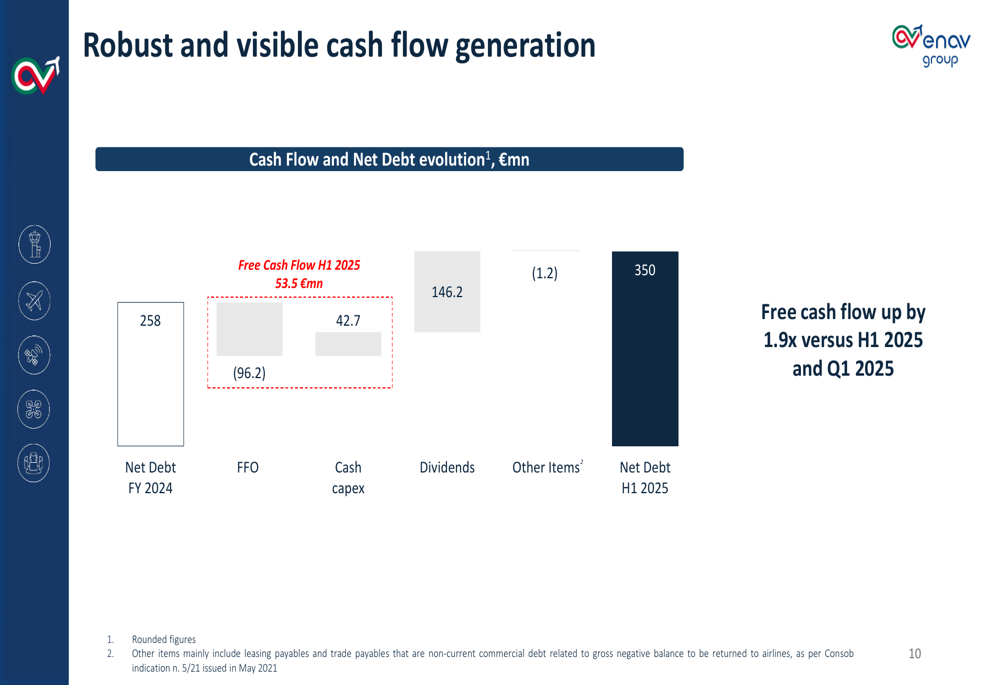

Despite the profit decline, ENAV’s free cash flow generation nearly doubled to €53.5 million, demonstrating the company’s focus on cash management efficiency. Net debt increased to €350 million, up from €258 million at the end of 2024, primarily due to dividend payments of €96.2 million.

The following chart details the cash flow generation and net debt evolution:

Forward-Looking Statements

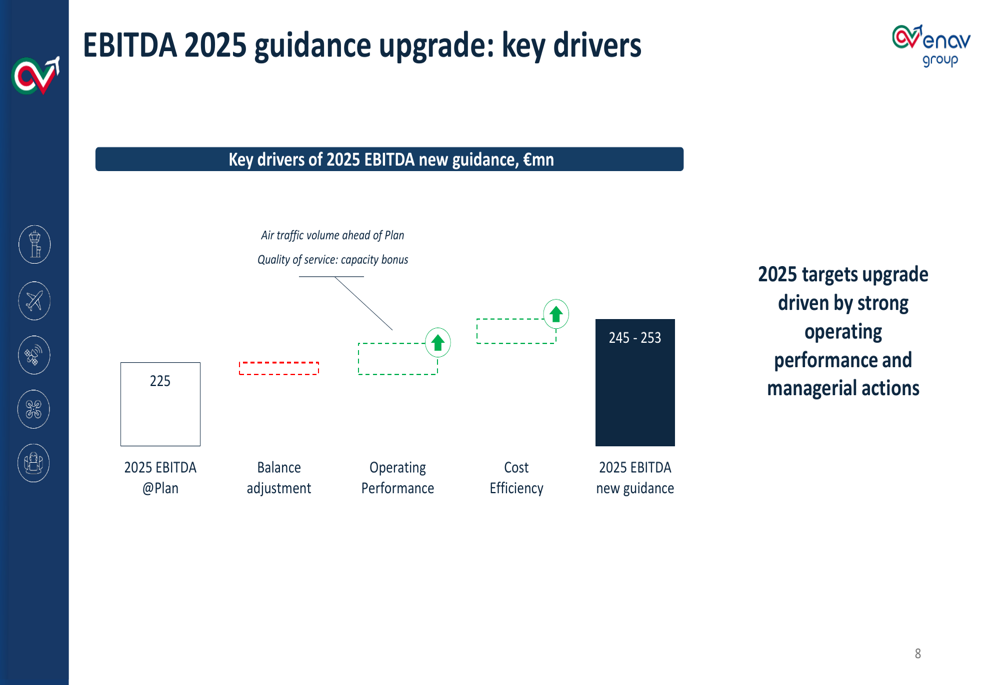

ENAV has upgraded its 2025 guidance based on two key drivers: air traffic volume exceeding plan and quality of service bonuses. The company now expects EBITDA to reach €245-253 million, a significant increase from the original target of €225 million.

The following chart outlines the drivers for the EBITDA 2025 guidance upgrade:

Management remains optimistic about future performance, emphasizing operational excellence in a record traffic environment, continued focus on efficiency to improve the cost curve, and strong cash flow generation. The company anticipates continued traffic growth and full performance bonuses of approximately €13 million for the year.

Market Reaction and Analyst Perspectives

Following the earnings announcement, ENAV’s stock initially declined by 2.53%, reflecting investor concerns over the revenue dip and increased net debt. However, the stock has since recovered, suggesting that investors have recognized the value in the company’s upgraded guidance and strong cash generation.

According to available market data, ENAV maintains a notable 6.8% dividend yield and has raised its dividend for four consecutive years, demonstrating strong shareholder returns despite market fluctuations. Analysis suggests the stock may be undervalued based on current fundamentals.

The company faces several challenges, including rising operating costs, particularly in personnel and energy, which could impact future profitability. Ongoing wage negotiations expected to conclude by year-end could also lead to increased labor costs. Additionally, the increased net debt position may constrain financial flexibility in the near term.

Nevertheless, ENAV’s upgraded guidance and strong operational performance in managing record traffic levels position the company favorably for the remainder of 2025, with management expressing confidence in continued efficiency improvements and strategic initiatives driving future growth.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.