Tyson Foods to close major Nebraska beef plant amid cattle shortage - WSJ

Enbridge Inc (NYSE:ENB) reported record second-quarter results with 7% adjusted EBITDA growth year-over-year, according to the company’s Q2 2025 presentation delivered on August 1. Management expressed confidence that Enbridge will finish 2025 in the upper end of its EBITDA guidance range while maintaining its status as a dividend aristocrat with 30 consecutive years of dividend increases.

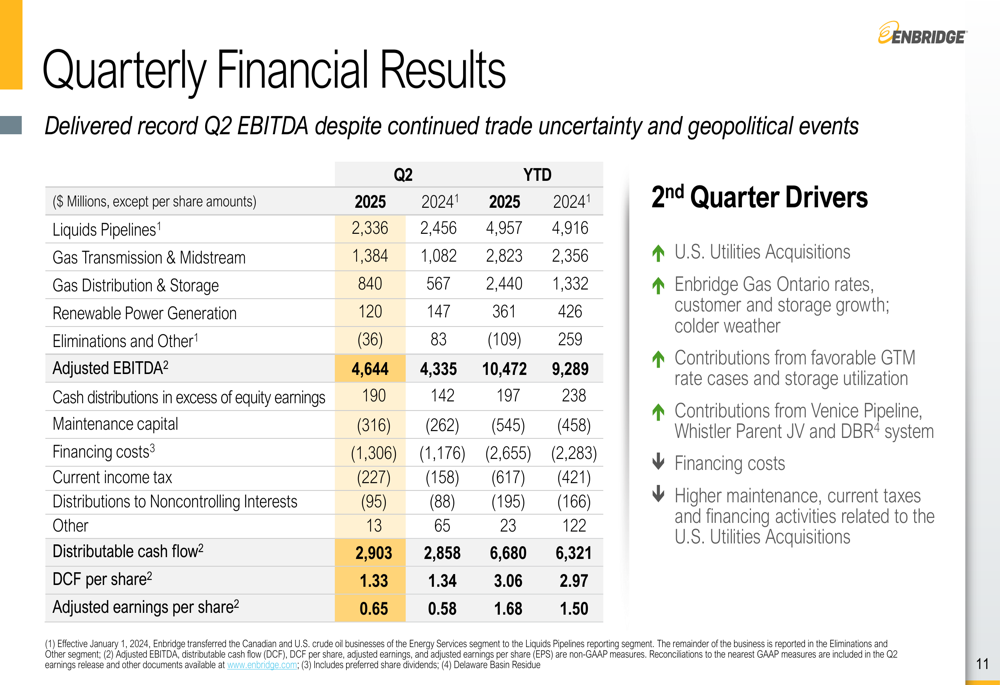

Quarterly Performance Highlights

Enbridge delivered strong financial results for Q2 2025, with adjusted EBITDA reaching $4,644 million, up from $4,335 million in Q2 2024, representing a 7% increase. Distributable cash flow (DCF) rose slightly to $2,903 million compared to $2,858 million in the prior year period. Adjusted earnings per share increased to $0.65 from $0.58 in Q2 2024, while DCF per share was $1.33, slightly down from $1.34 in the same quarter last year.

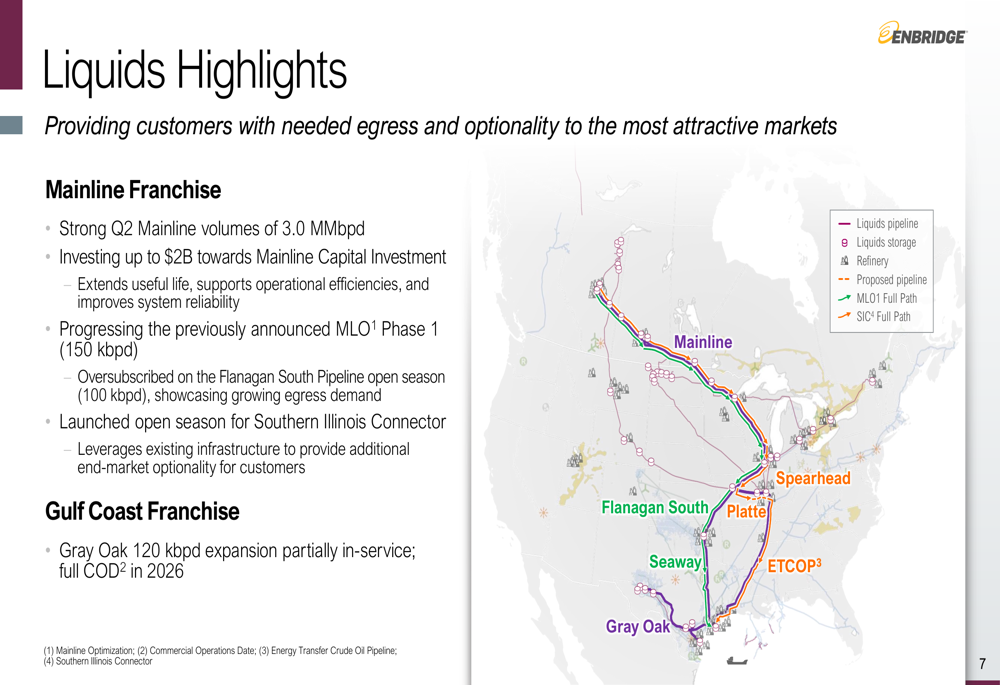

The company’s Mainline system reported solid volumes of 3.0 million barrels per day (MMbpd) during the quarter, though this represents a slight decline from the 3.2 MMbpd reported in Q1 2025.

As shown in the following quarterly financial results breakdown:

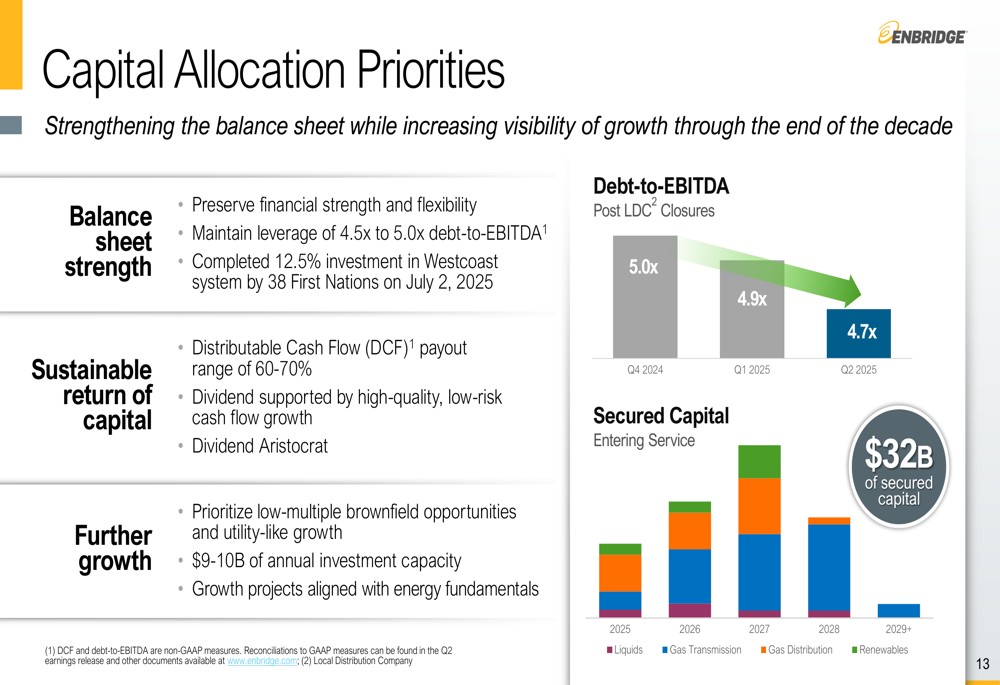

Enbridge has continued to strengthen its balance sheet, with its debt-to-EBITDA ratio improving to 4.7x in Q2 2025, down from 4.9x in Q1 2025 and 5.0x in Q4 2024. This places the company comfortably within its target leverage range of 4.5x to 5.0x.

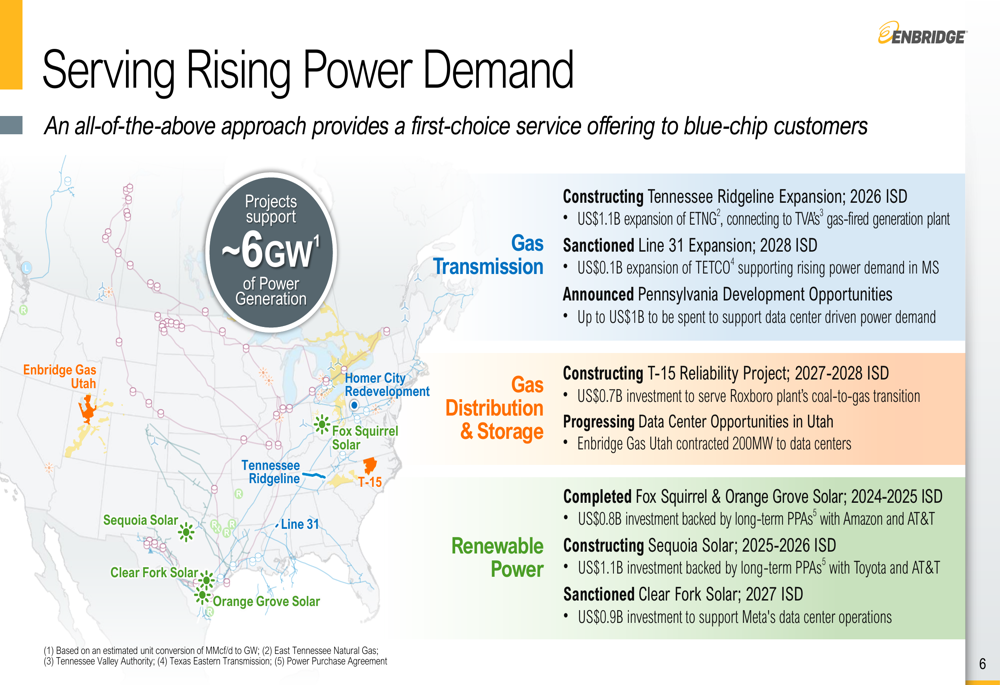

Strategic Initiatives & Growth Projects

A key focus of Enbridge’s strategy is positioning itself to meet rising power demand, particularly from data centers and AI applications. The company has sanctioned several new projects during the quarter, including Clear Fork Solar, Line 31 expansion on TETCO, and Aitken Creek Gas Storage expansion.

The company’s approach to serving rising power demand is illustrated in this comprehensive map of projects:

In the renewable power segment, Enbridge has sanctioned Clear Fork Solar, a 600 MW facility near San Antonio, Texas, supported by a long-term offtake agreement with Meta Platforms (NASDAQ:META) to support their data center operations. The $0.9 billion project is expected to be in service by 2027. The company is also progressing construction on Sequoia Solar, an 815 MW project west of Dallas, which is on track for partial service in 2025 and full operation in 2026.

On the gas transmission front, Enbridge has sanctioned a 160 MMcf/d TETCO Line 31 expansion to serve rising industrial and power demand in Mississippi. This $0.1 billion project is underpinned by 20-year agreements with investment-grade customers and is expected to enter service in 2028.

The company also highlighted its liquids business, focusing on its Mainline franchise and Gulf Coast operations:

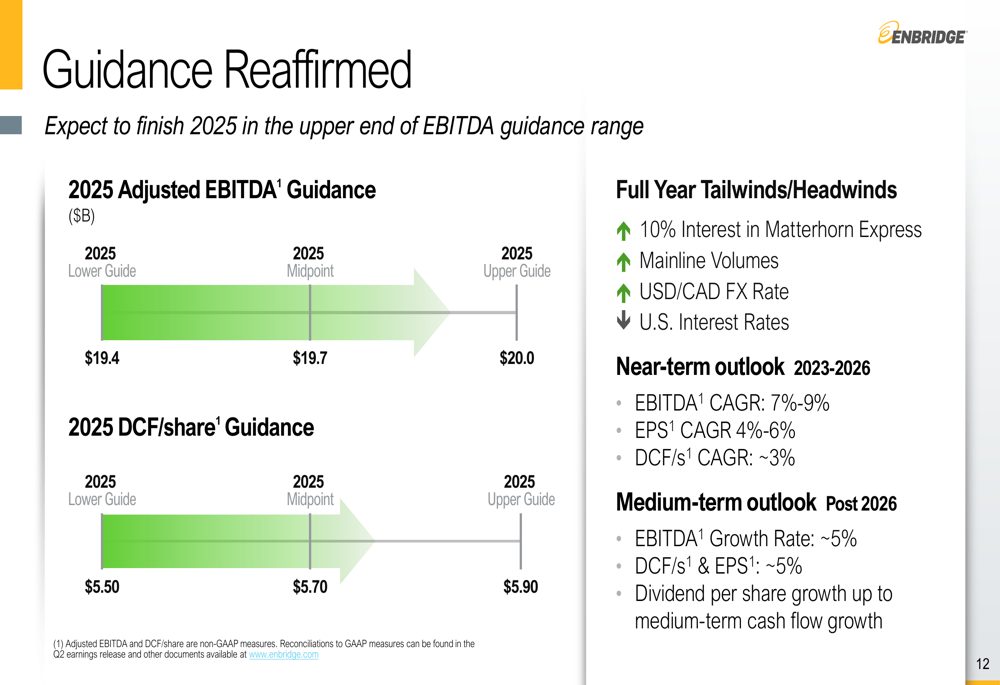

Financial Outlook & Guidance

Enbridge reaffirmed its financial guidance for 2025, with adjusted EBITDA expected to be between $19.4 billion and $20.0 billion, and DCF per share projected between $5.50 and $5.90. Management indicated they expect to finish 2025 in the upper end of the EBITDA guidance range and well on track to meet the mid-point for DCF.

The company’s guidance and outlook are summarized in the following chart:

For the near term (2023-2026), Enbridge projects an EBITDA compound annual growth rate (CAGR) of 7-9%, an EPS CAGR of 4-6%, and a DCF per share CAGR of approximately 3%. In the medium term (post-2026), the company expects growth rates of approximately 5% for EBITDA, DCF per share, and EPS.

Capital Allocation Strategy

Enbridge’s capital allocation priorities remain focused on maintaining balance sheet strength, providing sustainable returns to shareholders, and funding further growth. The company completed a 12.5% investment in the Westcoast system by 38 First Nations groups on July 2, 2025, and closed a 10% acquisition of Matterhorn Express Pipeline.

The company’s capital allocation approach is detailed in this chart showing secured capital entering service through 2029 and beyond:

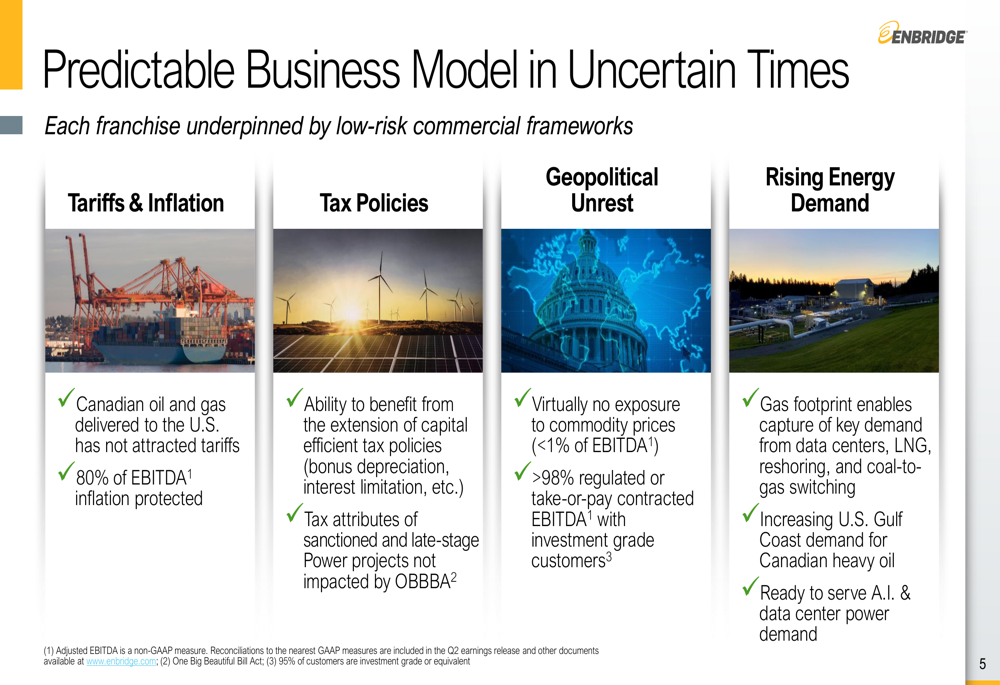

Enbridge emphasized its resilience through various economic conditions, noting that 80% of its EBITDA is inflation-protected and more than 98% is regulated or covered by take-or-pay contracts with investment-grade customers. The company has virtually no exposure to commodity prices, with less than 1% of EBITDA affected.

This business model resilience is illustrated in the following slide:

Despite the positive quarterly results, Enbridge’s stock was down slightly in pre-market trading on August 1, 2025, with a 0.22% decline to $45.19. The stock closed at $45.29 on July 31, 2025, representing a 0.69% increase for that trading day.

With its consistent performance and strategic positioning across multiple energy segments, Enbridge continues to present itself as a "first-choice investment" with a low-risk, utility-like business profile and predictable cash flows, targeting approximately 5% growth through the end of the decade.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.