Gold prices just lower; monthly gains on track

Introduction & Market Context

Encore Capital Group (NASDAQ:ECPG) delivered a strong first quarter performance for 2025, capitalizing on favorable market conditions in the United States where credit card charge-off rates have reached their highest levels in over a decade. The debt collection specialist’s investor presentation, released on May 7, 2025, highlighted significant growth in portfolio purchases, collections, and profitability compared to the same period last year.

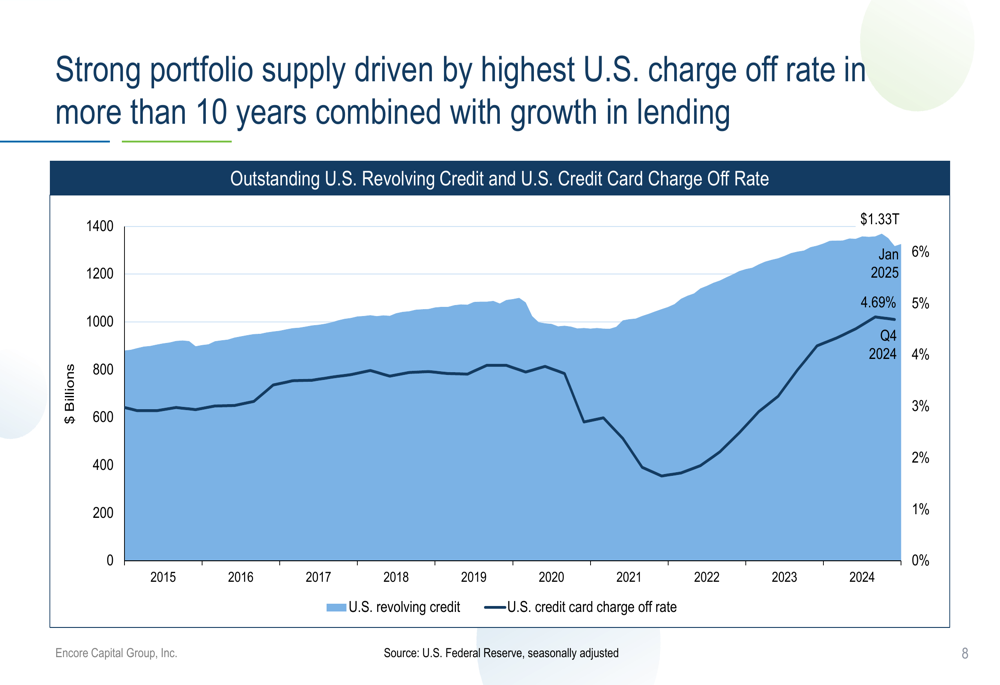

The company’s strategic focus on the U.S. market has paid dividends as consumer credit delinquencies remain elevated and credit card debt continues to grow. U.S. revolving credit reached $1.33 trillion in January 2025, while the credit card charge-off rate climbed to 6% in the same month, creating a robust supply of non-performing loans for Encore to purchase.

As shown in the following chart illustrating the relationship between outstanding U.S. revolving credit and charge-off rates:

Quarterly Performance Highlights

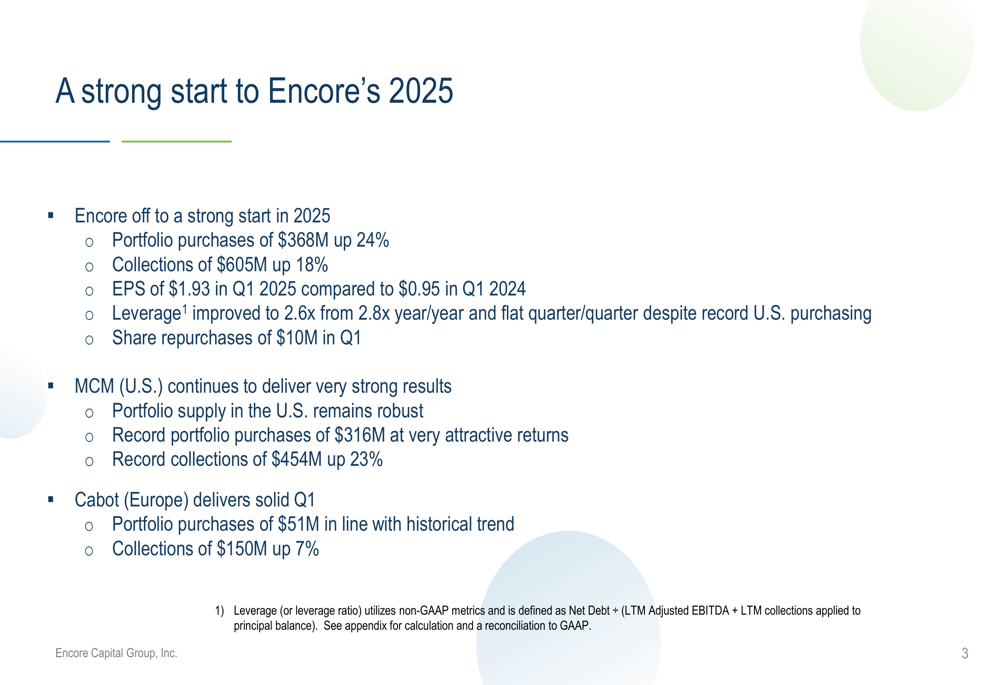

Encore Capital reported exceptional first-quarter results, with earnings per share of $1.93, more than doubling the $0.95 reported in Q1 2024 and significantly exceeding analyst expectations of $1.45. This 103% year-over-year increase in EPS was driven by strong performance across key operational metrics.

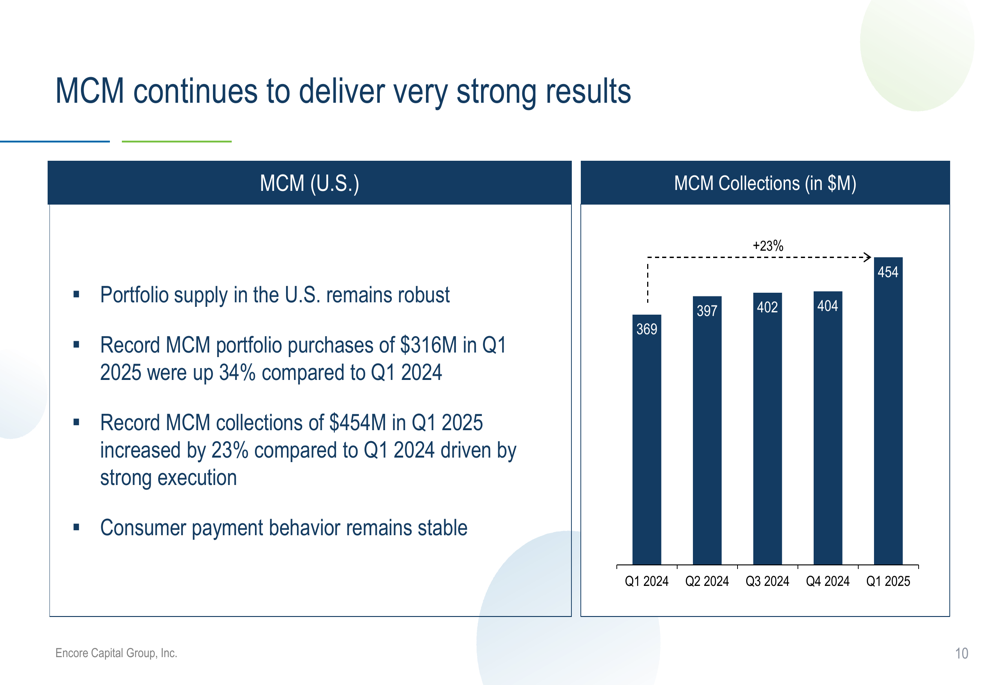

The company’s portfolio purchases increased by 24% to $368 million, while collections grew by 18% to $605 million compared to the same period last year. Notably, the U.S. business (MCM) delivered record portfolio purchases of $316 million, up 34% year-over-year, and record collections of $454 million, representing a 23% increase from Q1 2024.

The following slide summarizes Encore’s strong start to 2025:

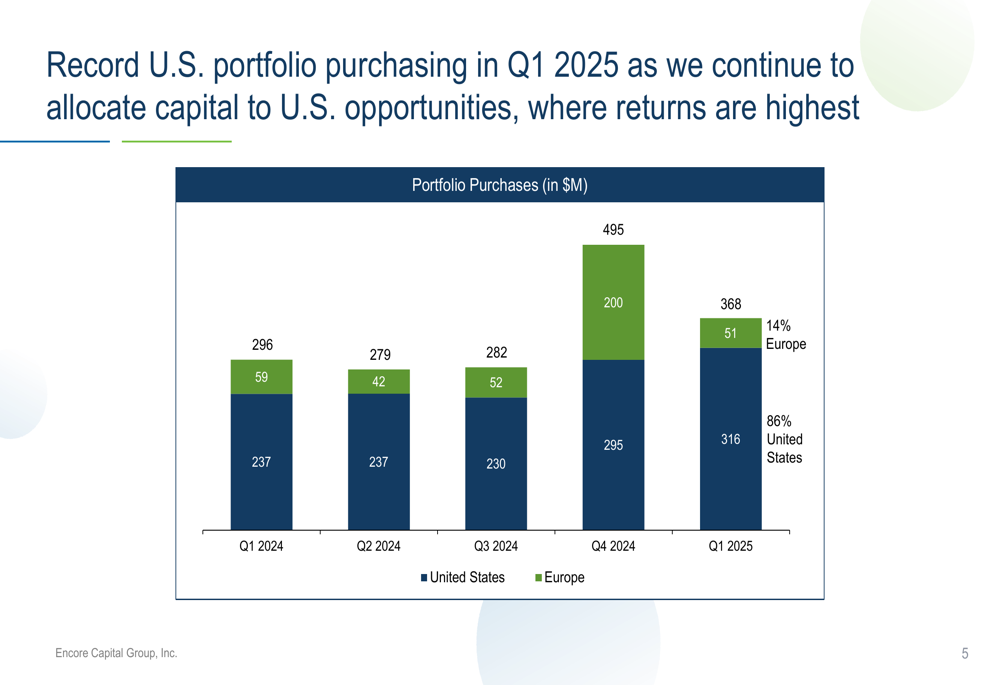

The company’s strategic shift toward the U.S. market is evident in its portfolio purchasing allocation, with 86% of Q1 2025 purchases concentrated in the United States. This represents a significant increase from previous quarters and reflects management’s view of the attractive opportunities in the U.S. market.

The following chart shows the trend in portfolio purchases by geography:

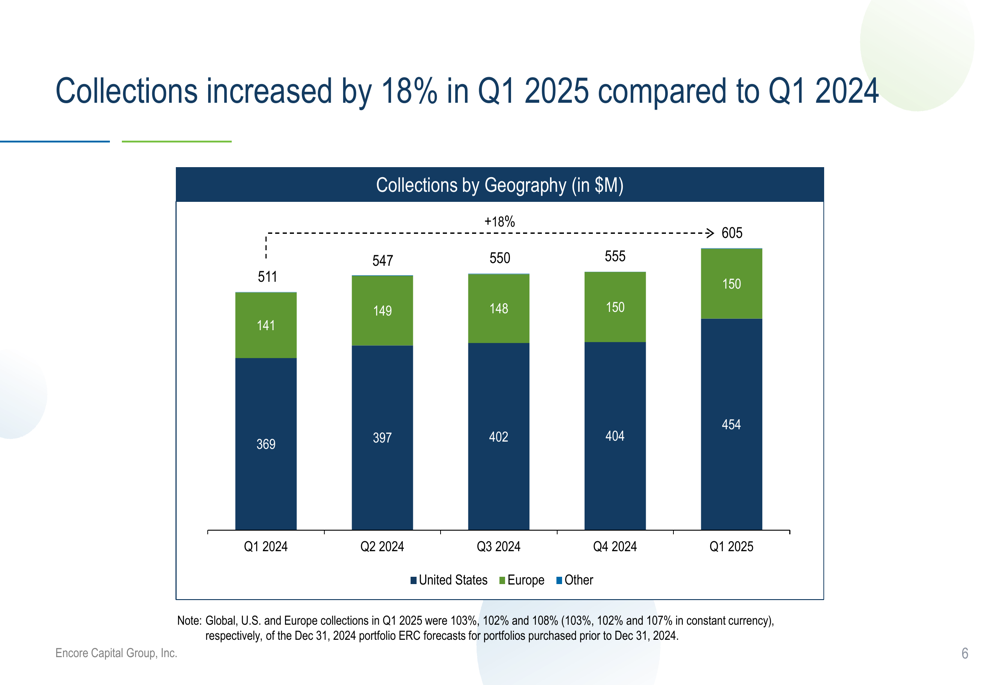

Collections performance also showed strong growth, particularly in the U.S. market. Global collections increased by 18% year-over-year to $605 million, with U.S. collections growing by 23% to $454 million and European collections increasing by 7% to $150 million.

As illustrated in this collections breakdown by geography:

Detailed Financial Analysis

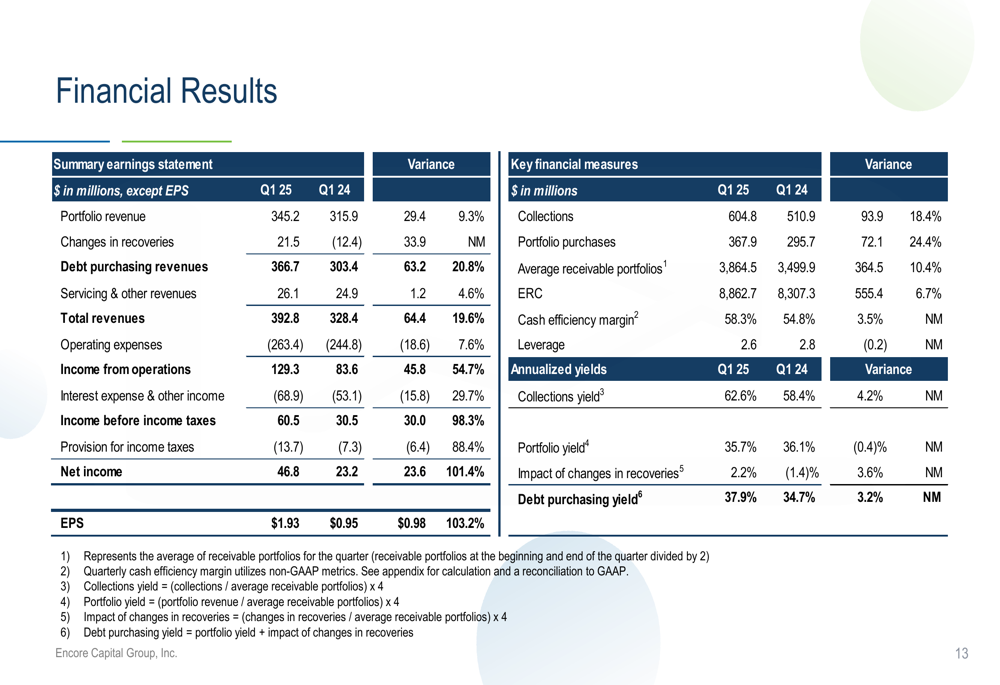

Encore Capital’s financial results for Q1 2025 showed substantial improvement across multiple metrics. Total (EPA:TTEF) revenues increased by 19.6% to $392.8 million, driven by a 20.8% increase in debt purchasing revenues to $366.7 million. Income from operations surged by 54.7% to $129.3 million, while net income more than doubled to $46.8 million, representing a 101.4% increase compared to Q1 2024.

The company’s cash efficiency margin improved to 58.3% in Q1 2025 from 54.8% in the same period last year, indicating better operational efficiency. Leverage also improved to 2.6x from 2.8x year-over-year, reflecting a stronger balance sheet position.

The comprehensive financial results are detailed in the following table:

Cash generation, a key metric for Encore Capital, increased by 23% on a trailing twelve-month basis. This improvement was driven by higher collections and improved operational efficiency, providing the company with greater financial flexibility for portfolio purchases and capital allocation.

The company’s debt maturity profile remains favorable, with no significant maturities until 2027. Available liquidity stood at $544 million as of March 31, 2025, consisting of $379 million in available revolving credit facilities and $165 million in cash.

Strategic Initiatives and Market Position

Encore Capital continues to leverage its market-leading positions through its two primary operating units: MCM in the United States and Cabot (NYSE:CBT) in Europe. MCM, with over 25 years of operational experience, is benefiting from robust portfolio supply in the U.S. market due to high credit card delinquency and charge-off rates.

U.S. consumer credit card delinquency rates remain elevated across all categories (30+, 60+, and 90+ days past due), creating a favorable environment for debt purchasing. The company noted that consumer payment behavior remains stable despite these elevated delinquency rates.

The European business, operated through Cabot, delivered solid results with collections of $150 million in Q1 2025, up 7% from the previous year. However, the U.K. market remains challenged by subdued consumer lending, low delinquencies, and robust competition, leading to a more selective approach to portfolio purchases in Europe.

The following chart illustrates MCM’s strong collections performance:

Forward-Looking Statements

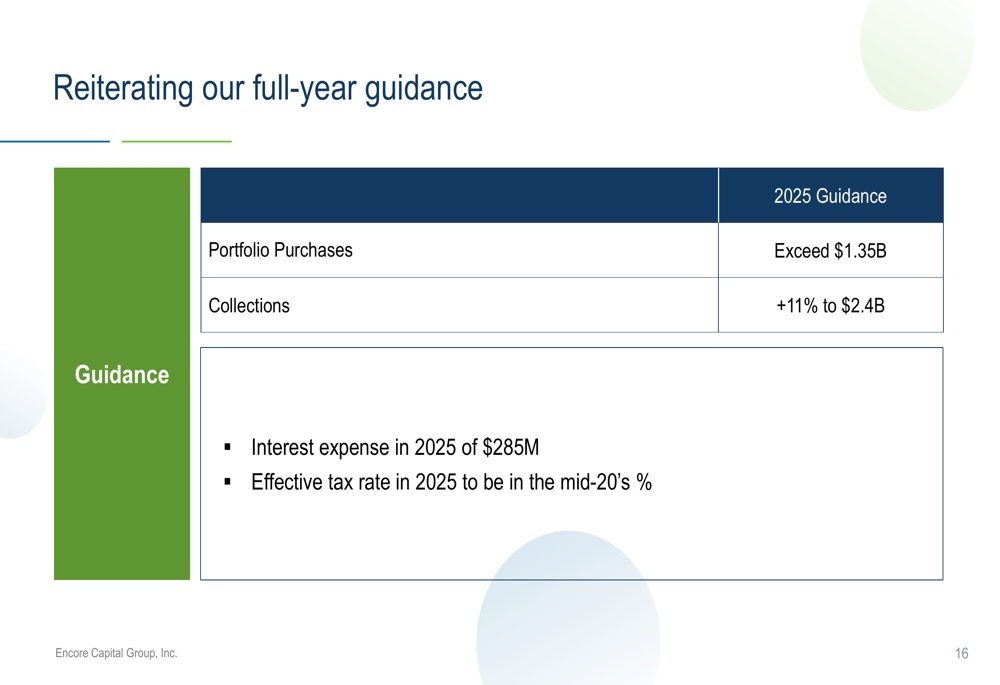

Encore Capital reiterated its full-year guidance for 2025, projecting portfolio purchases to exceed $1.35 billion and collections to grow by 11% to $2.4 billion. The company expects interest expense to be approximately $285 million for the year, with an effective tax rate in the mid-20% range.

Management’s capital allocation priorities remain focused on portfolio purchases at attractive returns, share repurchases, and strategic M&A opportunities. The company targets a leverage ratio between 2.0x and 3.0x, aiming to maintain a strong BB debt rating and preserve financial flexibility.

Following the earnings release, Encore Capital’s stock rose 3.28% in aftermarket trading to $34.00, reflecting investor optimism about the company’s strong performance and outlook. Despite this positive reaction, the stock remains well below its 52-week high of $51.77, suggesting potential upside if the company continues to deliver strong results.

The company’s full-year guidance is summarized in the following slide:

Encore Capital’s strong first-quarter performance, driven by record U.S. results and improved operational efficiency, positions the company well to capitalize on the favorable market conditions in the debt purchasing industry, particularly in the United States where high credit card delinquency rates are creating robust portfolio supply.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.